Beef Wrap April 21

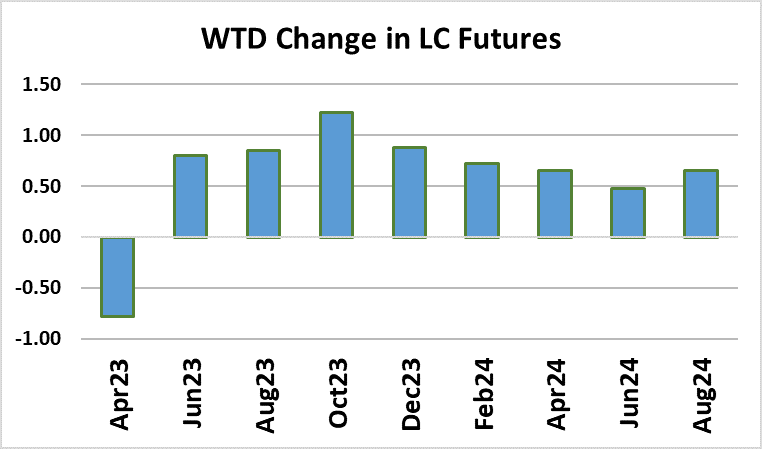

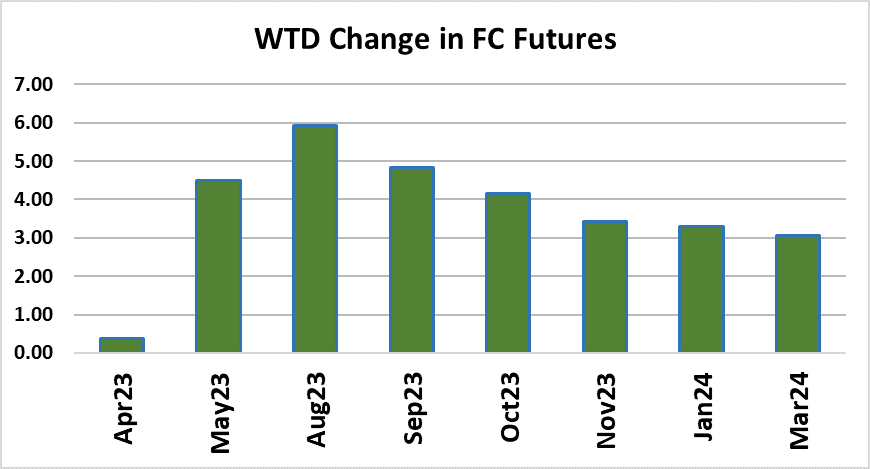

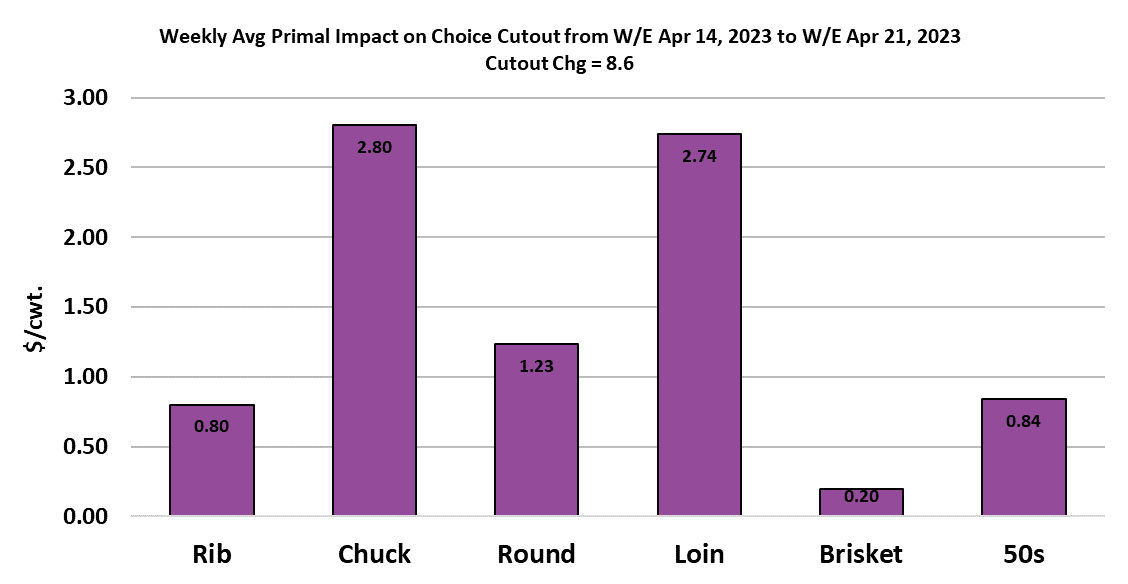

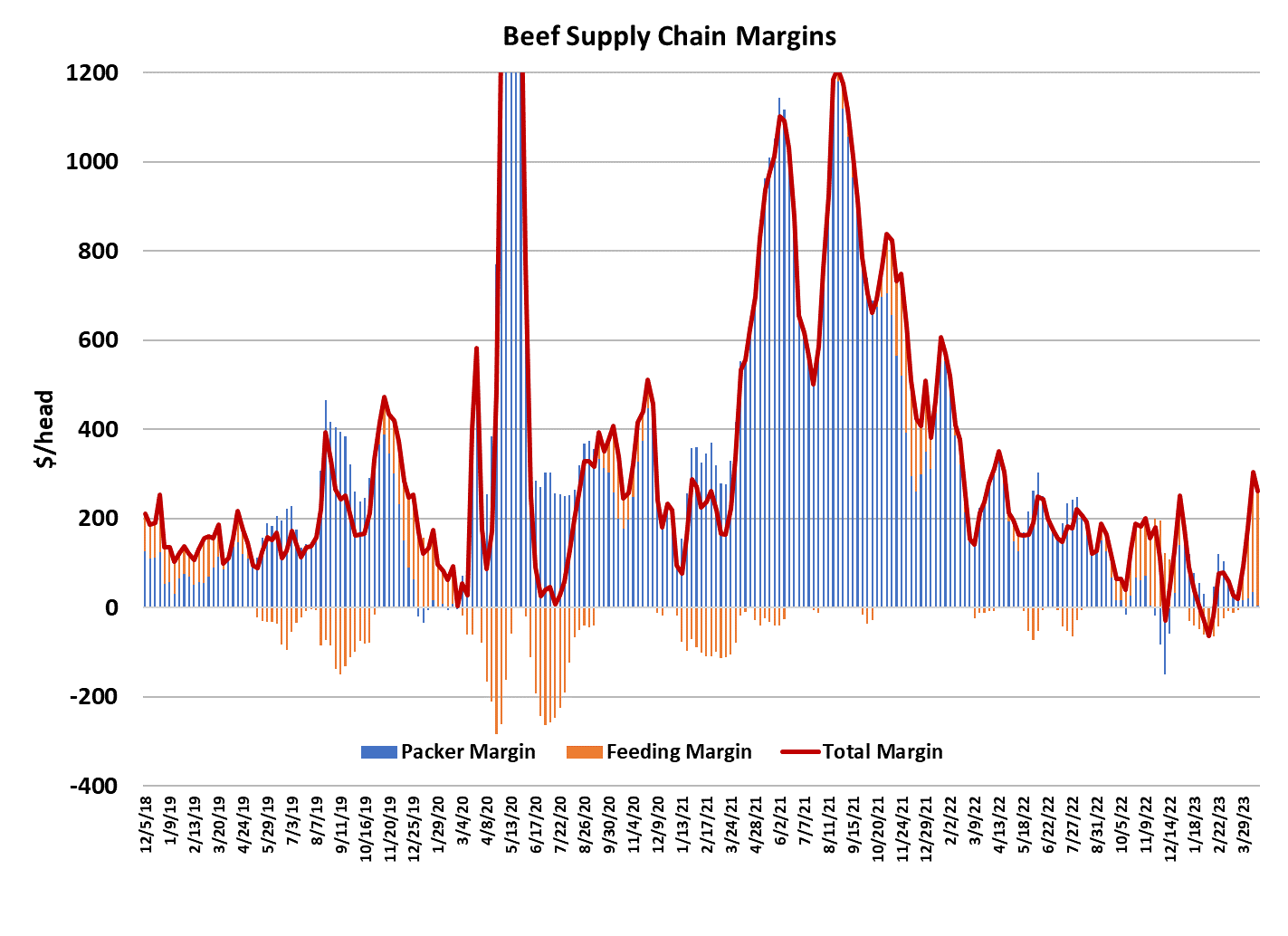

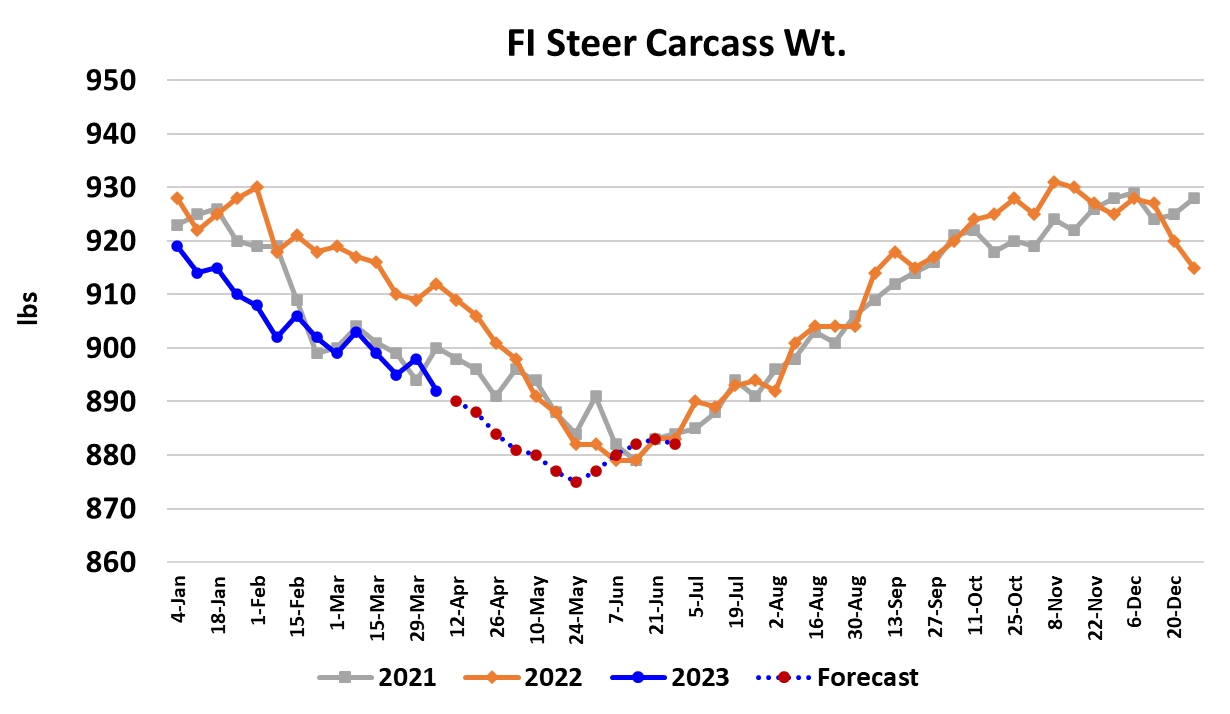

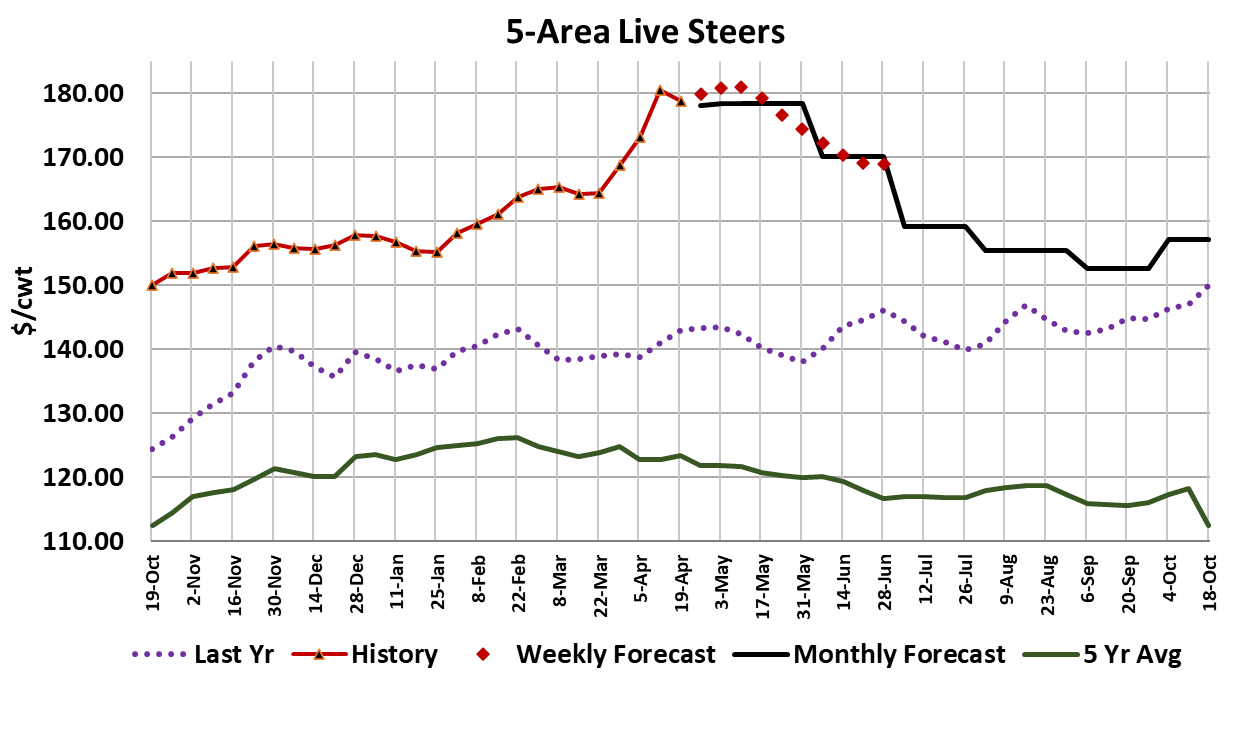

Beef packers managed to barely keep their heads above water this week after a sharp increase in cash cattle prices the week before. Packer margins are estimated at $4/head, down from $34 the week before. In order to stay afloat, packers had to press hard on the beef market and they found some success there, raising the Choice cutout by $8.60/cwt. and the Select cutout by $7.89/cwt. Making margin might be a little easier for them next week since they managed to get cattle bought a little cheaper this week. When all the data are compiled, I think it will show that cash cattle prices averaged $178.75/cwt. this week, down about $1.70/cwt. from the previous week. A big impetus for cash cattle trading lower this week was some significant weakness that developed in the futures market from Wednesday through Friday. Nearby Apr bore the brunt of that selling pressure, but it also tempered prices further back on the curve. When packers saw the board selling off on Wednesday, they were quick to offer bids a little below last week in the Southern region and they found some takers. That pretty much set the tone for the trade that followed. It doesn’t look like packers bought all that many cattle this