Beef Wrap April 5

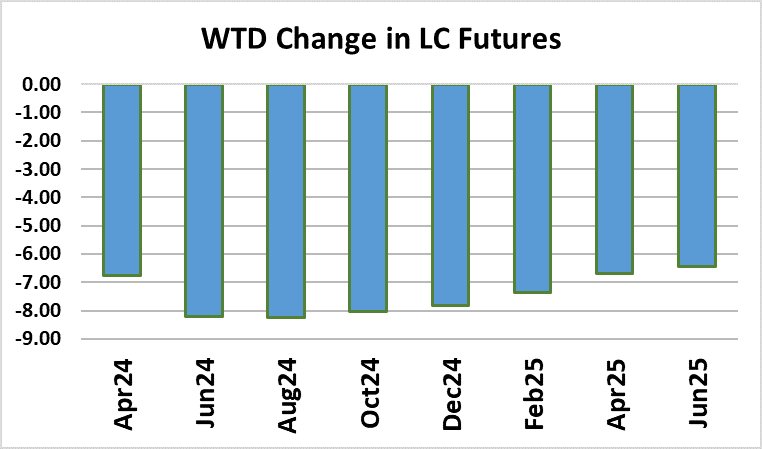

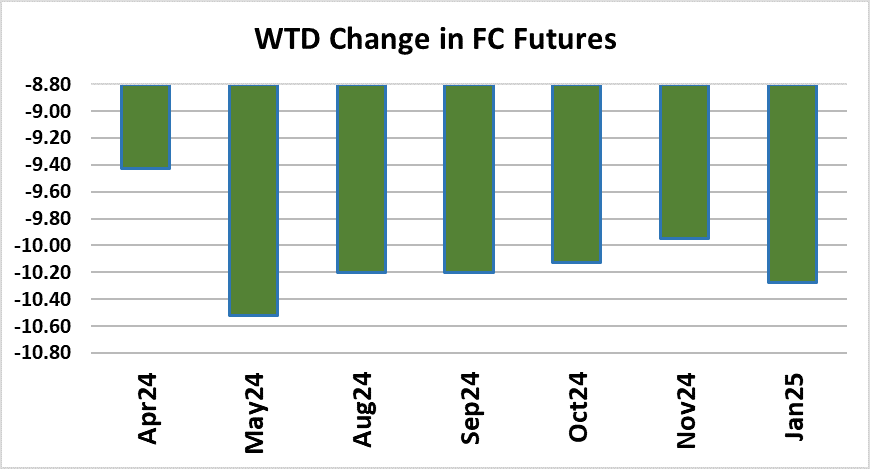

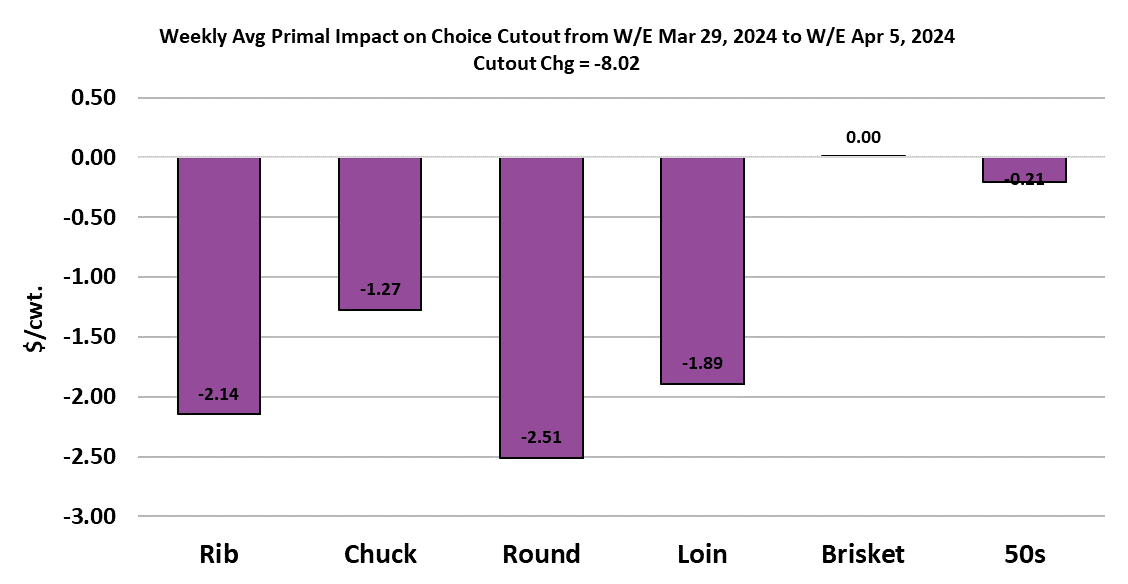

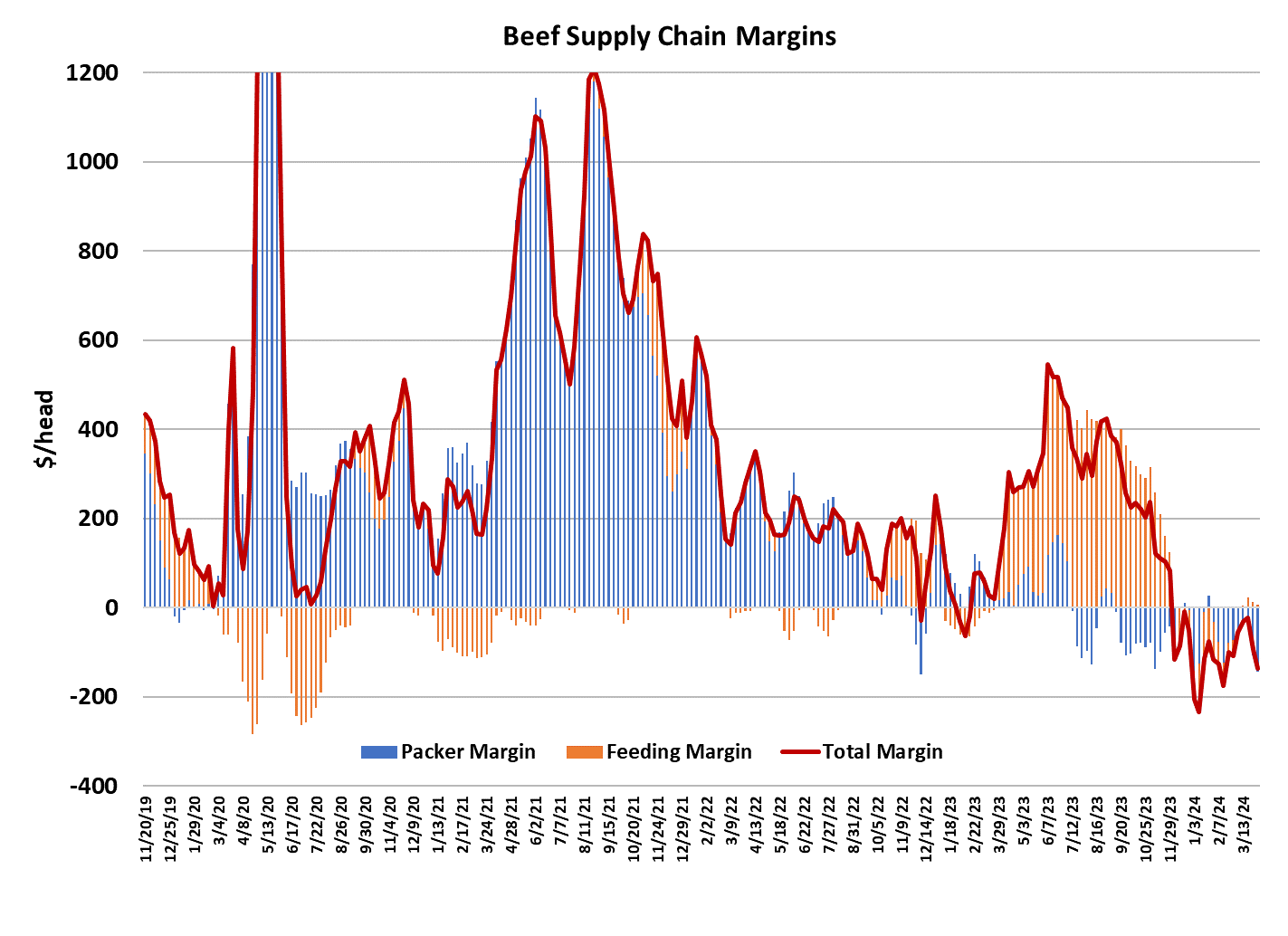

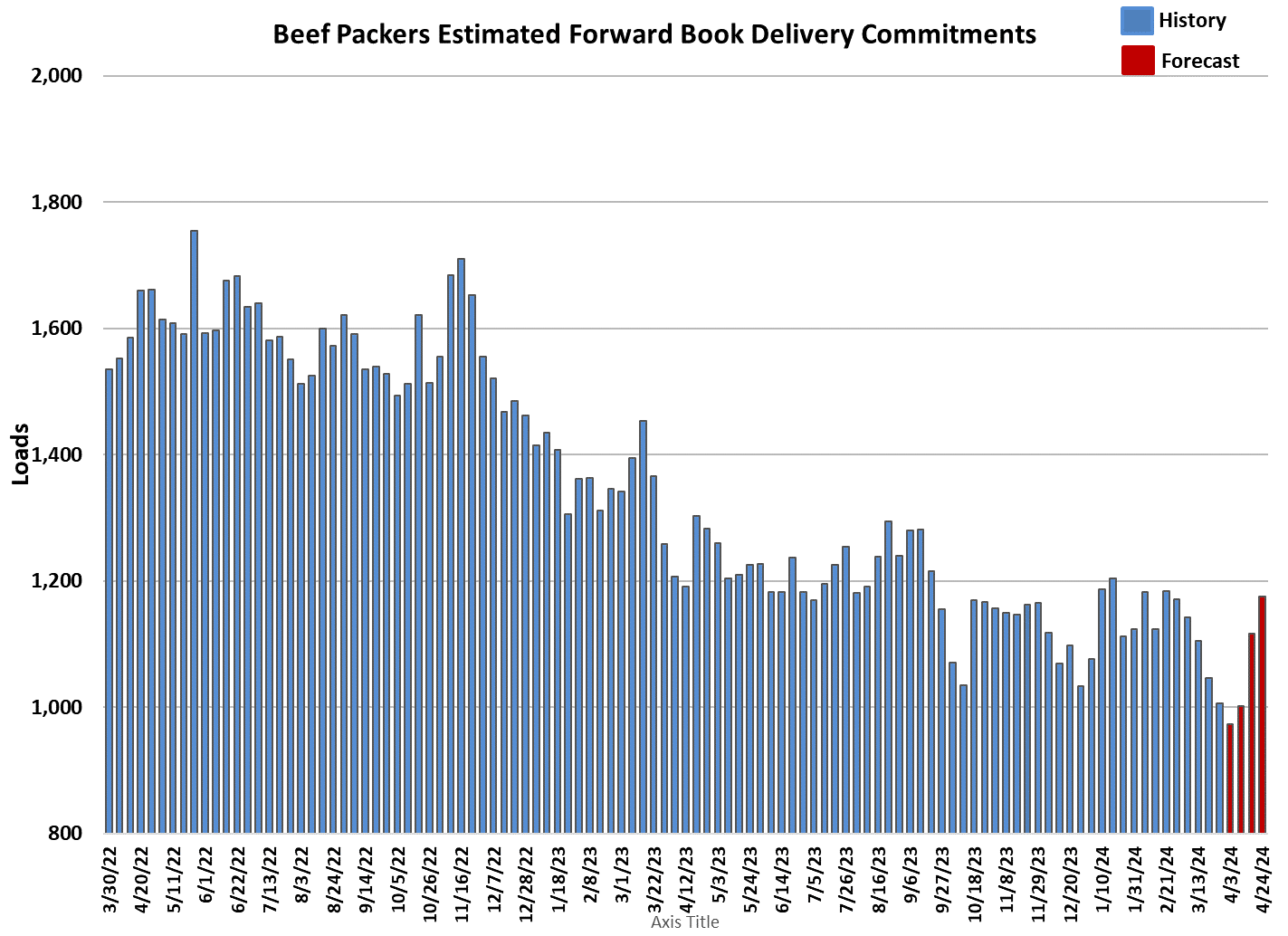

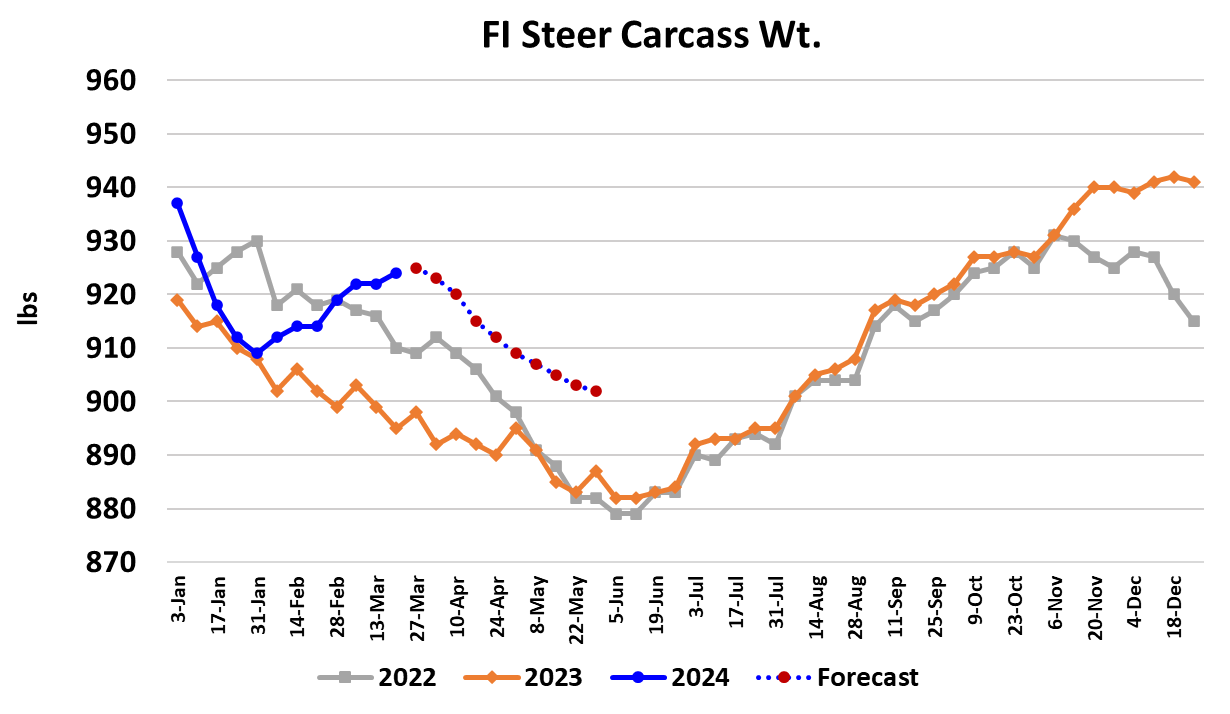

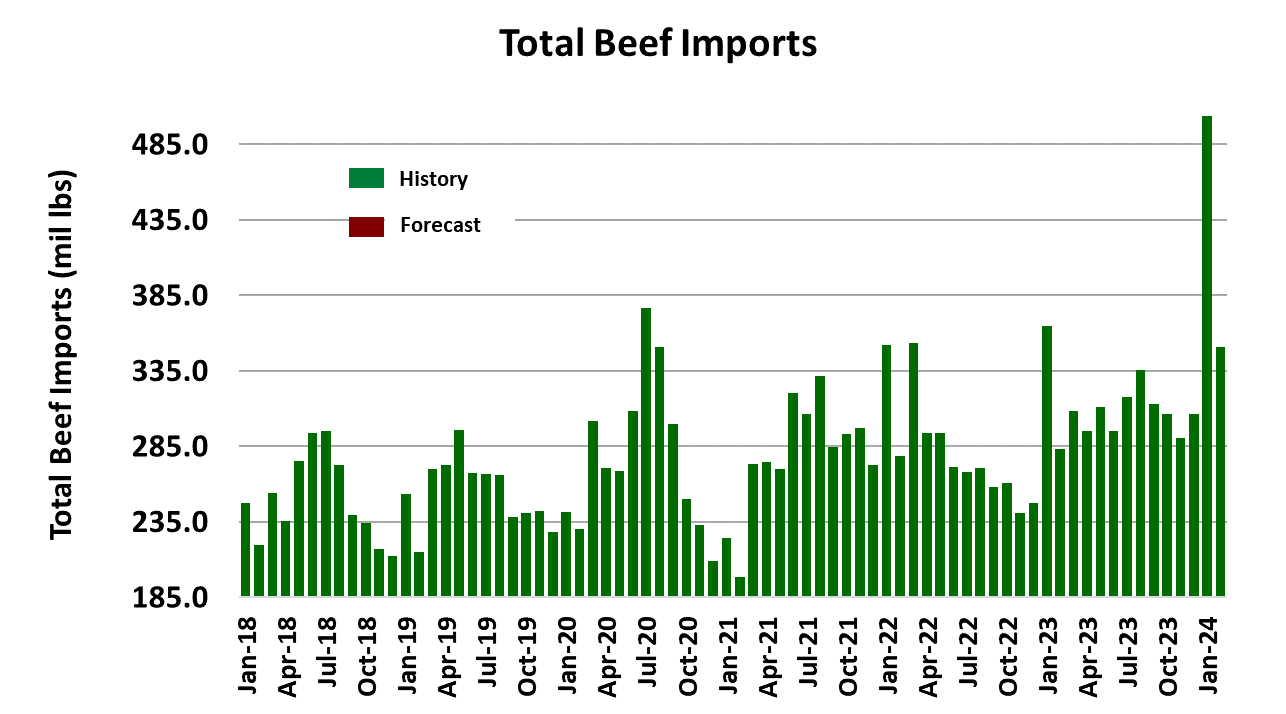

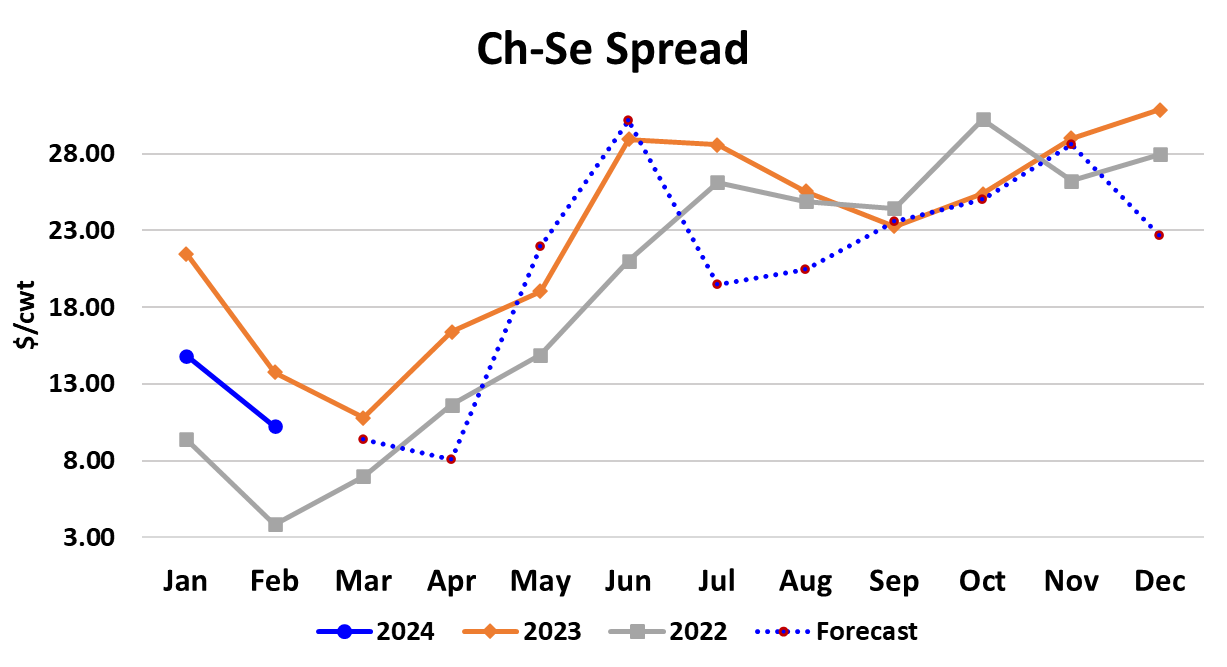

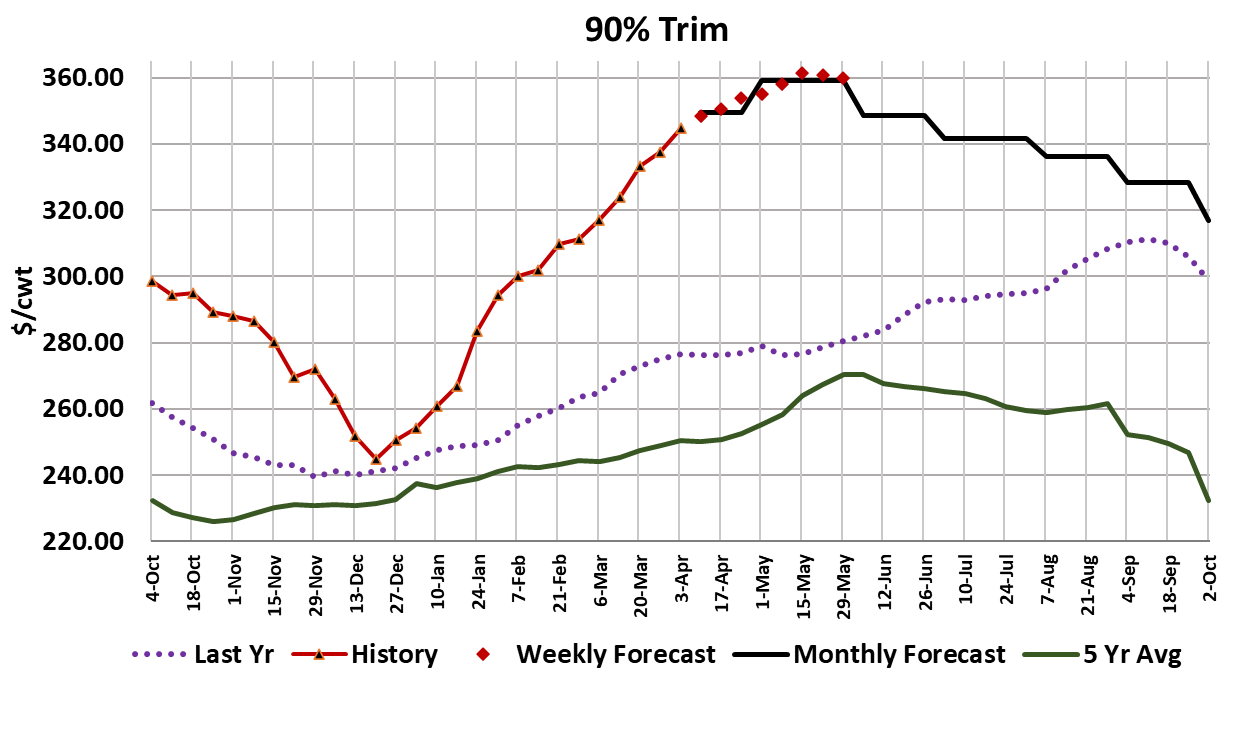

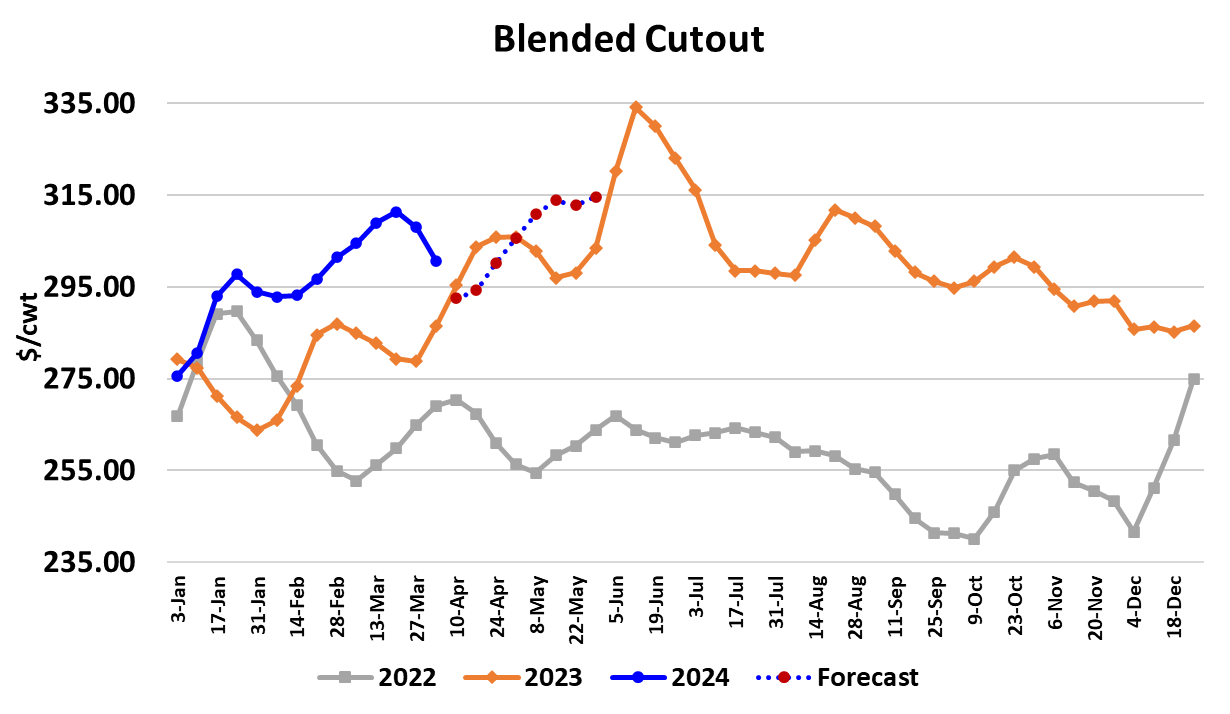

The beef market hit a bit of an air pocket this week, with the Choice cutout dropping $8.02/cwt. to average $301.10 and the Select cutout losing $3.36/cwt. to average $297.69. Apparently, it is just too early for spring demand improvements to take hold. The northern section of the country experienced colder-than-normal temperatures