Beef Wrap April 22

Cash cattle averaged $143 this week, up almost $2 from last week’s

average. However, the national average price masks a wide disparity

between prices in the North, which were $145-147, and those in the South,

where $140-141 was more common. Cattle supplies are tighter in the north

and packers have a big book of product to deliver on as May approaches, so

they were forced into bidding up the northern market. Of course, this leaves

cattle feeders in the South feeling a little like second-class citizens, so in their

search for better pricing they turned to delivering against the futures contract.

Seven delivery certificates were tendered on Thursday and another 25 were

tendered this afternoon. This highlights an important characteristic of the live

cattle futures contract, which is settled by physical delivery of cattle at one of

16 delivery locations scattered across cattle country. When there are

significant regional differences in cash prices, deliveries will be attracted to

the delivery points where cash cattle prices are the lowest. For students of

futures markets, this is known as the “cheapest to deliver” phenomenon.

Imagine if the Apr contract was priced close to the $145 that was paid in the

North this week. Cattle feeders in the South, who can only muster $141 from

the packers, could “sell” their cattle to the CME through the delivery process

at a much higher price than they can get locally from packers. Thus, an indelivery futures contract must remain close to the prevailing price level in the

cheapest market or else it will attract deliveries. Sometimes speculators

forget this important feature of markets and bid the nearby up too much when

they see prices in one region advancing rapidly (like the North did this week).

In the case of today’s 25 delivery certificates, the tendering short didn’t have

to submit those to the clearinghouse until 3pm Central today. That means he

got the opportunity to see today’s Cattle on Feed report before making his

decision on whether or not to deliver. That probably made the decision to

deliver a lot easier. Speaking of the Cattle on Feed report, it looks like it is

going to be a big market mover. USDA pegged March placements nearly the

same as last year, but analysts were looking for an 8% decline on average.

That is a huge miss and will likely send the market plummeting on Monday

morning.

The market had already begun to look overdone after a three-day rally this

week that had added about $4 to the Jun contract before it pulled back today.

