Beef Wrap April 23

The cash cattle market felt soft again this week, but the weekly

average cash price for the live trade was only down about $0.70 to

$121.36. Part of the reason that it felt soft was that there were

some cattle feeders that accepted prices below $120, although the

average suggests there weren’t too many of those. The dressed

trade was decidedly lower, down over $3 from the week before to

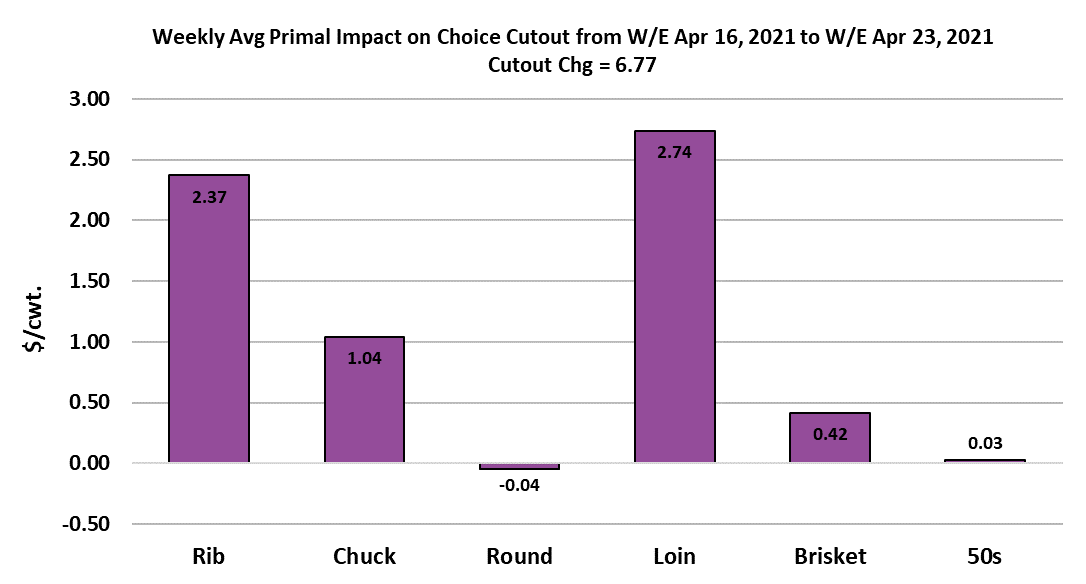

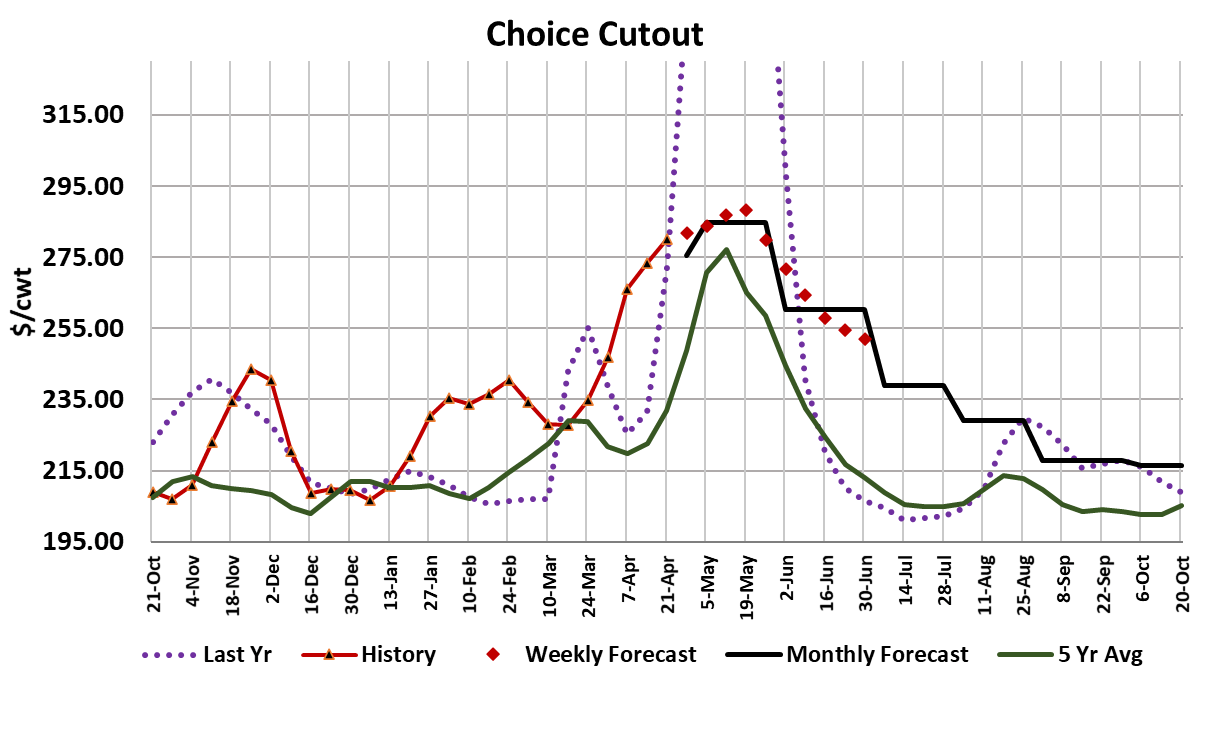

$192.11. The beef markets were stronger yet again, with the

Choice cutout adding almost $7 on a weekly average basis and

the Select cutout up almost $4. When the beef goes up and cattle

prices go down, that is a sure sign the packer margin is growing

larger.

