Beef Wrap March 9

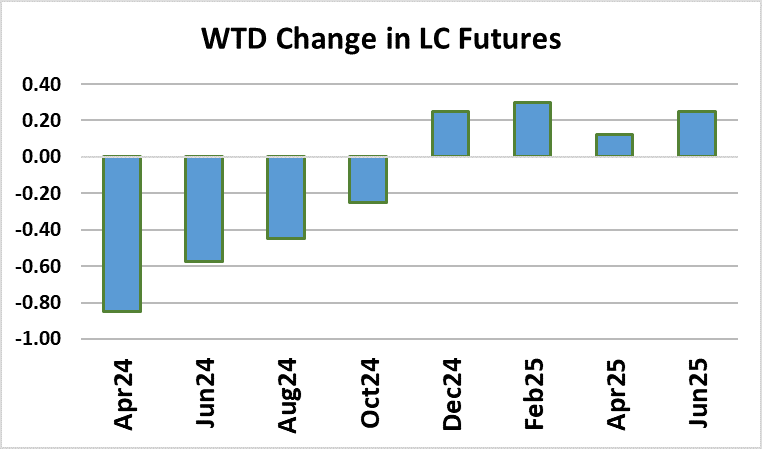

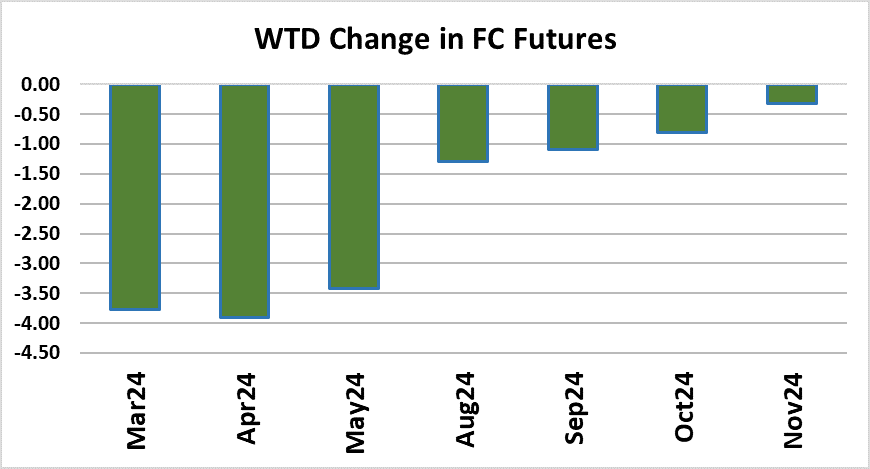

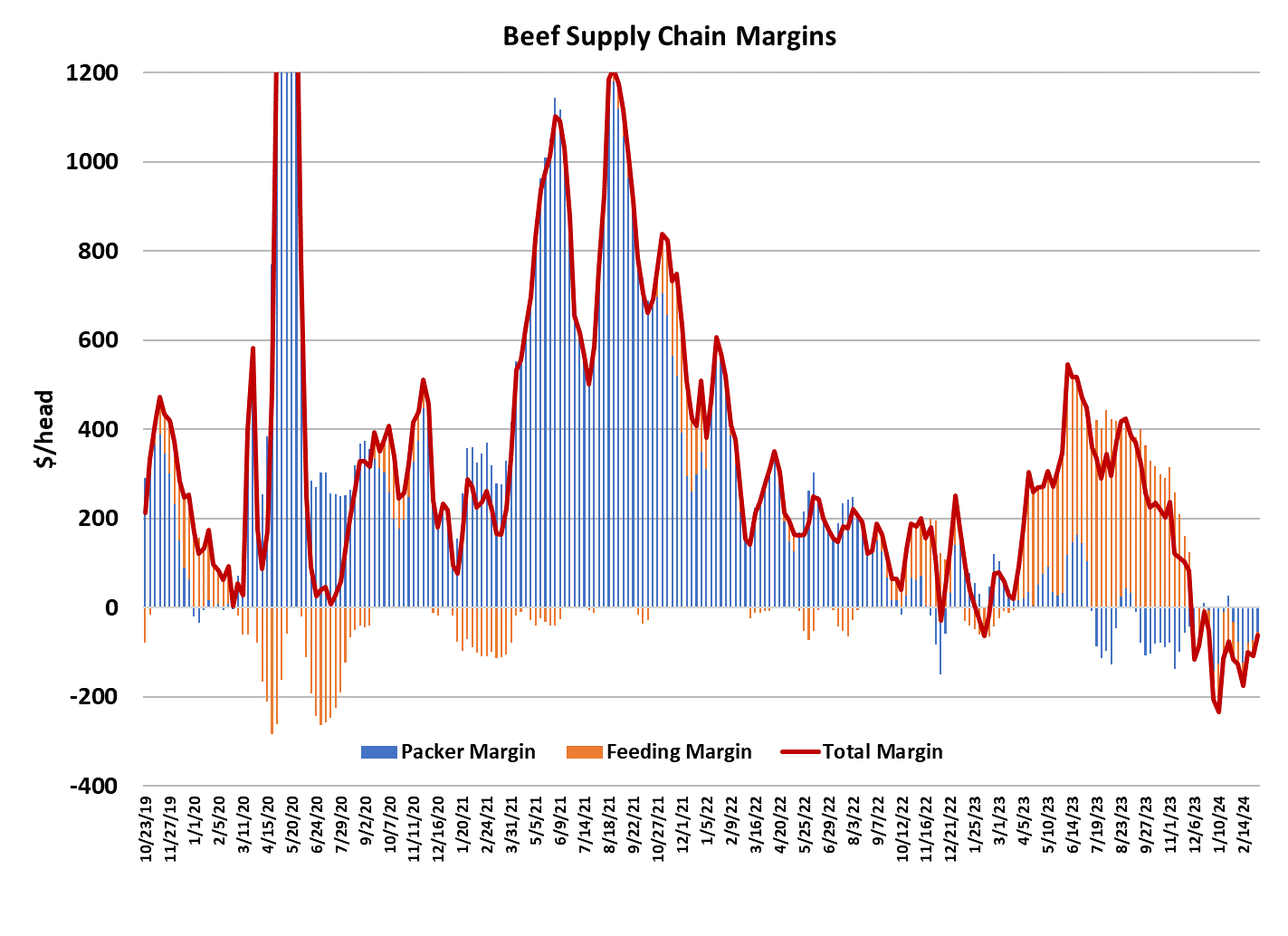

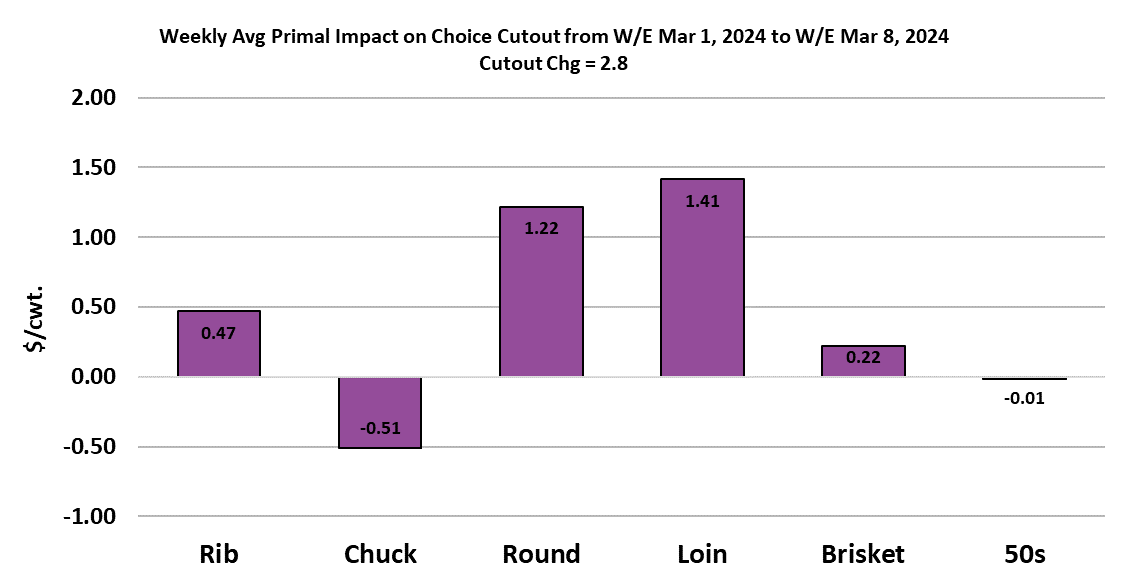

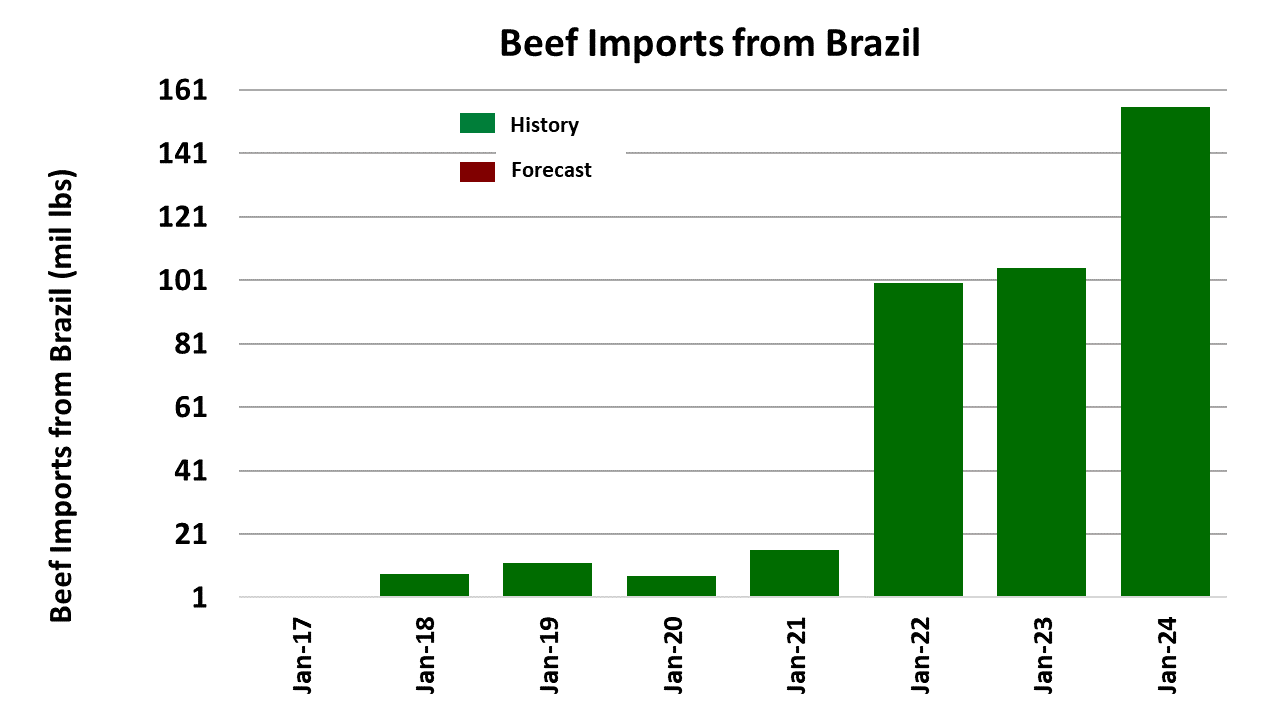

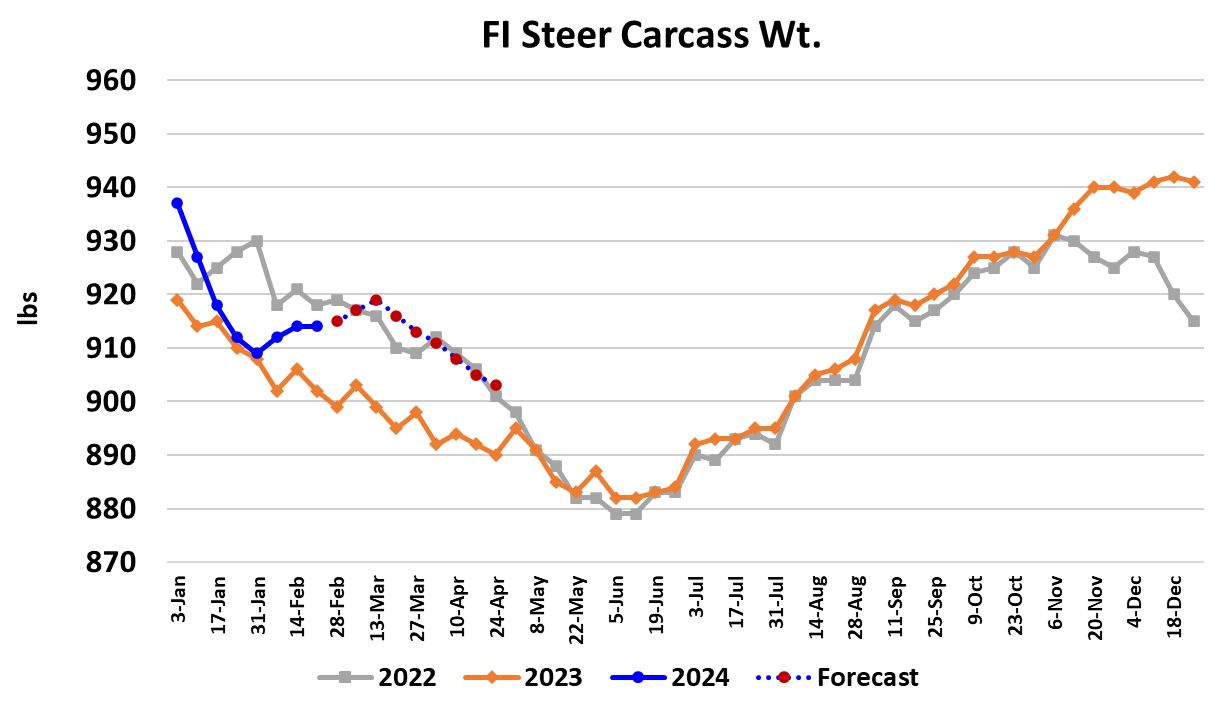

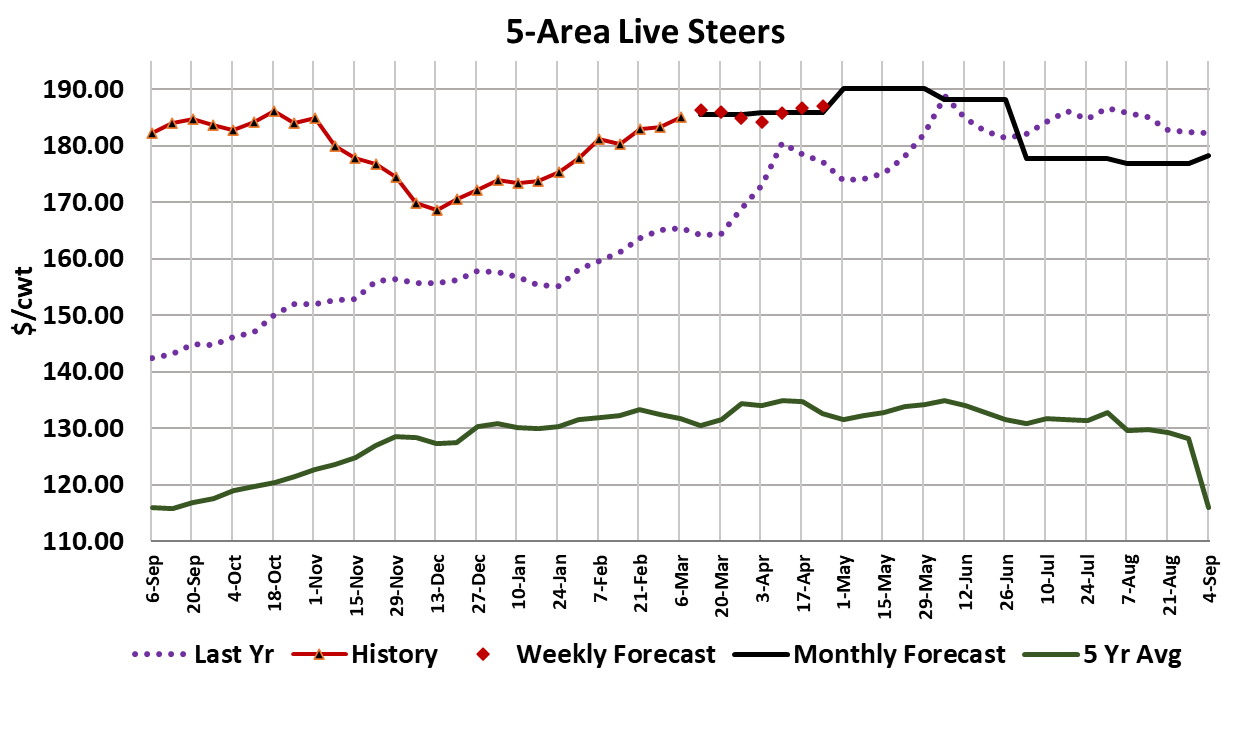

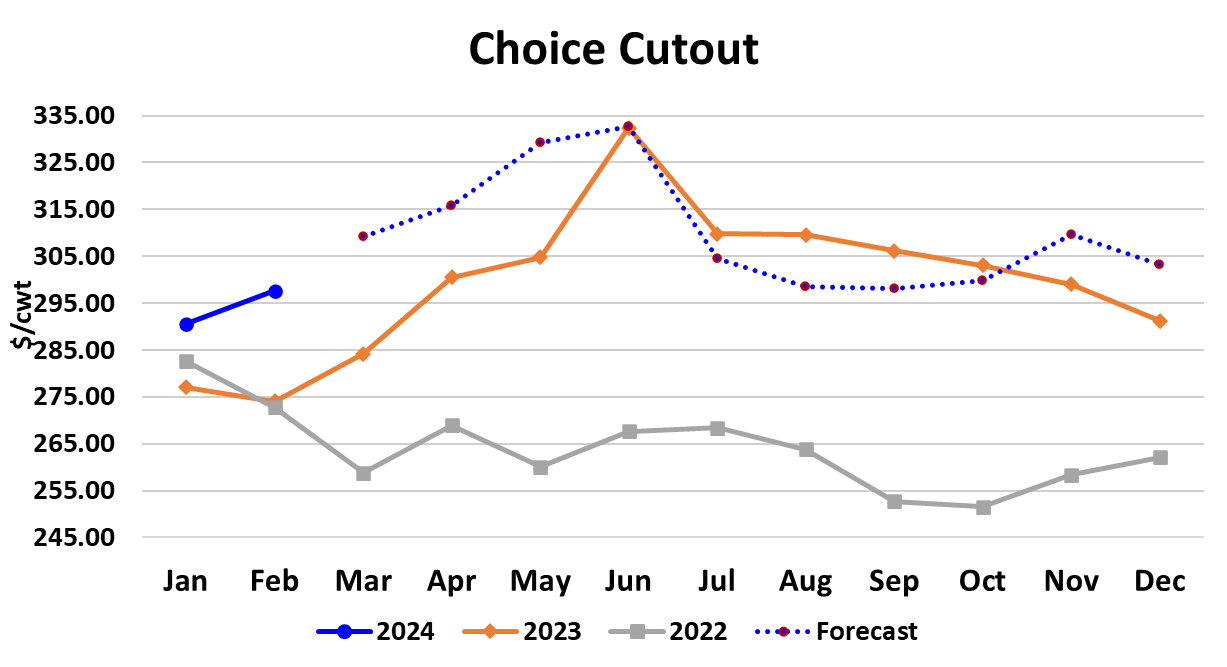

Another week, another increase in cash cattle prices. This week cattle feeders were able to coax another $2/cwt. out of packers as the cash trade nationally averaged a little over $185. Packers got a small consolation prize in the beef markets where the Choice cutout gained $2.80/cwt. on a weekly average basis in moving to $306 and the Select cutout added $3.95/cwt. on its way to $296.20. Packer margins are now estimated to be about $53/head in the red. It seems that slashing the kill the week before didn’t really do much to improve packer profitability, so