Beef Wrap May 10

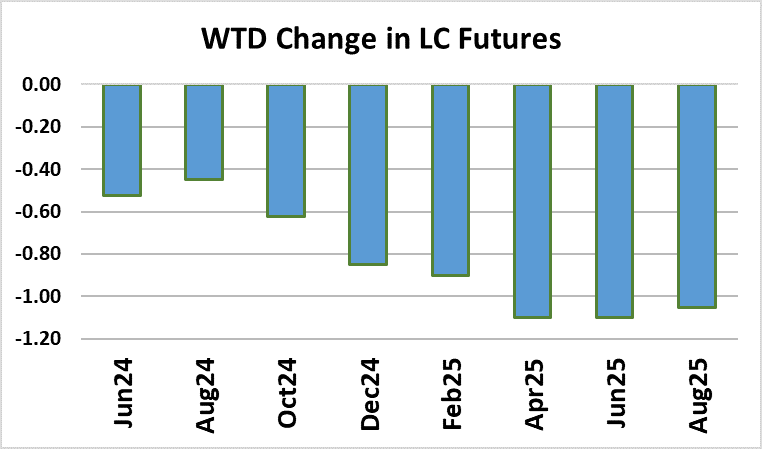

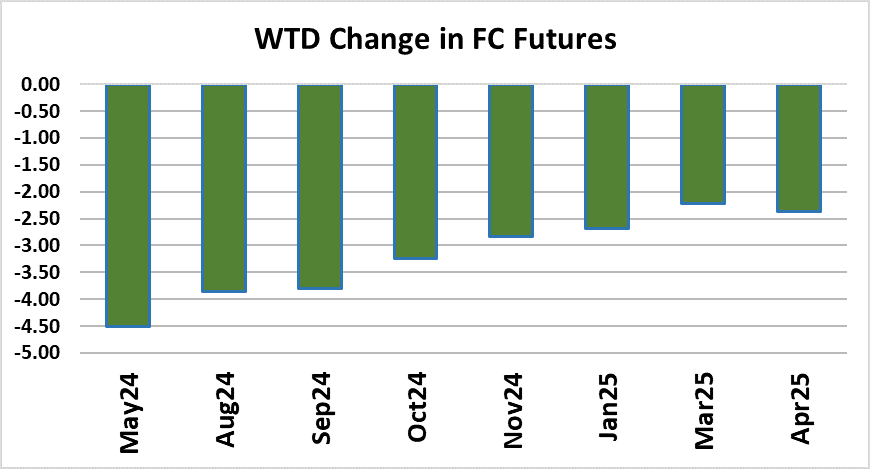

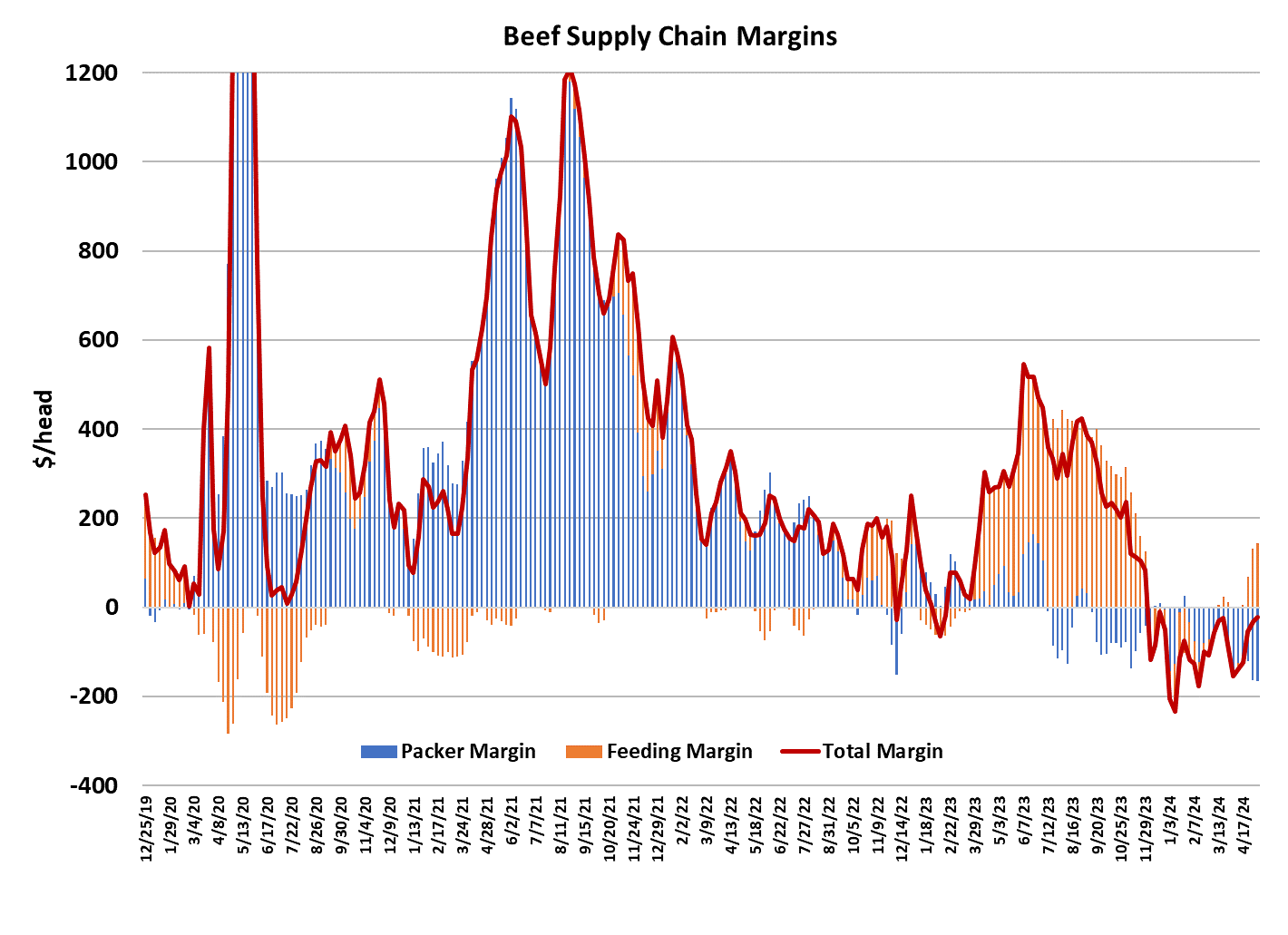

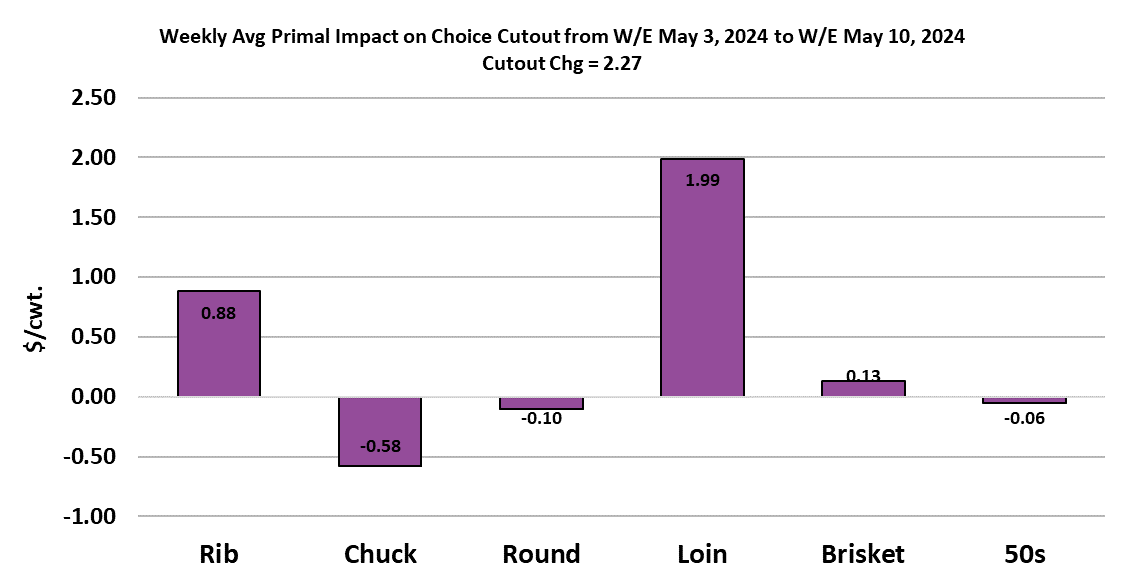

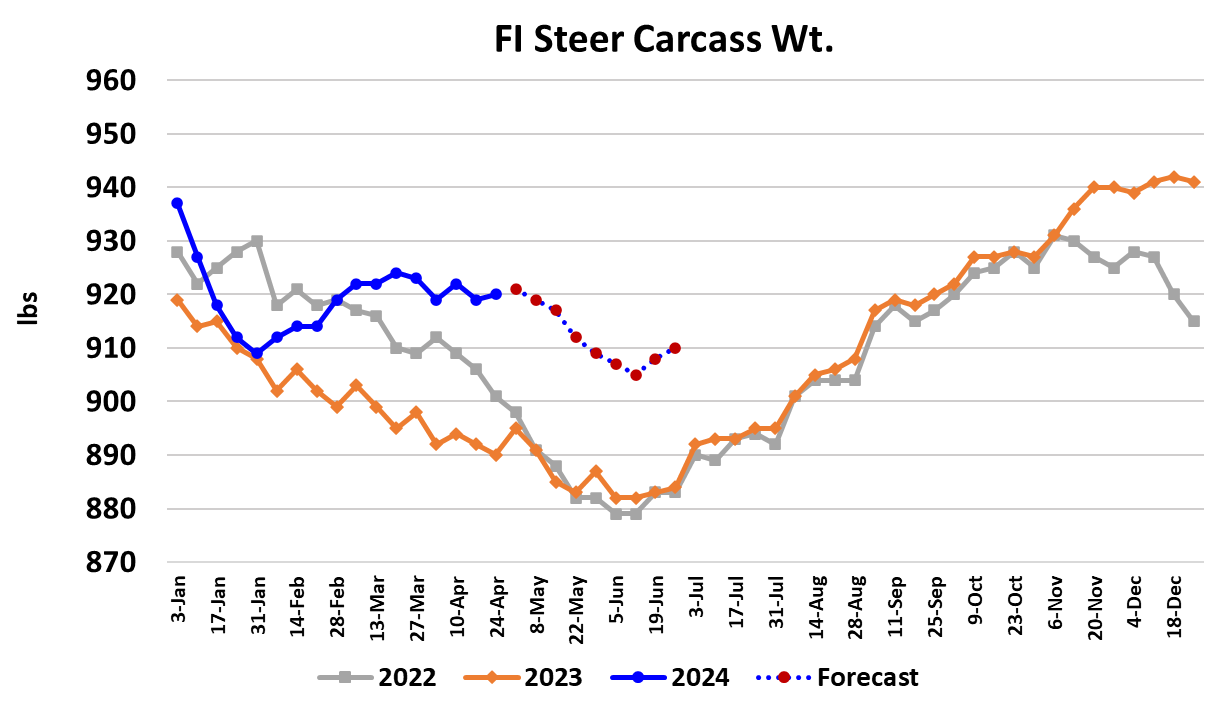

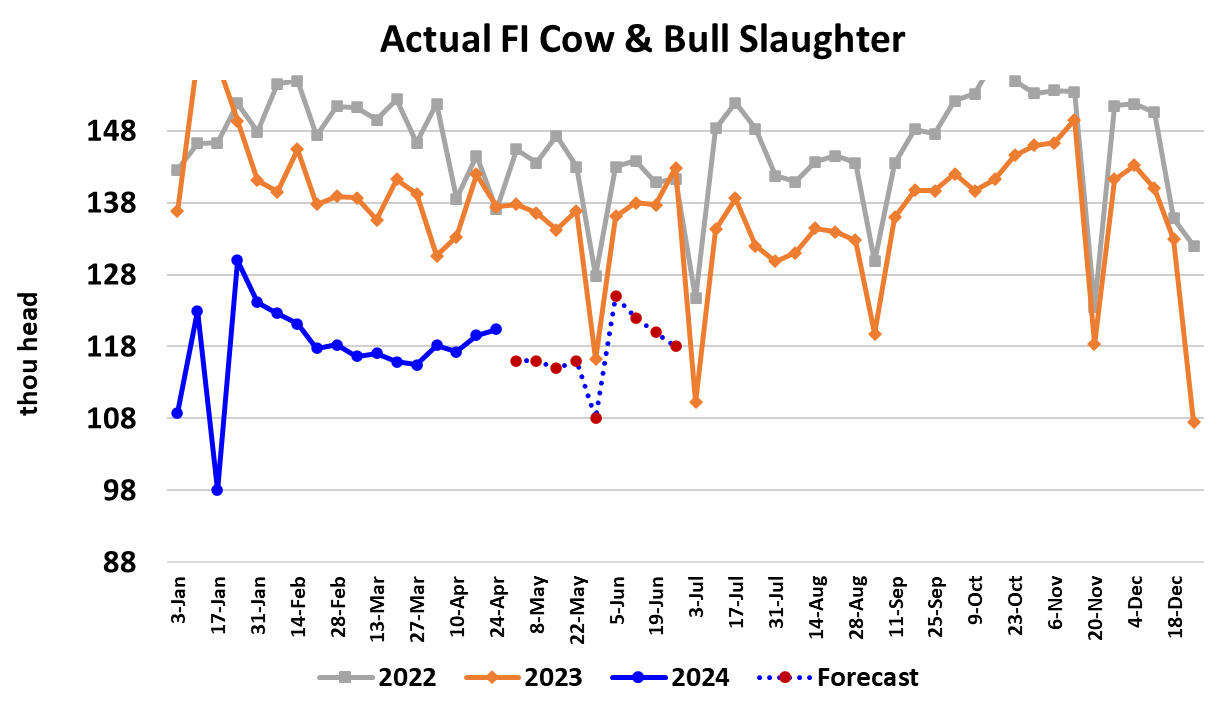

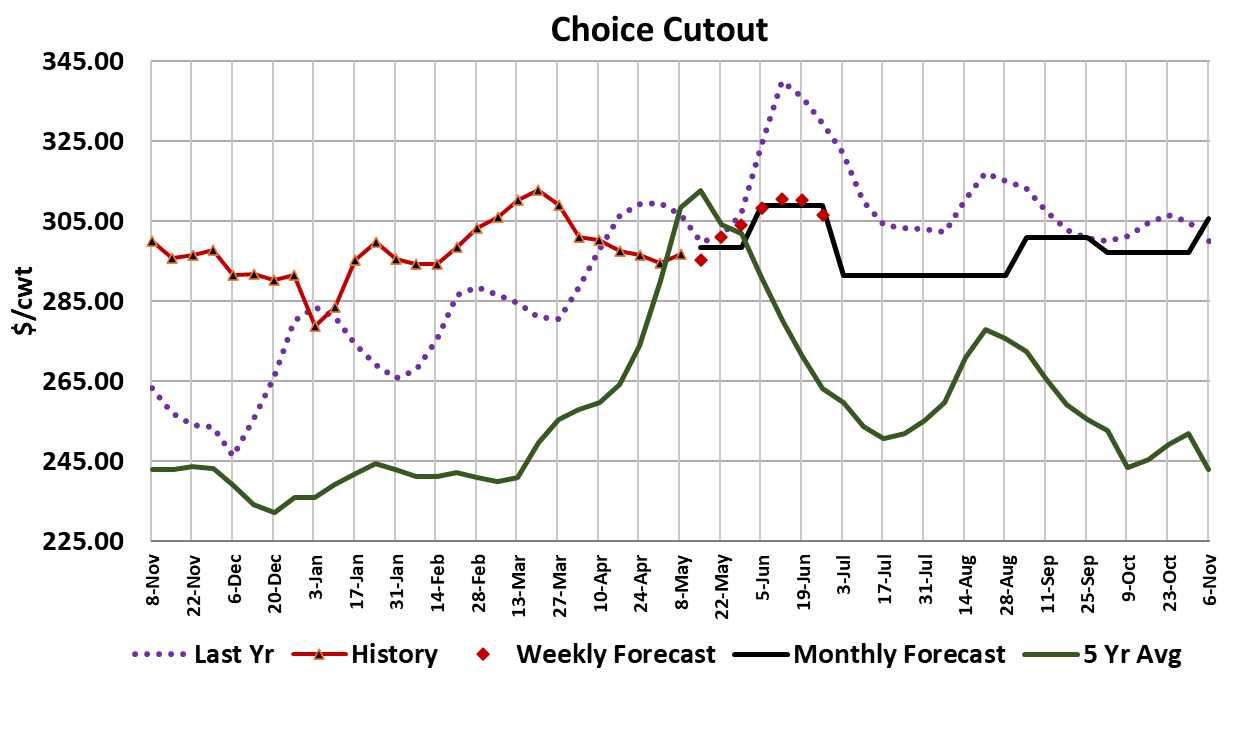

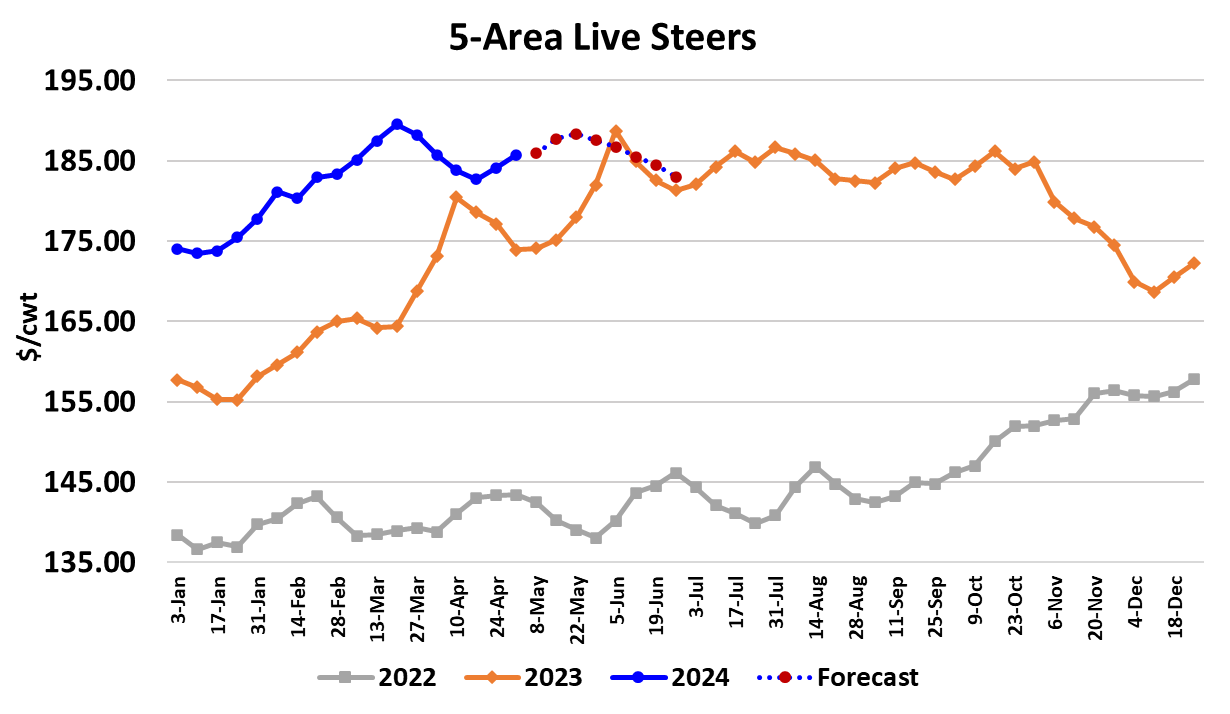

The beef cutouts finally got a little lift this week, with the Choice adding $2.27/cwt. to average $296.78 and the Select losing $0.72/cwt. to average $288.05. The gains were driven mostly by increases in the rib and loin primals, with all of the other primals either slightly lower or nearly unchanged on the week. For packers, even a little upward movement in prices had to feel good, but it falls way short of what is typical with only two weeks to go before Memorial Day. Packer margins actually got worse this week because the small gains in the cutout were not enough to offset last week’s $2 increase in cattle costs. I calculate this week’s margin at about -$170/head. Fortunately for packers they won’t have to deal with increasing cattle cost for next week’s slaughter because they managed to get cattle bought this week at an average price very close to last week’s $186. If they can keep the cutouts moving higher, then their margin situation should be a little better next week. Cattle feeders, on the other hand, are experiencing strong margins near +$144/head and that should grow to $250/head or more in the coming weeks as the breakeven value for cattle leaving the yards will be declining from now through June. Often times, cash cattle prices will loosely follow breakevens and given where we are in the calendar, it seems reasonable to expect some easing in the cash cattle market a few weeks down the road. The fundamental forecast suggests a little more cash strength as we approach Memorial Day and then prices decline in June. It is pretty amazing that cattle feeders aren’t exhibiting any sense of urgency to market cattle with steer carcass weights 30 pounds over last year. Steer weights were reported one pound higher this week, but heifer weights were four pounds lower. The challenge for packers is going to be to keep the cutouts supported until we get to the point where cattle prices have moved materially lower. That is probably do-able between now and Memorial Day, but the risk of cutout slippage increases once we are past the holiday. Thus, it seems likely that packer margins will remain solidly in the red for some time to come, and maybe all summer long. This weekend brings Mother’s Day, which is typically a good middle meat demand holiday, particularly through the foodservice channel. That could result in some restocking demand for middle meats that will generate more upward movement in the cutouts next week. The chuck and round primals both eased a little lower this week and the 90s were also down a small amount. That could be the beginning of a stall in lean beef prices, but Memorial Day is also a strong hamburger holiday, so I don’t want to call a top in