week however, so that may force them back into the cash market sooner than they would like next week. The cutouts started to loose some steam toward the end of the week and that must be a concern for packers heading into next week. The Choice cutout has risen over $26 in the past three weeks. Buyers are now starting to adjust their purchasing strategies and packers may find it difficult to keep moving the cutout higher. The best hope for further gains lies in the middle meats. Ribs haven’t yet made their normal seasonal move higher as grilling season gets started, so perhaps rib demand will spring to life in the next couple of weeks and help to keep the cutouts from sagging. Loins have done pretty well so far, but they too could see improving demand in the near term. The end cuts have probably peaked for this cycle and have some downside risk as we wrap up April. The most impressive item in the beef complex has been 50% trim, which averaged $18/cwt. higher on a weekly average basis and were quoted Friday afternoon near $182/cwt. That could be a sign that the cattle are greener than expected and/or that demand for manufacturing beef is very strong. Let’s see how long it stays at these lofty levels and how quick prices come back down. My guess is that it still has a little higher to run before it turns lower. Overall beef demand has really surged in the past few weeks and the combined margin chart makes that pretty clear, but what is less clear is whether or not that demand was organic and arising from consumers or if it was simply demand from wholesale buyers caught short and forced to pay what the packers asked. If it was the latter, then we might expect to see the cutouts start to retreat next week. This week’s fed kill clocked in at 485k, very close to what the flow model suggests, but 8k stronger than last week. Packers seem to realize that the key to getting out of their current margin bind is not to press the kill much over current levels. Honestly, I don’t think cattle availability will increase much until near the end of May and I suspect it will be tough for packers to maintain the kill in the 480-490k range as the weather warms up and consumer demand improves. More cattle should become available in June, but not a ton more, maybe enough to support weekly fed kills in the 500-510k range. Last year during June, packers were slaughtering 525k per week. Speaking of cattle supplies, USDA released another Cattle on Feed report this afternoon and it showed feedyard placements during March down only 0.6% from last year. Analysts had been expecting a 4.4% decline, so this report may have a negative influence on the futures come Monday morning. The data indicated that cattle feeders were placing more light weight animals and that suggests that they were trying to target the post-summer period for those cattle to be marketed. In a bull market, it is common to expect that prices are going to be higher in the fall than in the spring and that might be what motivated feeders to place large numbers of animals. They paid up for those feeder cattle also, so they had better hope that the cash cattle market posts some high prices in the fall or they could find their margins underwater. Right now, margin problems only belong to packers because cattle feeding margins are running close to $260/head by my calculation. The last time cattle feeders enjoyed really strong margins was back in November when packers were over-killing the cattle supply in search of high quality middle meats to fill holiday orders. That may also help explain this spring’s large cattle feeding margins. Steer carcass weights are still trending seasonally lower and were reported down six pounds to 892. Weights are now below the past two years and projected to remain that way until June. I see the seasonal bottom in weights coming rather late this year, perhaps around the end of May. The weekly export data for beef looked a little softer this week and is tracking well below last year. That shouldn’t be too much of a surprise given how much beef prices have risen in the past few weeks. My guess is that exports will remain below a year ago for the next several months. Next week, watch the cutouts for signs that buyer resistance is developing and keep an eye on those 50s prices because sometimes they can be a leading indicator for cattle prices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}