Beef Wrap April 19

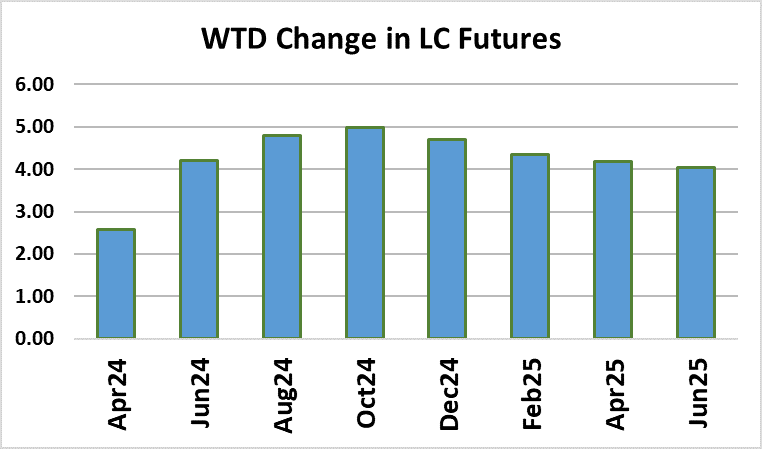

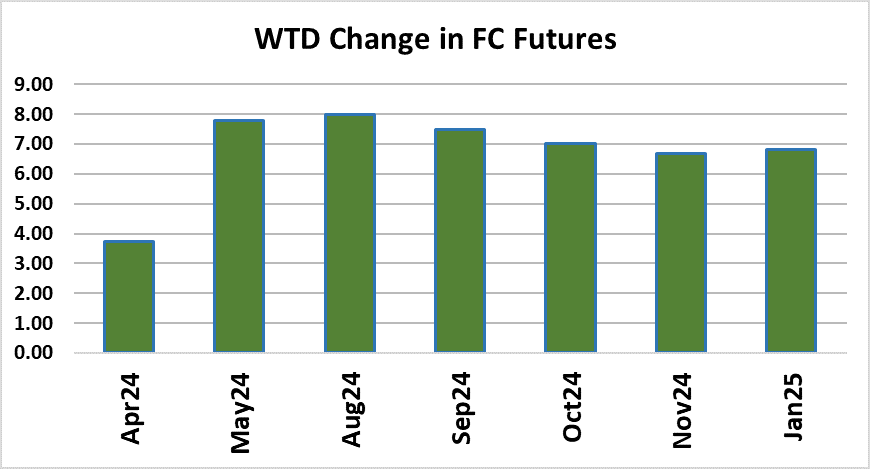

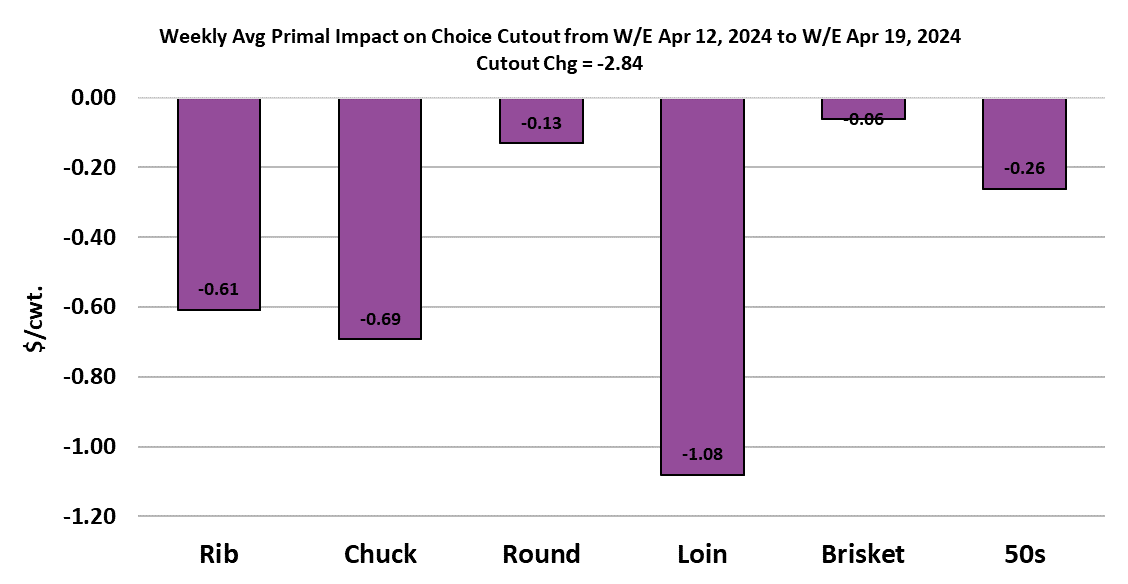

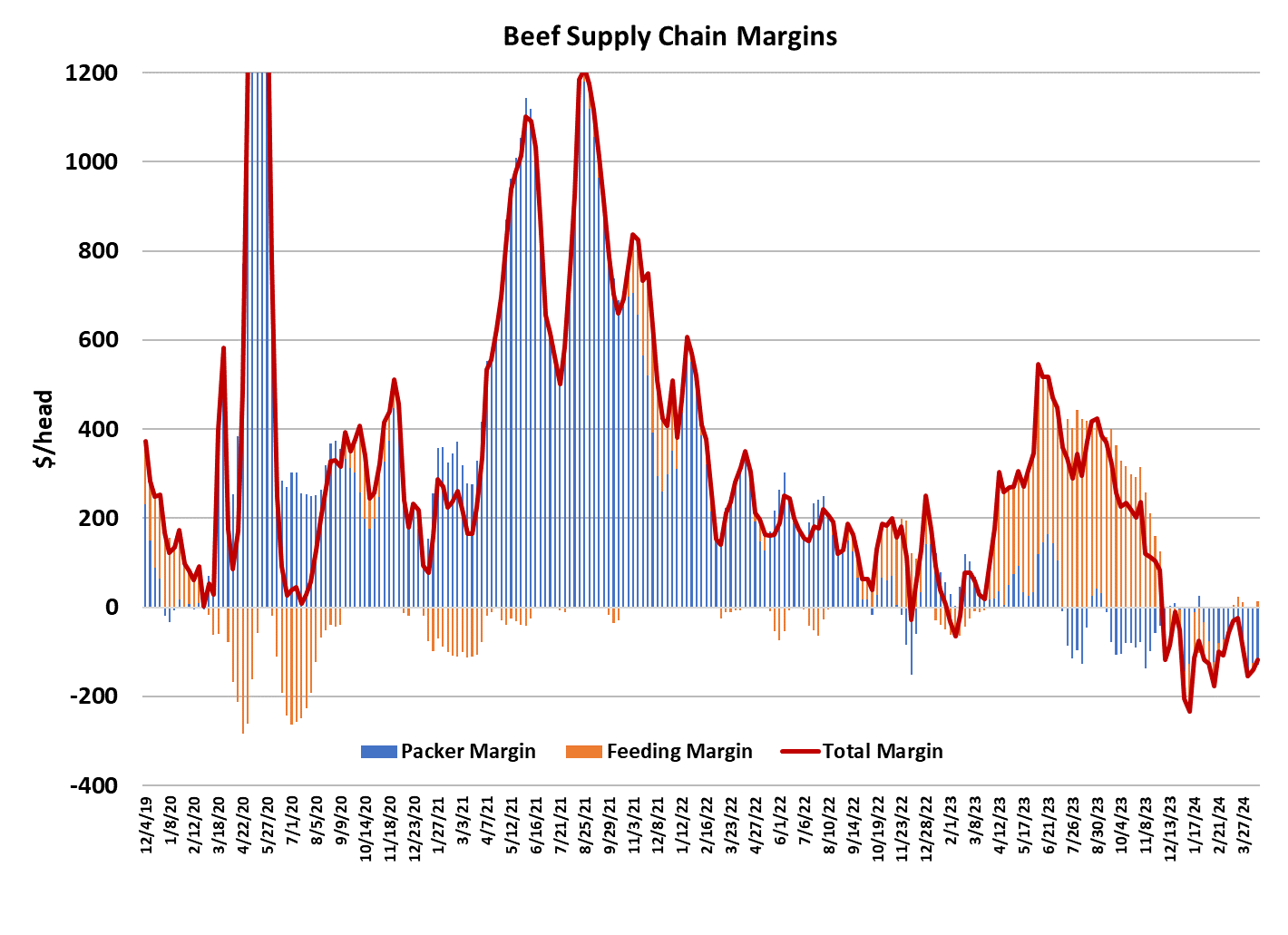

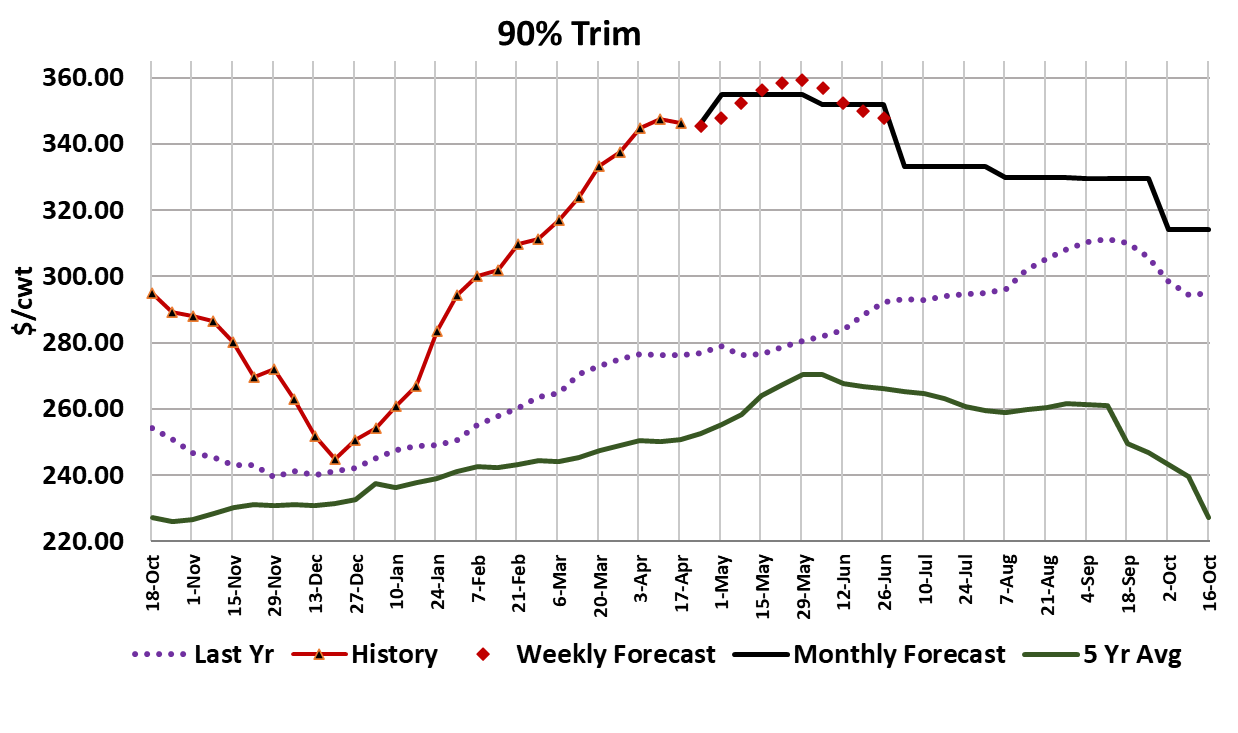

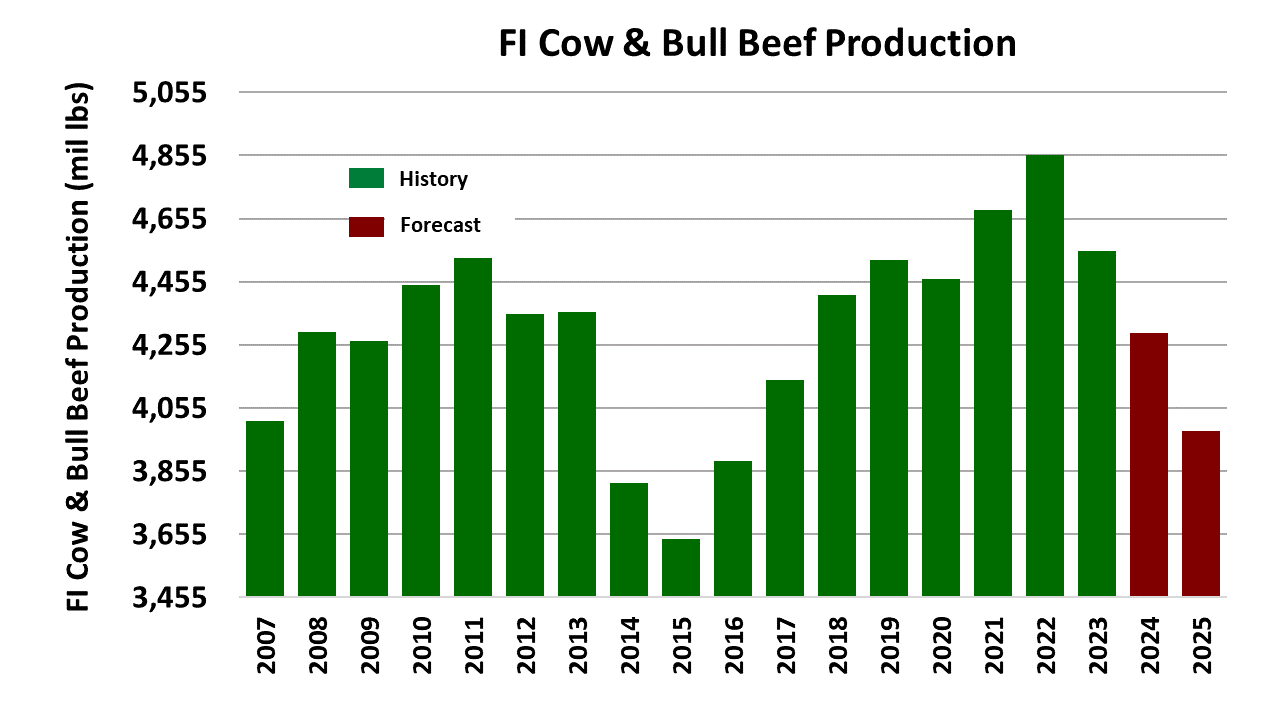

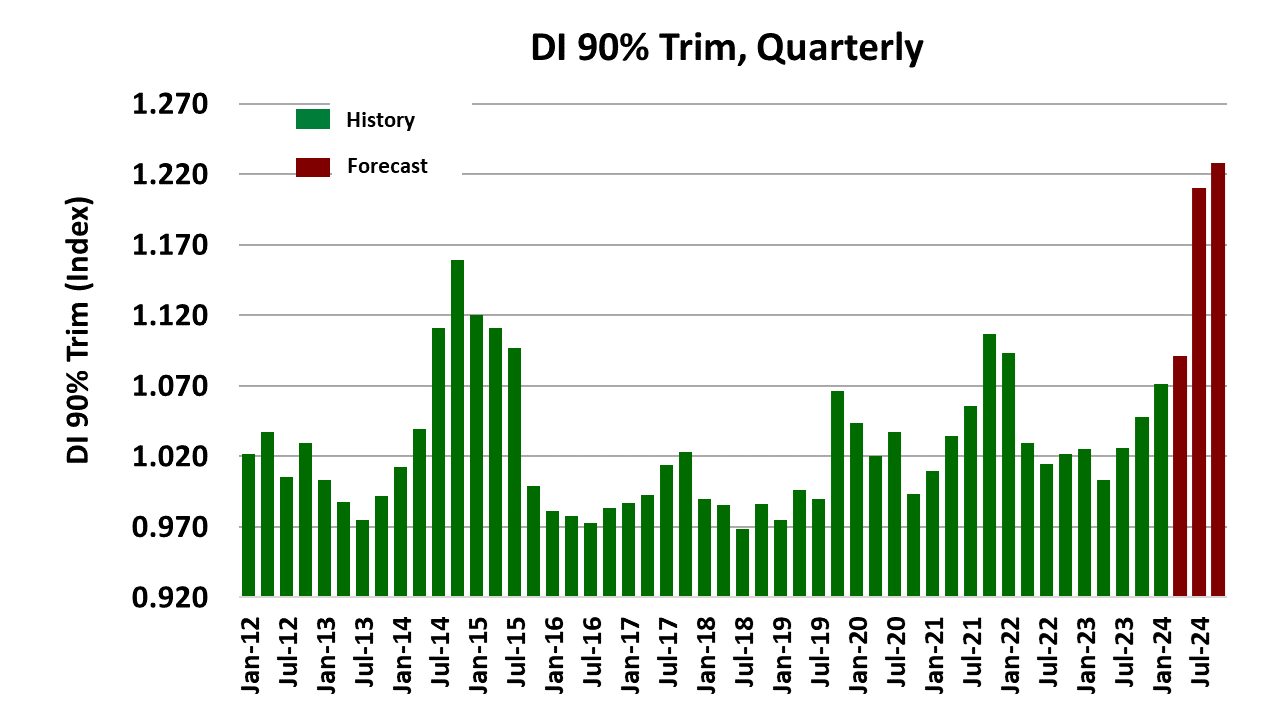

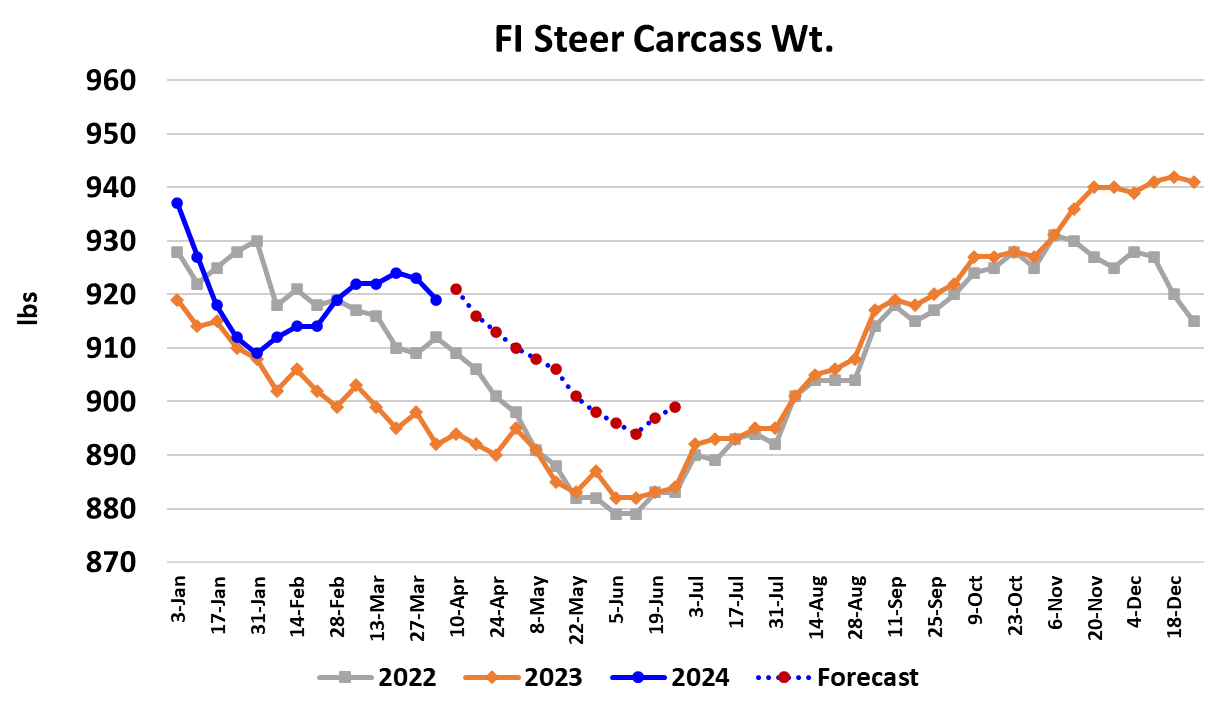

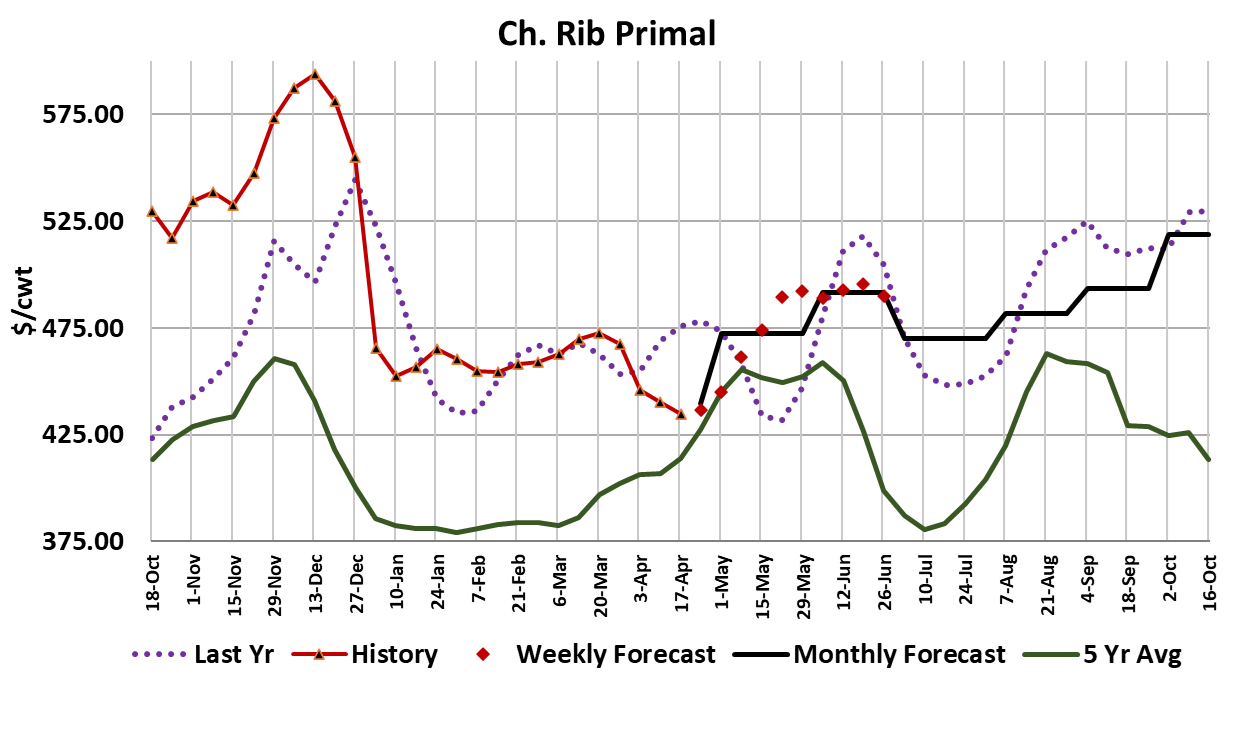

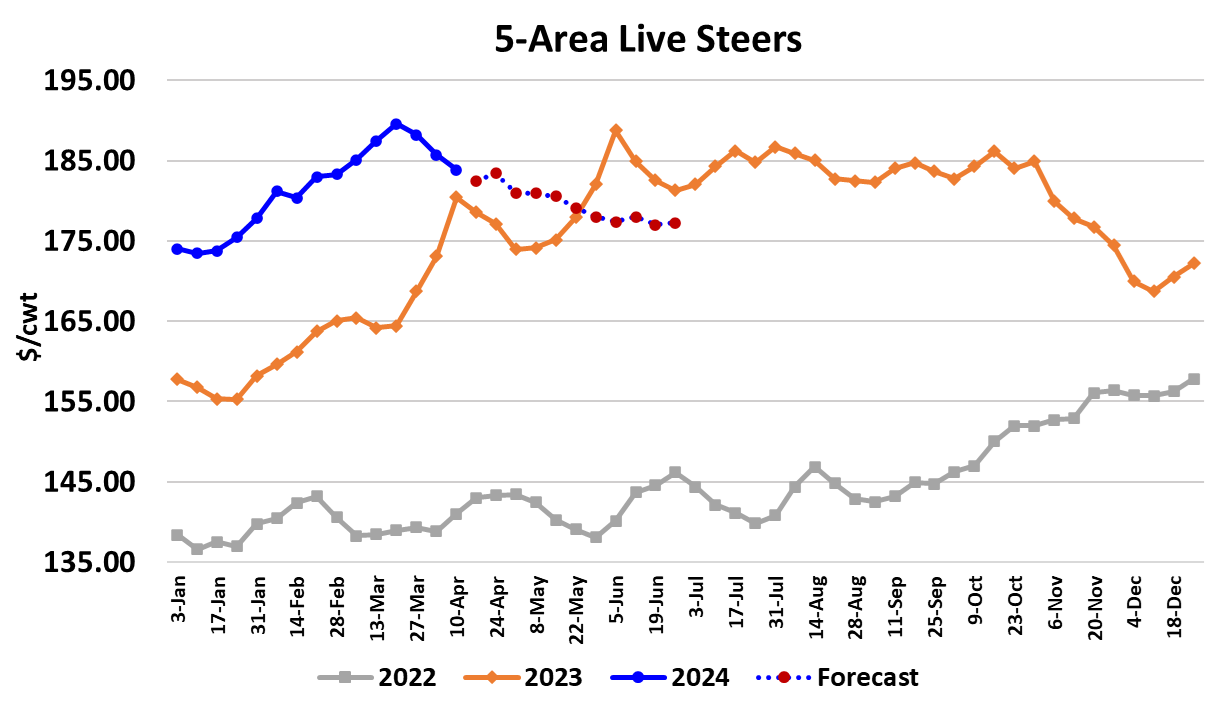

Prices in the cattle and beef complex slipped lower again this week, with the Choice cutout dropping $2.84/cwt. on a weekly average basis and the Select cutout losing $6.38/cwt. Cash cattle markets were mostly lower also and it looks like the 5-area weighted average will ring in somewhere close to $182.50, down about $1.25 from the previous week’s average. Trade in the Southern Plains was at mostly steady at $182, but prices