they decided to double down on it this week and reduced the kill even further. Fed slaughter for the week was a tiny 458k, 11k below the previous week’s kill. There has been talk of slow kills causing cattle to back up since December, yet the steady upward progression of cash cattle prices suggests that it is the cattle feeder who is in the driver’s seat, not packers. Perhaps the kill-cutting strategy isn’t working because packers have deployed it right when cattle feeders decided that adding more days on feed would be a good way to avoid high feeder cattle replacement costs. A tumbling corn market made that decision even easier. Another reason that it isn’t working is because cattle feeders purposefully time placements so that they don’t have an abundance of cattle to sell during Feb/March, when demand it typically very soft and pricing is weak. So, when cattle feeders decided to extend the feeding period at the same time that available supplies are seasonally low, that created an even tighter supply of spot cattle. The carcass weight data clearly shows that feeders are succeeding in making cattle heavier. This week’s FI weights showed steer weights unchanged and heifer weights up three pounds. This is happening in a period of the year when carcass weights should be trending seasonally lower. The danger for cattle feeders comes if they carry this strategy too far and end up will lots of super-heavy cattle that need to be moved quickly. Packers won’t show much empathy if that situation develops. Since cutting the kill hasn’t worked very well, packers are likely to shift to another tried and true approach: scaring beef buyers with talk of even more severe kill reductions and thus very little availability in the near future. Sometimes that works, but sometimes it doesn’t, and this is the time