Beef Wrap April 14

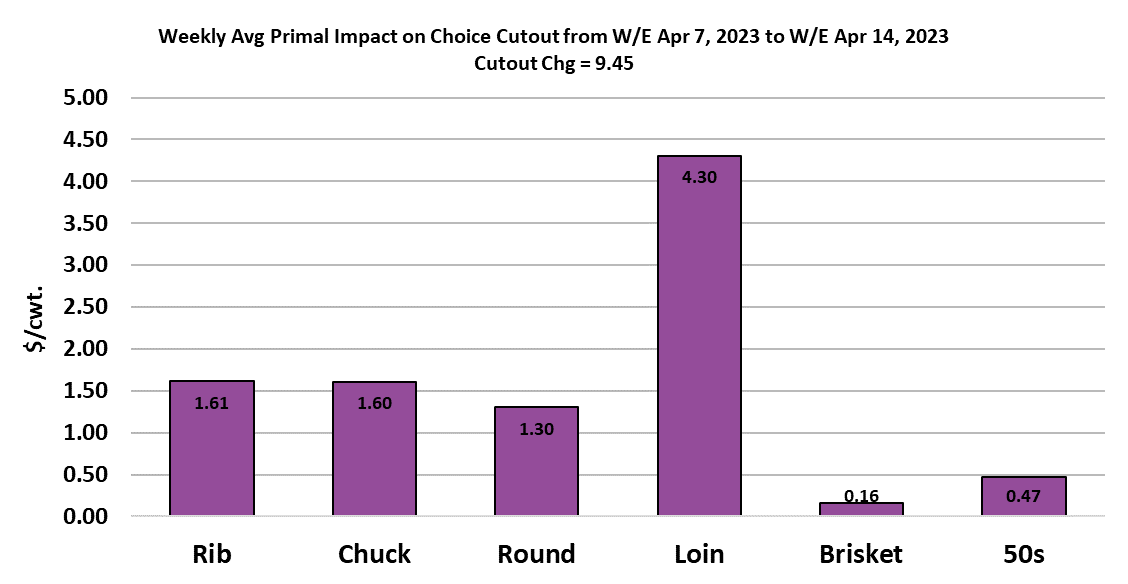

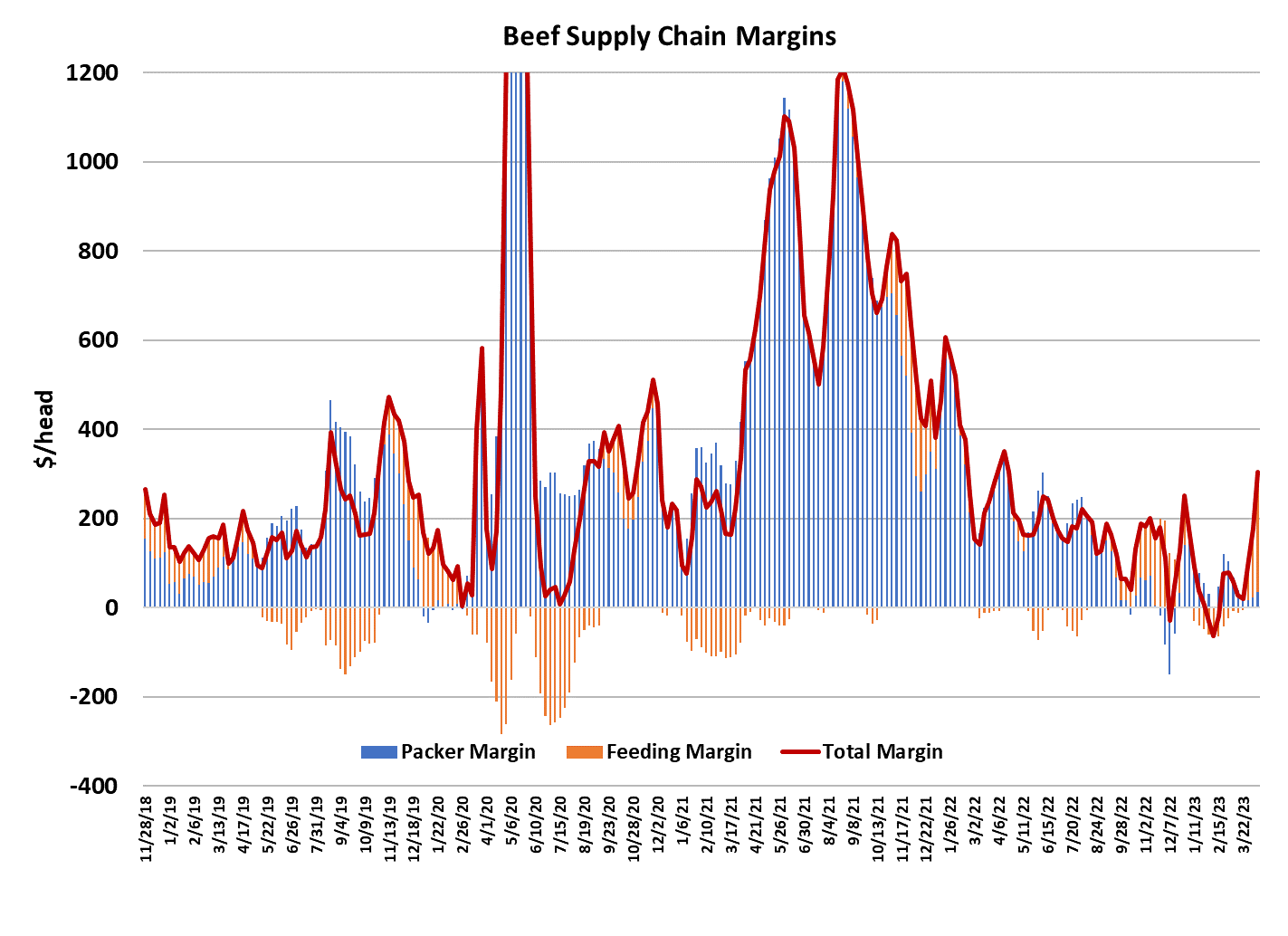

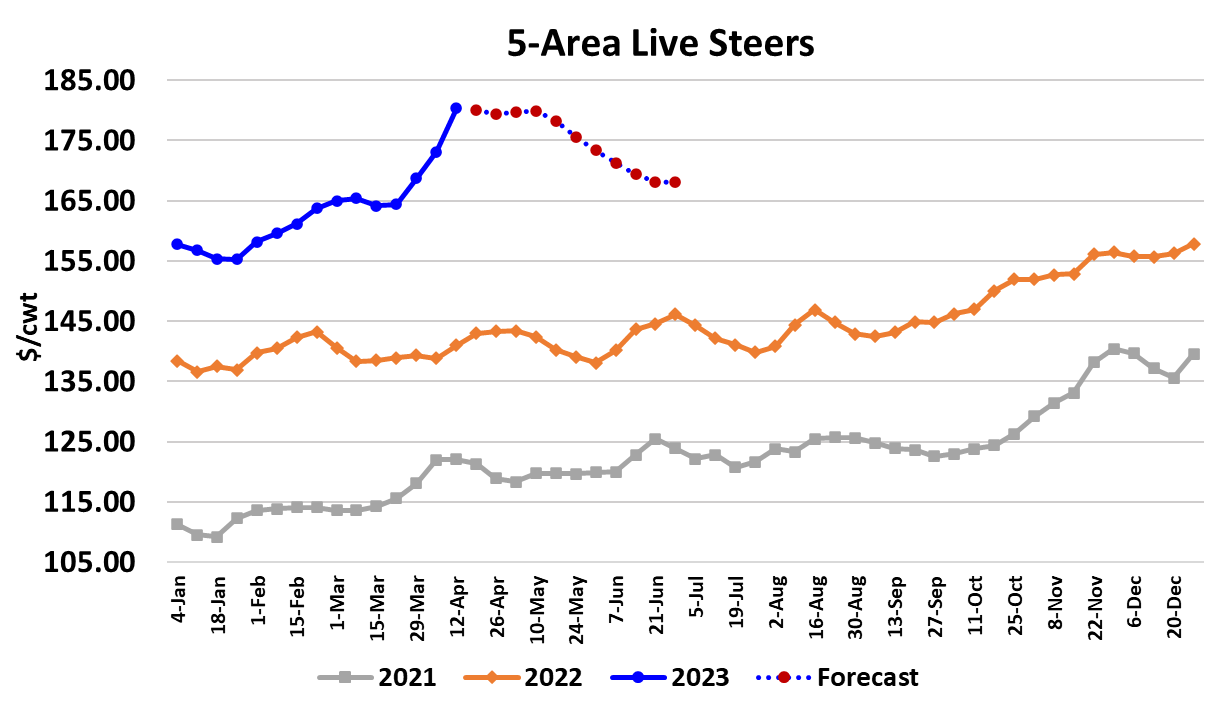

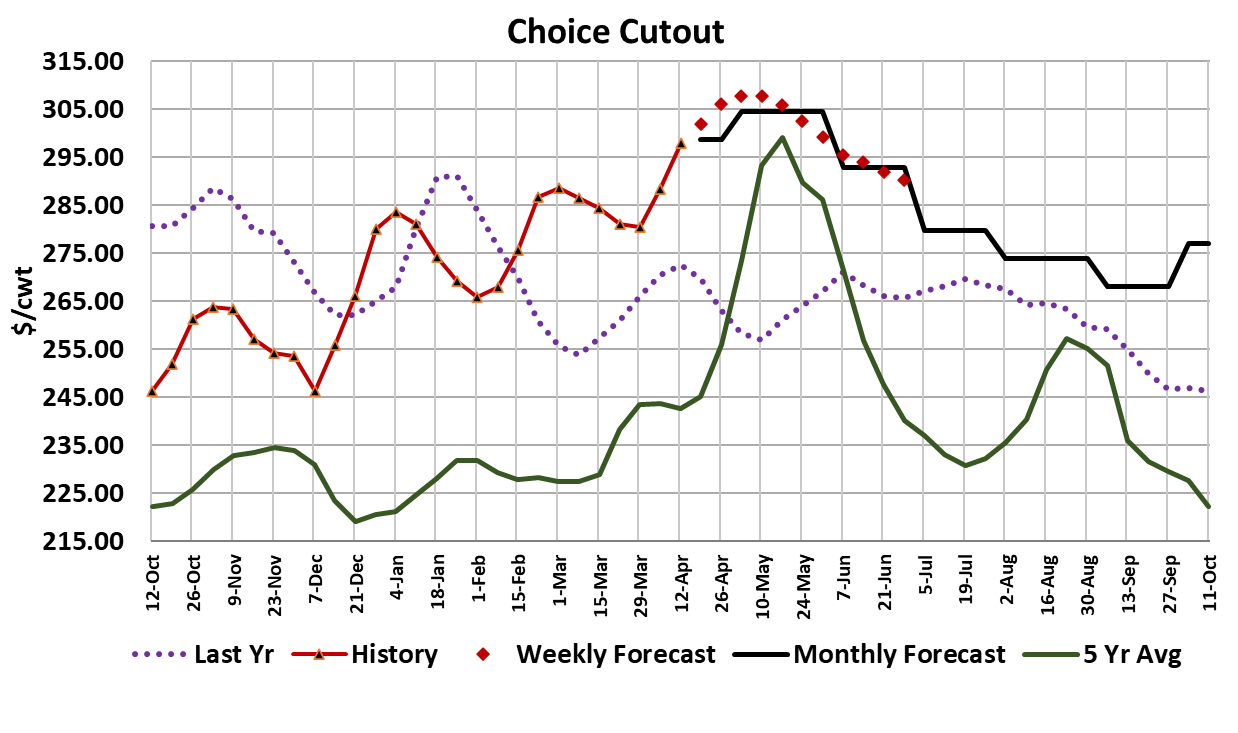

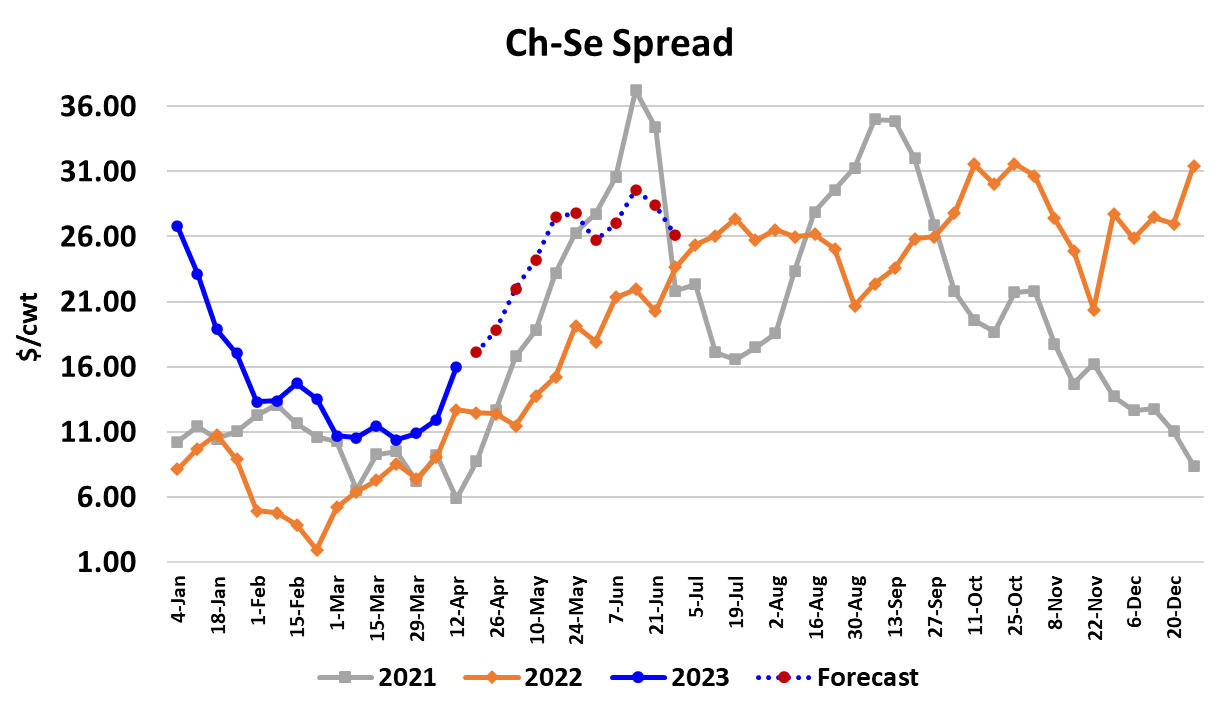

After rising $4/cwt. in each of the previous two weeks, the cash cattle market really outdid itself this week with a $7/cwt. increase to average just over $180 for the week. Trading started in earnest on Wednesday, which is a bullish signal in and of itself. Packers weren’t even able to pretend that they could wait until Friday to buy cattle. Instead, they rushed into the market on Wednesday and Thursday and made it rain money on cattle feeders. Cattle feeders seem to know that they have the packer on the ropes. How were they able to accomplish this? It seems like a combination of three things that have come together in perfect timing. First, we already knew from past placement patterns that fed cattle supplies this spring were going to be quite tight. Then, the northern feeding areas got some nasty winter weather at in February and March that reduced weight gains and caused cattle to need to remain on feed a lot longer than normal to reach the coveted Choice grade. Finally, the calendar