Beef Wrap August 18

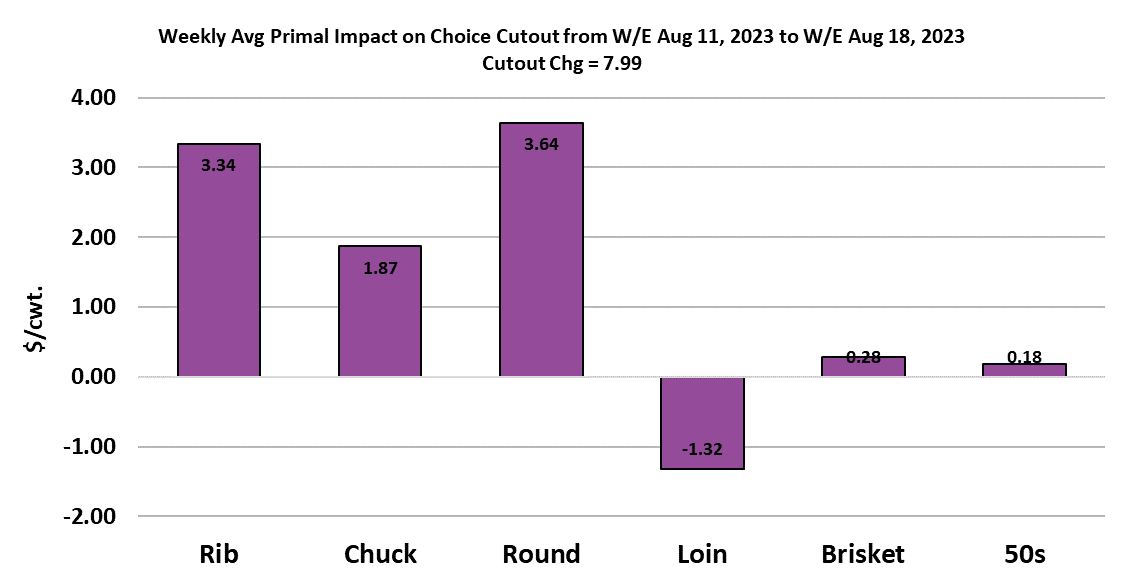

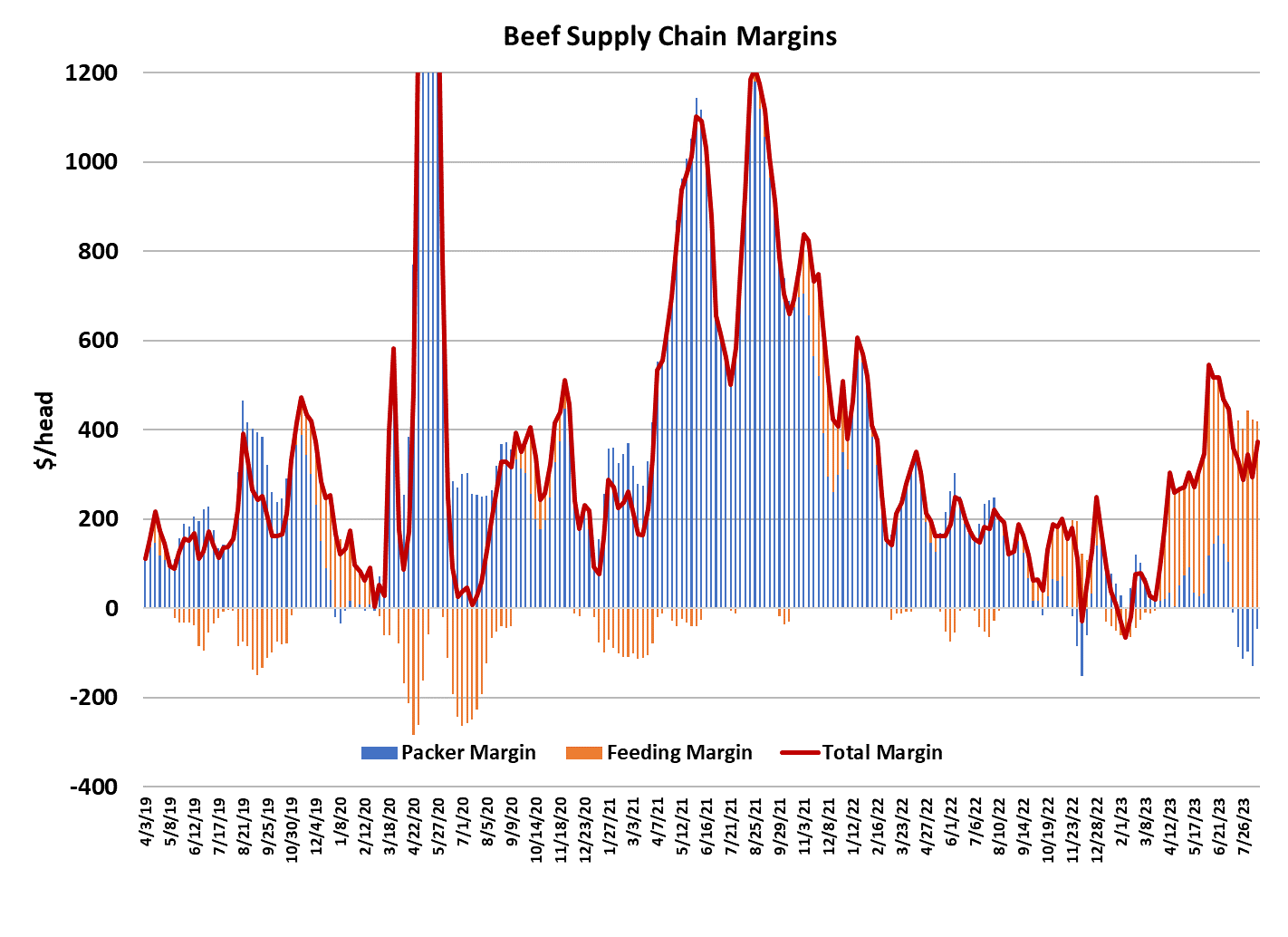

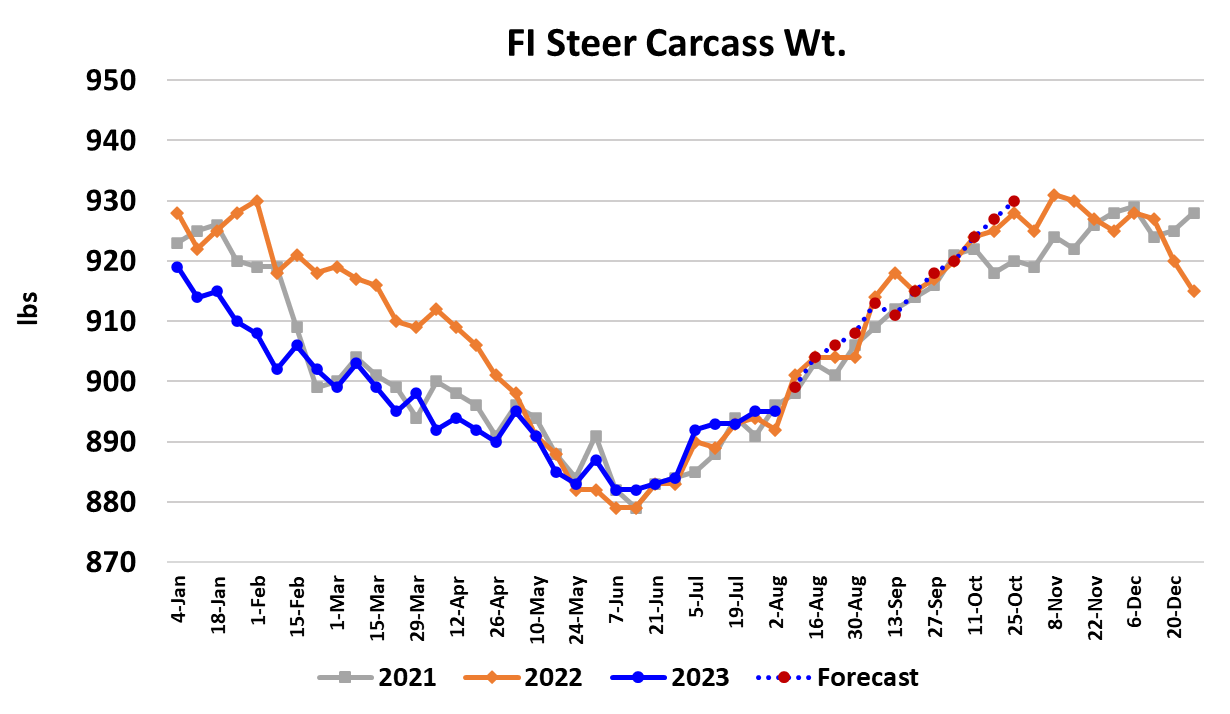

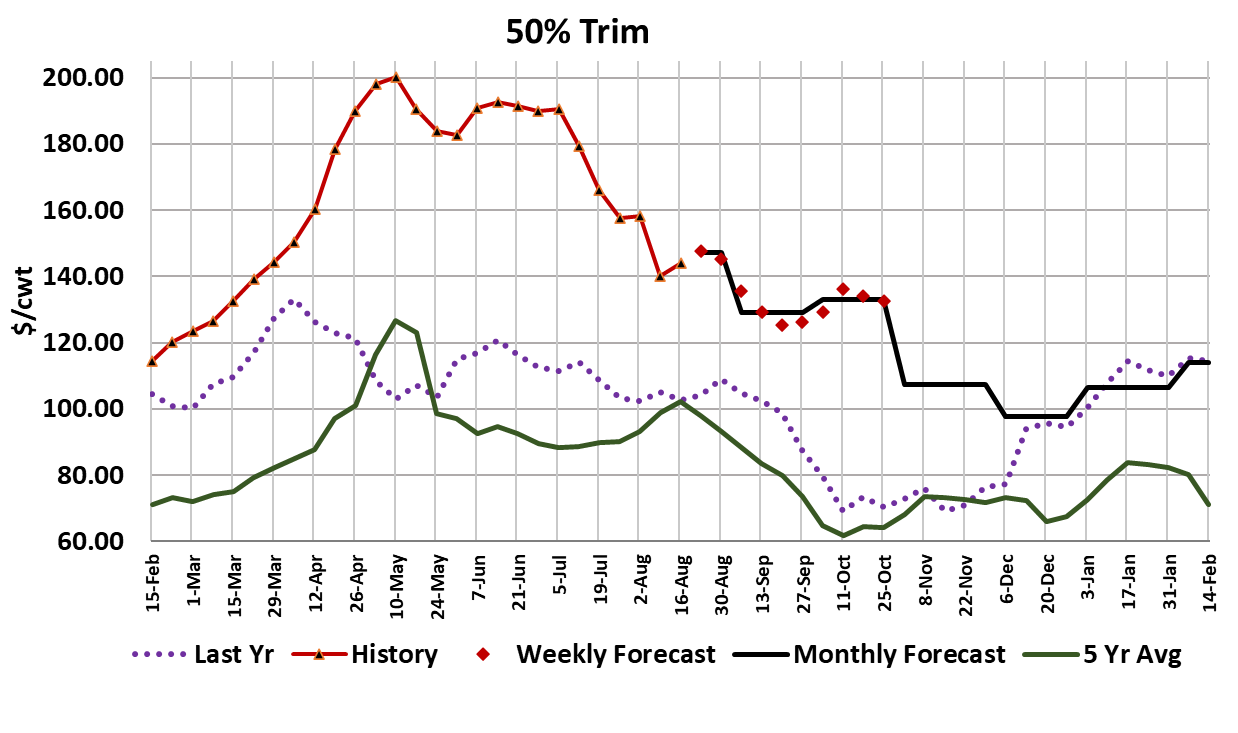

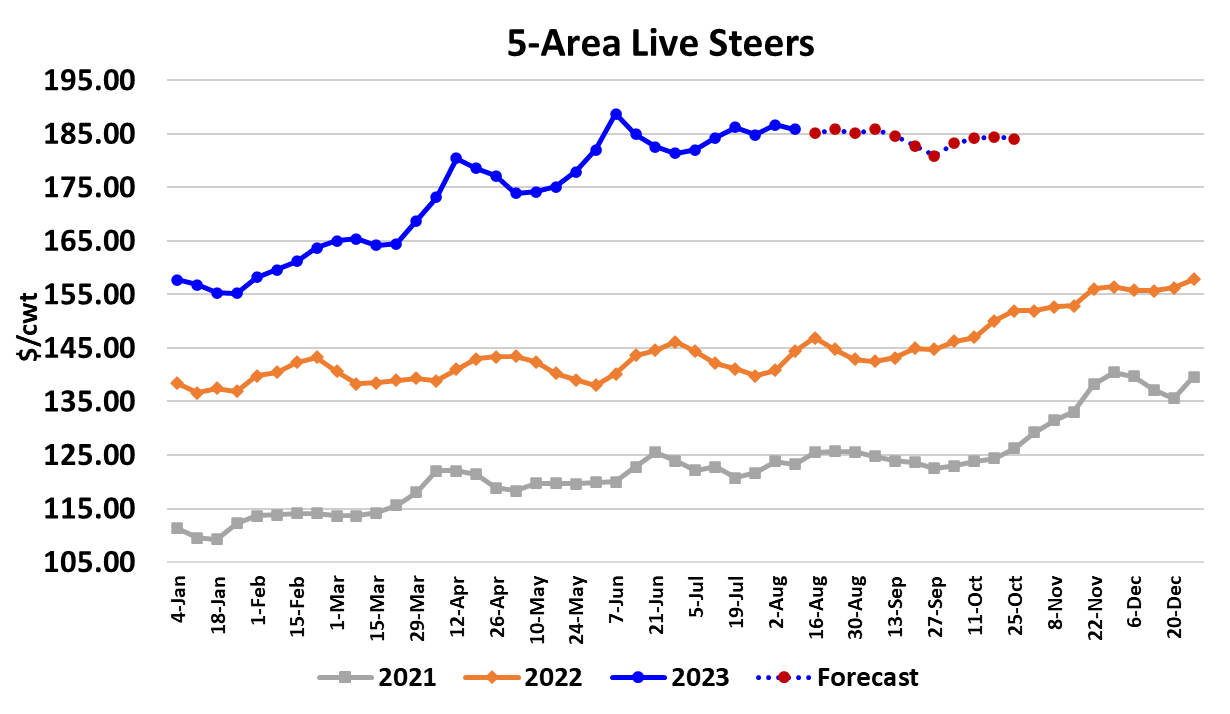

Packers’ efforts to improve their margins by cutting back on the kill finally started to pay dividends this week. That tightened up beef availability enough so that, when combined with a boost in demand ahead of Labor Day, the Choice cutout was able to add $8/cwt. to average $310.40 for the week and the Select gained $7.70/cwt. to average $284.57. At the same time, packers were able to get cattle bought a little cheaper as prices in the South dropped $1 to $179 and prices in the North were about $2 softer at $186. Packer margins went from about -$130/head last week to about -$47 this week and when those cheaper cattle they bought this week show up for slaughter next week, packer margins are likely to move back into the black by $10-20/head. So does that mean the problem is solved and kills can expand again? Probably not without some margin sacrifice by packers. Remember, this boost in beef prices has a demand component as well as a supply component. The last minute buying ahead of Labor Day won’t last much more than another week and when that