Beef Wrap April 16

The weekly average of cash cattle traded live this week was $121.93,

just a hair under the $122.01 posted last week. The dressed trade

came in at $195.63, slightly above last week’s average of $195.30. So

it is safe to say the cash cattle market was essentially flat this week,

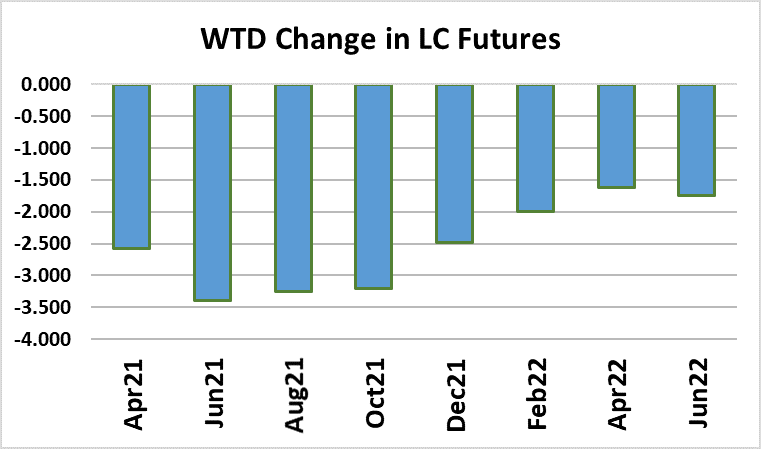

but boy it sure didn’t feel like it. The futures board was down hard and

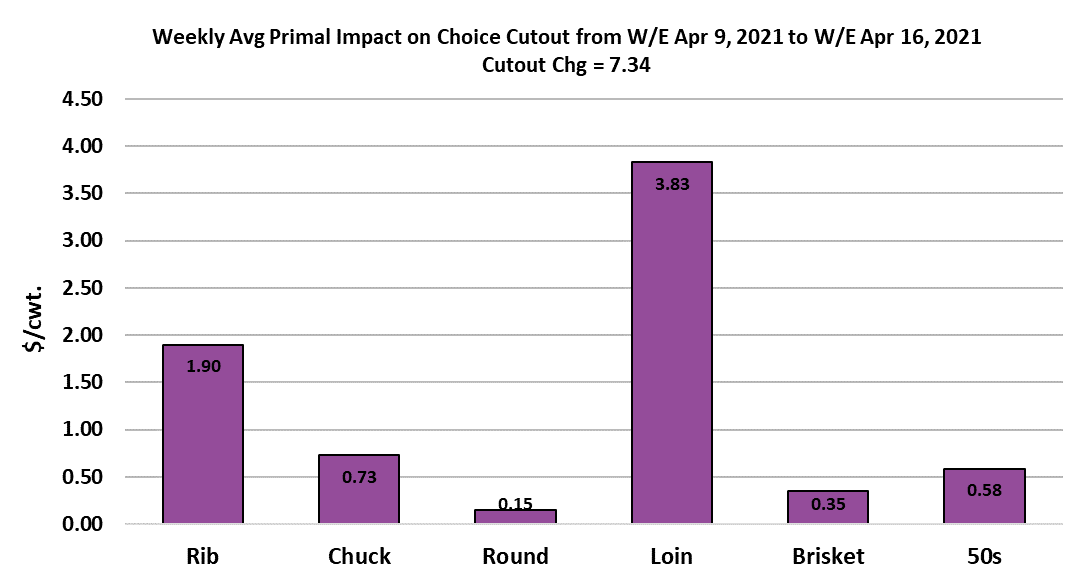

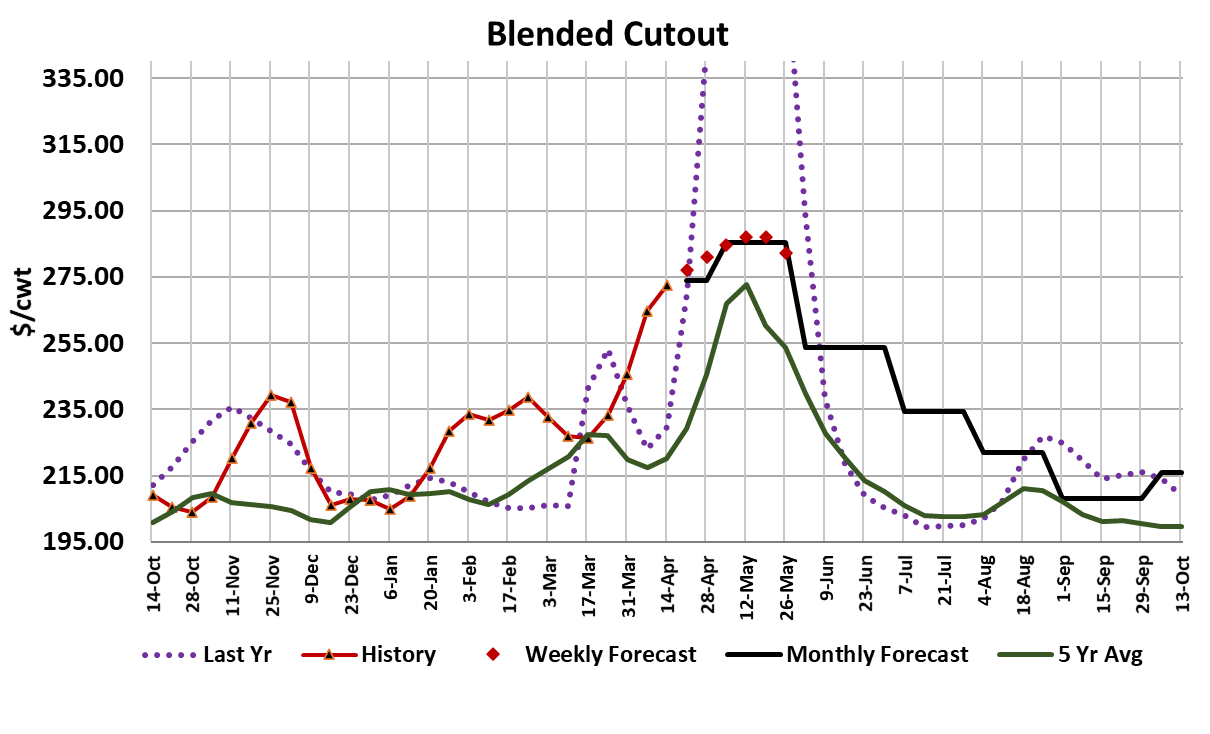

that seemed to suck all of the life out of the cash market. The cutouts

continued to move higher this week, with the Choice up over $7 and

the Select gaining more than $10.

With such a robust beef trade this week, one would have thought that

the futures market would have been a little more optimistic. But the

story was essentially the same in the pork market, where the

fundamentals held solid yet the futures sold off in a big way. It is

almost as though futures traders suddenly “lost faith in the future.”

Just last week they were buying both cattle and hogs like there was no

end in sight, but this week their psychology turned. I think that the

hog market meltdown helped exacerbate the softness in the cattle

market. A big part of the bull story in cattle has been the idea that pork

is going to be very expensive this summer. That story took a hit when

the hog futures started to move lower. The new sales numbers in the

weekly export report looked a little light this week for both beef and

pork, but that should have been expected given how pricey both have

become. Cargill had some software problems at its Dodge City plant

that caused them to do lighter kills than normal and perhaps that

spooked futures traders. That plant should be back to full speed on

Monday.

Now that the Jun futures are no longer premium to the spot market, it

reduces cattle feeder incentive to hold out for higher prices in the

future, particularly if the cattle are hedged. With the cutouts rising and

the cash cattle market remaining essentially flat this week, packer

margins moved up to $530/hd. The fed kill looks like it will come in

around 497k, down almost 20k from the week before. That looks to be

just a tad bit over what the flow model would suggest for this week.

Packers may want to increase the kill next week to capitalize on strong

margins, but they will need to be careful of running their inventories

too low and thus giving feeders an opportunity to advance the cash

market. Cattle supplies are tight in the North and packers are buying

cattle in TX and KS and trucking them to northern plants. The market

should be moving solidly into the hole created by light placements last

fall and should give cattle feeders some leverage. Futures traders

may think that the top in the cash cattle market has been made, but I

can guarantee that cattle feeders don’t see it that way. The truth will

be exposed by the demand side of the market.