in the North dropped over a dollar to $183. Despite all of those declines, the futures market posted a nice advance, with soon-to-expire Apr gaining close to $4 and the more deferred issues adding $4-5/cwt. on the week. Once again, the decline in the cutouts outpaced the drop in cattle prices and packer margins moved deeper into the red. I calculate the average packer margin at close to -$175/head this week. Cattle feeding margins are slightly positive at the moment, but if cash cattle prices decline just a little more, it could push them into the red. Cattle feeders are getting the benefit of declining breakevens because the cattle finishing today were put on feed last fall when feeder cattle prices were moving lower. Substantial declines in corn prices are also helping. The combined margin ticked a little higher this week, but it just looks like it is oscillating in a sub-zero range. The big question at the moment is “Where is the spring boost in demand?”. The rib primal normally sees strong gains from mid-April until mid-June, but so far that hasn’t shown up. It may still come, but many in the market are getting concerned that the failure of middle meat prices to advance is an early warning sign that beef demand is waning. It does look like beef demand is softer at the moment, but what is more difficult to discern is whether or not this is just a brief lull for a few weeks or a more pronounced downward shift in the demand curve that might persist for months. Right now, I’d cast my vote with the former, but don’t fully discount the latter. Two weeks from now middle meat prices could be advancing and the talk of weak demand would be forgotten. The fundamental forecast has a decent rally built into the