Beef Wrap March 1

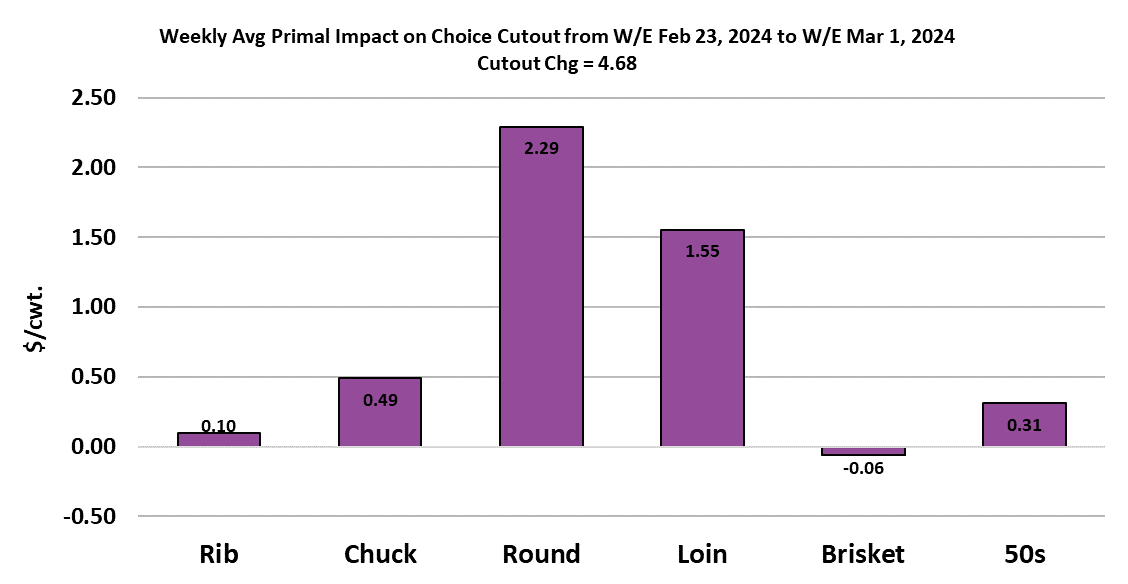

