Beef Wrap April 15

The cash cattle market took a step up this week, with prices

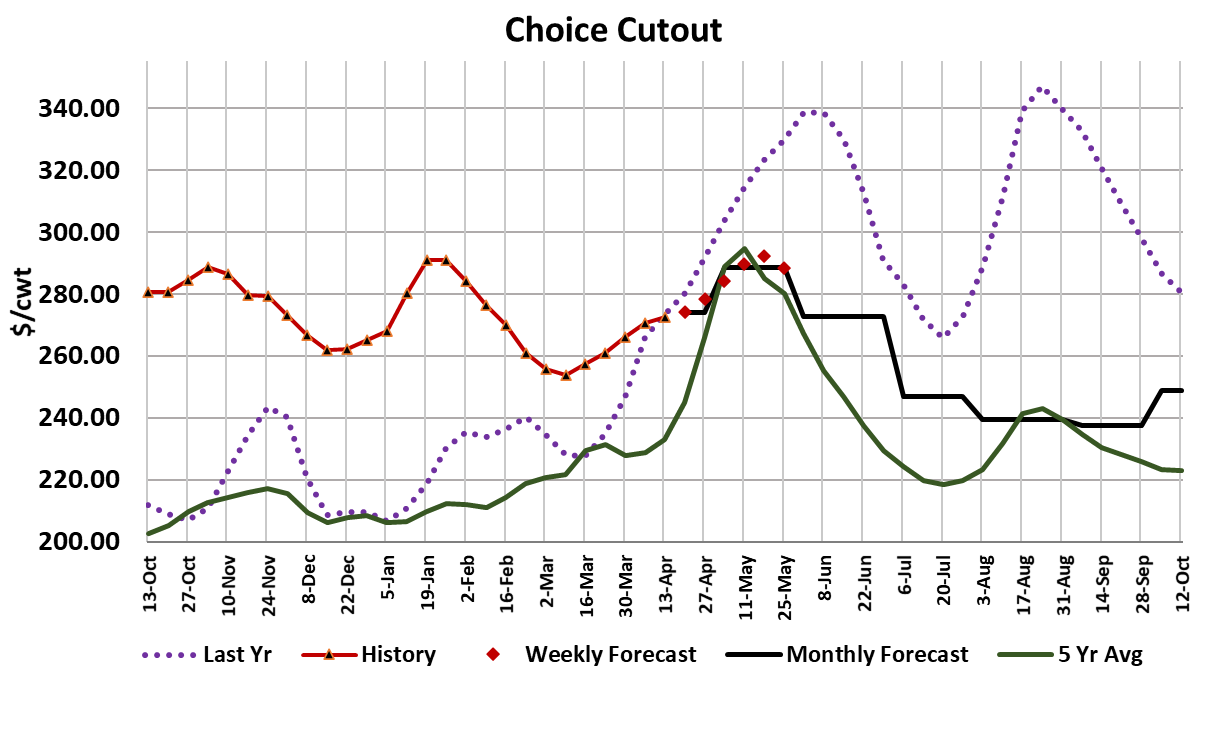

averaging just over $141, up $2 from the week before. The

cutouts were mixed, with the Choice gaining $1.99/cwt while the

Select lost $1.64/cwt. That had to be a disappointment for

packers, after recent weeks where the cutouts have been gaining

$5 or more. So, if the cutouts were so sluggish, why did they pay

up for cattle? That probably has a lot to do with the fact that they

are going to be delivering on big forward sales for the next two

weeks. I’ve included a chart of estimated deliveries on forward

sales that I derive from the comprehensive beef reports that

USDA releases weekly. You can see that that the next two weeks

have a big delivery commitment and that often will tie packer’s

hands with respect to the cash cattle market. Packers are much

less likely to risk a showdown with cattle feeders when they have

large orders to deliver on in the near future. Obviously, retailers

are planning for big beef features in the two weeks after Easter.

