Beef Wrap April 26

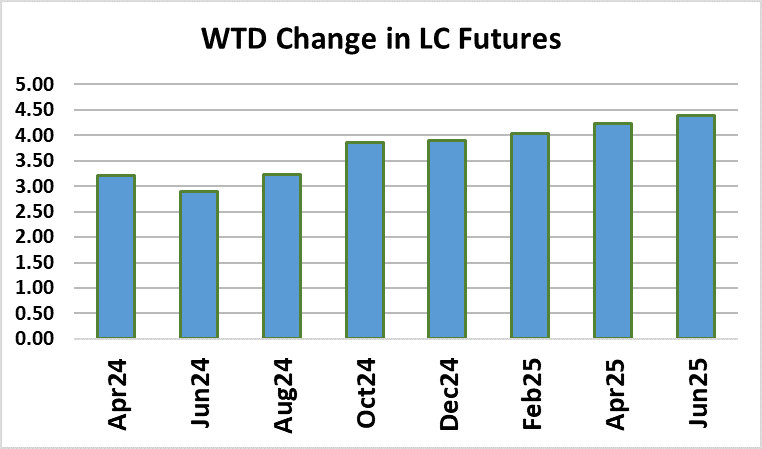

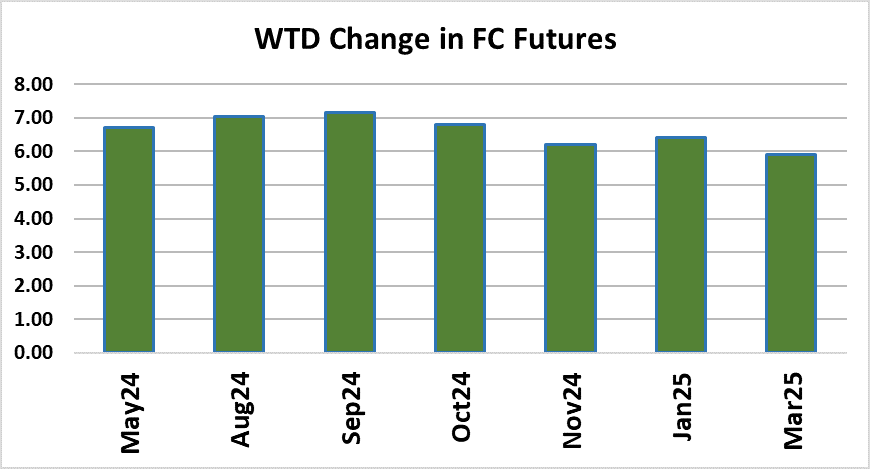

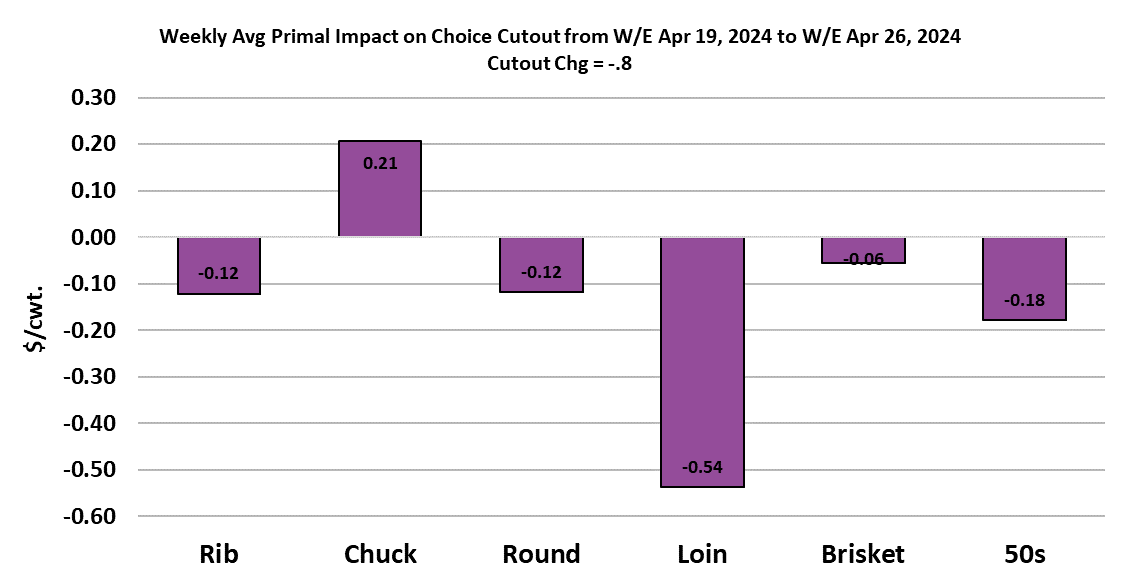

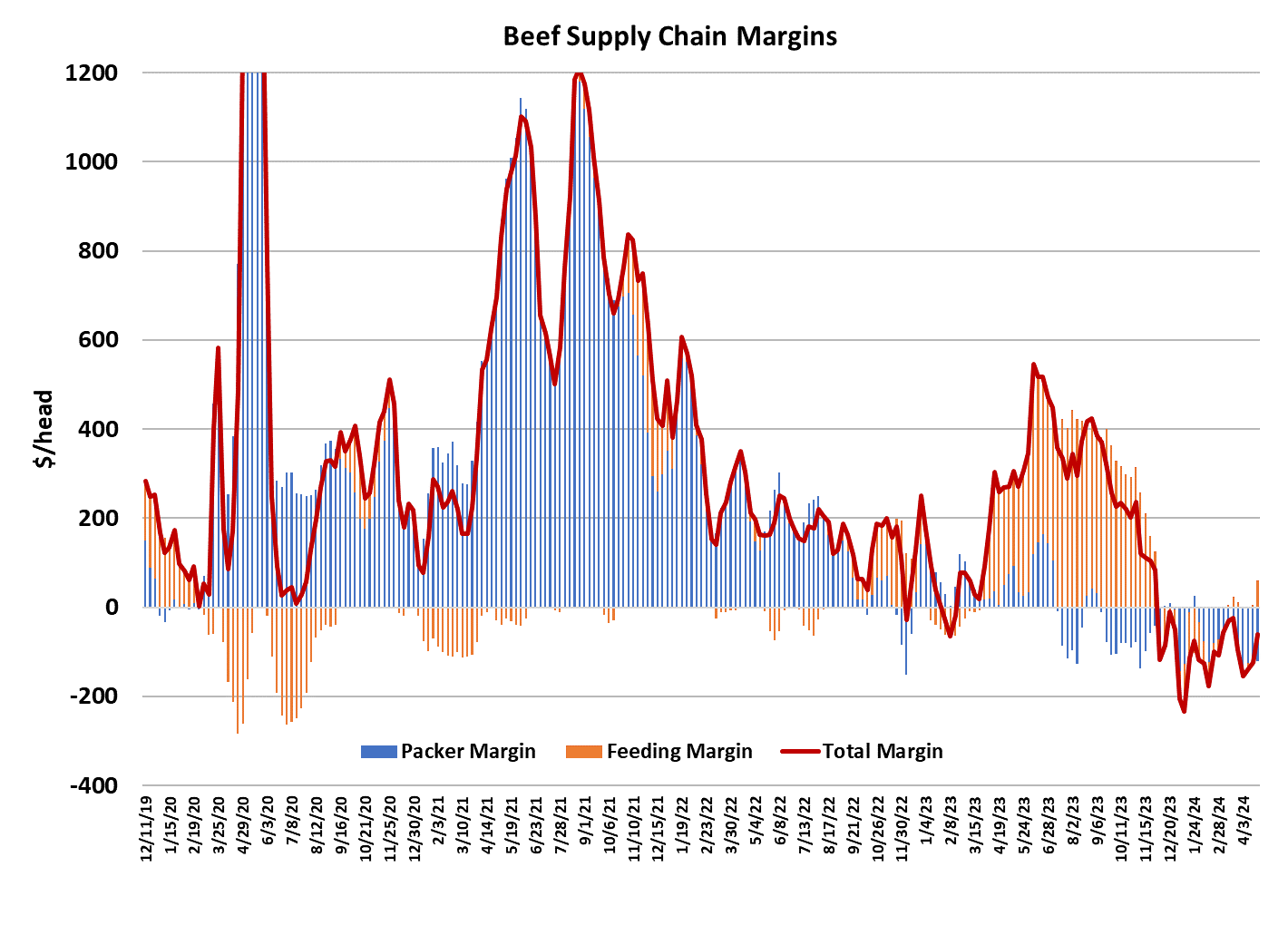

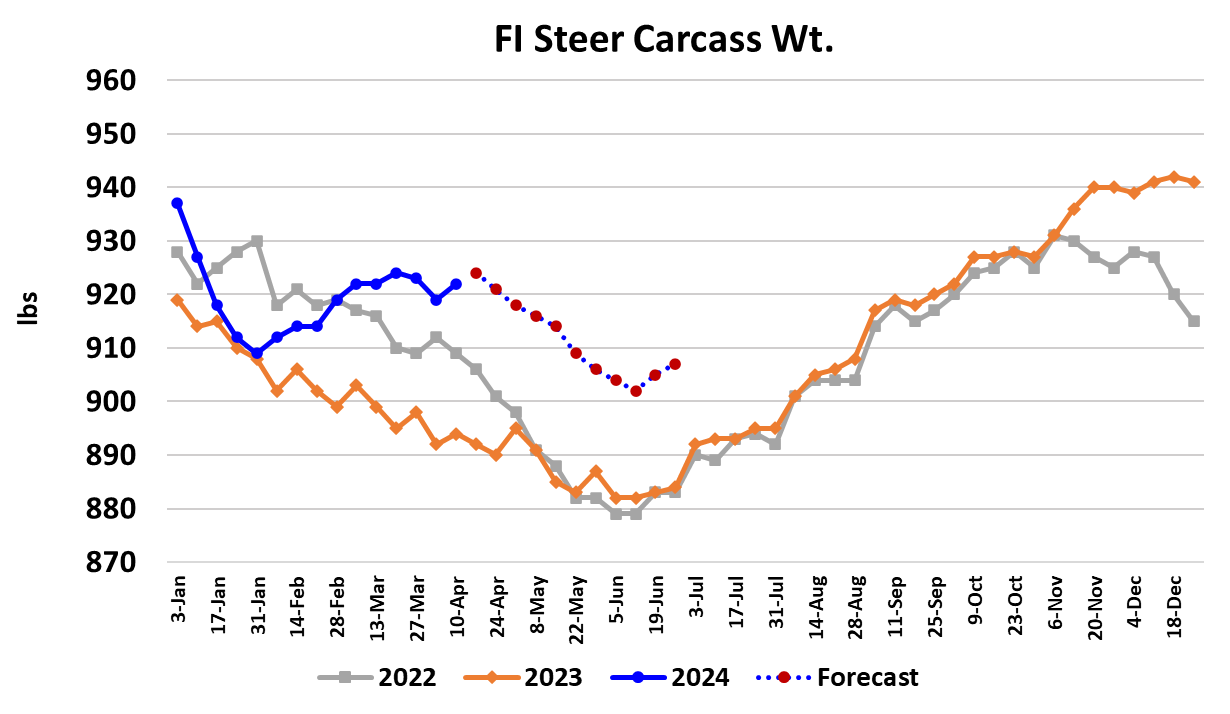

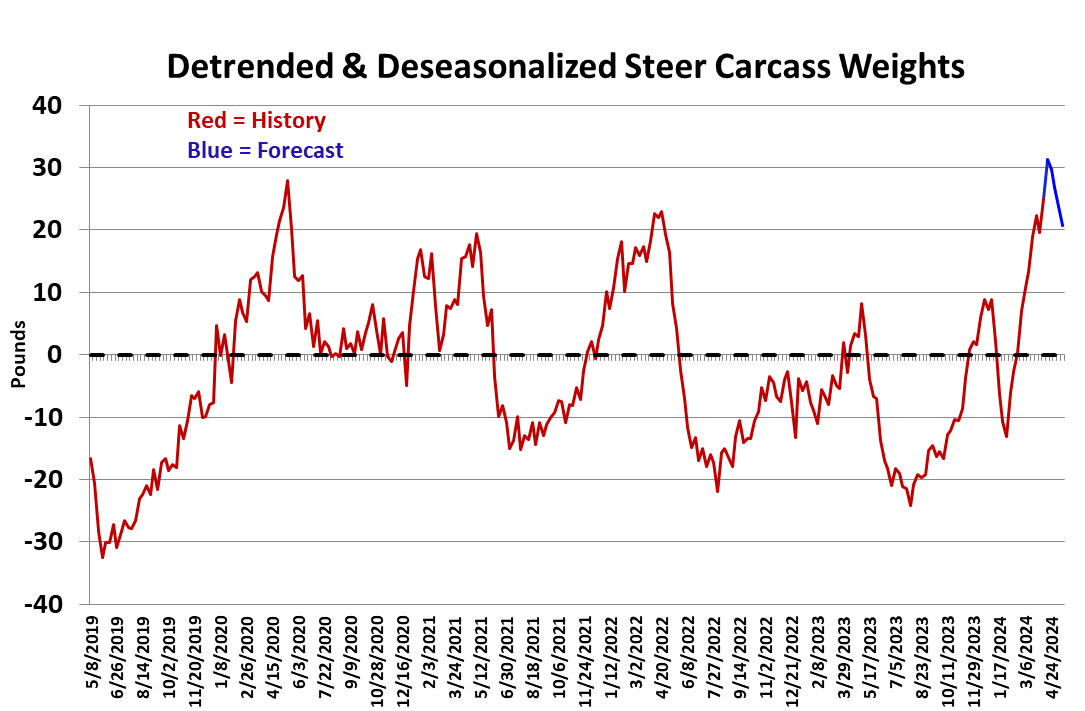

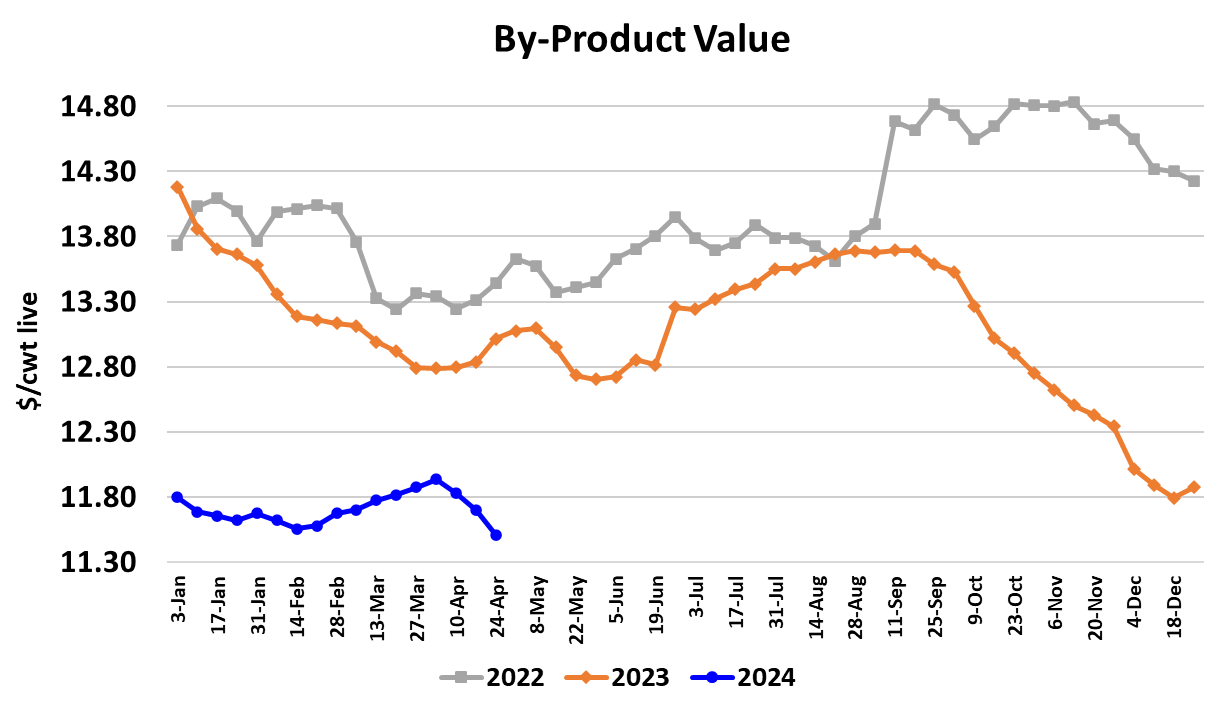

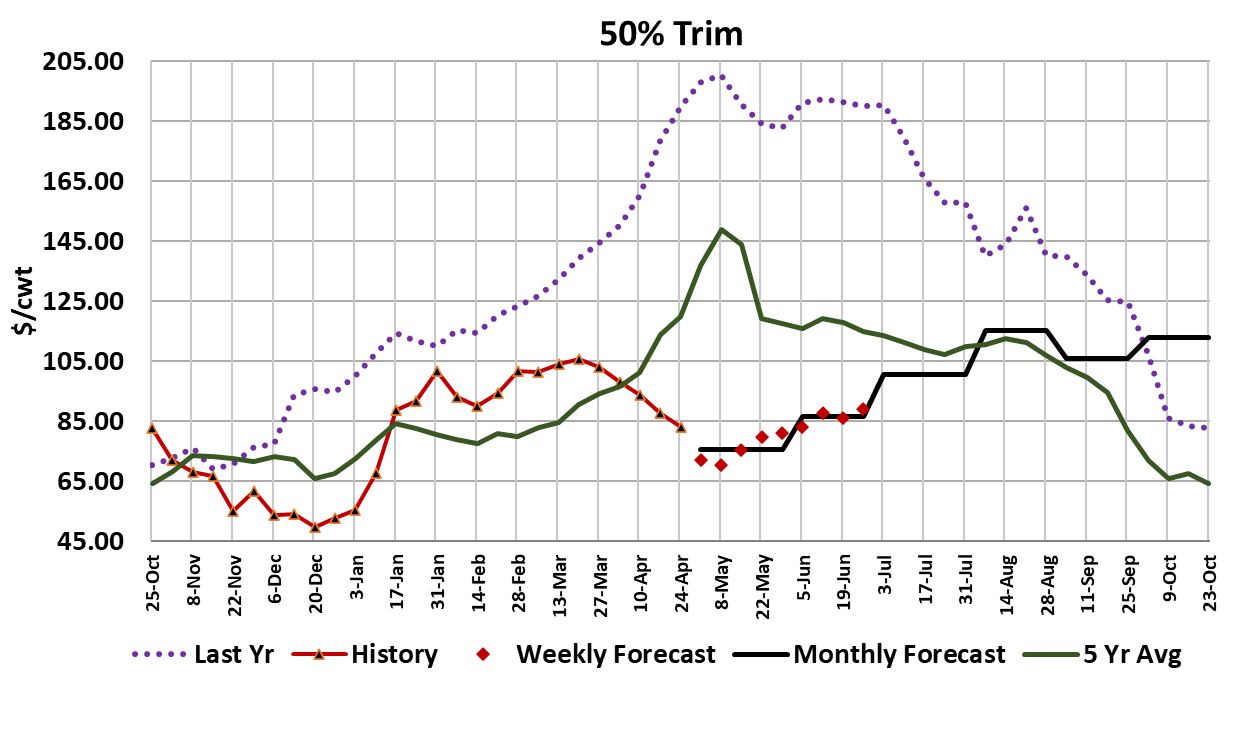

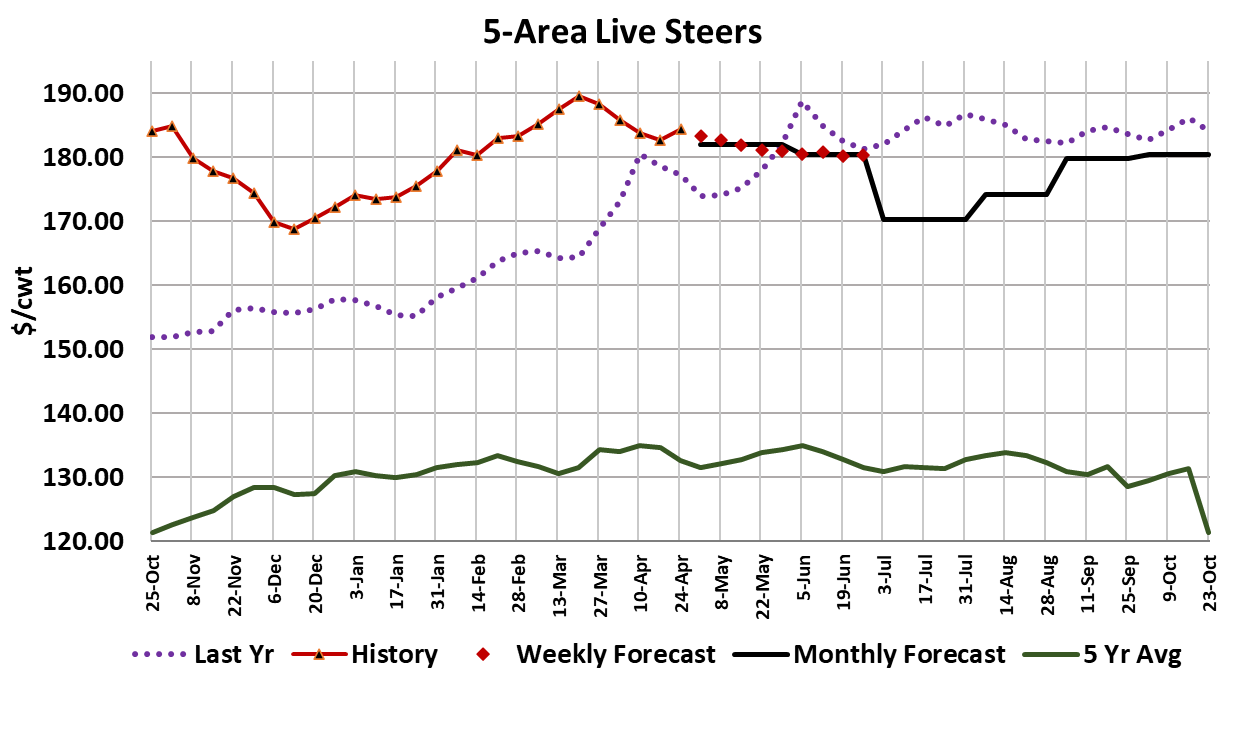

Traders bought the futures aggressively on Monday following the COF report and that seemed to set the tone for a solidly higher cash cattle market this week. On Wednesday, there was news that DNA of the avian influenza virus had been detected in pasteurized milk and that caused some selling in cattle futures, which packers quickly took advantage of, coming out with steady $182 bids, which many