middle meat prices starting in May, but it would be starting from a relatively low level, so the tops this year are likely to be below last summer’s strong levels. The thing that bothers me the most about the weak beef demand hypothesis is that lean trim prices continue to be very firm and that should set the tone for pricing in the end cuts from the fed sector. The attached graph shows that 90s prices did ease a tiny bit this week, but it is hard for me to believe that the top is in with Mother’s Day, Memorial Day and Father’s Day right around the corner. Non-fed beef production is rapidly declining following a drought-driven peak established in 2022, but we are still a long way off of the lows that were set back in the 2014-15 period when the last cattle cycle bottomed. So, while we may see some seasonal easing in 90s prices after mid-year, they are likely to come roaring back in 2025 and easily exceed what we’ve seen this year. The attached bar chart shows how the 90s demand index surged back in 2014-15 when animal numbers got exceptionally tight. That is a function of very inelastic demand by some users and when supplies get tight, prices get very high. If you are running a quick serve restaurant that sells hamburgers, you can’t run out of ground beef and will pay whatever it takes to source it. I think that we are just entering that phase in this round of the cattle cycle. That alone should provide substantial support to the demand side of the beef market in the next couple of years. Ground beef is a staple of lower income consumers while ribeyes tend to be consumed by higher income individuals. The current situation with strong 90s pricing and weak rib pricing would seem to suggest that lower income