Beef Wrap April 30

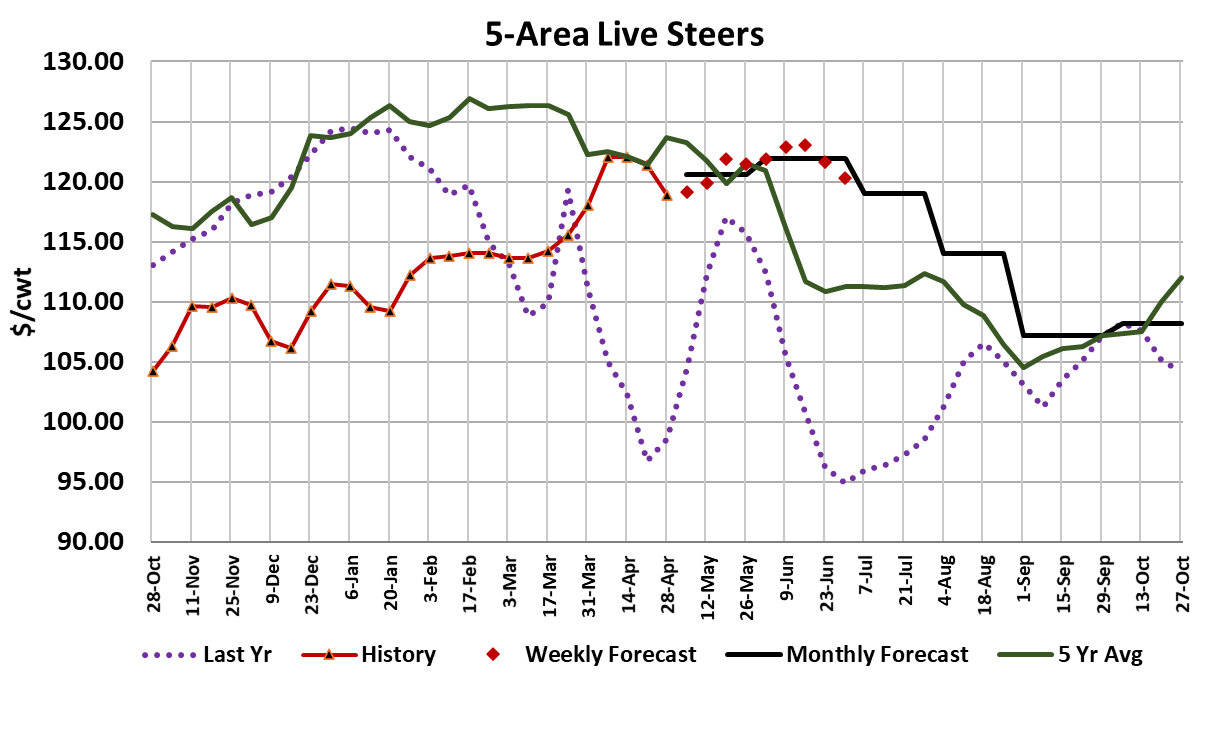

Cash cattle averaged close to $119 this week, down about $2 from

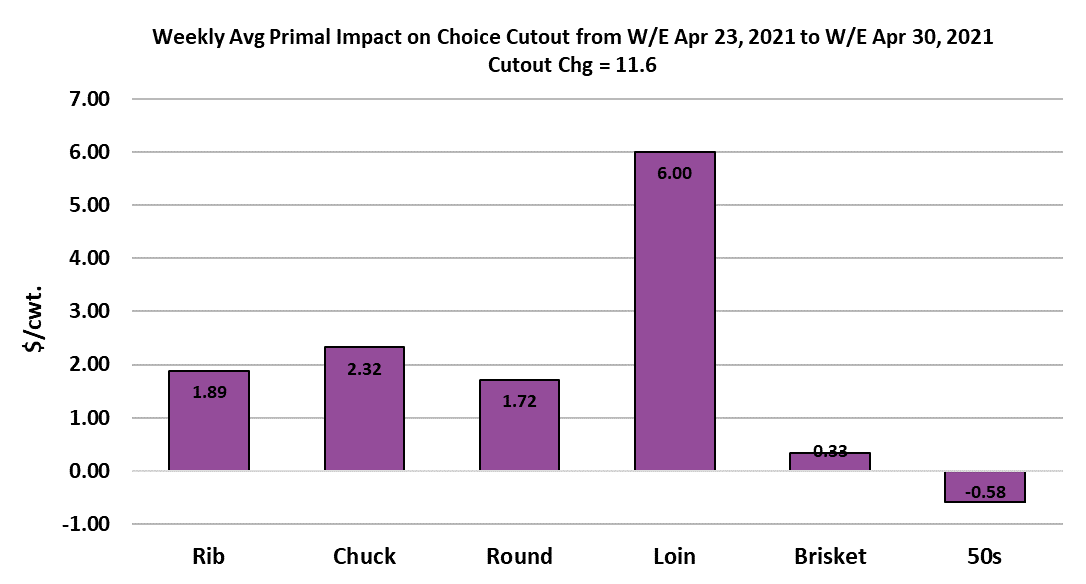

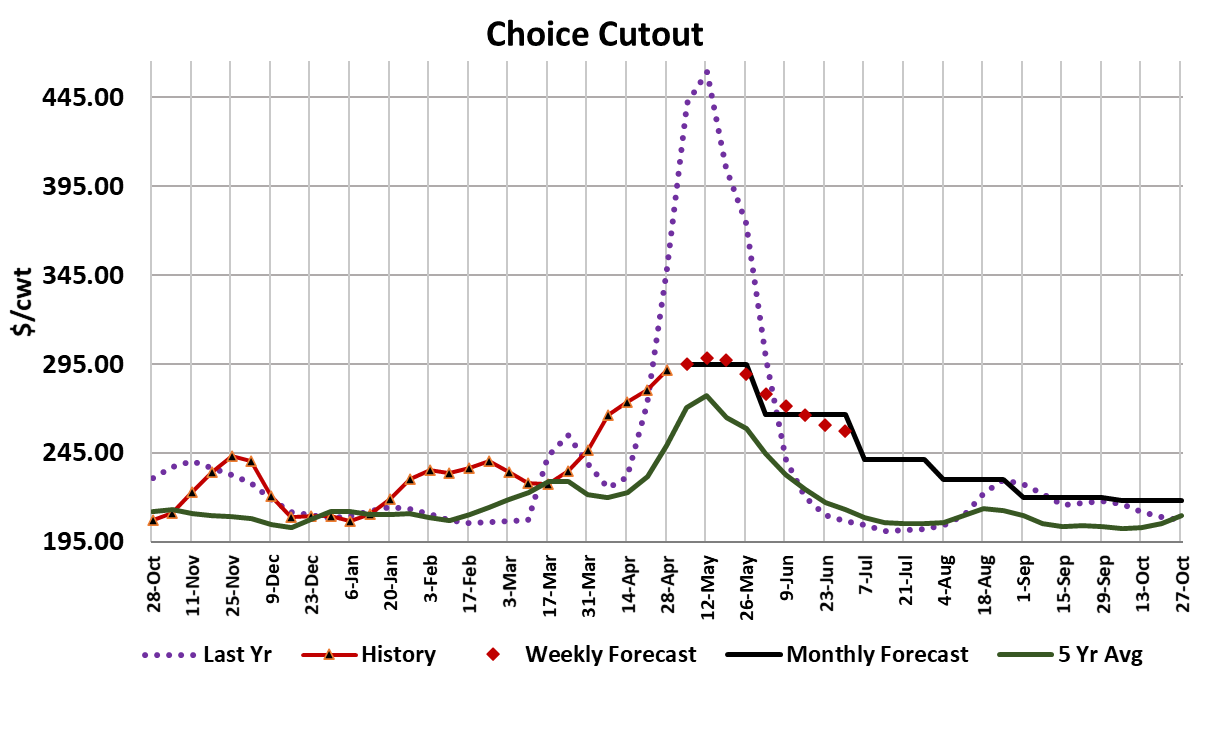

last week’s average. The cutouts were headed in the other

direction, with the Choice gaining $11.60 on a weekly average basis

and the Select up $7.68. At the end of the week, the Choice cutout

was approaching $297 and yes, I had to revise all of the beef price

forecasts upward once again. The scary thing for beef buyers is

that the calendar is now rolling into May, which is when the really

strong beef demand normally appears.