If demand continues to run super strong, then that could move the

Choice cutout to nearly $300 before all is said and done and I would

be very surprised if the cutout reaches that level and the cash cattle

market remains unchanged. The combined margin advanced again

this week, but at a much slower pace than in recent weeks. Once

again, it looks like it is making a top, but it did the same thing a few

weeks back and then continued higher, so I’m not quite ready to call

this a top in the demand cycle. Beef 50s finished the week over

$100, which seems pretty bullish to me. Carcass weights moved a

little lower but are poised to rise next week and that is a bit

concerning. However, the price of 50s doesn’t make it seem like

cattle are carrying an abundance of fat. Packers will be needing to

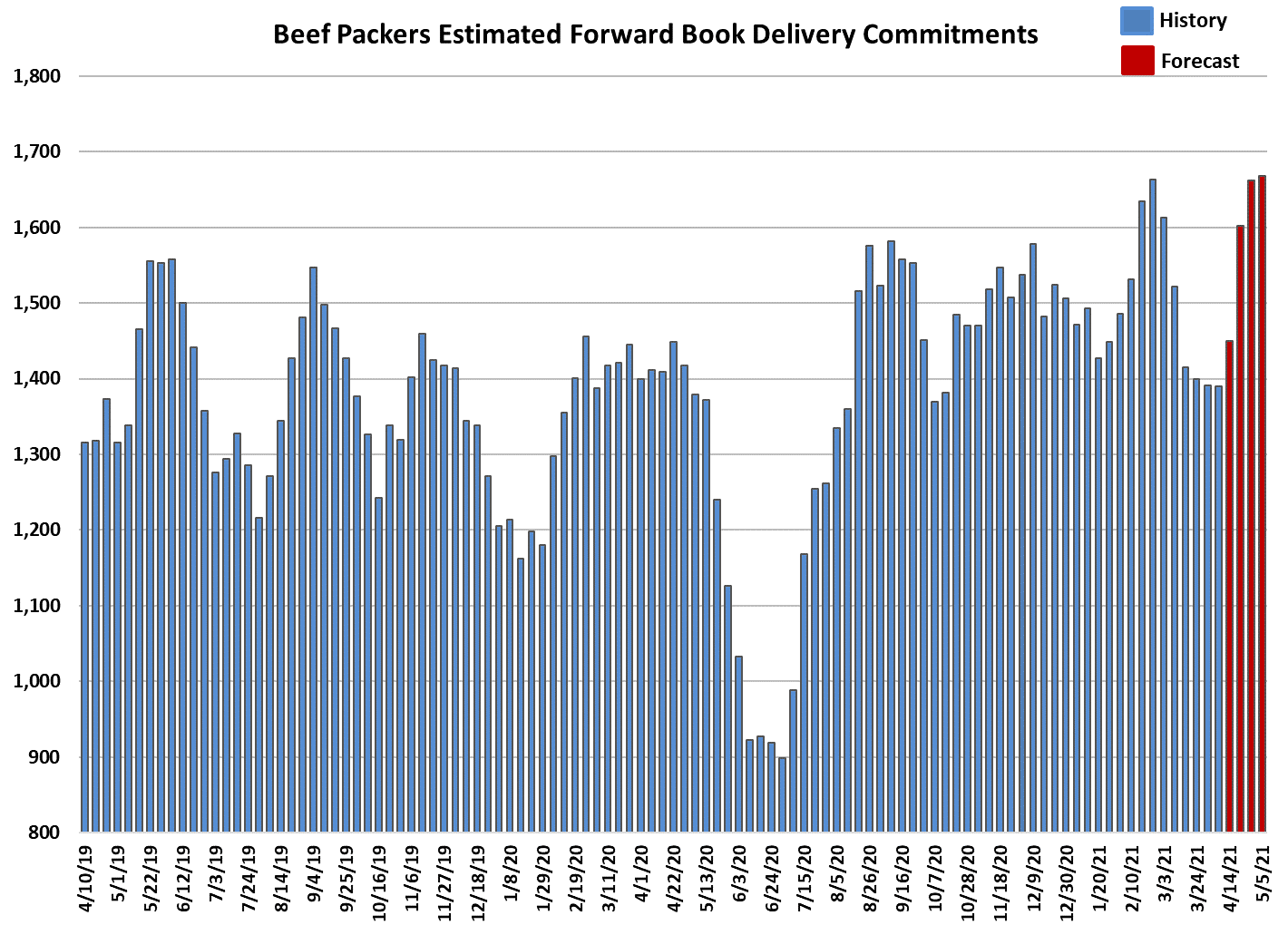

deliver on a large amount of forward-promised beef in the next few

weeks (chart to the right) and in my experience, that is a very important

factor in forcing packers to pay higher money for cattle. Feeders

know this and will likely try to capitalize on in the next few weeks. It

is pretty clear to everyone now that the spring market for beef is

going to be very good. An important question is what happens after

Memorial Day.

