Beef Wrap April 8

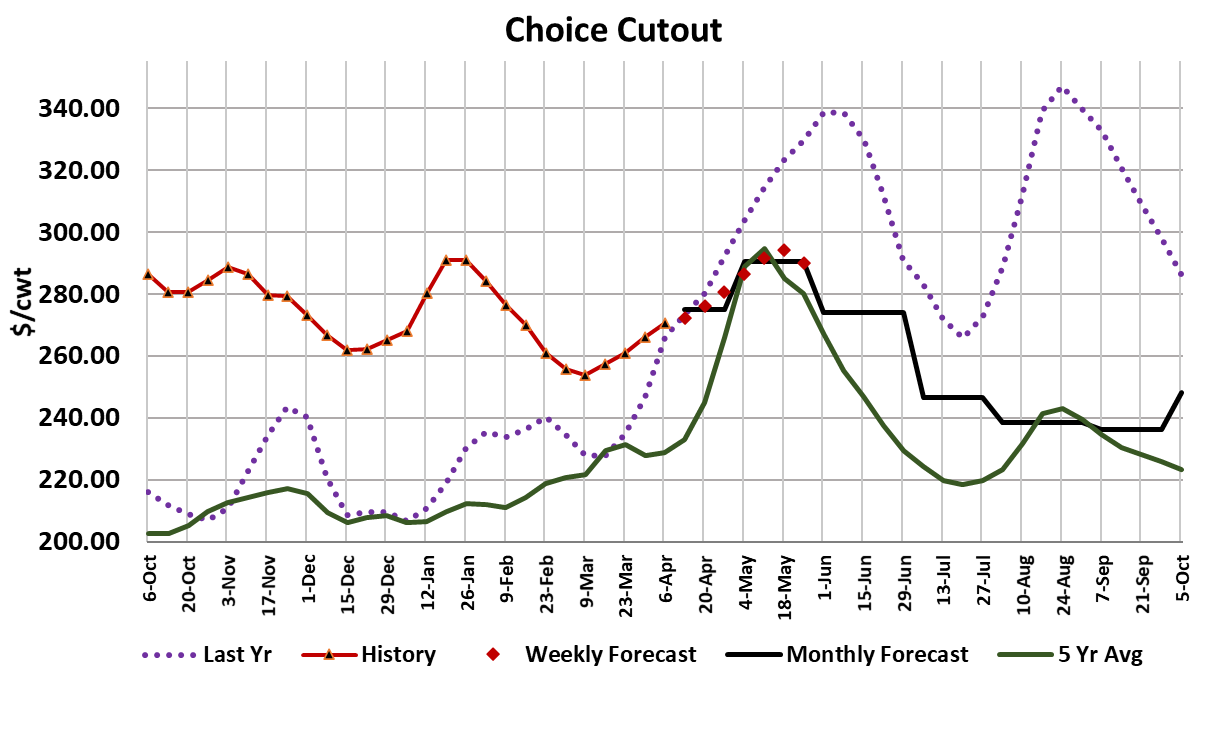

The cash cattle market moved a little lower this week, but for all

practical purposes it remains stuck in the $138-139 range it has been in

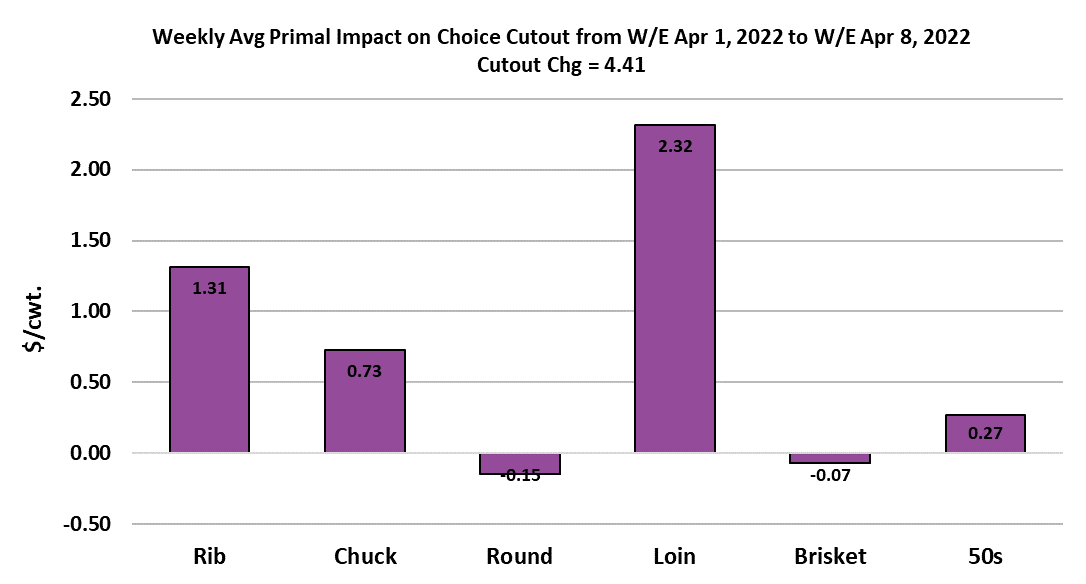

since early March. The cutouts continued higher, but at a little slower

pace than expected. The Choice cutout added $4.41 on a weekly

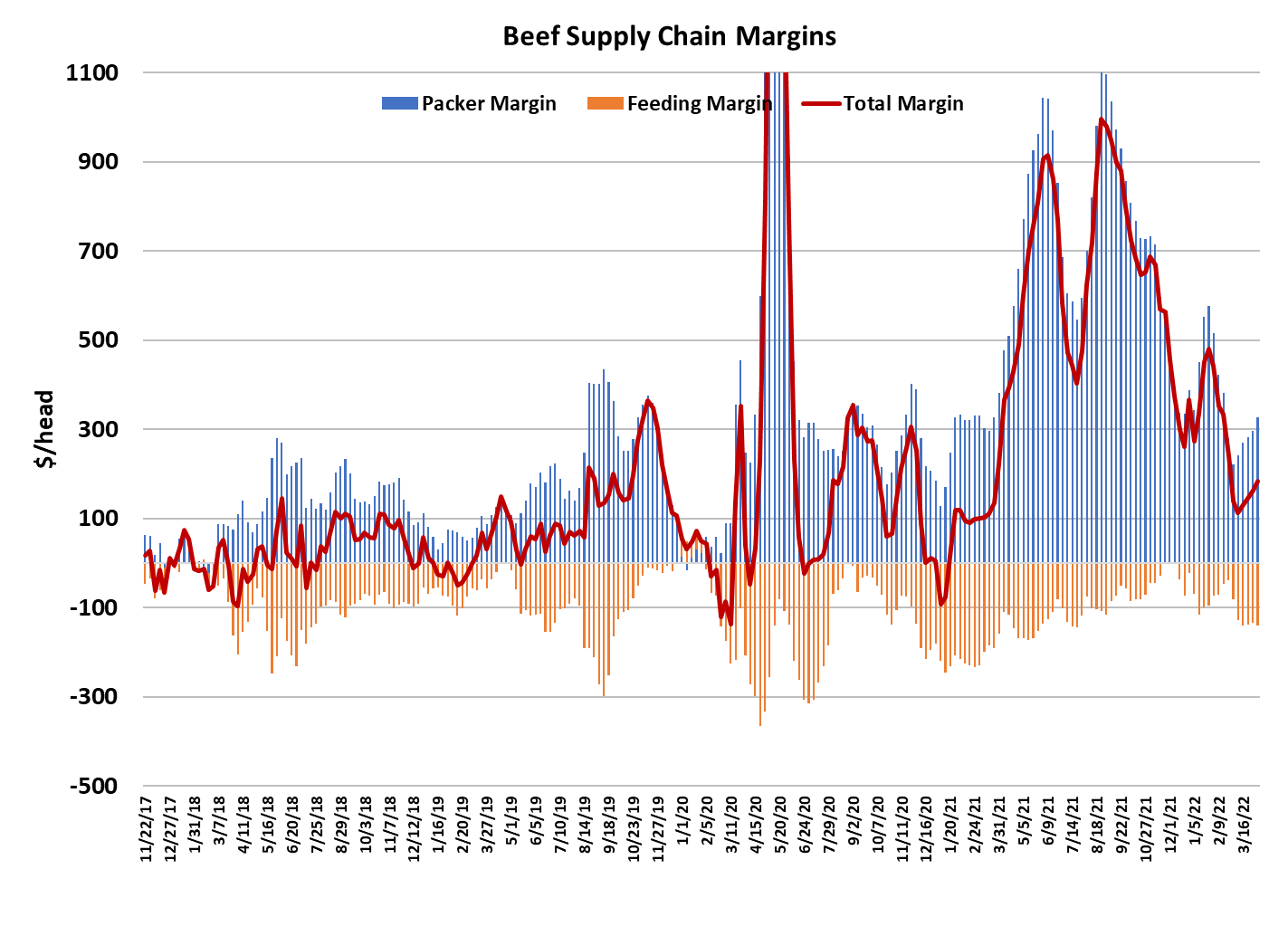

average basis and the Select cutout was up $2.74. Packer margins are

slowly working higher and I calculate this week’s margin at $326/head,

up $30 from last week. This appears to be a pattern that is going to be

with us for the next few weeks at least—cutouts moving higher, cash

cattle holding steady and packer margins growing. With feedyards full

of heavy cattle, cattle feeders have little leverage to push cash cattle

prices higher. In fact, this week, the cattle trade started on a Monday

and that is a sign that cattle feeders felt fortunate to get steady money.

As long as their margins are moving upward, I don’t expect packers to

pressure the cash cattle market. Now, what happens if the cutouts

should turn lower and start to compress packer margins?

Most observers would think that is an unlikely scenario and I’m among

them, but it is not outside the realm of possibility. I suspect that if the

cutouts and margins turn lower that packers would be pretty quick to

pressure the cash cattle market. They feel entitled to very good