My calculation has packer margins this week at $606/head. The

drop in cattle prices has cattle feeding margins now in the red by

about $140/hd. Such inequity in this market. I had hoped that as

beef prices rose this spring, packer margins would hold around

$300/head and that would allow cash cattle to participate in that

rally, but apparently the social distancing in plants has reduced

throughput enough to where packers don’t have to compete very

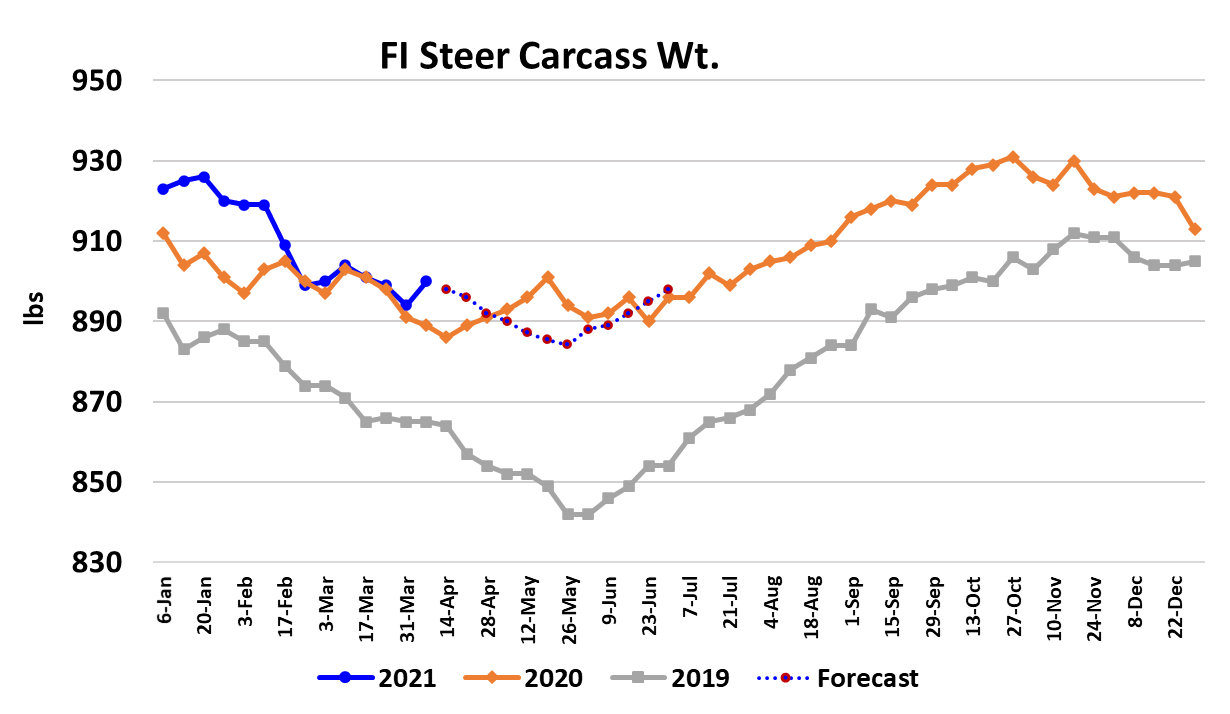

hard to fill their kill schedules. Carcass weights are the one

fundamental factor that have been looking bearish lately. I’m

really concerned that they might not decline much more from

current levels and thus start their seasonal increase from a much

higher point than normal. That would be decidedly negative for

cattle feeders and decidedly positive for packers. With corn

futures now at $6.50/bu, one would hope that cattle feeders would

cool down the rations and not put a lot of extra weight on the

cattle. So far that doesn’t seem to be happening.

Packers were skillful at anticipating the spring cattle tightness

created by limited Q4 placements and they forward booked a lot of

cattle for Apr/May delivery. Packers are also pretty skillful at the

art of jacking up beef prices in periods of strong demand by

forward selling just enough that the spot market stays tight for beef

and that runs negotiated beef prices higher and all of the formulas

that are based on those negotiated prices also pay up. Packers

want to take full advantage of their margin improvement and they

did that this week by putting together a huge Saturday kill. The

weekly total on steer and heifer slaughter looks like it will be close

to 525k—about 30k more than what our flow model suggests

should be available right now.

Doing a kill that big before May even arrives creates some risk that

it will compress packer margins by lowering the cutouts next week

while making feedyards more current and increasing the odds of a

cash cattle advance next week. My guess is that demand is so

strong that the extra beef will be easily gobbled up by the market, at

least on the Choice side, and the cutouts will continue higher next

week. The Choice is now only $6 below my (revised) spring top

target of $290 and I fear that forecast will need to be raised to $300

soon. The combined margin just keeps working higher and is now

higher than the spring 2017 market, which was very strong.

This is going to end up being the strongest demand cycle in the last

five years outside of the COVID spike from last year. Pork demand

has continued very strong also. Retailers have no cheap options

for features this spring. My guess is they have already set their ads

for May and beef plays a big role in those. They may have to

increase their feature prices to help keep their margins from getting

crushed too much, but I really don’t think consumers will bat an eye

at higher prices.

I’ve said before, there is something very unusual going on in the

demand for animal proteins. This does not seem to me to be a

normal 6-8 week cycling demand. Demand is very, very strong

and will likely stay that way for at least a couple more months and

possibly for many more months. Buyers need to adjust and be

prepared to pay a lot more than they are used to for red meat items

this spring and summer. Adding fuel to the fire, today’s Cattle on

Feed report showed feedyard placements more than 5% below

what analysts were expecting. This week I raised all of my packer

margin forecasts in light of recent developments and that, of

course, lowered my cash cattle price forecasts. Next week watch

those carcass weights and the DTDS for some signs that cattle

feeders are seeing improved currentness. Also watch the cutouts

as demand gets tested by this week’s much bigger beef production.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}