Beef Wrap June 14

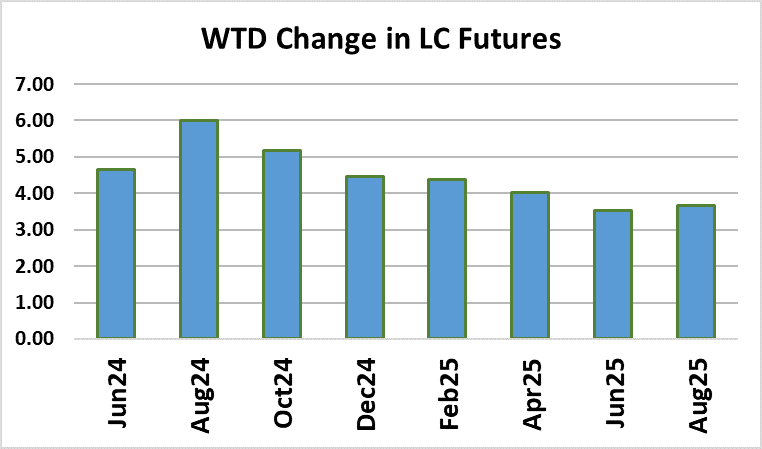

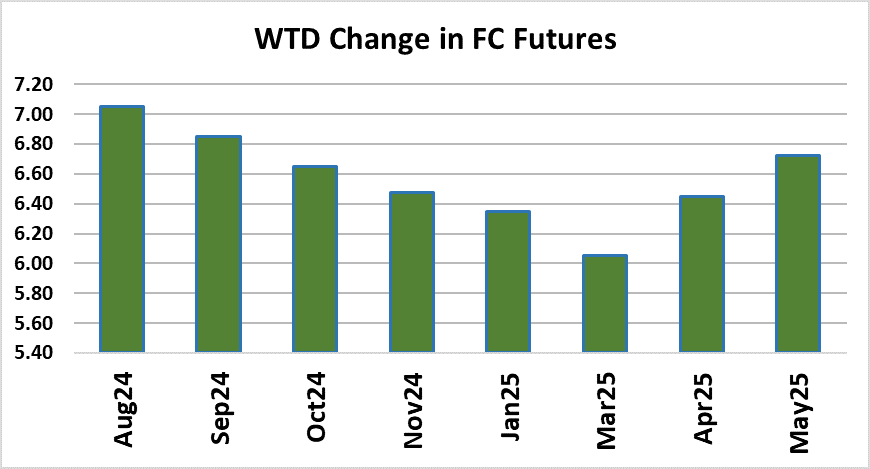

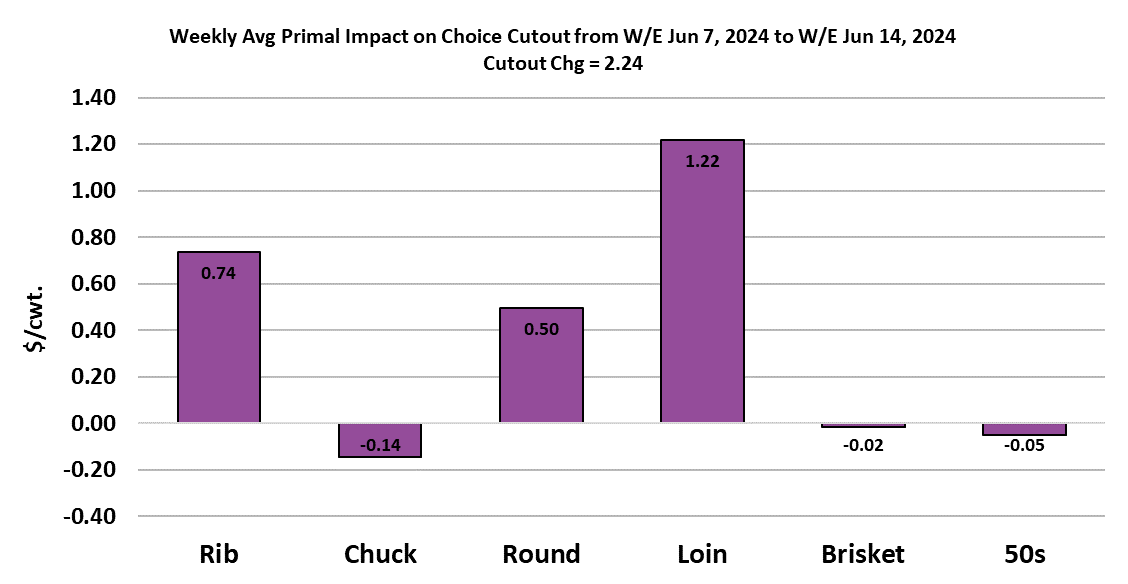

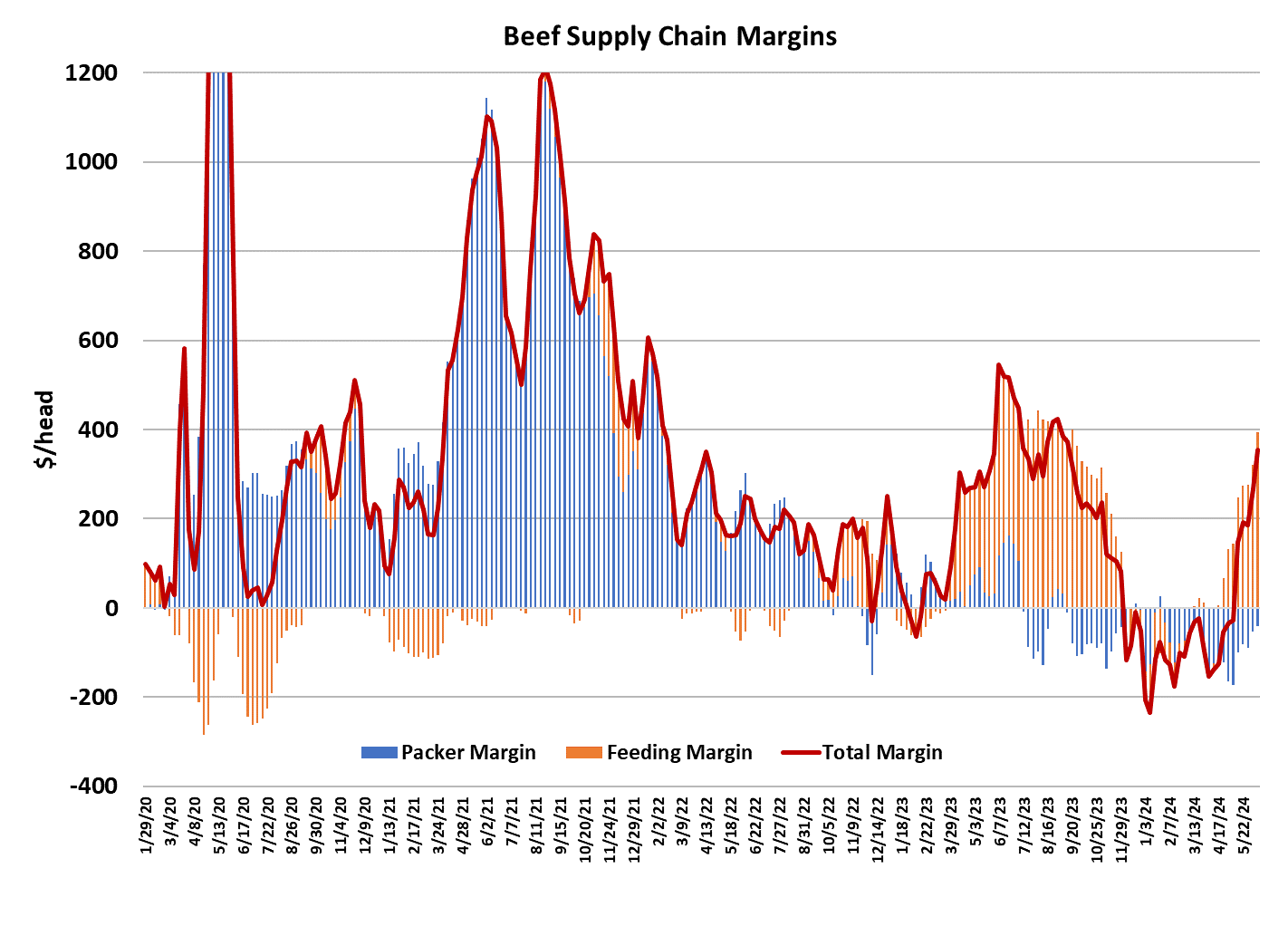

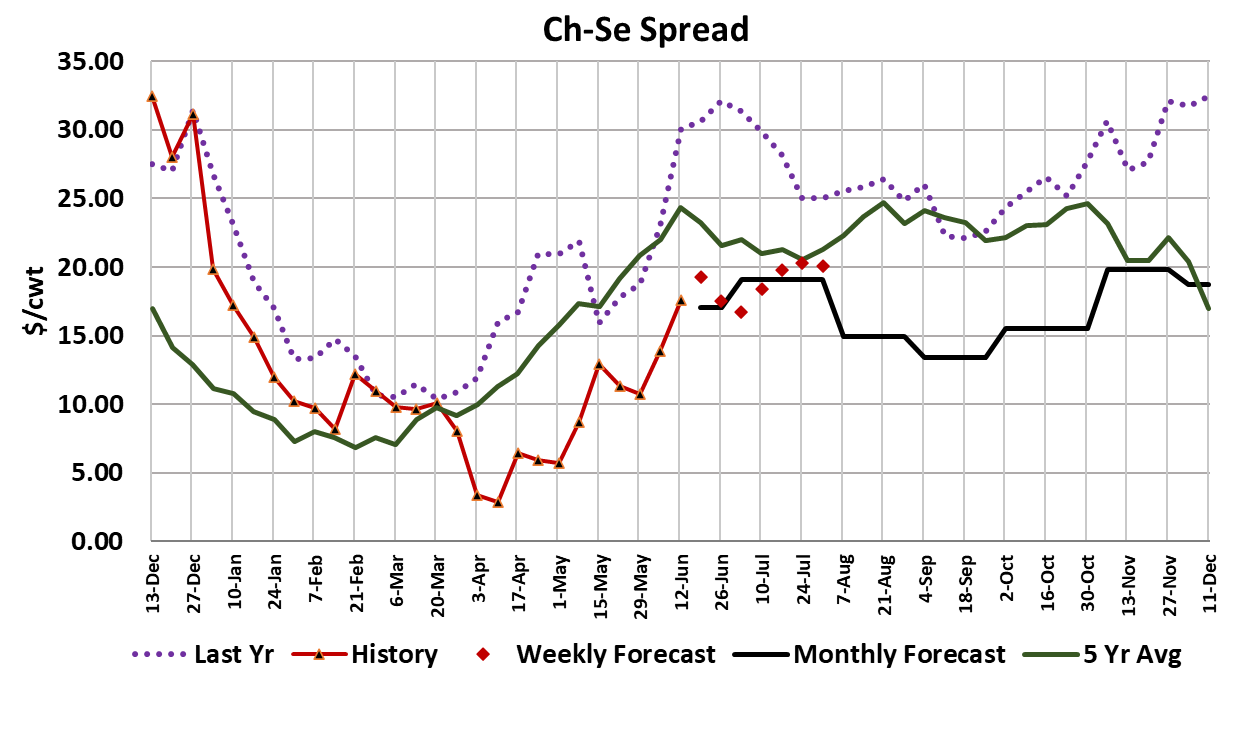

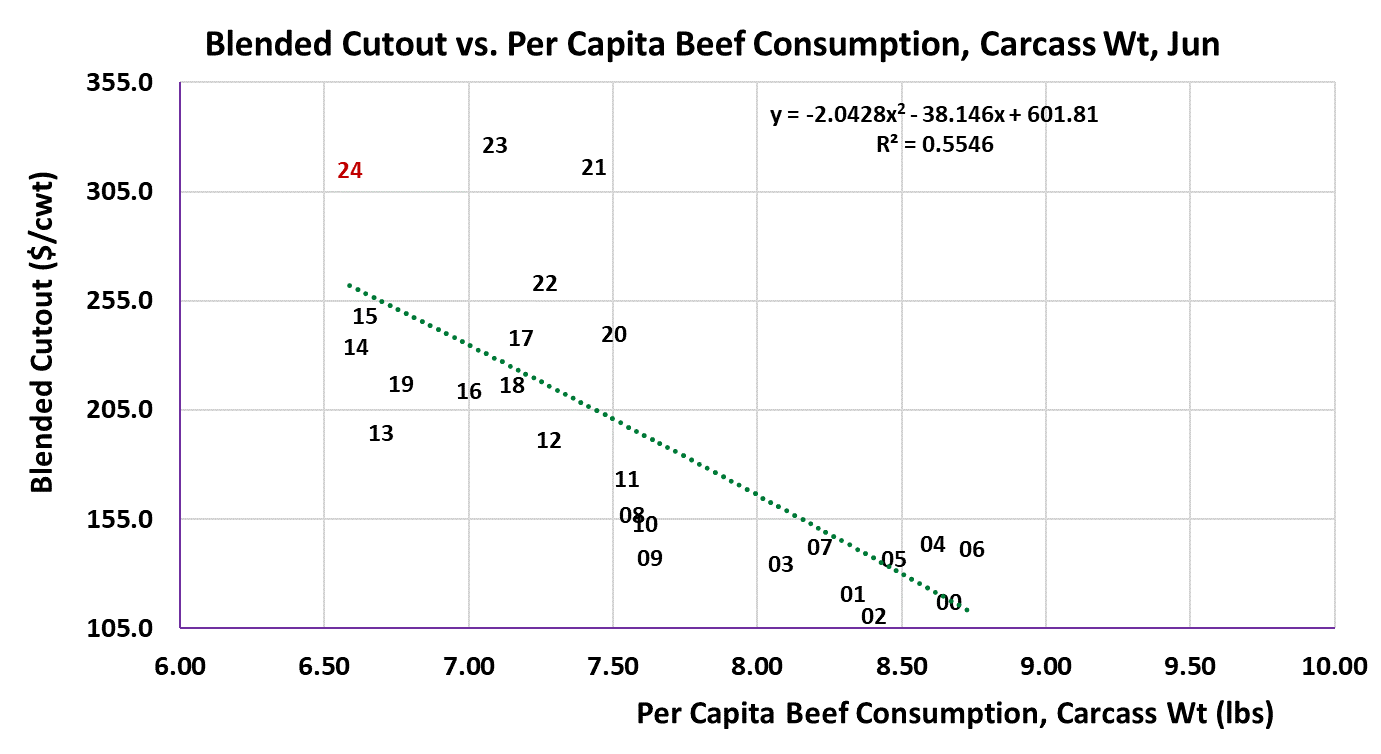

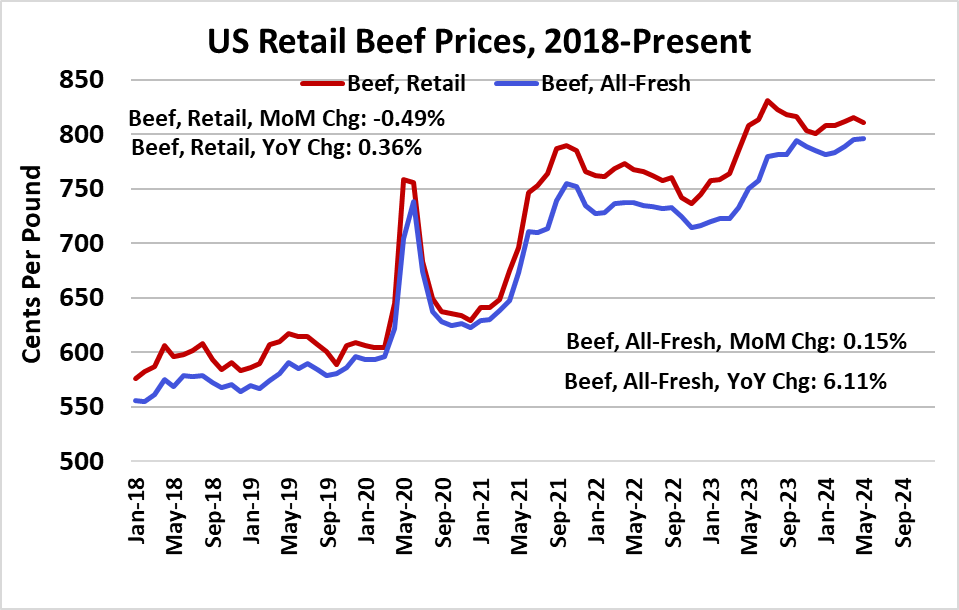

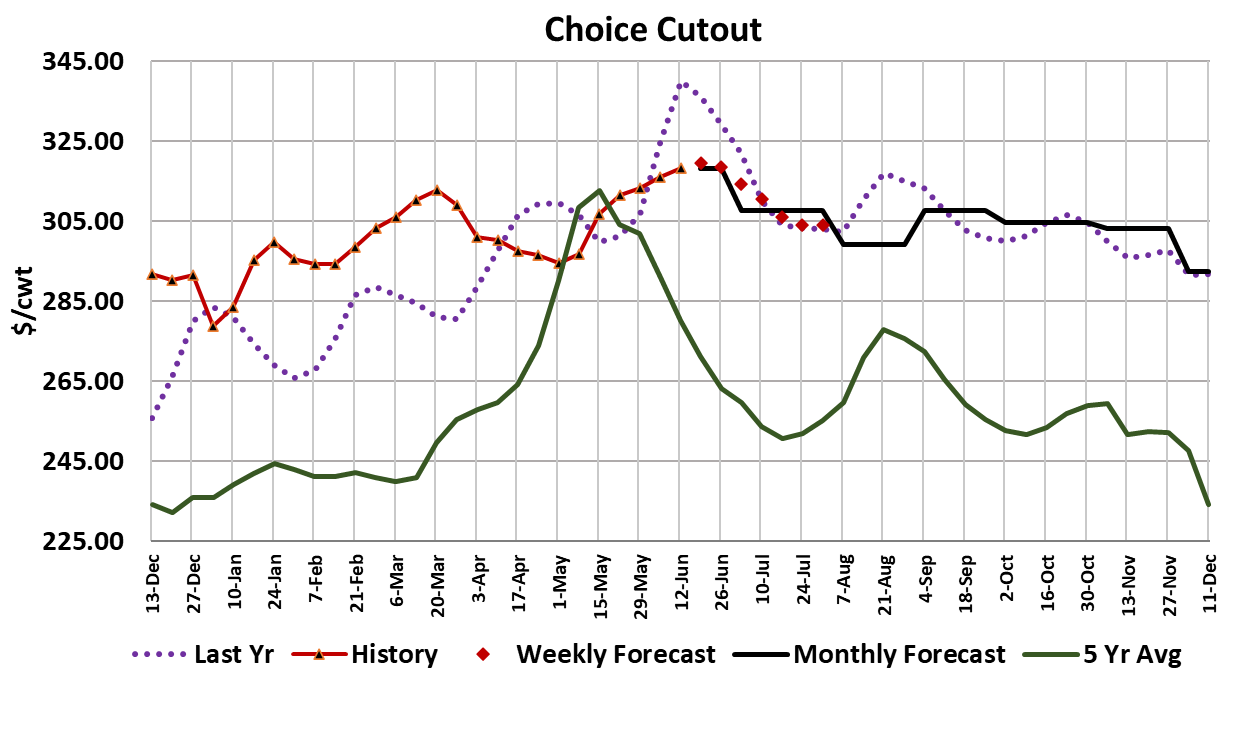

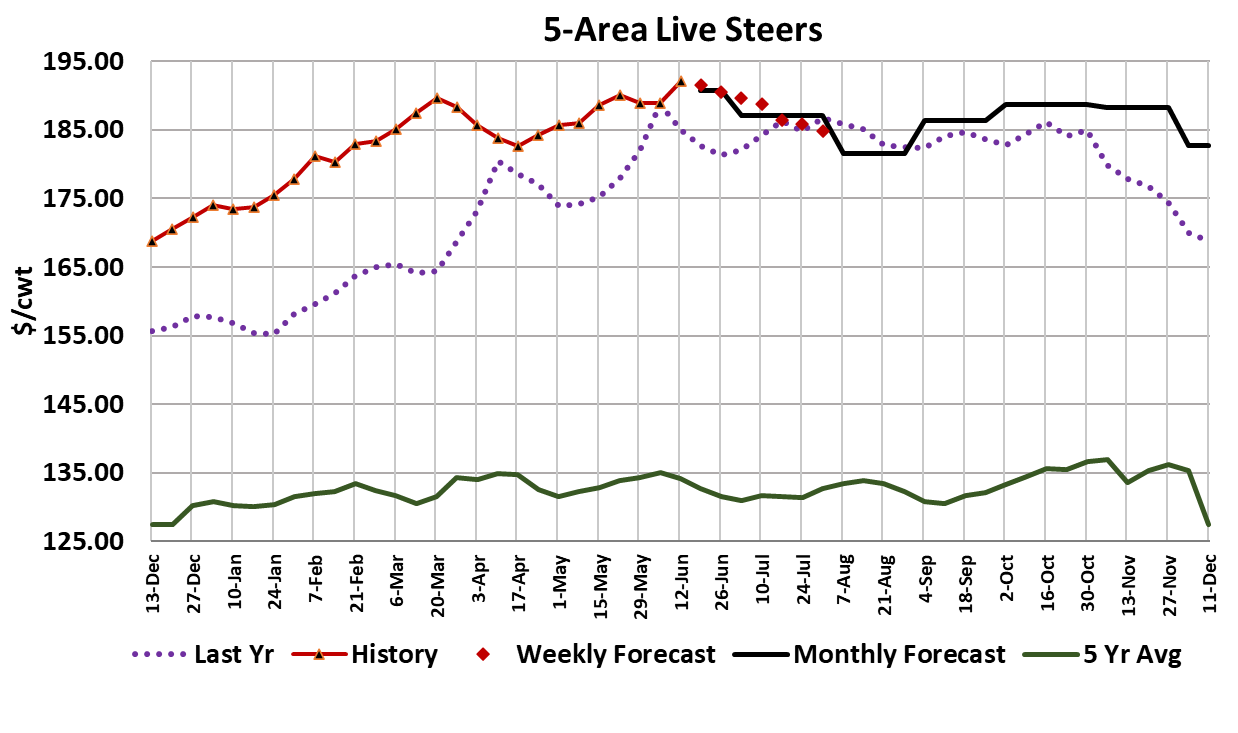

The cash cattle market in the North caught fire this week, with live trades reported in the $195-196 range, which is up $5-6 from last week’s trade in that region. The price advance was more muted in the South, where the majority of trades occurred at $186, up $1 from the week before. Clearly there is a supply imbalance between the Northern and Southern feeding regions as the price spread has now reached close