margins during the spring season and will seek to make that happen

however they can. I have to admit that the gains in the cutout recently

haven’t been all that impressive. I’m finding that more often than not, I

have to lower forecasts each week because the market is just not living

up to expectations. Now, that could change, of course, and the big

hump on the horizon that the market needs to clear is the Easter

holiday next weekend. It could be that retailers are just full up with

hams and turkeys for Easter promotions that they just don’t have room

for a lot of extra beef at the moment. It is possible that once we get

past Easter, the beef orders will pick up substantially. On the other

hand, the softer-than-expected interest in beef could have more to do

with extremely high retail beef prices and a consumer that is seeing his

budget stretched by price inflation on almost everything he buys.

If we don’t see stronger beef pricing immediately following the Easter

holiday, I’m going to lean toward the second explanation and that

would be a real negative for prices over the next few months. There

are a lot of cattle that will need to be processed between late April and

early August and if consumer demand for beef is struggling, then lower

prices will be required to help clear all of the beef that will need to move

through the domestic market. I have been saying for some time now

that consumer demand for beef is very likely to revert to more-normal

levels this year after a host of factors, including massive government

payments direct to consumers, gave us the best beef demand ever

recorded. The quarterly demand index chart below provides an idea of

how I see this playing out in 2022. First, notice how strong the

demand indexes were in 2021 (blue bars), relative to the five-year

average (yellow bars). Last year’s demand surge really got going

good in Q2 and demand peaked in Q3 (remember August?).

Then demand moved a tiny bit lower in Q4 and lower yet again in Q1 of

this year (green bars). The shaded green bars report the demand

index that is impounded in my beef price forecasts for the rest of the

year. I have it continuing to work lower in Q2 and Q3, with a slight

uptick in Q4. If we realize those demand levels, they would still be way

stronger than normal, but significantly below the 2021 super event. My

working theory is that the 2021 demand bubble was caused by external

events (pandemic, stimulus) and the further away we move from those

things, the more demand is going to revert back toward the longer-run

average. Time will tell. On the supply side, packers put together a

very large fed kill this week at 525k. That was 39,000 head more than

the week before and probably reflects packers’ desire to build some

inventory ahead of a lighter kill next week due to the Good Friday/

Easter events. Even so, it creates a big supply of beef that will be

looking for a home next week when retailers’ attention will still be

focused on hams and turkey.