consumers are exhibiting stronger demand than those in the higher income brackets, or else there is trading down going on. Trading down normally happens in soft macro environment, but by most indications, the US macroeconomy is humming along just fine. So, I think the most logical explanation at the moment is that the spring middle meat demand is just a little late getting started this year and overall beef demand will look a lot better as we get into the May/June period. This week’s fed kill clocked in at 494k, a big improvement over the 480k kill the week before. Packers have more forward orders to deliver on in the next few weeks and that requires larger kills. There should be enough cattle out there to fuel weekly kills in the 500-505k range, but with packer margins so deep in the red, it is unlikely we will get there until June. My expectation is that packer margins will get much better moving through May as the cutouts advance, but cash cattle price stagnate or move lower. FI carcass weights moved lower for the second week in a row, but other data is pointing to an increase in weights when next week’s data is released. Steer weights are 21 pounds over last year and if weights advance next week as expected, they would be close to 30 pounds over last year. That is a bit concerning, but we need to recognize that weights last spring were unusually low. The front end supply of cattle is building, but kills are also poised to rise seasonally, so I think that the industry can get through this without a train wreck as long as demand improves and thus helps packer margins. Today’s Cattle on Feed report indicated that cattle feeders are working on the supply problem by sharply reducing the number of animals put on feed. USDA’s survey found that placements during March were down 12.3% YOY and total feedyard inventories as of April 1 were only 1.5% higher YOY instead of the 2-3% higher that many analysts were expecting. That is supportive to cattle pricing this fall and the futures will probably indicate that on Monday morning, but it doesn’t do much for the near-term cattle supply and pricing situation. However, if placement activity remains light in April, we could easily see on-feed inventories equal to or below last year when the next Cattle on Feed report is released. For now though, it is a waiting game for the bulls. Waiting for spring demand to kick in; waiting for packer margins to improve; waiting for feedyard inventories to shrink; waiting for the price gains that a shrinking cattle herd promises.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}