cattle feeders in the Southern Plains accepted. However, both Thursday and Friday saw further gains in the futures and that resulted in Northern trade in the $184-186 range which was $1-3 higher than last week. When all of the data are tabulated on Monday, I’d expect the 5-area live price to be close to $184.45/cwt., up about $1.75 on the week. Packers bought pretty large numbers this week and they need them because they have been pushing the fed kill higher recently. This week’s fed slaughter came in at 493k, only 2k below last week’s strong kill. Why are packers running such large kills when their margins are deep in the red? Because they have commitments coming due in the next couple of weeks to deliver product that was previously booked. That said, the spot beef market remained lethargic. The Choice cutout lost $0.80 on a weekly average basis and the Select cutout dropped $0.30. After four weeks of declining cattle prices, packers are now caught in a vise caused by this week’s cash cattle increase and stagnant beef prices. No doubt that packers’ sales desks will be working the phones early next week looking for beef price increases, but so far buyers have shown little interest. I calculate packer margins at -$122/head. One positive development for packers is that the Choice-Select spread averaged $9.82/cwt. this week, well off of lows near $1 about three weeks ago. It was a mixed bag among the primals this week, with some up slightly and some down slightly. 50s prices continued to retreat, averaging close to $83/cwt., which is down about $20 over the past month. I have to believe that, given the heavy carcass weights we’ve been seeing, cattle are carrying a lot of finish into the packing plant and that is resulting in strong 50s production, which is forcing the price lower. Speaking of carcass weights, the FI steer weights moved higher this week after 2 weeks where they had been reported lower. It also looks like next week’s FI steer weights will be higher also. Steer weights are now 28 pounds above last year. The de-trended and de-seasonalized carcass weights look poised to reach +30 pounds next week, which would be even higher than the peaks reached back in the pandemic when cattle were rapidly backlogged due to plant closures. My expectation has been that as spring grilling demand kicked in, it would incentivize packers to ramp