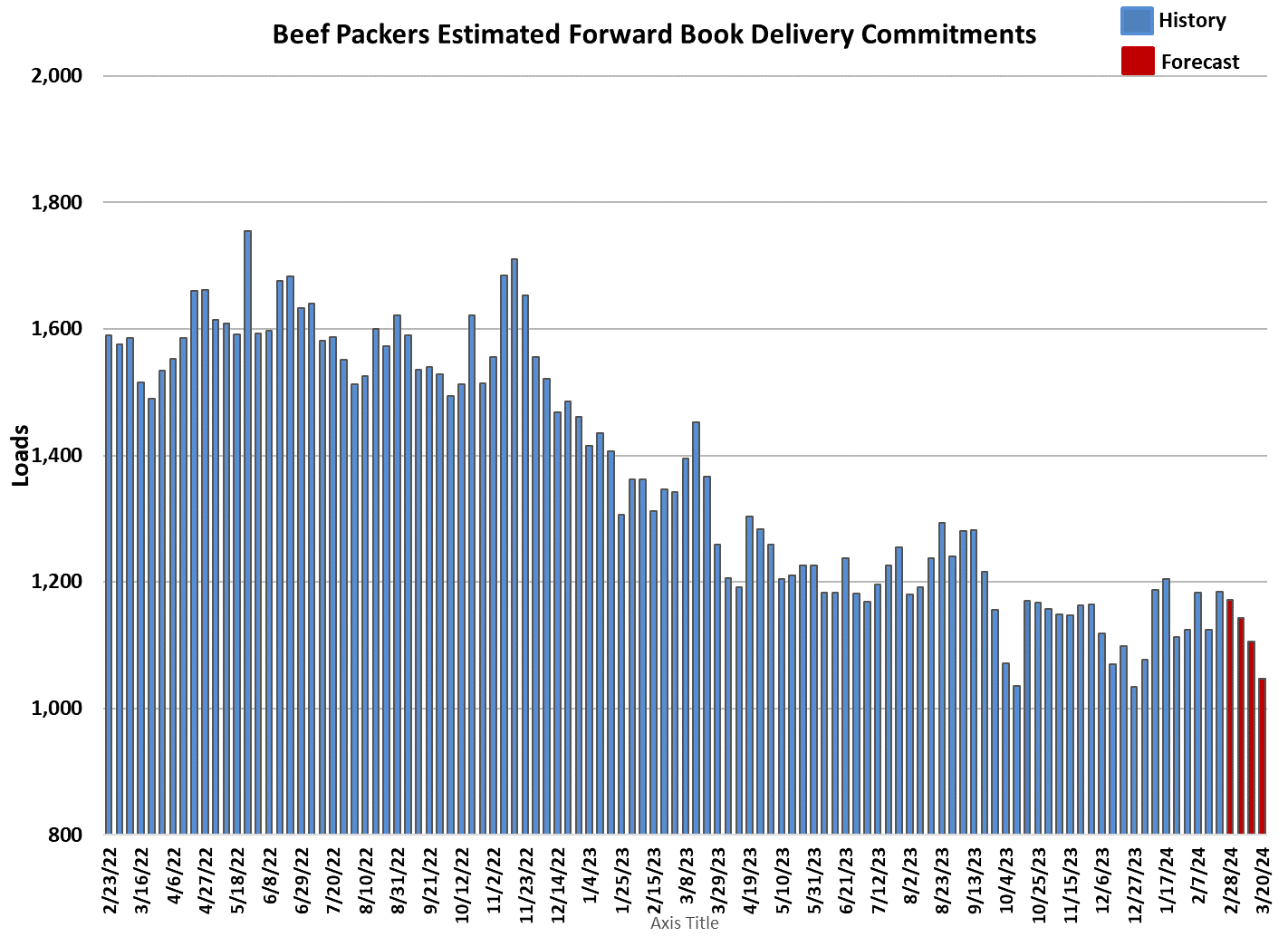

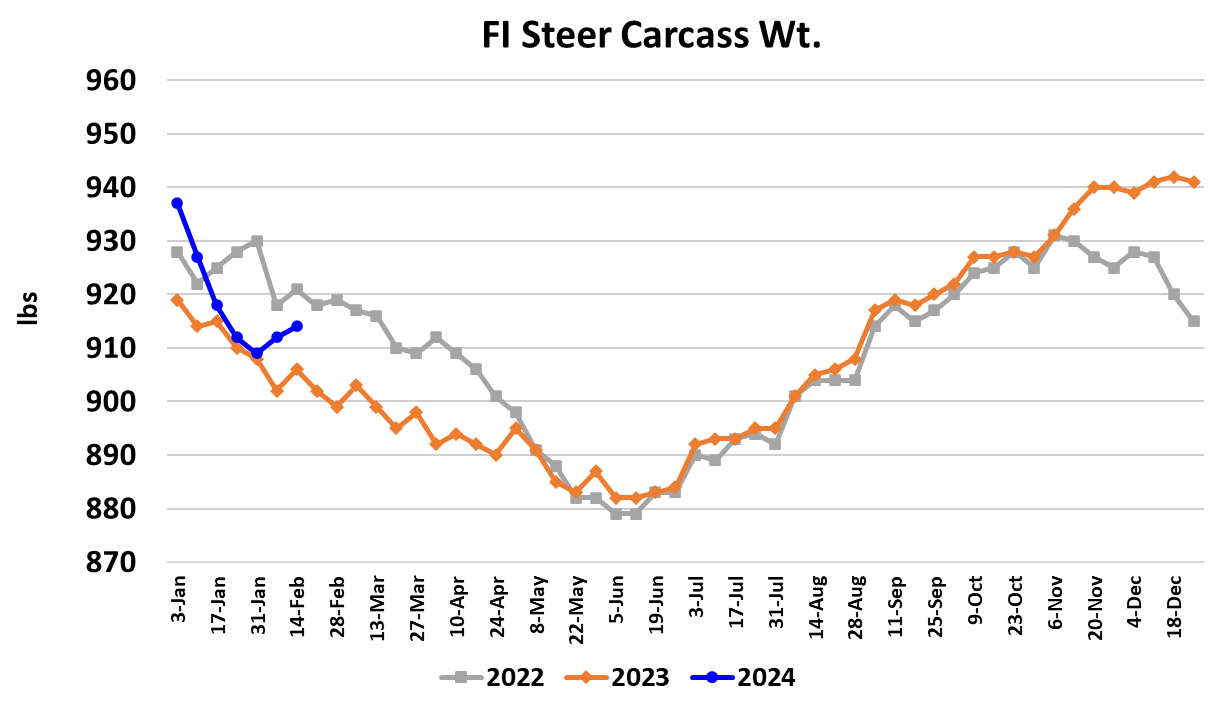