So, the bearish COF combined with 25 fresh deliveries has the making for a

deeply red day in the market on Monday. That will likely have packers

bidding lower for cash cattle and they could very well find some takers since

those producers that have short-hedged their cattle will be happy to take the

gains on their hedges and let the cash cattle go at lower money. Further, the

underlying fundamentals in the cattle market haven’t looked all that great

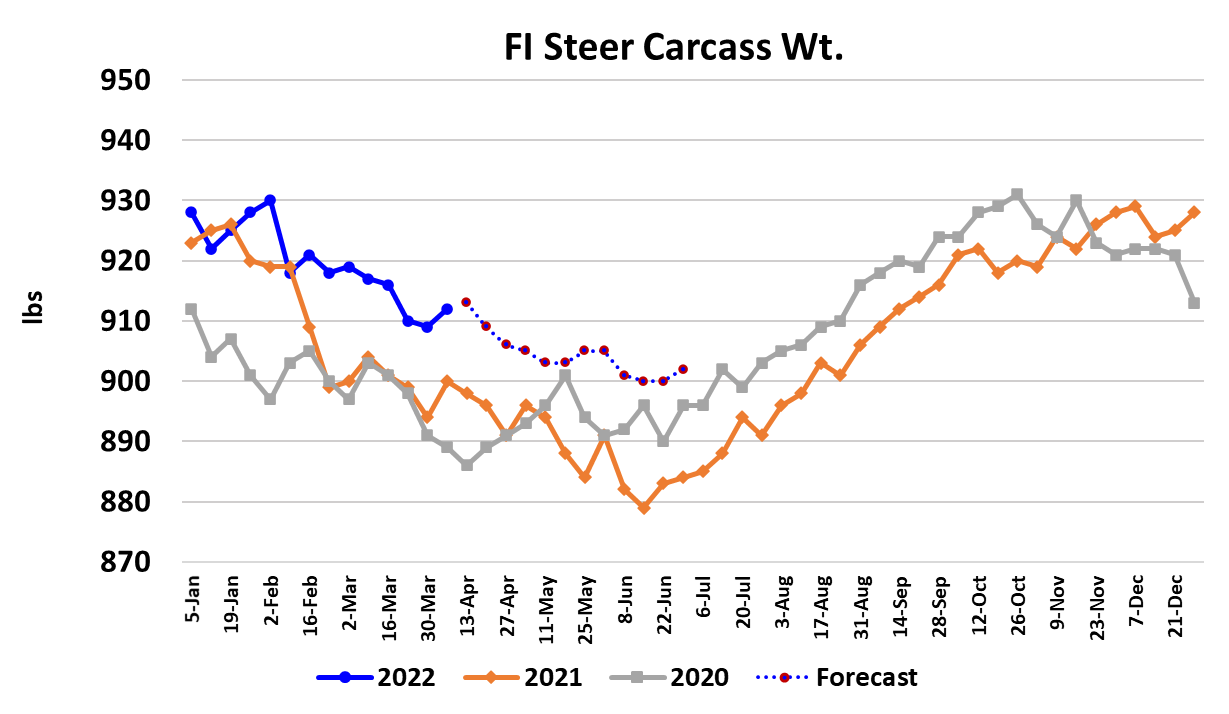

lately. Steer weights were reported up 3 pounds this week when they should

be trending seasonally lower. The DTDS weights shot higher and are now

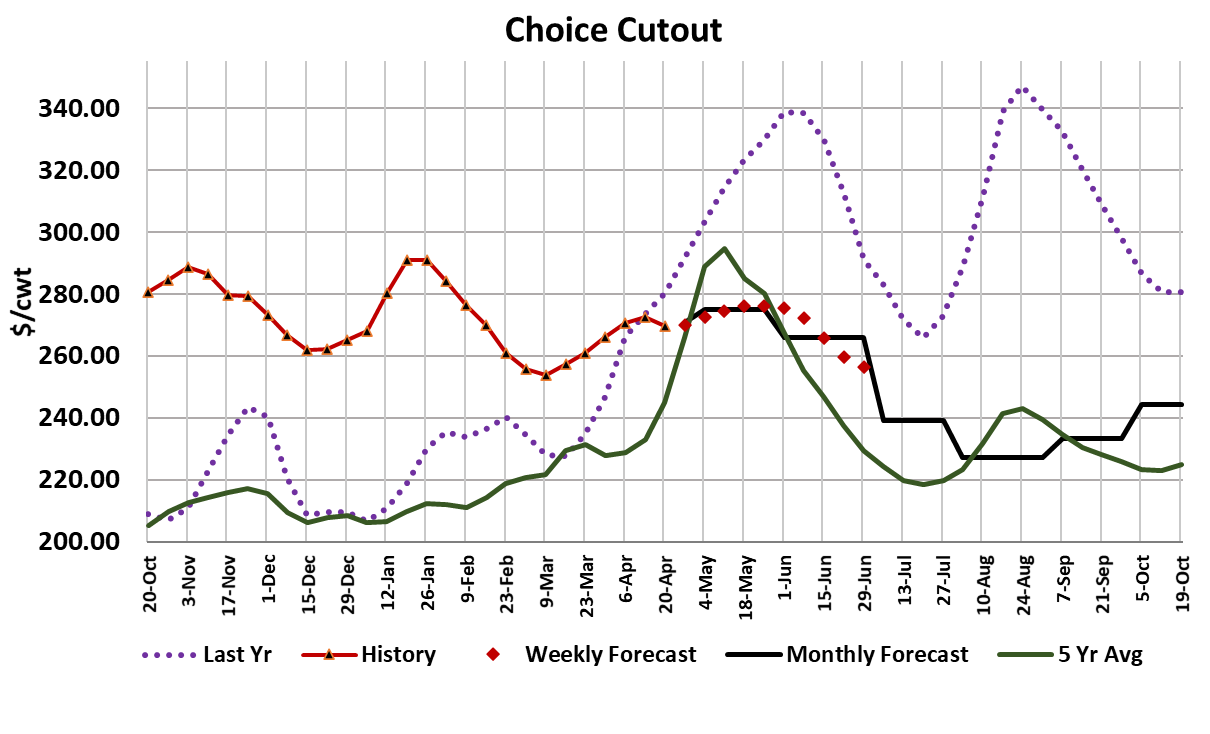

close to +30 lbs. Beef demand also looks pretty shaky, with the Choice

cutout losing -2.90/cwt on a weekly average basis and the Select down

$2.67/cwt. Late April is not the time of year one would expect the beef

market to head south. As a result, a lot of buyers taking delivery on those

forward beef orders in the next few weeks will likely end up paying well

above the spot market and that often creates the temptation to find an

excuse to trim the order back or evade delivery.

Many retailers may be finding that beef simply isn’t moving out of stores

as quickly as they anticipated. Very high retail pricing and the lack of

attractive features is starting to take it’s toll on consumers’ willingness to

put that package of beef in their cart. The cure for that is to lower retail

prices but with inflation surging in nearly every item that consumers buy,

retailers have very little incentive to take retail beef prices down. So how

to solve this problem? Well beef is a perishable product and if it isn’t

moving well out of grocery stores, it will soon start to back up at the

packing level. Packers will be forced to lower wholesale prices and, since

their margins are already pretty thin compared to what they’ve had over

the last couple of years, they will look to pressure the cash cattle market

lower. Cattle feeders will find that their ability to resist lower pricing is

limited because of big placements in the past that are now starting to

become market ready. So, while average cattle prices were higher this

week, the conditions are setting up to take them lower in the weeks to

come.