With the Jun futures selling off this week and moving discount to

Apr, traders seem to be saying that beef demand is going to wane

as we move into June. That might happen, but all I can say is that

we haven’t seen much waning of either beef or pork demand in the

past few months, so this doesn’t seem like a normal demand cycle

that fades every couple of months. Now of course, kills will be

expanding in June and that could pressure the beef market after

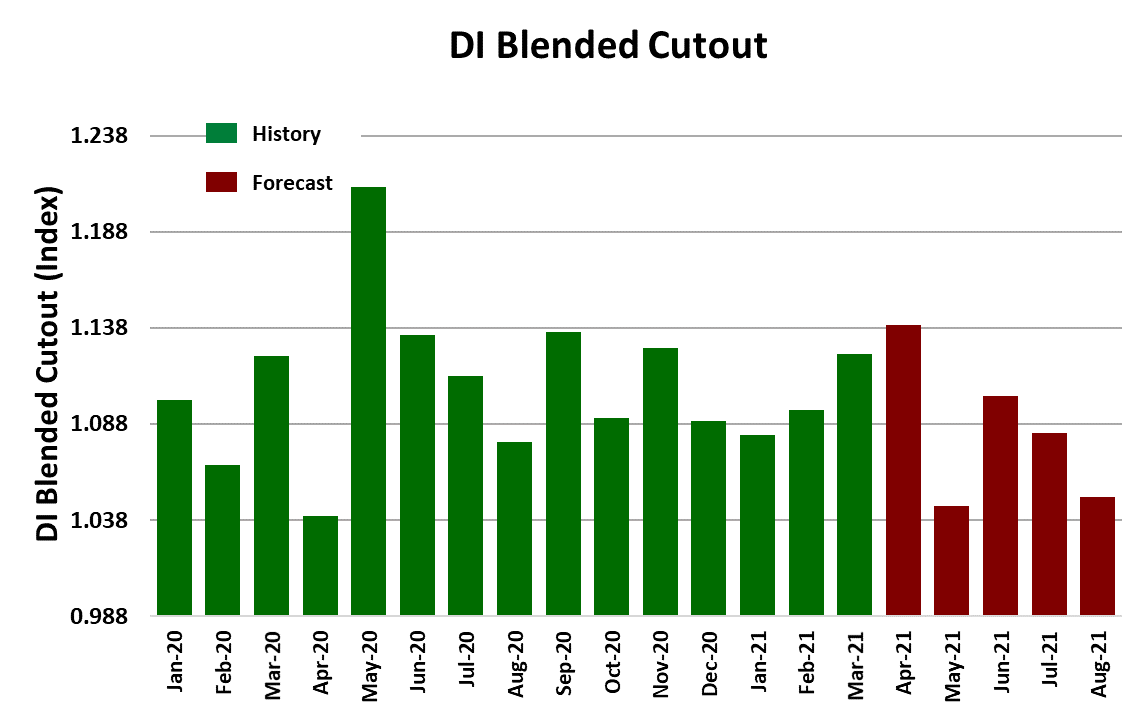

Memorial Day. The bar chart to the right shows the historical demand

indexes by month for the past year and what I’m assuming for

demand over the next few months. Note that Apr is looking like the

strongest demand month since the plant shutdowns in May 2020.

Demand has been steadily increasing since January. I’ve got May

demand toned way down because if I didn’t the tight supply would

force my price forecasts off the chart. But, the decline in demand

from Apr to Jun to Jul to Aug is apparent. So, I’m not expecting the

current demand strength to last forever. Next week we will get a

COF report and it is likely to show a huge YOY increase in

placements, simply because of the sharp reduction in March

placements last year when COVID broke. Still, there is a risk that

the computers trading the market will see a 30%+ increase and

placements and go into selling mode.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}