Beef Wrap May 3

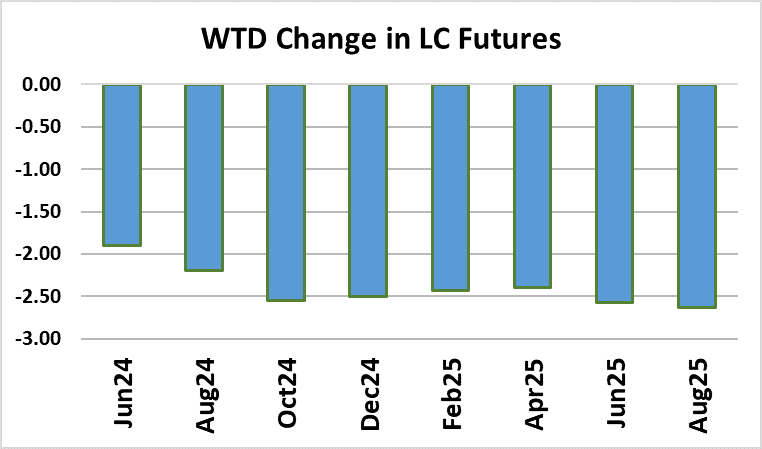

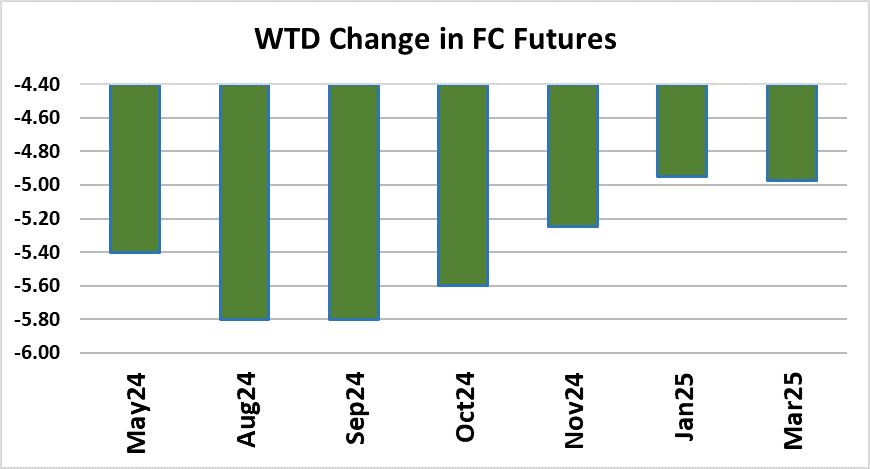

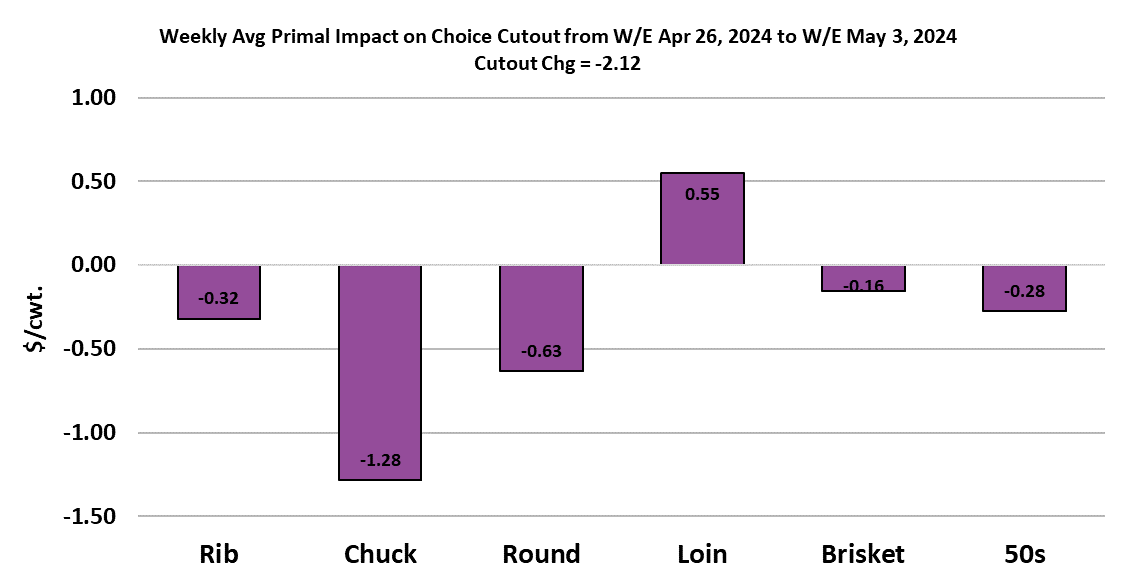

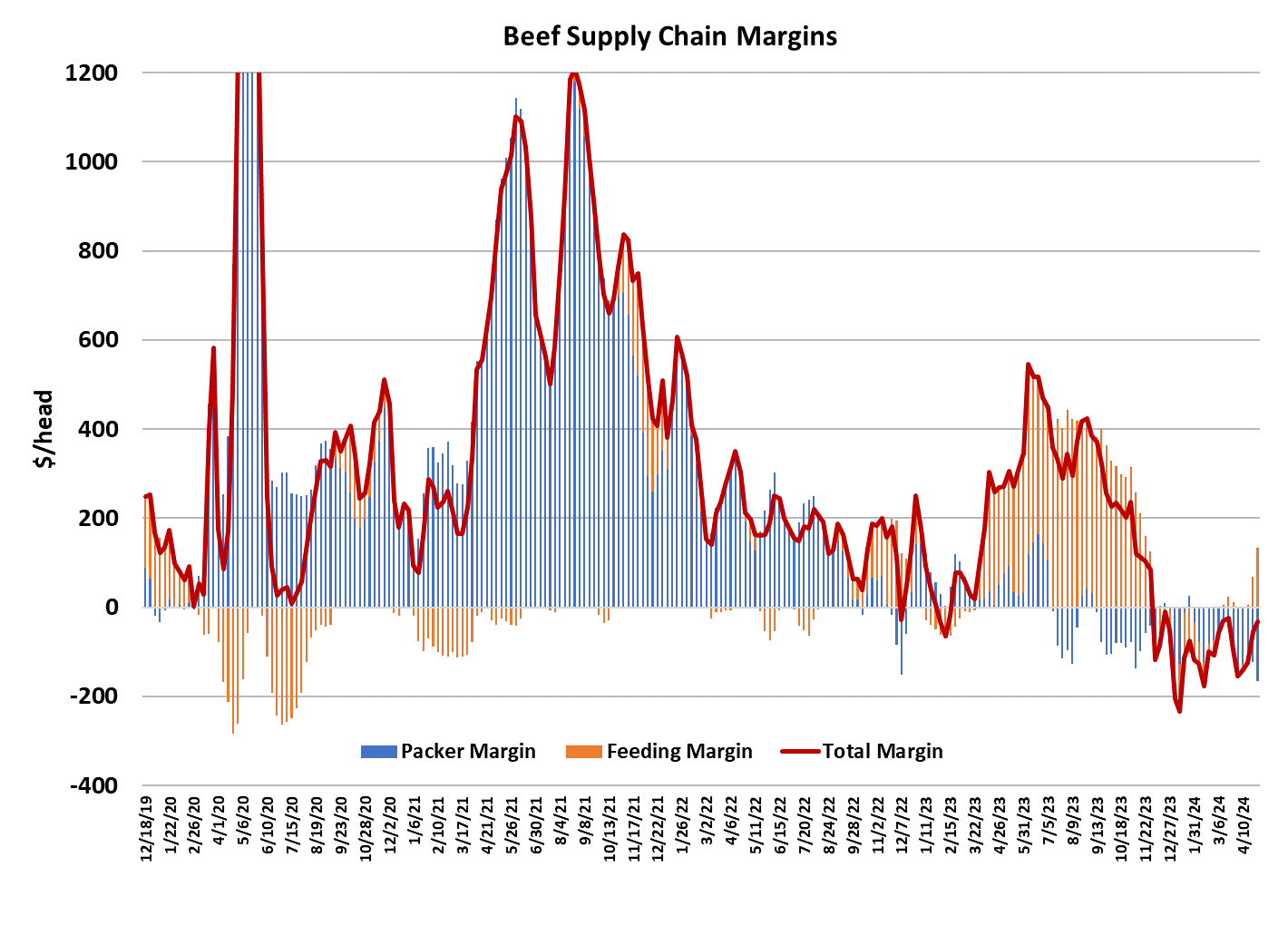

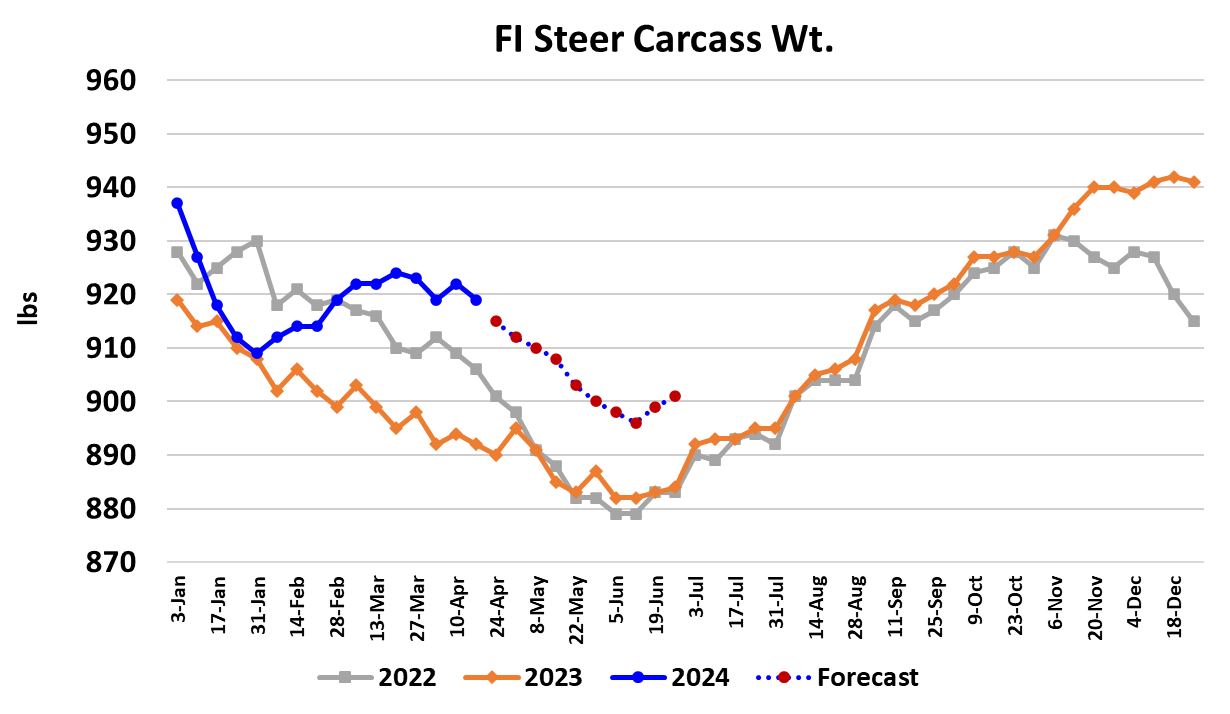

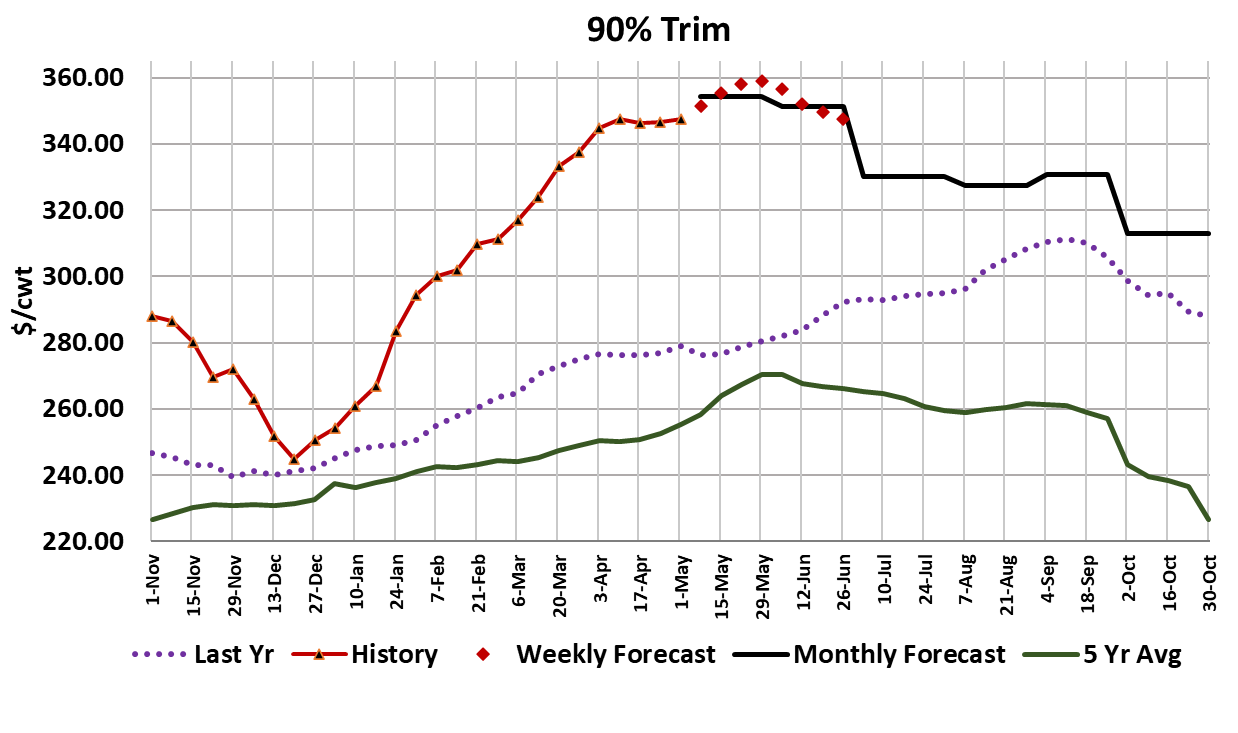

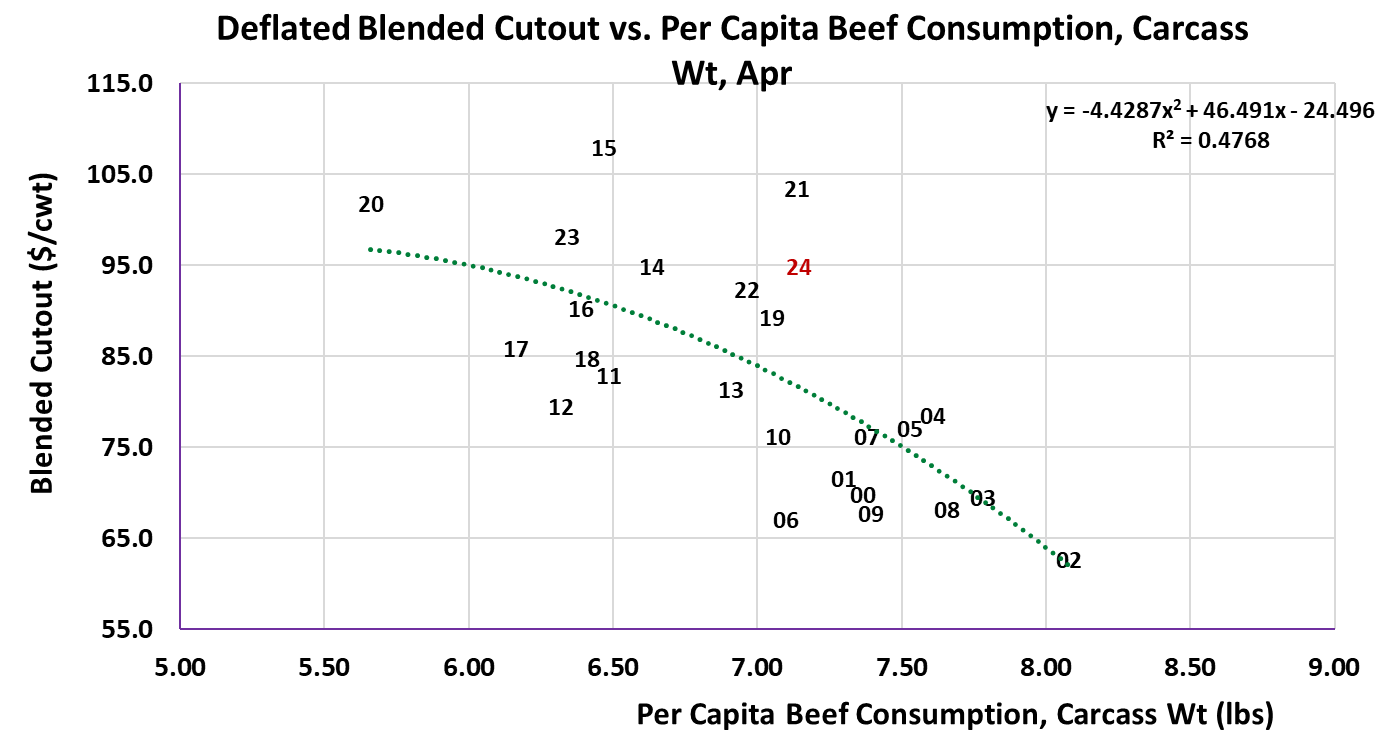

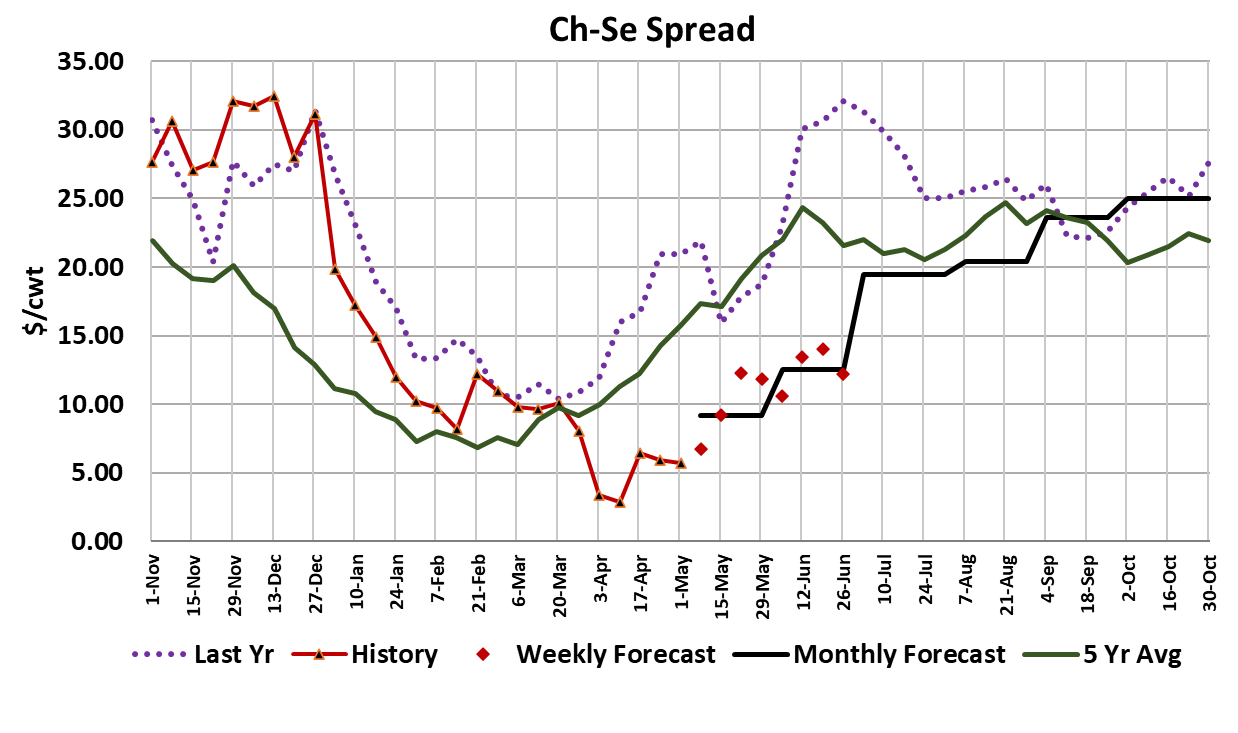

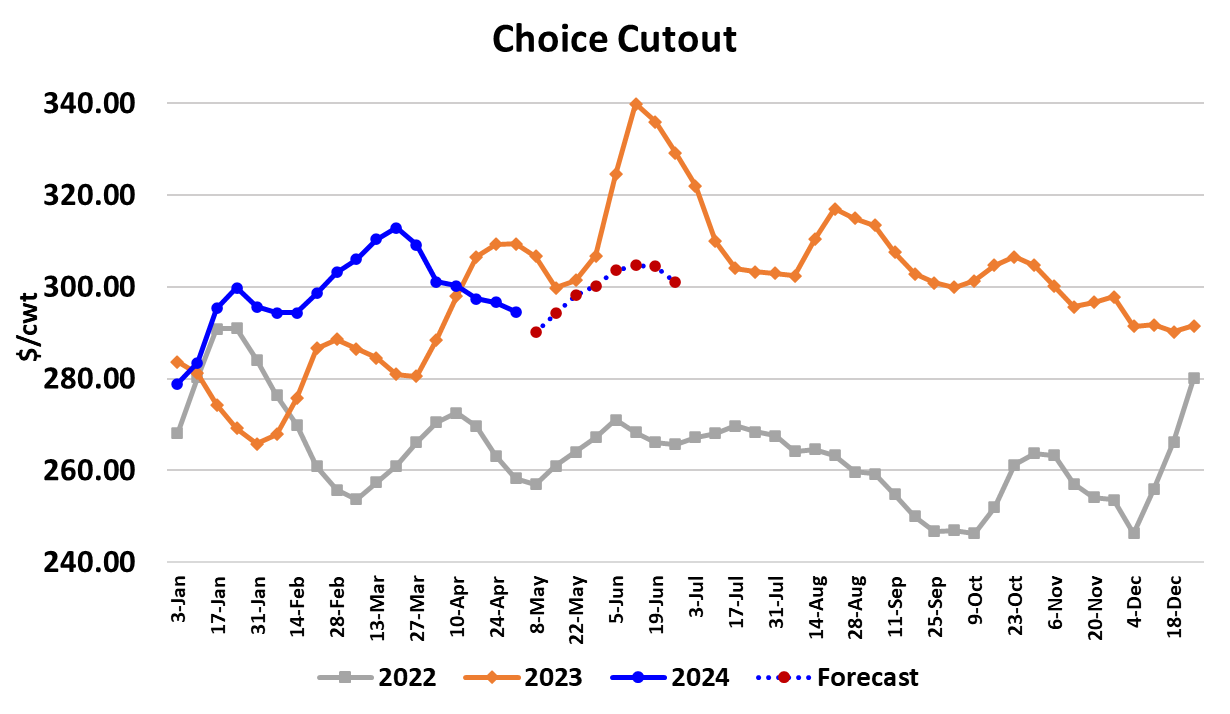

The avian influenza story reared its head again this week as government officials announced they would be testing for traces of the virus in ground beef. That sent the futures sharply lower as traders assumed that, similar to milk, fragments of the virus would be found in beef. Then on Thursday, it was announced that all 30 samples came back clean and the futures rebounded sharply. For the week as a whole, the summer futures were down about $2/cwt. In