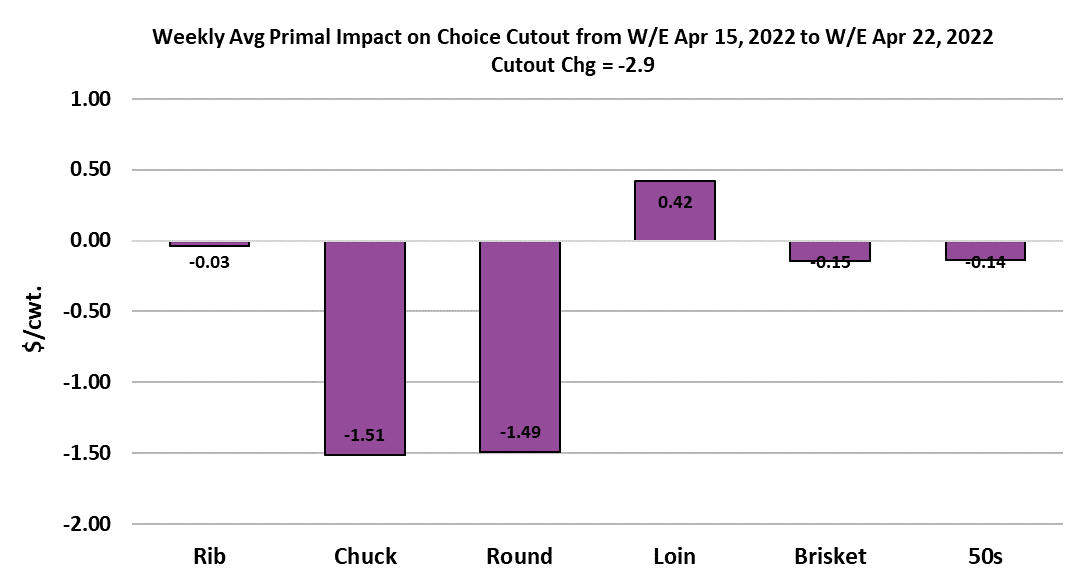

But what about the spring rally in beef prices? I hate to say it, but there

might not be much of a spring rally this year. My initial target was for the

Choice cutout to top around $295 this spring, but each week I’m finding

that the beef market isn’t performing well enough to justify that and so the

target gets lowered. Now I’m thinking it may be a stretch to get the

Choice cutout to $280. The attached chart shows the contribution of each

primal to the cutout this week. Naturally, our eyes will be drawn to the

negative bars on the end meat primals and that indeed is a problem, but

the bigger problem is that we aren’t seeing the big positive bars in the

middle meats that normally occurs at this time of year. Notice that the

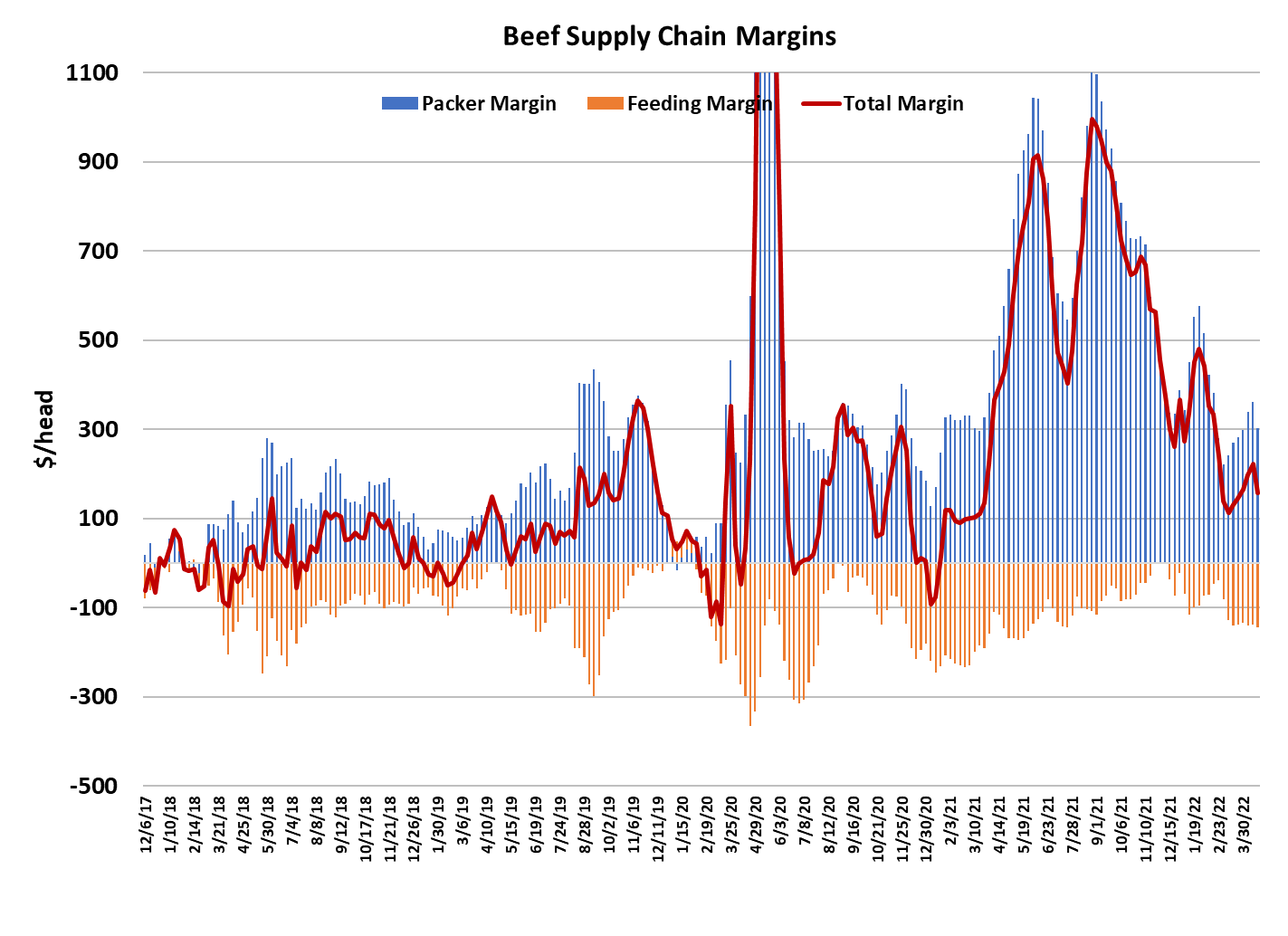

combined margin chart is also signaling some problems with demand. It

turned sharply lower this week and if that continues next week, it would be

a strong sign that the spring price tops in the beef market may be in for

this year. I’m still holding out hope that the middle meats will spring to life

and help produce at least a modest rally from here, but it is far from

certain. This week’s fed kill is estimated at 515k, up over 20k from last

week.