and even temps in the south were down from the prior week. There is another factor at play here as well. Beef buyers have watched the cattle futures drop about $12 in just three weeks and that has probably fostered a desire to step back from the beef market where possible, with the aim of filling needs later at a lower price. No one want to catch a falling knife. But that approach could leave buyers short bought and thus lead to a bigger rally once they begin to perceive that a bottom is in place. The cattle market followed the beef lower, but the drop there wasn’t nearly as large as in the cutouts so packer margins moved deeper into the red. Once all of the data is complied on Monday, I expect the 5-area average price for fed cattle to be very near $186/cwt, down about $2.25 from the week before. Trade in the North is likely to average around $187, while trade in the South was closer to $184. Numbers are tighter in the North right now and the price premium is expected to persist for a least a couple more months. The weakness in the cutouts was spread rather uniformly across the four major primals, which I take as further evidence of a general backing away rather than a demand problem with a particular primal. Interestingly, the beef 90s kept charging higher this week, up almost $7/cwt., to average $344.80. Shoulder clods are trading close to $325, so there should be some incentive to buy those up and grind them as a replacement for expensive 90s. I’ve been forced to lower the near-term forecasts in order to reflect the current market conditions, but I don’t think that beef demand is going to just trend lower from here. The attached chart of packers’ estimated forward delivery commitments indicates that this week those commitments were the lowest they have been in the past two years. However, there is a surge coming in mid-to-late April and that suggests that retailers have plans in place to feature beef much more aggressively than what we’ve seen recently. It will also move some product out of the spot market to fill those orders, so buyers who are comfortable being short bought today might feel the pinch in a couple of weeks. This week, there was news of more dairies where cattle tested positive for avian influenza and also news that one human who worked in a diary