of year when it isn’t likely to work very well because wholesale buyers aren’t seeing strong demand from their customer base. If we were in early May, then buyers might panic if told there might not be any ribs available for Memorial Day, but here in early March there is much less reason for buyers to panic. Of course, March will eventually give way to April and May when demand should be much better, so there is a good chance that the calendar will be what restores packer margins. There could even be a scenario later this spring where packer margins surge sharply higher because demand has improved and cash cattle prices have collapsed because feedyards allowed cattle to get too heavy by holding them on feed for too long. The combined margin is slowly working higher now, so perhaps some seasonal demand improvement is already beginning to surface. I don’t want to make it sound like beef demand is awful right now, because that isn’t the case. The blended cutout demand indexes for January and February are averaging about 3% better YOY and about 8% better than the ten-year average. International demand for US beef isn’t all that shabby either. Total beef exports for January were down only 4.1% YOY and that comes after beef exports for all of 2023 were off 14%. No one seriously expects exports to post YOY gains with the cattle supply shrinking and price levels rising, but to be down only single digits is a notable accomplishment. Beef imports during January were reported up 38%, mostly as a result of huge in-shipments from Brazil. Brazil doesn’t have its own tariff rate quota (TRQ), it shares in the “Other” quota with several other countries. Apparently, Brazil got busy in January trying to fill as much of that quota as possible. Futures traders weren’t all that impressed with this week’s gain in the cash cattle market as the spot Apr contract lost $0.85/cwt. on the week. But at today’s close of $187.60, the Apr futures are only a little over $2 higher than the current cash trade, so traders must be expecting cash prices to stumble at some point before Apr expires in two months. I tend to agree with the futures that cash cattle prices will set back at some point, but I’m not looking for a huge collapse unless carcass weights continue to trend counter-seasonally higher. Beef buyers probably should prepare for steadily increasing prices through spring and into summer regardless of what the cash cattle market does. The current forecast has the Choice cutout approaching $330 by May and that may be too low. Next week, expect the cutouts to continue higher on this week’s smaller production and look for a cattle market that trades no worse than steady.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}