Beef Wrap April 12

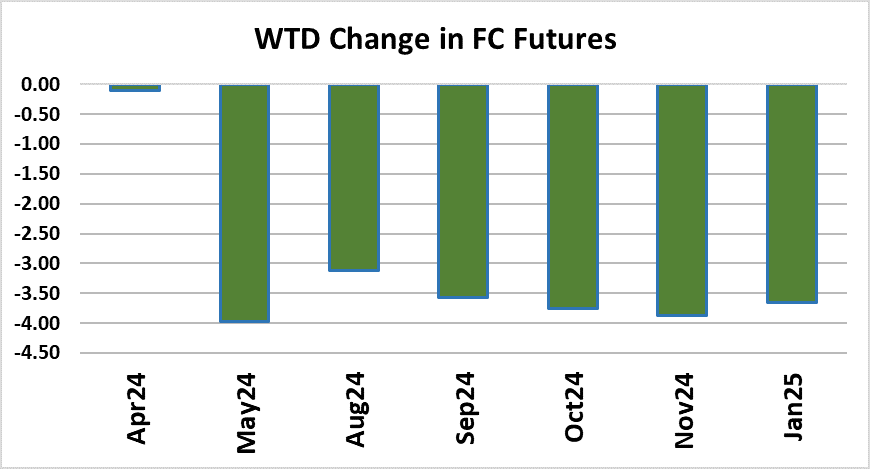

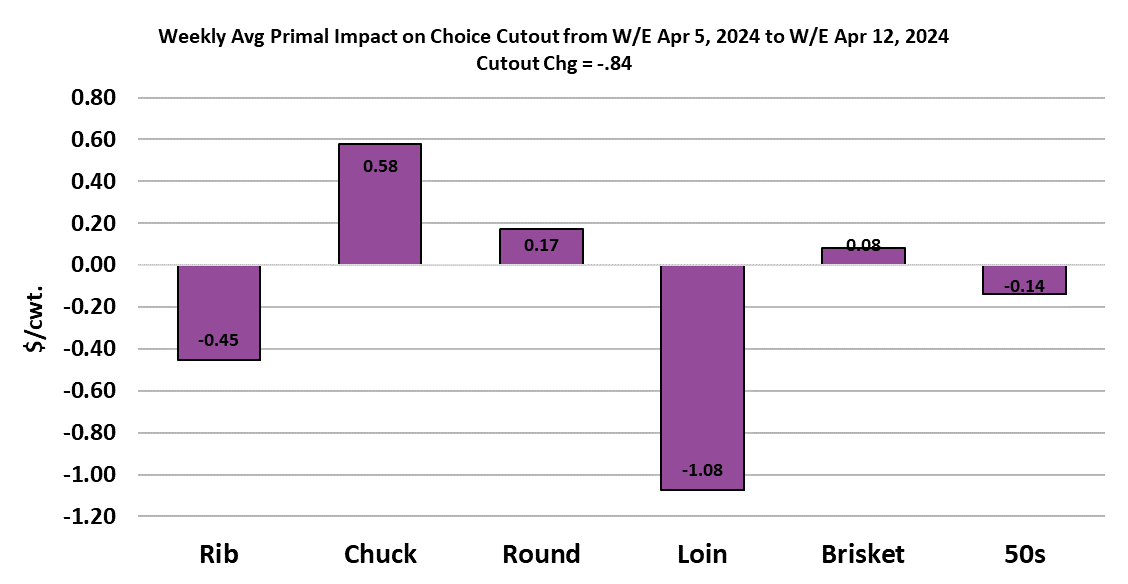

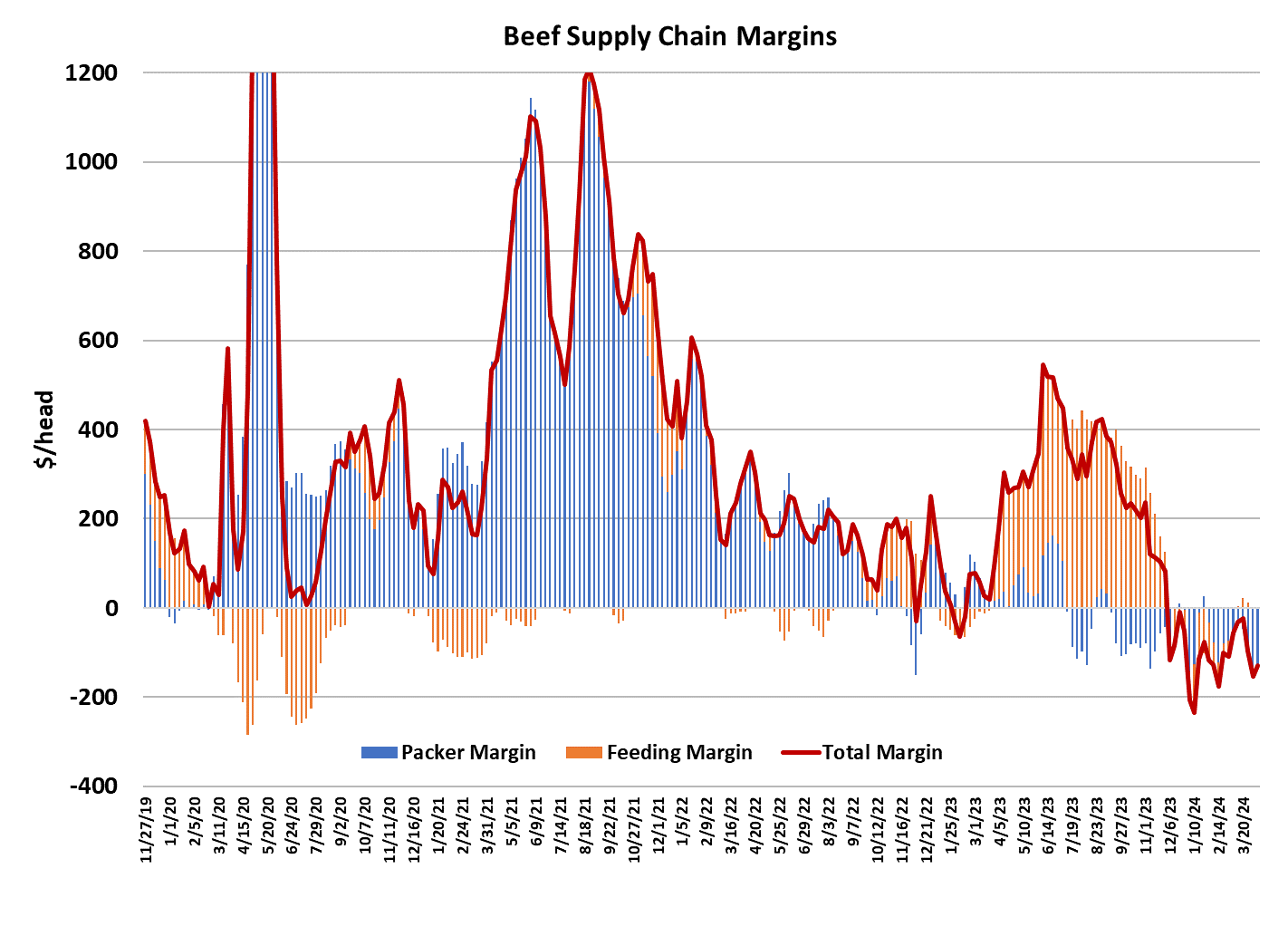

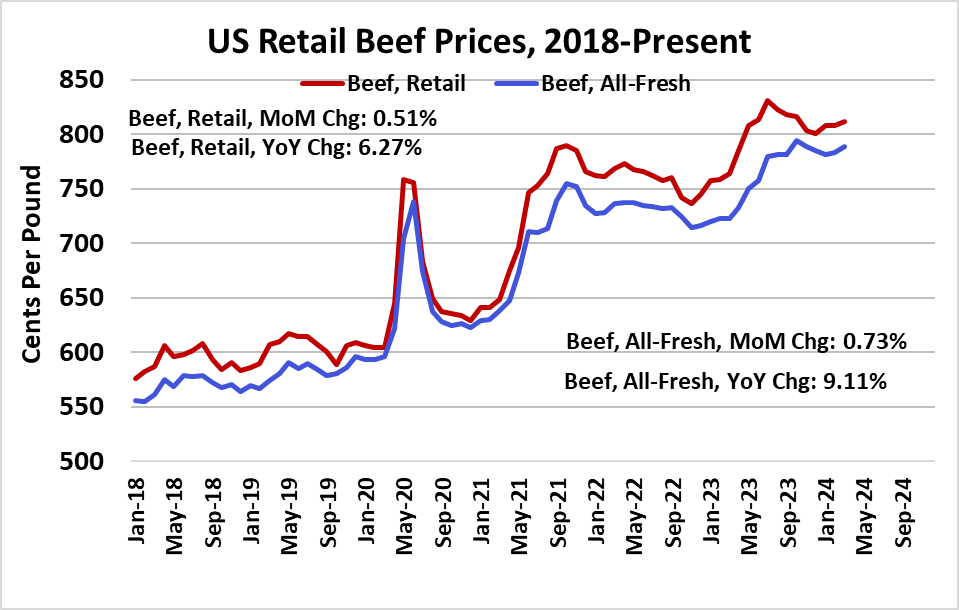

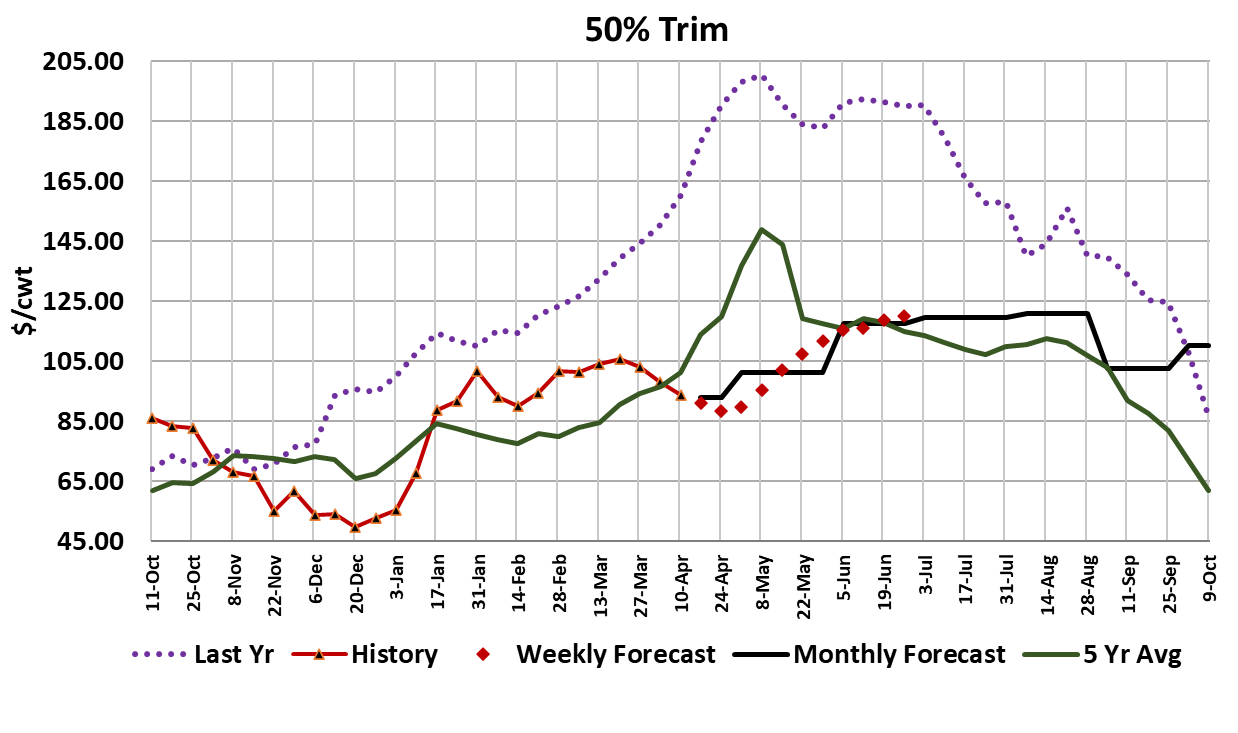

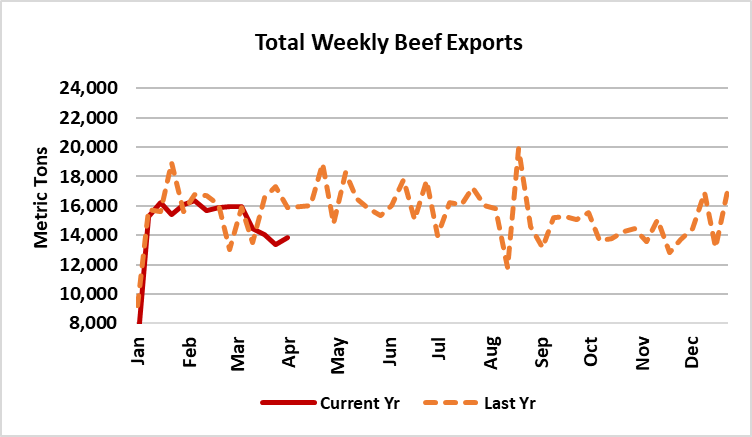

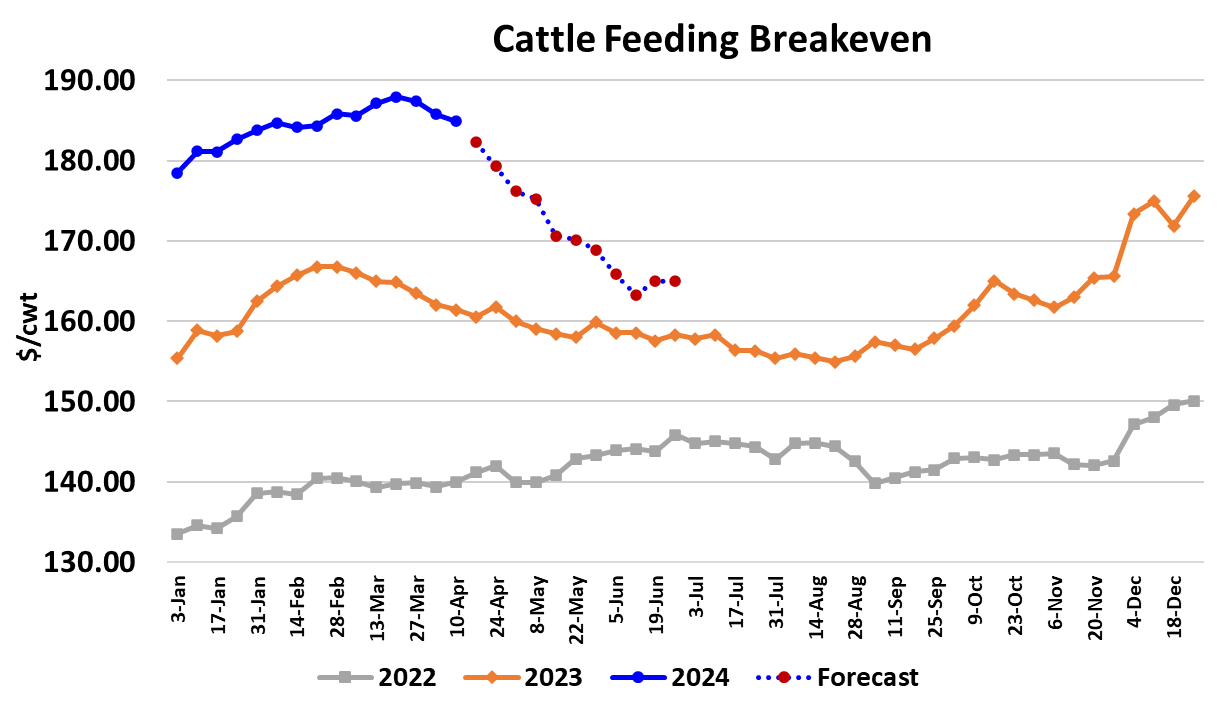

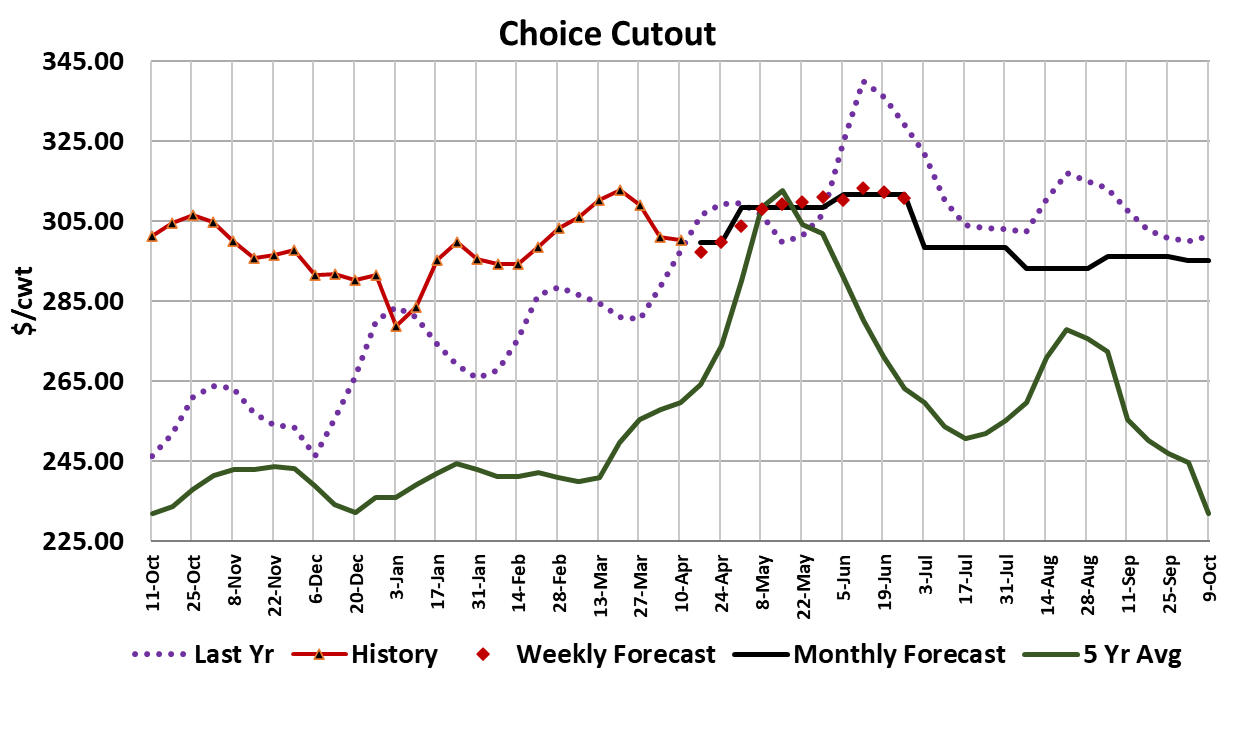

Cash cattle traded lower again this week, with the average live price expected to come in around $183.80/cwt., down a little over $2 from the week before. The cutouts were also lower, but not by much, as the Choice averaged $300.27 on the week, down $0.84 and the Select averaged $297.38, down $0.31. The Choice-Select spread, which has been uncharacteristically narrow recently, finished the week a few cents north of $5. Apr futures, which are now in delivery, finished the week up $0.65. There were losses in the back of the curve and it is unclear why traders are selling