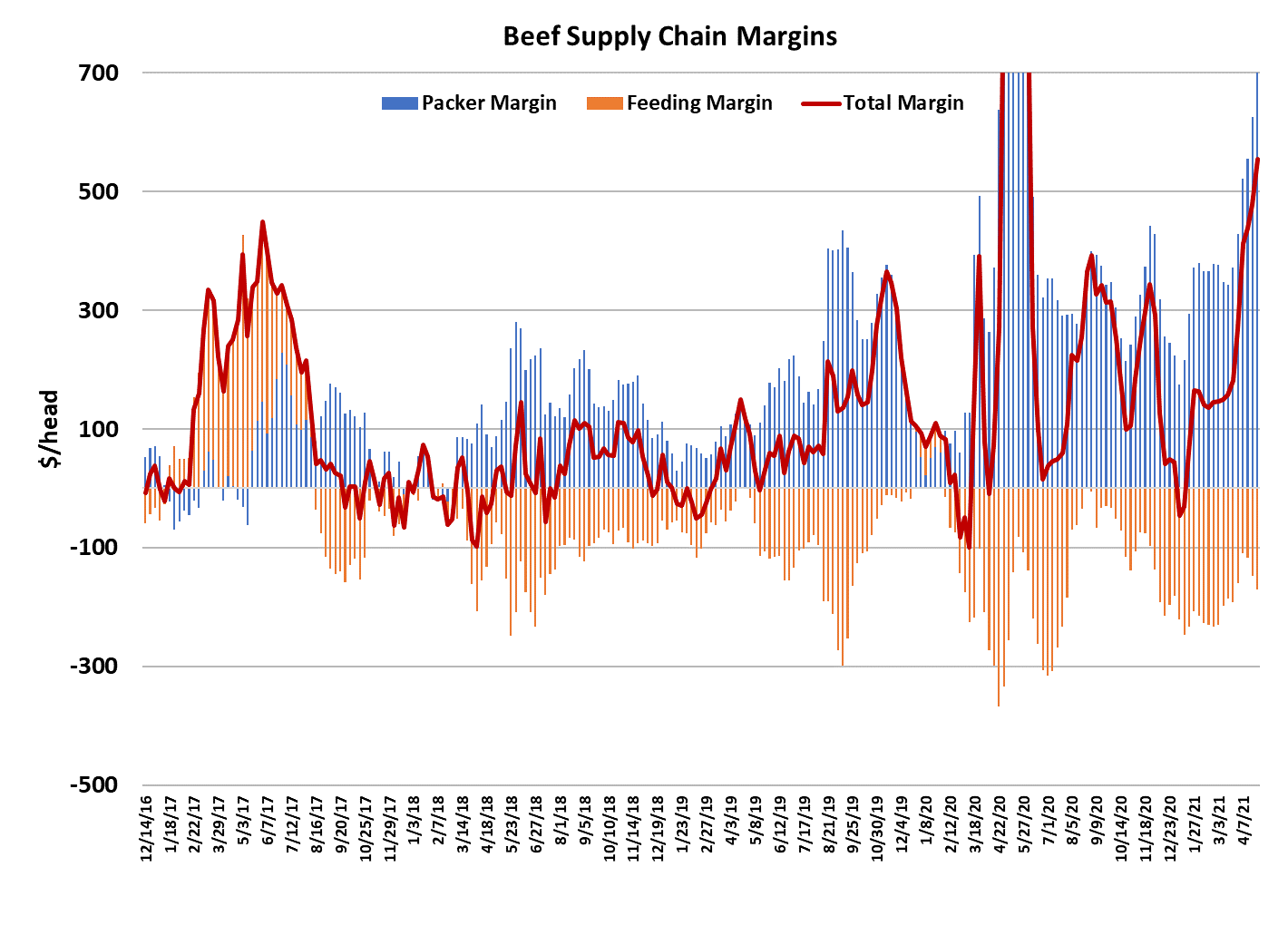

I calculate this week’s packer margins were close to $735/head and

am forecasting next week’s margins near $800/head. It is really

good to be a beef packer these days. One interesting aspect of this

rally in the beef market is that the end meats are moving higher at a

time of year when they are normally shunned by consumers. I think

that fits with the idea that renewed consumer interest in high protein

diets is helping to fuel this incredible spate of demand strength.