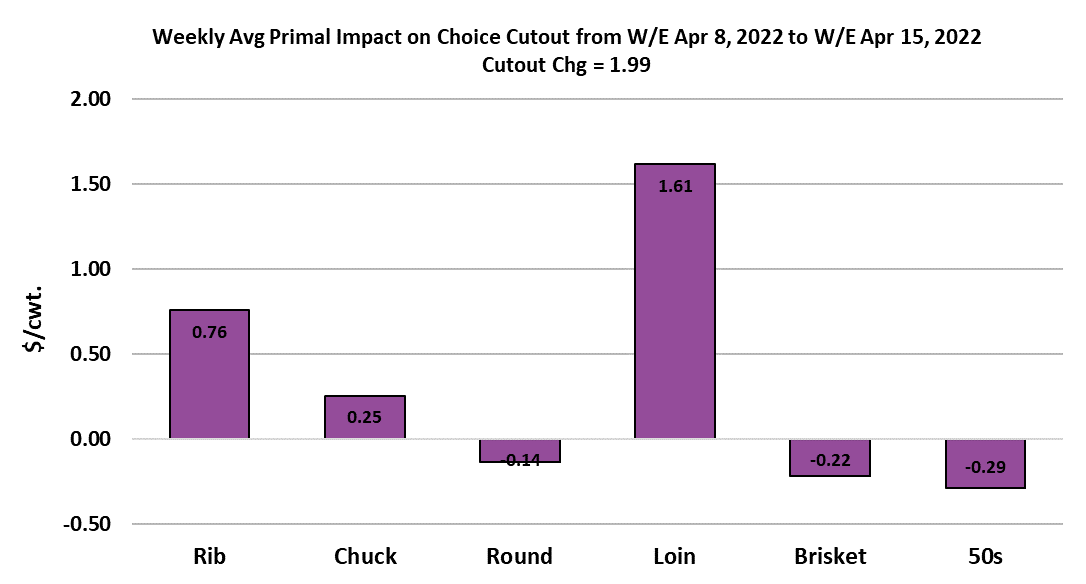

The big slug of booked orders to be delivered next week might

also explain why buyers were not very aggressive in the spot beef

market this week. Those buyers that were active in the spot

market this week were more interested in middle meats than end

meats. The rib and loin primals were responsible for nearly all of

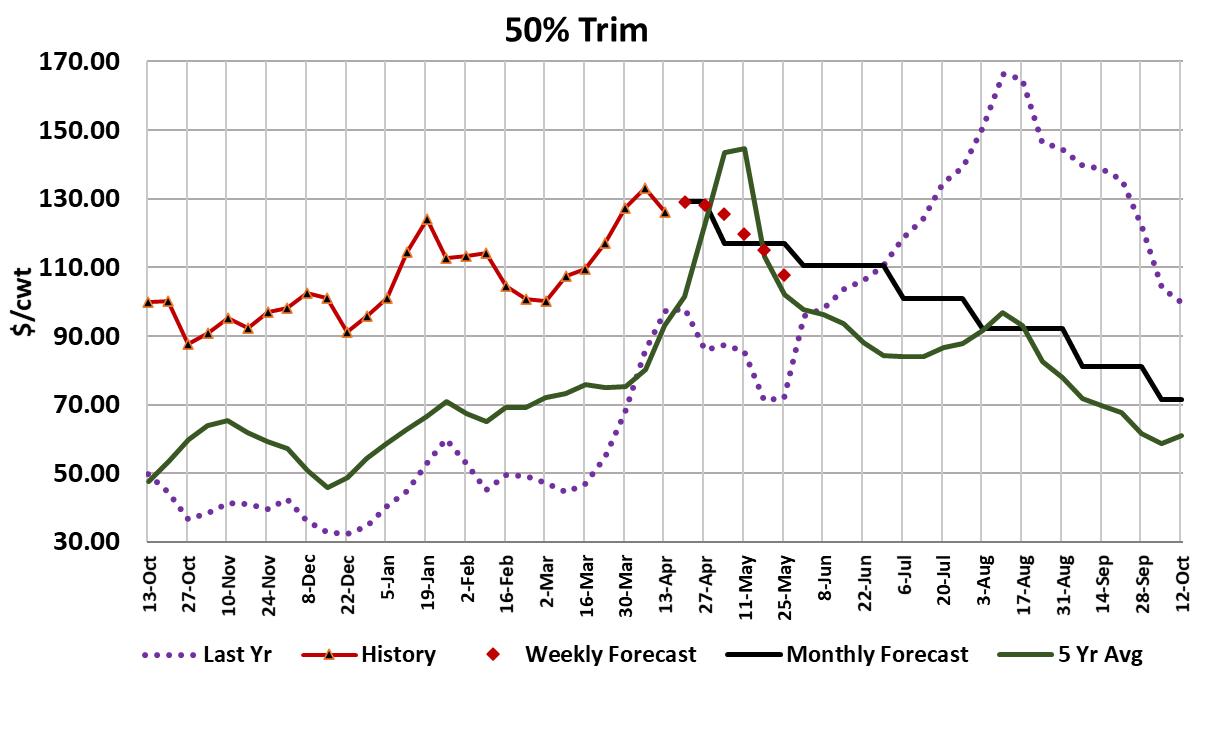

the gains in the Choice cutout this week. Even the 50s market