the deferred contracts so hard, when it would seem that if there is a problem with backlogged cattle, that would have much more negative impact on the front months. Perhaps there are concerns about the long-run health of beef demand. It is worth noting that the combined margin ticked a little higher this week, so perhaps we are near the end of the current downcycle in demand. Certainly, the seasonal would suggest that it is time for the cutouts to move higher from now until Memorial Day. One area that doesn’t look all that great is international demand for US beef. This week’s data showed shipments down about 13% YOY and ERS data for February was down 2.6% YOY. There is a very real chance that monthly exports for March and April will be down 10% or more. The middle meat primals continued to be a drag on the cutout this week, but the chucks and rounds were mildly supportive. 50s have been easing lower and were last quoted on Friday a little over $91. Carcass weights finally ended their counter-seasonal move higher and this week’s FI data showed steer weights down a pound from the week prior. More timely carcass weight information suggests that the downtrend will continue in next week’s FI data. Steer weights are now 25 pounds over last year, which sounds like a lot, but the spring of 2023 saw some unusually light carcass weights. I’d look for the YOY gap in weights to narrow as we move into summer. With the herd shrinking cyclically and corn much cheaper than in recent years, it makes sense to expect carcass weights to post YOY increases and we could see that persist for the balance of the year. This week’s fed kill registered 482k, down 7k from the week before. The flow model suggests that about 160k went un-harvested in March, but a portion of that is likely to be made up in April. Packers’ margin situation doesn’t provide a lot