Consumers following high protein diets will often deviate from the

normal seasonal consumption patterns, simply because they are

consuming so much protein that variety is desirable. The 50s were

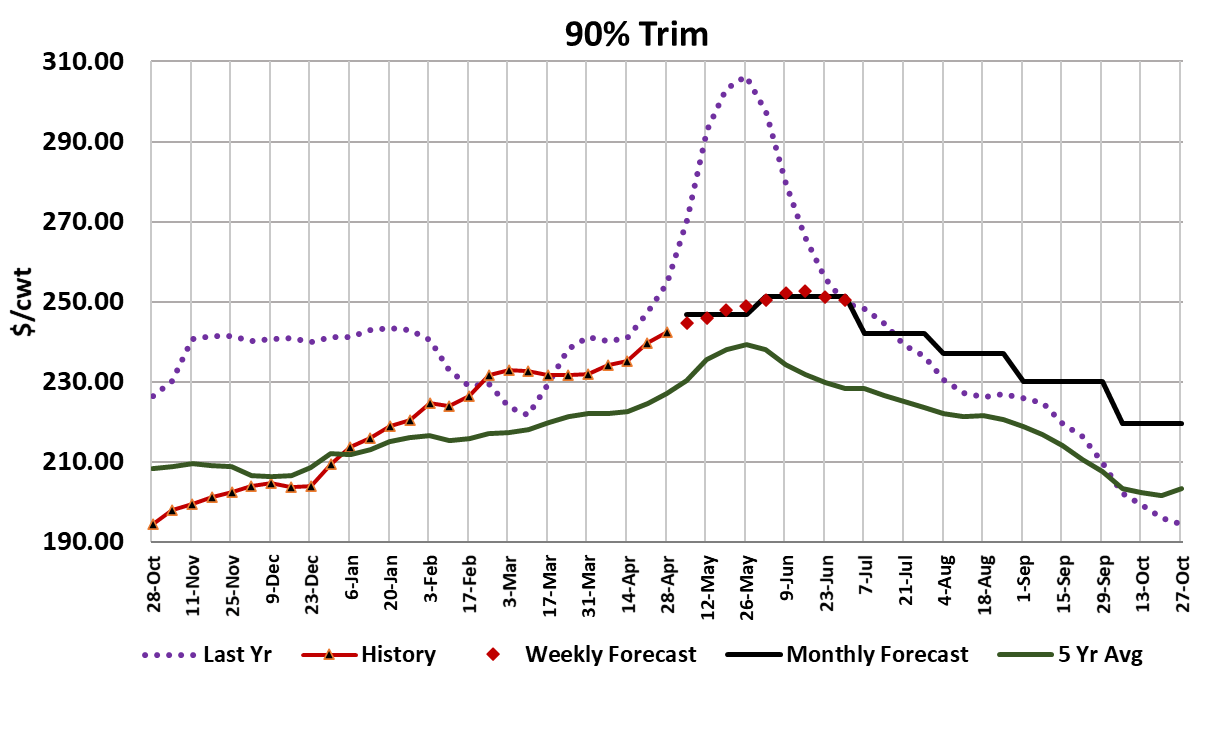

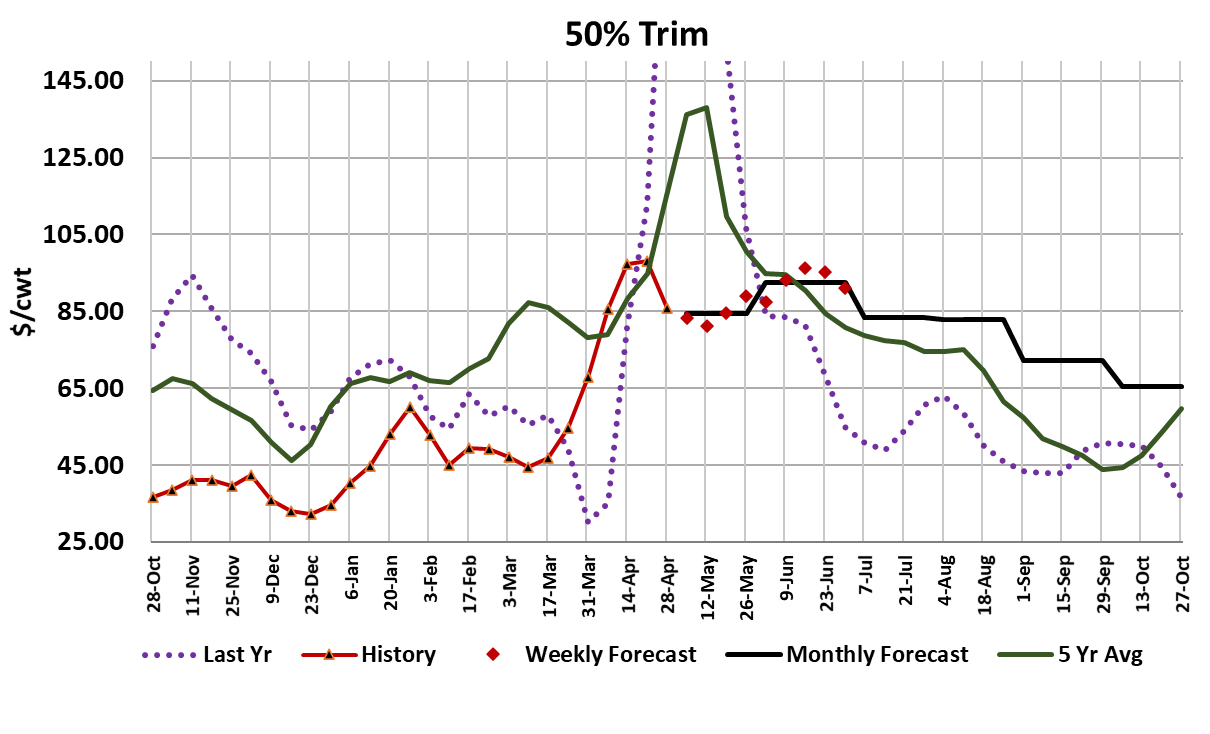

the only item that didn’t contribute strength to the cutout, but by the

end of the week 50s prices were starting to move higher once again.

90s have been on a solid upward trajectory for months. With the

muscle cuts getting so expensive, I would look for retailers to start

putting more grinds in their ads over the next couple of months and

that should keep the trim markets relatively firm. The recent

weakness in the 50s may be tied to carcass weights not declining in

normal seasonal fashion this spring.

This week, USDA reported steer carcass weights down 2 pounds,

but heifer carcass weights up 8 pounds. That means the blended

carcass weight moved higher—something that is not normal at this

time of year. The YOY chart to the right shows that blended weights

appear to following last year’s abnormal weight pattern rather than

declining rapidly toward a bottom in mid-May. To me, that is

somewhat confounding because nearby corn futures closed the

week at $7.40/bu and one would think that high corn prices would

prompt cattle feeders to tone down the energy component in rations

somewhat and that would be reflected in weights. That is not the

only unusual thing that cattle feeders are doing in this period of high

corn prices. They are also placing a high value on lighter weight feeder cattle.

Data from feeder cattle auctions over the past few weeks shows

that the price spread between light and heavy weight feeder cattle

is hovering near traditional levels. In times of high corn prices, it

makes financial sense for cattle feeders to shun the light weight

feeders and increase their demand for heavy weight cattle, which

require less corn to reach market weight. So, there are a lot of

things going on in the feedlot sector right now that don’t seem to

make a whole lot of sense.