the background of all this noise, the cash cattle market was trading higher with prices in the North trading steady to $1 higher at $186-187 and trade in the South coming in a full $2 higher at $184, with some trades being reported higher than that late on Friday. When it is all said and done, it looks like the 5-area weighted average price will be close to $186, up about $2.50 from the week before. This is the second week in a row where cash cattle prices have advanced, yet futures traders seem skeptical that it will last. There are a lot of good reasons for that. The normal seasonal tendency is for cash cattle prices to move lower from April to June as available supplies of market-ready cattle increase. There is also considerable concern surrounding carcass weights, which are now running 27 pounds over last year for steers. The FI steer weights did move three pounds lower this week, so perhaps that is a sign that they will now honor the seasonal trend and work lower into June, but it is still adding a lot to YOY beef production. Finally, there are the issues of sluggish beef demand and poor packer margins, which should limit packer’s desire to slaughter aggressively and thus make it more difficult to work through the front end supplies of cattle. It is pretty amazing that this is the first week of May and the beef cutouts moved lower again. The Choice dropped $2.12 on a weekly average basis to $294.51 and the Select was off $1.91 to $288.77. Given that packers paid up for cattle last week, the lower cutouts put further pressure on packer margins, which are now close to $165/head in the red. May normally sees some of the best packer margins of the year, so something is