flipped to April and grilling season demand started to kick in. In the past few years, consumer demand for high quality beef has expanded a lot. So when the cattle supply gets small, it is harder for packers to identify and source sufficient numbers of cattle that will grade Choice or better. Also, when the cattle supply gets small, packers have to compete fiercely in order to keep their plants running at an acceptable capacity utilization rate. Beef packing is very capital intensive and the cost curves in this industry are steep. If a packing plant were to run at only half capacity, its per-unit cost of producing beef would soar because of the high level of fixed costs (equipment, labor, etc.) involved. Packers really don’t want that to happen, so they compete aggressively for cattle and that drives cattle prices upward. To solve that problem, one or more large plants needs to close so that industry packing capacity is better aligned with the smaller cattle supply. However, no one wants to be the guy that closes a plant. They all want their competitor to close a plant. Thus, in the early stages of cattle supply tightening, there is this massive fight between packers trying to maintain their market share. I think that is playing a role in this crazy market right now. So, how long will this continue? Well, our flow model has been suggesting that available supplies of fed would only be about 480k during April and most of May. This week the fed kill was 476k. The flow model doesn’t account for cattle that were delayed by weather, so the actual number of market ready cattle is probably below 480k right now. It may be 4-5 weeks before available cattle supplies begin to expand. Now, that doesn’t mean that cash cattle prices are going rise $7 a week for the next 4-5 weeks, but it probably does mean that the potential for a significant setback in cattle prices is limited over the next few weeks. The other variable that plays a role is the packer’s ability to pay up for cattle based on his profit margin. I calculate that packer margins this week were about $35/head—not great, but still in the black—and that comes after 2 weeks where cattle prices gained $4 per week. So its clear that packers have been able to “afford” these more expensive cattle. How have they done that? By pushing beef prices upward rapidly and essentially making retailers pay a portion of the increased cattle cost. This week, the Choice cutout topped $300 and on a