to $10/cwt. That is a big enough difference to prompt packers to purchase “cheap” cattle in the South and truck them to plants in the North. Once USDA has complied all of the data on Monday, I expect the 5-area average to be a little over $192—a new record high and fully $3 over the previous week’s average. The volume traded this week looks rather large and usually when packers are paying sharply higher money for large volumes it is a bullish signal. This price action is certainly confounding to the bears who have been looking at carcass weights well over last year and expecting a price collapse. The FI steer weights were reported four pounds higher (in data for the week containing Memorial Day) and a whopping 37 pounds higher than last year at this time. As I’ve pointed out many times, this year’s carcass weight increase is not about cattle backing up in feedyards, but rather cattle feeders opting to make cattle heavier on purpose because their cost of gain is so much lower than it was last year. A nice side effect of feeding to heavier weights is that producers have more high-grading cattle to sell, which bring significant price premiums. June is prime time for selling high quality beef as consumers prepare for Father’s Day and Independence Day. The Choice-Select spread is now approaching $20/cwt., less than last year, but well off of the lows around $5 back in April. Given this week’s sharp increase in cattle costs, packers will likely be on the phone Monday morning informing beef buyers that prices have to go up. This week the Choice cutout increased $2.24 on a weekly average basis to $318.29 while the Select cutout dropped $1.48 to $300.73. Buyers that still need product for Independence Day features will likely be forced to pay up. The weather forecast looks very favorable for grilling across the US this Father’s Day weekend, so there could be good fill-in demand early next week. Of course, demand is not likely to stay red hot for long because once the calendar moves beyond early July, stifling hot weather and a lack of holidays normally results in a downshift in demand. The attached price-quantity scatter diagram for June, shows beef demand (for the blended cutout, deflated by the CPI) very close to where it was during 2014-15 period. It’s certainly not as strong as what we saw last year or in 2021, but demand seems to be holding together rather well. That helps to allay concerns