of incentive to run the kill hard at present. I calculate this week’s packer margin at close to $125/head in the red. That’s about $25 better than last week, but still nothing that will get packers excited. With the recent declines in the spot cattle market, cattle feeding margins are teetering on the brink of going negative also. However, breakevens are declining for fed cattle—the result of cheaper feeder cattle prices last fall when the market went into a swoon and falling corn prices. The forecast has fed cattle breakevens moving down into the mid-to-low $160s during June, down from about $185 today. Since cash cattle prices are not expected to get that low, cattle feeders stand a good chance of starting the summer with positive margins. The fundamental forecast has cash cattle trading down into the mid $170s near the end of June (5-area average). That makes the Jun futures, which finished today at $171.47, look a few dollars too cheap. It is unclear what it will take to make futures traders relent with the selling that has dominated the market over the past few weeks. It would certainly help if the “avian influenza in cattle” story would die down, because that seems to be keeping the large specs on the sidelines and they are big fans of the long side. Perhaps some more solid gains in the cutout would help to bring back buying interest. I suspect that better cutouts are just around the corner. One thing that would almost certainly end the slide in futures is if the cash cattle market could hold steady rather than post a decline one week. At that point, we would likely see producers wanting to trim down short hedges and it could even tempt some renewed speculative buying. Going forward, the forecast has the Choice cutout working back up into the $310-315 range by early-to-mid June and the cash cattle market working lower during that same time frame, so packer margins should improve and are likely to be positive by the middle of June. That, along with stronger demand, should encourage larger harvest levels and help to clean up some of the sloppiness in front end supplies. Retail prices for March were released this week and they were up from February and the “all-fresh” price is now 9.1% higher than last year. It would certainly help if retailers would lower price levels, but there is little incentive for them to do that at present. Pork and chicken are much better values in the retail meat case and that could pose a problem for beef demand at some point. Next week, watch for further gains in the cutouts and perhaps some stabilization in futures prices. Cash cattle are likely to take another step lower, but a lot can be learned from how much cattle feeders resist before accepting that outcome.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}