clearly amiss here. One would think that packers would be slashing the kill, but just the opposite is happening. This week’s fed kill came in at 501k—the largest fed kill since late January—and up 6k from the week before. I think packers have some forward commitments to deliver on in the next two weeks that is causing them to kill more than they would like. The bigger kills will help feedyards clear some of the cattle backlog, but certainly not all of it. Cattle feeders have navigated this difficult market masterfully over the past few weeks. Cash cattle prices peaked at $188, then the avian influenza story broke and helped to push prices down to $182 over a three-week span, and now in the last couple of weeks cash has risen back to within a couple of dollars of the spring top. Clearly, the cash cattle market did not fall apart like some were expecting. In fact, if the “black swan” avian influenza situation hadn’t come along, the cash market might not have even dipped at all. Cattle feeders displayed a lot of discipline by not panicking in the face of the avian influenza event and it has paid off. I calculate cattle feeding margins currently near +$135/head and they are set to expand further in the next few weeks as feeding breakevens are declining rapidly. The combined feeder+packer margin is just below zero now and has been oscillating in negative territory since last fall. This week the only primal that posted gains was the loin, and it was up only slightly. The failure of the rib primal to advance at this point in the calendar is somewhat baffling. Perhaps retailers have just pushed prices for the premium cuts so high that they have finally choked off consumption. Or maybe the rib rally is just a little late getting started this year. If that is the case, the there is risk that the peak in the cutouts could come later Memorial Day, which is typically when the high water mark gets set. The fundamental forecast has the cutouts moving a little lower again next week and then rising through May and into June with the peak in the Choice cutout coming around Father’s Day near the $305 level. The Choice-Select spread was a little less than $6 this week, which is well below the five-year average of $15.75. It is hard to know if the Choice-Select spread is at such low levels due to demand for Choice being unusually weak or demand for Select being unusually strong. A case could be made for the latter, since Select end cuts would be the preferred substitute for sky-high lean beef. The 90s continue to defy gravity and inched a little higher this week after a couple of sideways weeks. My guess is that they will make one last push higher over the next few weeks before easing lower through summer. The official trade data for March was released by ERS today and it showed total beef exports down 10.4% YOY. That wasn’t surprising, given that it has been almost 2 years since a YOY increase in beef exports has been reported. With the US beef cattle herd shrinking, it may be another 2 years before we see another YOY gain in exports. Next week, it will be packers on the hot seat, trying to conjure more money out of beef buyers to help cover their rising cattle costs. If there was ever a time when the odds of success favored packers, it would be early May, but so far this year not much has been going their way.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}