cooled a bit this week, with prices down about $6/cwt on a weekly

average basis. This week’s slow market is jeopardizing my

forecast of $295 for the spring top in the Choice cutout. I still think

that the market can get there, but the odds of it falling short are

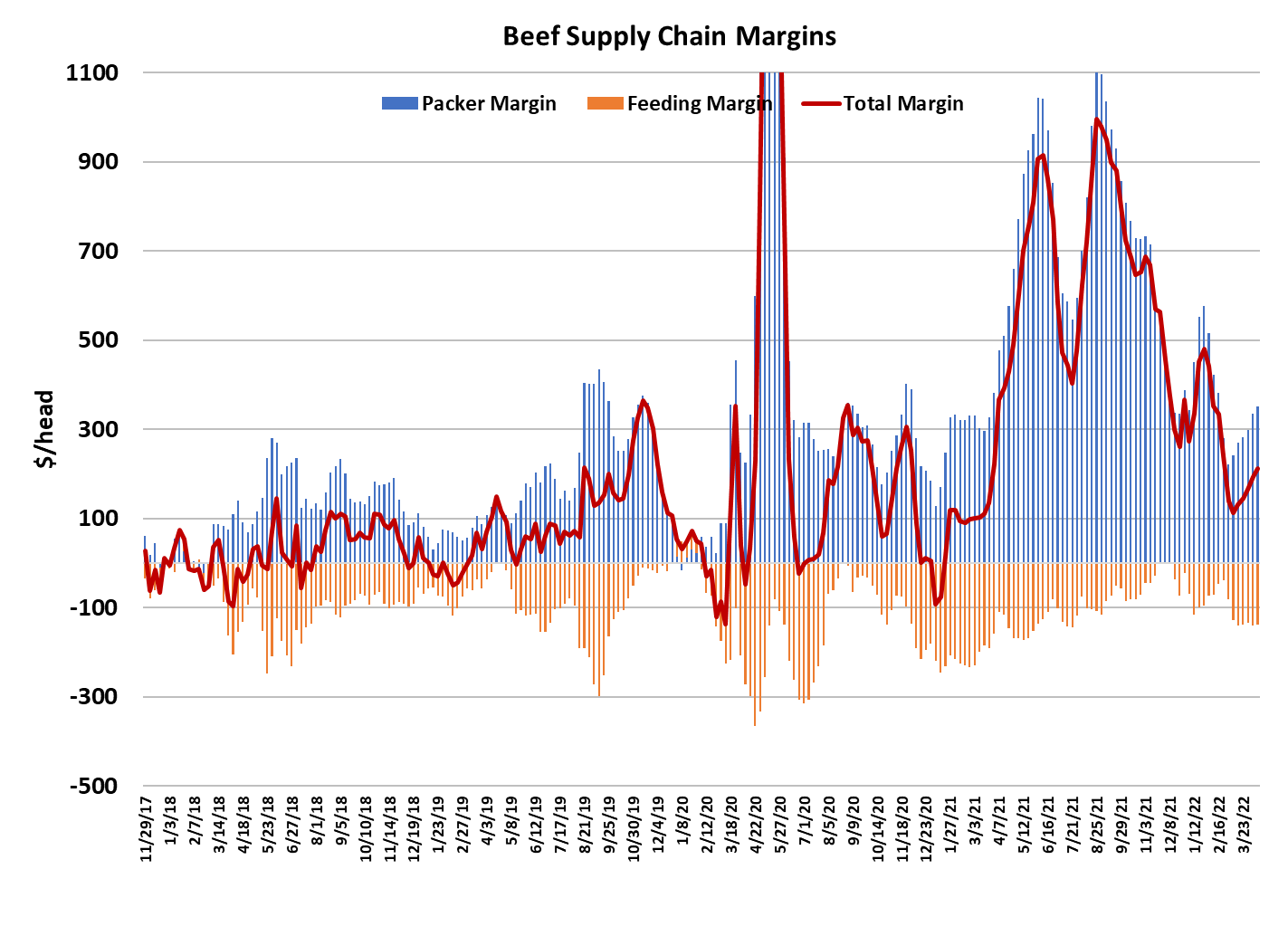

increasing. Packer margins were up $16/head this week to $350,

but there is a real risk that margins will be down a little next week

when the more expensive cattle show up at the packing house.