It will be interesting to see how wholesale pricing holds up. Steer

carcass weights were reported down six pounds this week and that big

decline was much needed. However, it didn’t really affect the DTDS

weights very much and there are indications that next week’s weight

data will show a much smaller decline. So, heavy carcass weights are

still a problem in my mind. It does look like cattle country might get a

heavy dose of precipitation next week and that could muddy up the

feedyards and result in some faster weight loss. USDA reported the

official export tally for February this week and it showed a 1.6% YOY

increase. That was a good bit less than what I was looking for, but still

the second strongest February on record. More importantly, beef

imports were reported up 41% YOY and thus imports exceeded

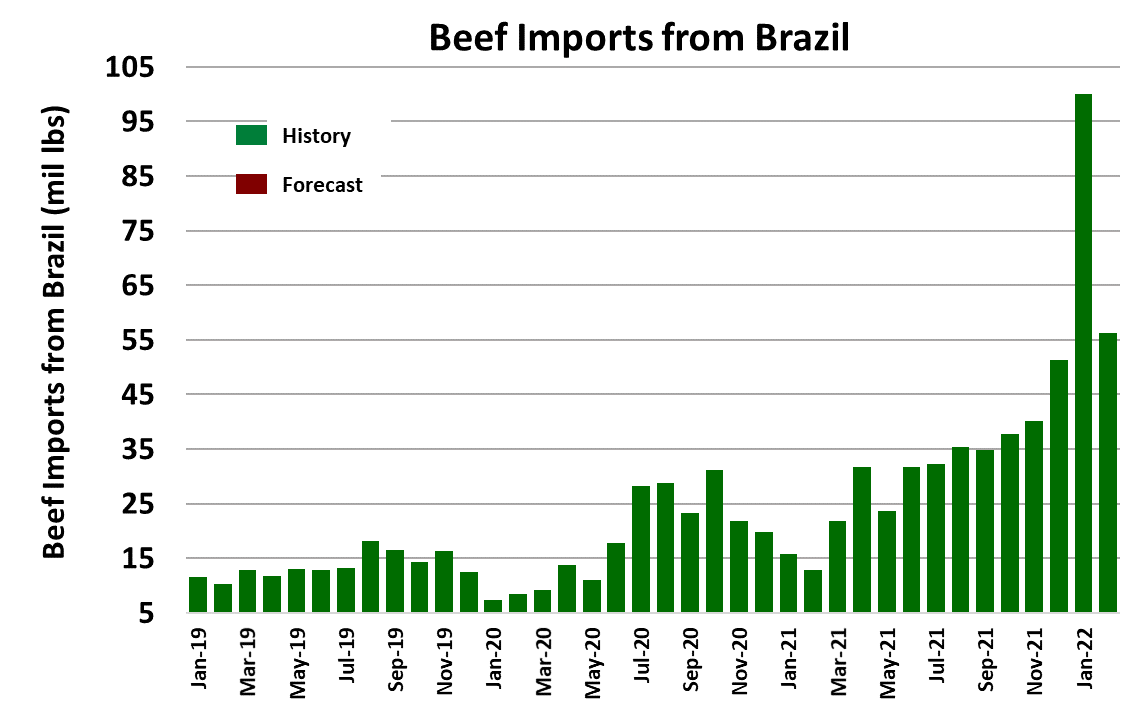

exports by 25 million pounds during February. Both Brazil and Mexico

are finding very advantageous to sell beef into the US market.

However, Brazil has now reached its tariff rate quota and that means

that we will probably see a lot less beef shipped from that source as we

get deeper into the year.

Bottom line, the US market appears to be well supplied at the moment

and the supply side only gets more bearish as we move into May and

June, when weekly fed kills above 525k could become commonplace.

Cattle feeders are frustrated that they can’t advance cash cattle prices

and appear to have dramatically slashed placements during March in

response. It is likely they will limit April placements also. That has the

potential to create some tightness in the beef supply, but not until

September and beyond. Between now and then, buyers should find

beef availability to be quite good. Next week, it is likely to be more of

the same—stagnant cattle prices and slowly rising beef prices. Watch

the pace of the cutout increase next week for a clue as to how strong

the post-Easter business might be.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}