weekly average basis, the Choice cutout was up $9.45/cwt. and the Select was up $5.36/cwt. Of course, retailers are not happy about this situation, but what choice do they have? It is prime grilling season and they must have beef in stock for their customers to purchase. Further, retailers don’t like to shock their customers with sudden, sharp price increases, so they will work retail prices higher over a period of weeks or months. That means for the next few weeks, consumers will be seeing prices in the retail meat case that are “too low” relative to the wholesale price and so their consumption will continue to be strong. The fact that all of this is happening just as grilling season gets started really limits what the retailer can do. From a retail meat manager’s perspective, it really sucks to see your margin eroded by rapidly rising wholesale beef prices, but it sucks even more not to have product in the meat case when your customers come looking for something to throw on the grill. If this rally in wholesale prices was happening at a time of year when demand is seasonally soft like January or February, then I would say it is likely that wholesale prices would turn lower quickly, but the fact is that it is happening at the time of year when demand is ramping up. That makes me think it will have staying power for at least several weeks. The 50s market has been signaling for some time that the majority of cattle are not coming to slaughter with a lot of finish. Carcass weights haven’t really sent the same signal however, and that is a bit of a head-scratcher. The combined margin shot higher this week, as cattle feeding margins ballooned out to $268/head. The loins were the biggest contributor to this week’s cutout gains, but all primals were up to some degree. I expect that the ribs will soon take over leadership role in moving the cutouts upward. Next week, look for packers to be working the phones hard and asking more money for beef. The cattle market is likely to cool some from this week’s red-hot performance, but it wouldn’t surprise me to see some more small gains there. Often, when we see the price of something shoot higher, there is natural tendency to think that it will also come back down very quickly, but in this case I think the tight supply situation and the seasonal improvement in beef demand might cause this elevated price environment to persist for many weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}