the 90s too early. My guess is that they will still have a little more to gain between now and Independence Day, but would be likely to work lower after that. There was no avian influenza news of consequence this week, thus the futures were a little less volatile. While I do think that the cash cattle market has some downside risk in June, it is hard for me to see it losing $10, which is what the Jun futures are currently pricing in. In spite of their awful margin situation, packers seem to want to run large kills and that will probably continue into June, helping to clear some of the cattle backlog from feedyards. This week’s fed kill clocked in at 506k, identical to the previous week. Look for next week’s fed kill to be at least that large or bigger and then we will see a couple of sub-500k weeks leading up to the holiday. Obviously, the week that contain Memorial Day (which always falls on a Monday) will be a low kill, but packers also tend to restrict the kill on the Friday and Saturday before the holiday, so that will make the kill for the week that ends on Saturday the 25th a little light also. The cow kill is trending seasonally lower, with this week’s non-fed slaughter coming in at 116k, down from 138k in the same week last year. Pastures are in much better shape this year compared to last and feeder cattle prices are pretty high, so it’s not surprising that cow-calf operators are opting to send fewer cows to slaughter. Since the beginning of the year, non-fed slaughter is down a little over 15% compared to last year and that undoubtedly is contributing to the strength that we’ve seen in 90s prices this year. I would add that the strength in 90s pricing is not only coming from the supply side, but also from improved demand as it appears that consumers are trading down from expensive middle meats to more affordable grinds. So far, that is keeping most of the demand within the beef complex, but there is risk that soon consumers will take their trading down a step further and start to shift more toward pork and poultry. As a result, I’ve been tempering the forward demand indexes for the balance of 2024 in recognition that demand is not likely to live up to my initial expectations. Another development that doesn’t bode well for beef demand is the fact that retailers are featuring beef a lot less this year than in the past couple of years. Consumers can’t buy what they aren’t shown and typically more than half of the beef that moves out of the retail meat case does so at a feature price. That said, even if demand cools further in the next year or two, the price improvement from cyclically shrinking cattle supplies is likely to outweigh any losses from softer demand, keeping cattle and beef prices on their upward trajectory over the longer term. Next week, look for some further modest gains in the cutouts as last minute buying ahead of the holiday kicks in. Cash cattle are likely to be steady or higher unless a bird flu story slaps the futures market lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}