about demand that were floating around back in the spring. This week’s fed cattle kill came in at 500k, which is just slightly below what the flow model suggests should be ready for market. Packer margins improved a little this week but are still about $37/head in the red. Next week, when those more-expensive cattle show up for slaughter, it is likely that packer margins will move deeper into the red. However, that is unlikely to prompt a reduction in the kill because packers probably have considerable Independence Day orders that need to be filled. Cattle feeding margins are now close to $400/head as cattle feeders reap the benefits of higher selling prices while their breakeven cost has been declining rapidly. The combined packer+feeder margin has rocketed higher recently and may soon challenge the highs made last spring. Retail prices were released this week and the results were a mixed bag with the traditional retail price series declining half-a-percent moving from April to May and the all-fresh series, which better captures feature pricing, showing a 0.15% increase over the same period. The message in this data is that retail prices might not be rising rapidly, but they certainly aren’t declining in a significant way. Export volumes continue to look mediocre, but probably a little better than should be expected given how high beef prices in the US are at the moment. On the macro side, this week’s CPI release showed inflation a little cooler than expected and that was cheered by the stock market with big gains. Gas prices in the US are also down from where they were earlier this spring and that often makes consumers feel better about the economy. With inflation cooling, there is a chance that the Fed will start to lower interest rates just a tad this fall and will also likely be cheered on by the stock market. Unemployment is slowly rising, but it is still at relatively low levels historically and it is very apparent that consumers are far more concerned about inflation than they are about unemployment. Overall, I’d say that over the past month or so, the macro picture in total has become a little more supportive of beef demand. Next week, look for some early-week gains in the cutouts that may begin to fade by the end of the week. Cash cattle stand a good chance of trading steady to higher, with low odds of a price reversal.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}