That means more beef that has to clear the system next week, although a

good bit should be headed for delivery to customers who booked ahead.

Market ready supplies of cattle should continue to grow right through June

based on past placement patterns, so if the cutout is struggling now, what

will happen in June when weekly fed kills could approach 530k or more?

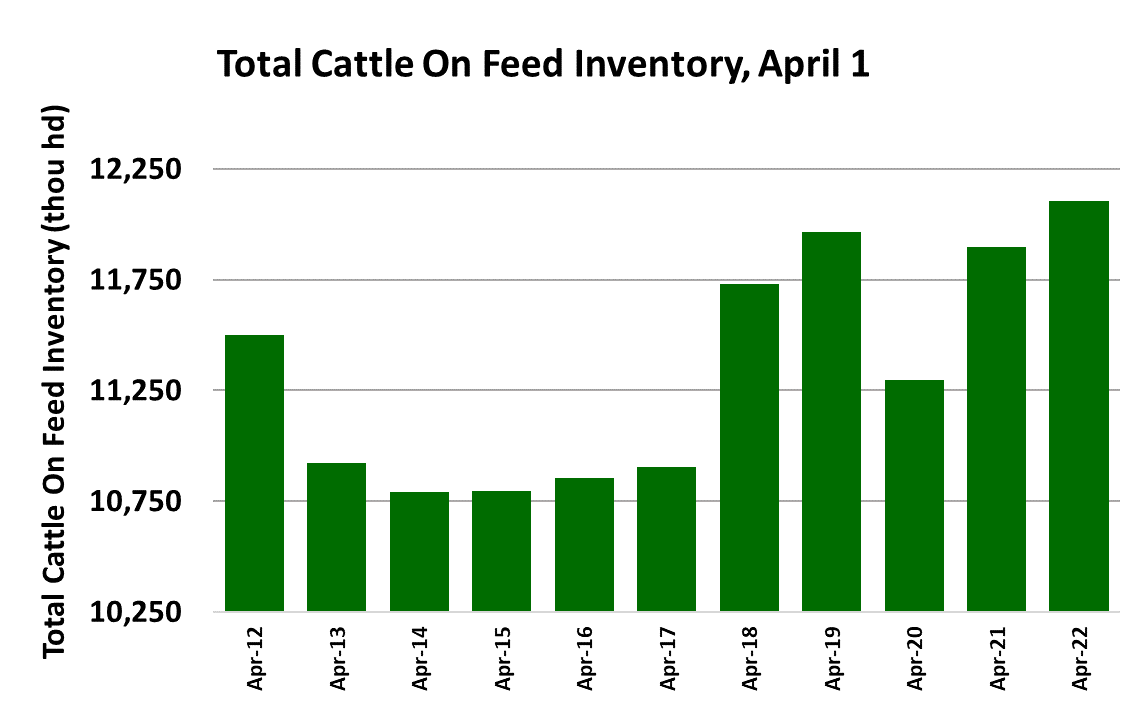

Today’s Cattle on Feed report indicated that feedyard inventories are now

the largest on record for April 1st and 1.7% higher than last year at this

time. Like I’ve said many times in recent weeks, feedyards are brimming

with heavy cattle. Unfortunately for cattle feeders, the financial aspect of

this market is likely to get a lot worse before it gets better, especially since

they are now paying $8/bushel for corn. Beef buyers should be the

beneficiaries, but what good is it to buy beef cheap if consumers aren’t

enthusiastic about taking it off your hands? I suspect this is going to be a

very interesting market over the next couple of months, starting with the

futures open on Monday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}