This week’s fed kill registered 509k, down sharply from last week’s

total. It was still a little more than the flow model suggests should

be ready for slaughter at this time. We know that packers can

slaughter at least 525k of steers and heifers, because they have

achieved that level several times during the pandemic. So, why

didn’t packers attempt to reproduce last week’s 523k fed kill this

week when margins were well over $700/head? One would think

that with margins that strong, they would be trying to push every

animal they could through the plant this week. It is not like the

extra production is going to dampen the cutouts much, given they

way they have been roaring higher. More cattle will become

available during June, but the market has to make it through May

first. I don’t see any reason why the cutouts should soften much

over the next few weeks, but can see several reasons why they

should be stronger.

We are right in the midst of the explosive spring beef markets that I

have been warning about for months. Further, I suspect that beef

prices might come down some in June as kills expand, but they are

not likely to plummet and so beef buyers might find themselves

paying stronger-than-normal prices for a long time to come.

Export demand may soon come under pressure as many importing

countries such as Mexico, won’t be able to afford as much US beef

at these price levels. We saw a modest decline in export

movement in this week’s data. The futures market prices cattle

and not beef, so it has not rocketed higher as this spring market

unfolded. With the way that beef and cattle prices often become

disconnected by fat packer margins, it becomes very difficult to

hedge beef prices using cattle futures. The CME should rectify this

problem by introducing beef cutout futures similar to the pork cutout

futures that were introduced late last year and have been very

successful. Next week watch for the cutouts to move even higher

and the middle meats to take over more leadership in those gains.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}