goes away packers could very well find the cutouts sinking again if they don’t keep beef availability constrained. This week’s fed kill came in at 482k, up 11k from the week before, but still well below the 500-505k that the flow model suggests should be available here in August. Of course, as margins improve there will be some financial incentive for packers to push the kill higher, so some discipline will be required if they are to maintain a positive margin. Also, it isn’t a given that cash cattle prices are going to continue lower from here. Cattle weights are really low for this time of year and there is a very hot spell scheduled to descend on cattle country over the next 7-10 days. That could slow weight gains and might even cause and uptick in death loss. It might swing the leverage meter back in the cattle feeder’s favor. Since they can see the cutouts rising just like the rest of us, they will want their fair share of the beef dollar. So the best course of action for packers is just to keep the kill constrained for at least another couple of weeks until they get to Labor Day, and thus will get another small kill week added on. This week steer weights were reported unchanged from the week before and the DTDS dropped even lower than it had been. That makes me think that feedyards are more current than most observers think and the upcoming hot spell will only improve currentness. The gains in the cutout this week were largely driven by the ribs and the end cuts. The boost in ribs didn’t surprise me since that is a prime target for Labor Day ads, but the gains in the chucks and rounds was a little more than I expected and thus the cutouts rose more than I expected. The gains in end cut pricing are probably tied more to tightening availability while the rib price increase is more likely due to last minute Labor Day orders. Buyers shouldn’t panic about the ribs because those will likely move lower in early September (or maybe sooner), and that will be another opportunity to acquire them on the cheap ahead of the Q4 seasonal price increases. However, buyers should have a strategy in place for holiday middle meat needs because supplies will be tight this year and price levels could well exceed last year’s strong market. After moving lower for five weeks in a row, the 50s posted a small gain this week. That seems temporary to me, but further declines might be smaller than what we saw during July and early August. A lot will depend on how much discipline packers exhibit in keeping the kill down. The lean trim just keeps going up. This afternoon 90s were quoted at $306/cwt. I keep expecting the lean trim to turn lower as it typically does around this time of year, but prices there have been stubborn. Cow kills should increase seasonally as we move past Labor Day and that might be what it takes to finally turn the lean trim market lower. However, 2024 could be an explosive year for lean trim as cow numbers continue to tighten cyclically. I’m expecting the 90s to average about $340/cwt. next year, a 22% increase from this year. If I’m wrong about that, I’m probably too low. Beef exports continue to run well below last year, but that is just par for the course when the cattle herd is shrinking and prices are elevated as they are now. There were estimates released this week that claimed consumers are getting close to exhausting their pandemic savings and that, combined with the restart of student loan payments in October, holds the potential to crimp beef demand. We need to keep an eye out for that. Next week, look for some further gains in the cutouts as the Labor Day buying finishes up, but I’m less certain about another drop in cattle prices. Watch the weather also for indications of the duration and intensity of the heat wave moving into the Midwest.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}