With all of that product the booked product that needs to be

delivered, packers had better get busy putting blood on the kill

floor. This week’s fed kill was light because of Easter, coming in

at 494k. That was down 20k from the week before. Look for

packers to step it up next week and we will probably see the fed

kill grow week after week until Memorial Day. The kills in June

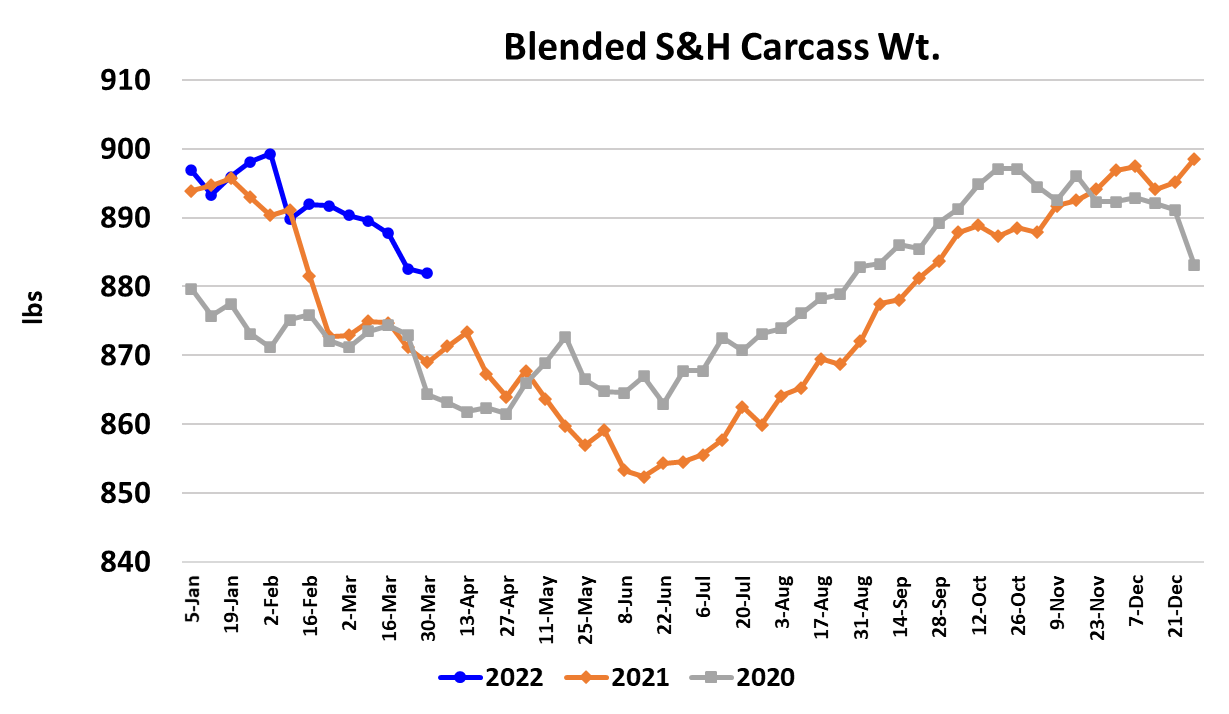

could be even bigger than those in May. USDA reported steer

carcass weights down only one pound this week, which takes

some of the edge off of the prior week’s six-pound decline. As a

result, carcass weights still look overly elevated and that is likely

to limit how much the cash cattle market can advance over the

next couple of months. Jun futures are trading about $5 discount

to this week’s cash, so clearly futures traders are not optimistic

that cattle feeders will be able to move cash prices higher as market-ready supplies increase

strongly in the next two months.

Domestic beef demand is still in a

seasonal uptrend and the combined margin reflects that.

However, the rate of increase in the combined margin currently is

not as impressive as some recent upcycles. That fits with my

thought that beef demand is going cool as we move deeper into

2022 and consumers deal with high energy prices and rampant

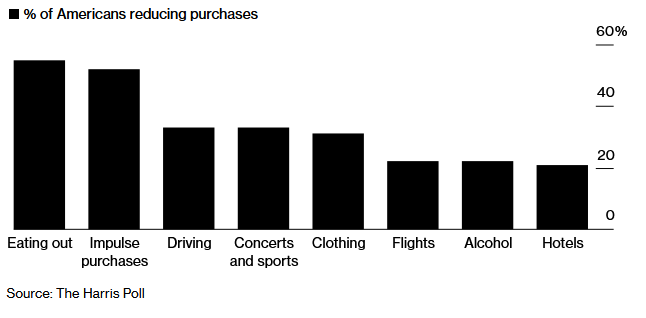

inflation in other parts of the economy. The attached chart shows

the results from a recent Harris poll on what areas consumers

foresee cutting back on due to inflationary pressures. Eating out

less was the number one activity consumers plan to curtail. I

guess they honed their cooking skills during the pandemic and so

they are more comfortable eating meals at home even though

