Beef Wrap June 7

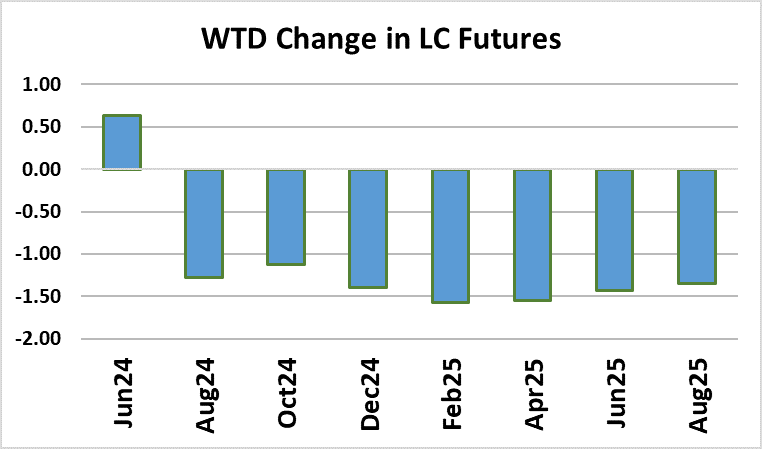

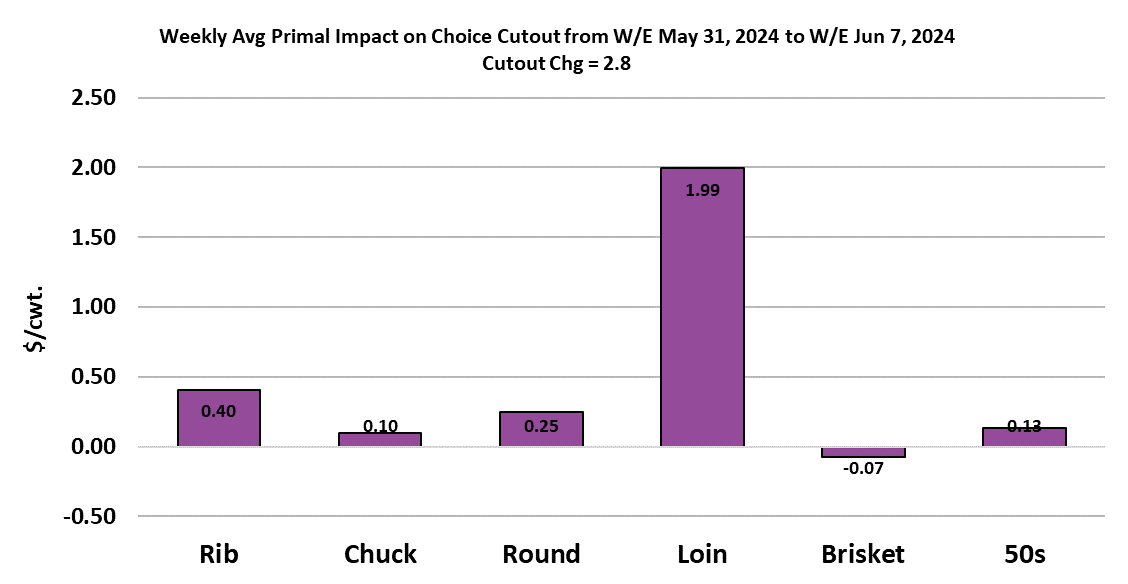

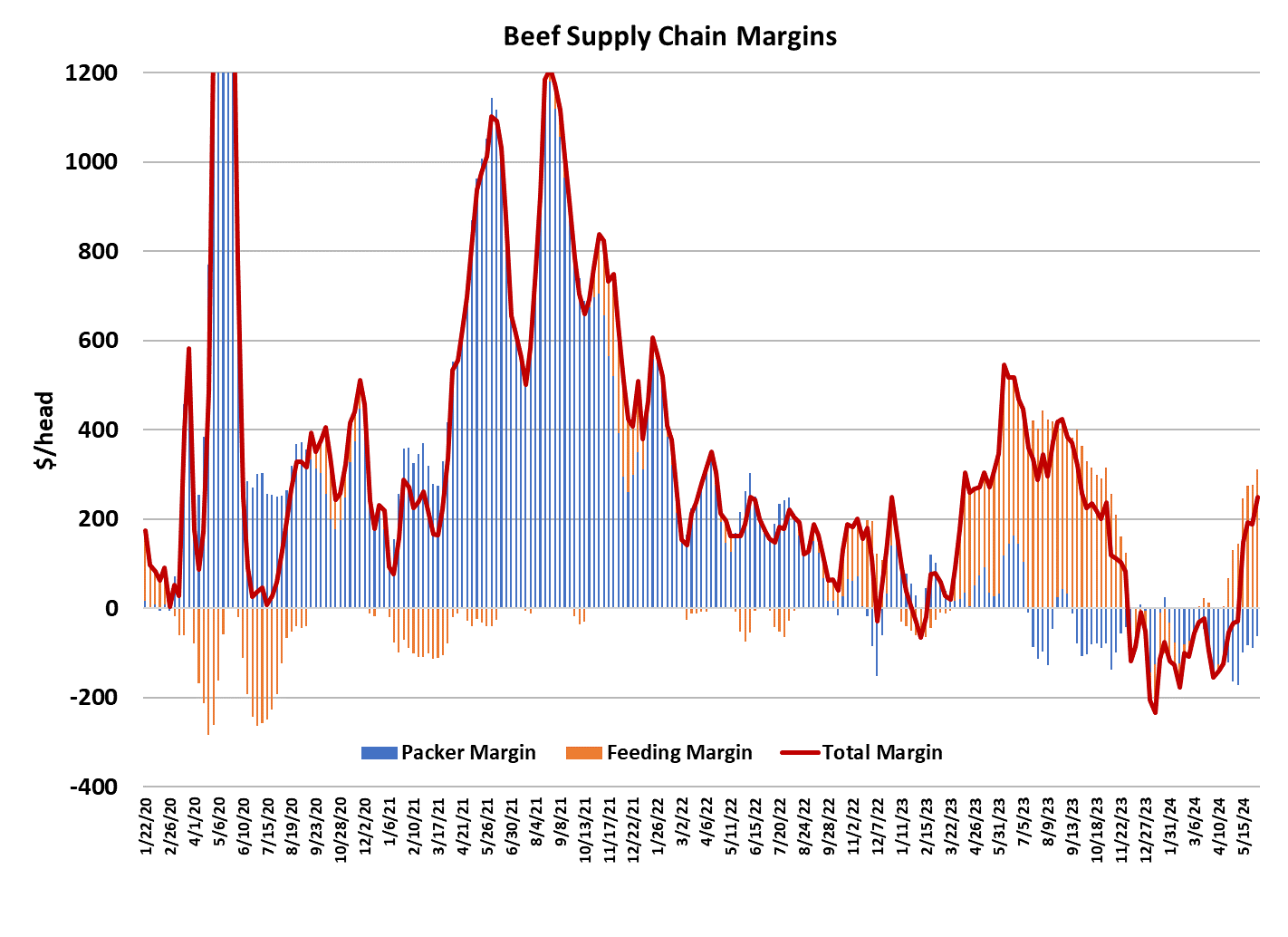

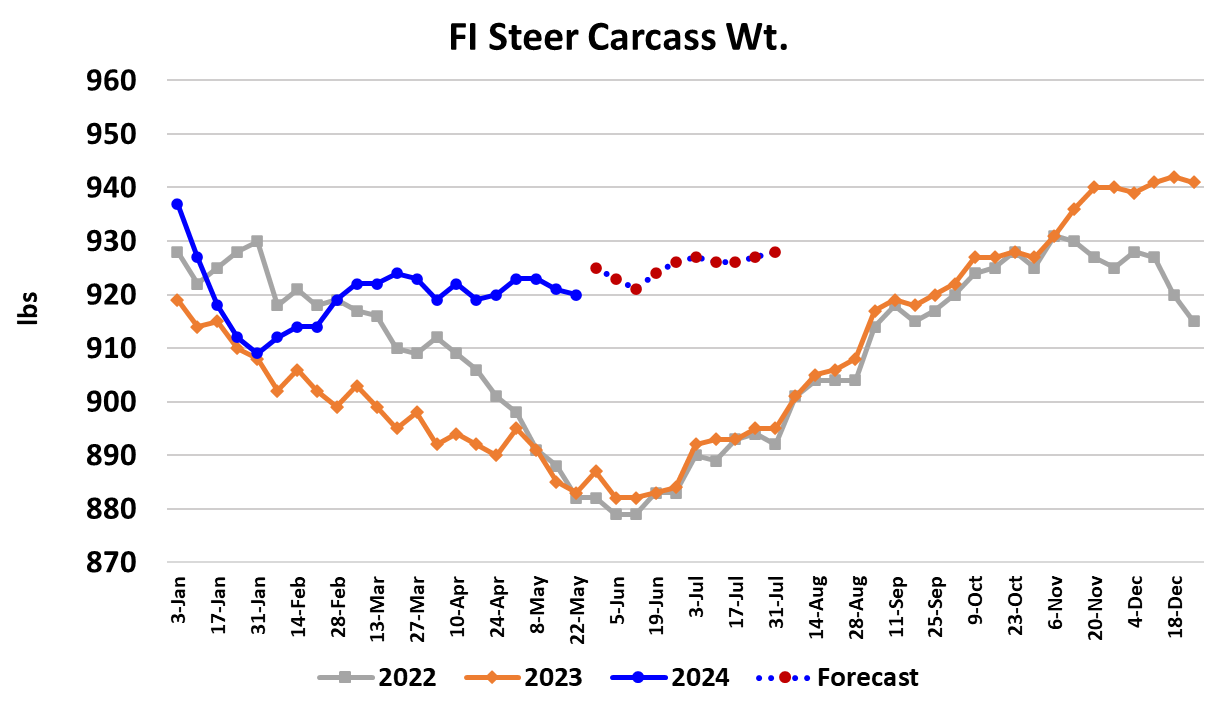

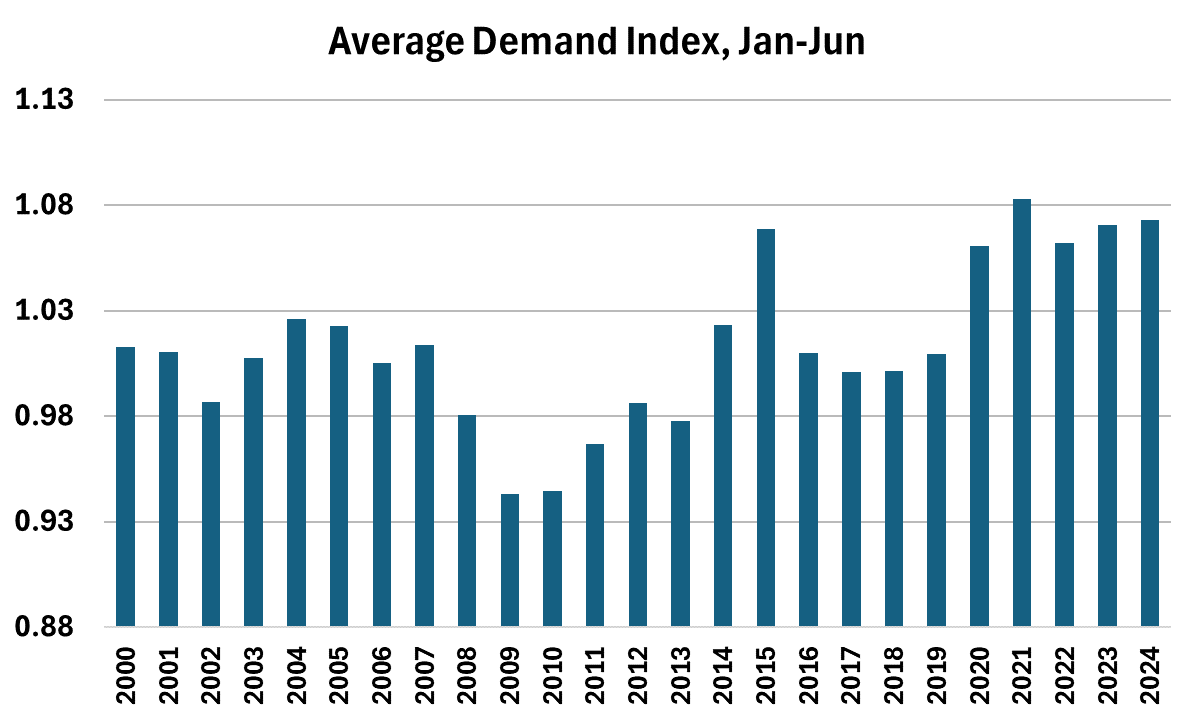

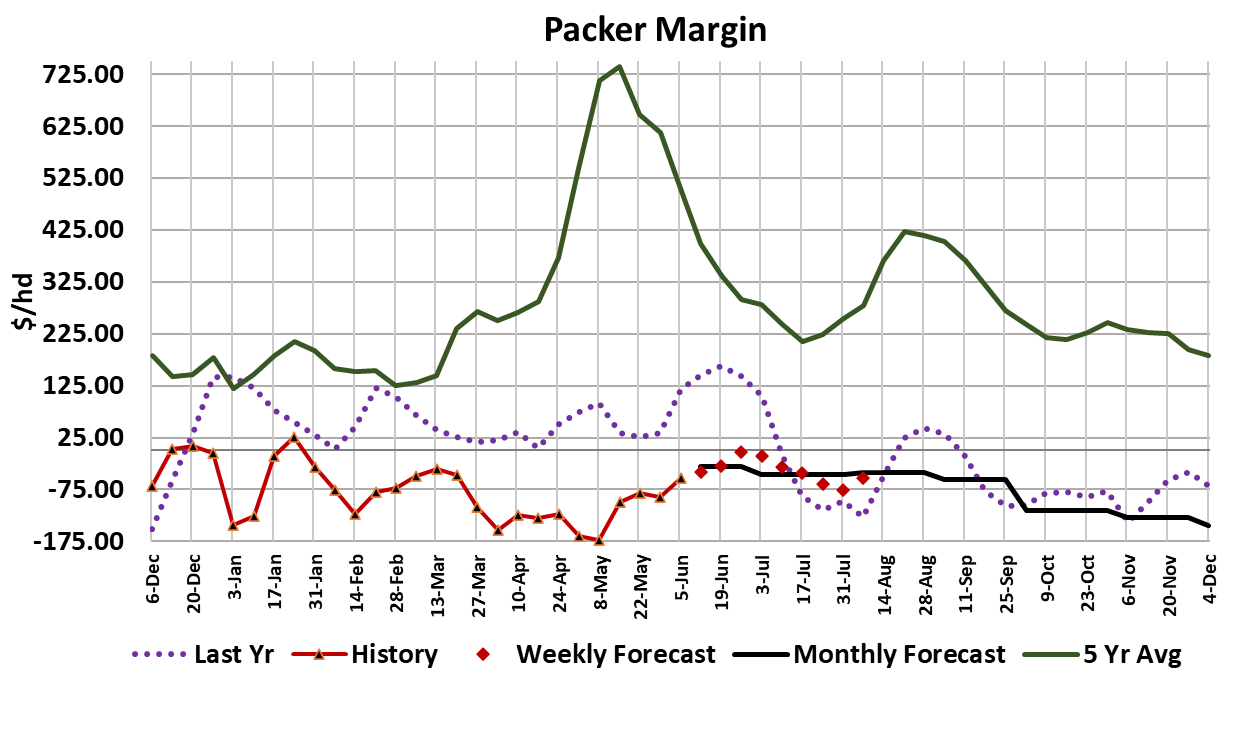

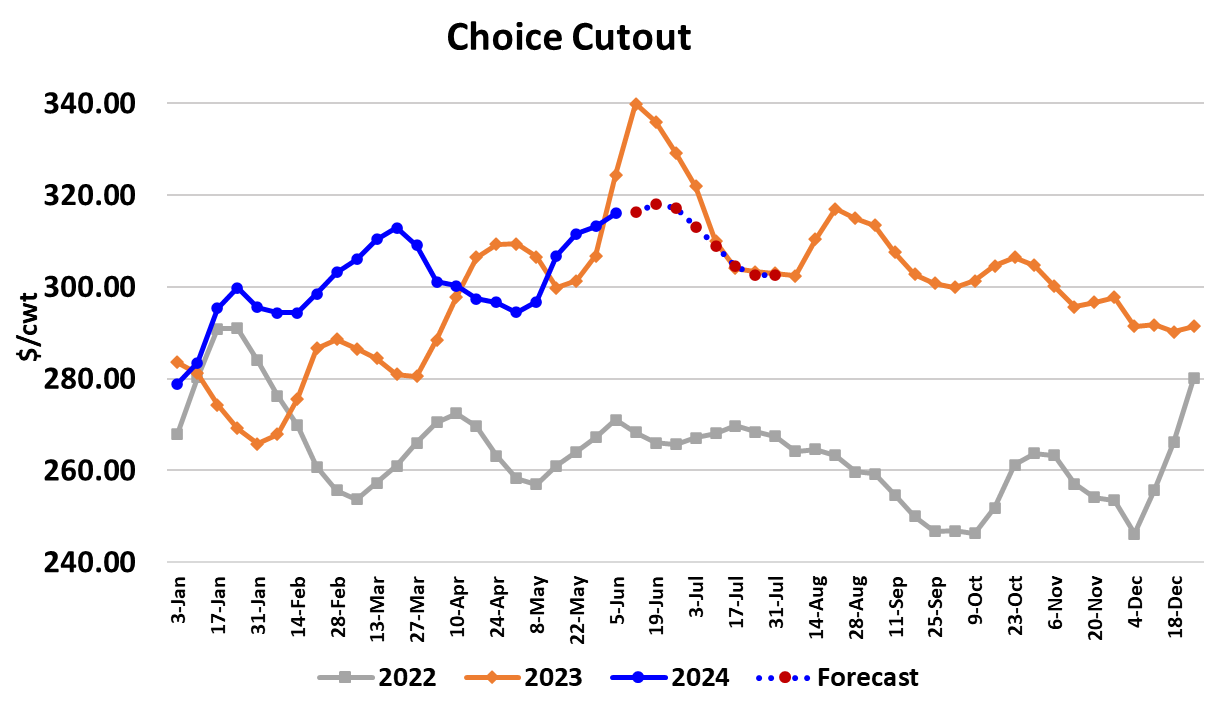

The beef markets were able to add to last week’s gains, with the Choice cutout up $2.80 to average $316.05 and the Select cutout down $0.33 to average $302.21. Sure, this week’s gains were small, but they helped mitigate the fears that beef demand would come tumbling down after the Memorial Day holiday. Instead, now the blended cutout is at it’s highest level so far this year. Packer margins improved to about -$50/head from -$88/head last week. For the time being demand concerns have moved to the back burner. This week’s increase was driven by the middle meats, particularly cuts from the loin primal and on Friday afternoon the Choice-Select spread was reported at a