up slaughter levels and that would keep carcass weights from becoming a major problem. However, the spring demand hasn’t really kicked in yet and weights have turned higher once again, so I’m getting increasingly nervous that front-end cattle supplies are going to build to an unmanageable level. Fed kills have been higher in the past couple of weeks, but still below 500k of steers and heifers per week and I can’t imagine that packers are going to push the kill much harder than that considering that their margin is in terrible shape. The fundamental forecast has cash cattle prices turning lower again in short order under the assumption that feedyards will begin to feel a much stronger sense of urgency to move cattle before they get so large that they can’t walk onto the truck. As we move into May, the fundamental forecast has the beef prices moving higher on better demand, taking to Choice cutout towards a top around $310/cwt. near the middle of June. If I’m in the ballpark on that and if cattle prices do ease, that could restore packer margins to the point where they would want to run larger kills and thus easing some of the pressure on front-end cattle supplies. Cattle futures have been strongly higher in the past couple of weeks and that seems to be convincing money managers that the bull market in cattle is back on. Of course, the bird flu story is still alive and well and that has the potential to send cattle futures sharply lower without notice, thus there is always the risk that the managed money might decide the bull story in cattle isn’t worth the risk of being blind-sided if bird flu is found in feedyard cattle. A cold storage report was released this week, showing total beef stocks as of the end of March down 9.5% YOY. Smaller cold storage inventories have been a regular feature of this market for many months now as high beef prices have reduced export volumes and thus tempered the need for putting a lot of product into cold storage. By-product values have been tracking well below year-ago since last fall. That weighs on packer margins and also may serve as a leading indicator of impending weakness in the macroeconomy. Next week, look for cash cattle to trade steady and the cutouts to start working higher on improving demand as warm weather spreads to most of the country.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}