COVID infections are very low. This could actually be a positive

for domestic beef demand because we know that demand soared

when infections were high and people were forced to spend a

larger proportion of their food budgets on at-home meals.

This time around it will be inflation that keeps them out of

restaurants, not COVID. However, people often say one thing on

a survey and do another. I want to see data showing restaurant

sales declining before I believe that consumers are cutting back

significantly on dining out. Overseas demand for US beef still

looks rather healthy based on the weekly FAS data. Corn prices

continue to increase, with cash corn in the cattle feeding areas of

Kansas now running a little over $8/bushel. That is going to keep

feedyard breakevens elevated and I calculate that cattle leaving

the yard today need to bring almost $152 to breakeven. Of

course, they won’t get anything near that this summer, so the long

stretch of negative feedyard margins is likely to continue. At

some point, cattle feeders will cut placements in response to poor

margins and that is probably what traders are thinking when they

price next spring’s futures at $155+.

I don’t doubt that fed cattle supplies will be tighter next year, but I

also a believer that demand will be a lot weaker next year than it

has been this year, particularly if a recession develops while the

Fed is trying to tame inflation. Next week, look for packers to

dial the kill up and that could result in another modest increase in

the cash market. It will be important to watch how the cutouts

react to growing kills over the next few weeks. They need to

move higher at a better clip than they did this week or traders are

going to turn pessimistic once again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}