respectable $15.61/cwt. It is likely that a good bit of this week’s demand improvement was driven by last minute purchasing ahead of Father’s Day, which occurs a week from Sunday. It was also encouraging to see the chuck and round primals post small increases this week. Both the 50s and 90s were reported about $5 higher on the week. Of course, cattle feeders who were watching the beef market hold firm felt like the cattle market ought to be at least steady this week, if not higher. As of press time, there was only some light trade at $185 in the South, down $1, and almost no northern trade reported. My guess is that cattle will eventually change hands at something close to last week’s average even if it means $1 lower in the South and perhaps steady in the North. Once again, the cash cattle market is proving more resilient than many thought given how heavy weights are and how many cattle should become market ready at this time of year. Just the fact that cattle feeders were willing to wait until late on Friday (and maybe even early next week) before trading cattle tells me that they aren’t feeling any sense of urgency to move cattle. Until that sense of urgency appears, it is unlikely that we will see big declines in cattle prices. Futures traders are still pretty negative on the outlook, but they no longer feel safe selling the nearby Jun, which goes into delivery on Monday and is currently trading about $4 below the last established cash trade in the South, so they sold the back months instead. It seems to me that the best chance for a big break in the market might come near the end of June when all of the Independence Day purchasing is done and the focus will then turn to the hot, “dog days” of summer. The fed kill this week came in at 499k, just a tad below the 505k that I estimate would keep feedyards from losing currentness. I would look for fed kills to hold in the 495-505k range through June before dropping back below 500k during