contracting it. None of these illnesses are very serious, but it does have the futures market on edge. Large speculators can put their money into any number of markets, so why would they choose to be involved in a market like cattle where a disease story is active? If a case turns up in feedyard cattle, the selloff could be swift. Since speculators have historically taken the long side of the market, this has left the cattle futures without many willing buyers. In fact, open interest in live cattle futures has recently fallen below lean hog open interest. That doesn’t happen very often, but it highlights the exodus of money from cattle futures. I don’t think that we would have seen the futures drop this far without the bird flu story and the same goes for cash cattle and the cutouts. Fortunately, the incidence of avian influenza tends to decline sharply as the weather warms, so hopefully, the “bird flu in cattle” story will also fade quietly away in the next few weeks. This week’s fed kill came in at 486k, up 20k from the week before and there were even 20k scheduled for Saturday. My guess is that next week’s kill will be even higher as packers start to prepare to deliver on upcoming forward commitments. They will need cattle in order to do that, so if cattle feeders hold firm, perhaps they can stem the slide in cash cattle prices. Of course, cattle availability should increase as we move into the May/June period and that often keeps a lid on the cattle market even though the beef cutouts are usually rising at that time. I estimate packer margins this week at -$153/head, which is about $45/head worse than the week before. I expect that packers will get back to moderately positive margins in May. FI steer carcass weights increased two pounds this week, continuing the counter-seasonal trend that has dominated in recent weeks. However, some of the more-timely weight data is suggesting that weights are now turning back lower into their normal seasonal pattern. We may see one more week of increasing FI weights before they start to reflect the new downtrend. USDA reported the trade data for February today and it showed beef exports down 2.6% YOY and beef imports up 23.8%. The US imported 107 million pounds more than it exported in February. We have been a net importer now for well over a year and that is projected to continue at least through 2025 and maybe beyond. The more-timely weekly export data has looked soft recently and that raises concerns about export interest, particularly in the next couple of months when US prices are expected to increase. Feeder cattle imports from Canada and Mexico were up 15% and 10% YOY, respectively, during February as cattle feeders looked to offset tight numbers in the US by placing more cattle from outside our borders. Next week, watch for some buying interest to surface in the beef market, but the gains will probably be small. Keep an eye on those news feeds for bird flu stories because that seems to be the biggest risk to the market right now.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}