July. The non-fed kill was particularly light this week at 115k and there is risk that it may get even smaller over the next couple of months. That should keep fairly good support under the 90s market. FI steer weights were reported down one pound at 920 pounds this week, but it looks like we could see 4-5 pound increase next week. I guess we should stop worrying about carcass weights not coming down seasonally since we are now well past the point in the calendar when weights make a bottom. From this point forward weights should be rising, but my guess is that rise will be very slow and it will look like carcass weights are mostly sideways through the summer. If I’m right on that pattern, then as we approach the end of summer, the YOY gap in weights will have narrowed considerably and then weights may start to track seasonally higher until November. This week’s fed beef production was up 8.1% YOY, but we are comparing to an unusually small number last year. Over the next few weeks, it looks like a 4% YOY increase is likely. On the pricing side, last year at this time we saw a huge surge in beef prices, with the Choice cutout going from around $305 to $340 in just a couple of weeks. Of course, it retraced that move pretty quickly, but it gives you an idea of what June demand is capable of. This year, I think the increase will be much more muted and would be surprised if the Choice cutout can clear $320 in the next few weeks. Non-fed beef production (from cows and bulls) was down 10.7% YOY this week, continuing a long string of big YOY declines. We received the April trade data today from ERS and it showed total beef exports down only 3% YOY. I think there is a good chance that when the data for May are released, we will see a small YOY increase in exports. That probably won’t last more than a month or two and then we will be back to ongoing YOY declines. It does look to me like beef exports are holding up better than expected given domestic price levels this spring. The Mexican peso has recently weakened relative to the US dollar and that has the potential to curtail interest from that important destination if it persists. Mexico primarily purchases lean cuts like Select end meats from the US. Despite all of the worries about domestic beef demand, it looks like the average demand index through the first six months of 2024 will be very close to the near-record average posted last year. For the second half of 2024, the forecast has the demand index holding nearly steady with the first half of the year, but about 2 percentage points below the second half of 2023. I think the risk is to the downside on second half demand, but I haven’t yet seen enough evidence of demand softening to justify moving the forecast lower. That may come in the next couple of months. Next week, look for the cutouts to trade steady to slightly higher and cash cattle to trade steady to $1 lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}