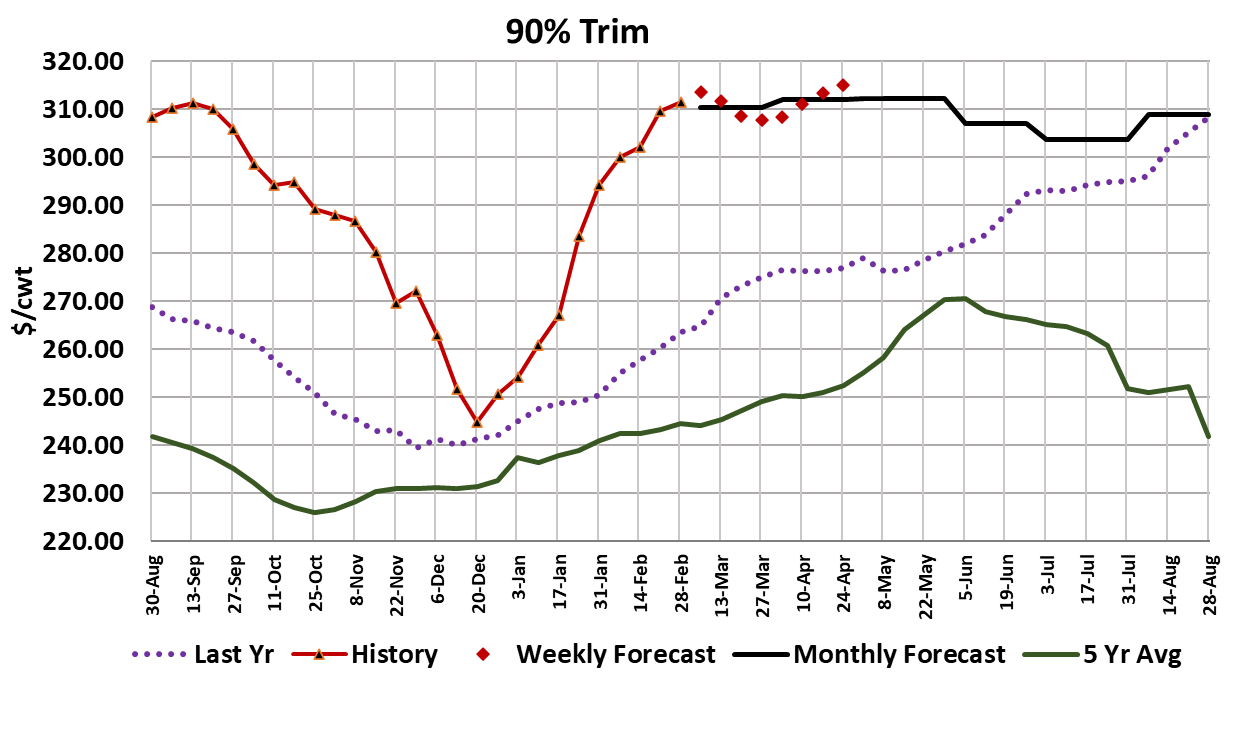

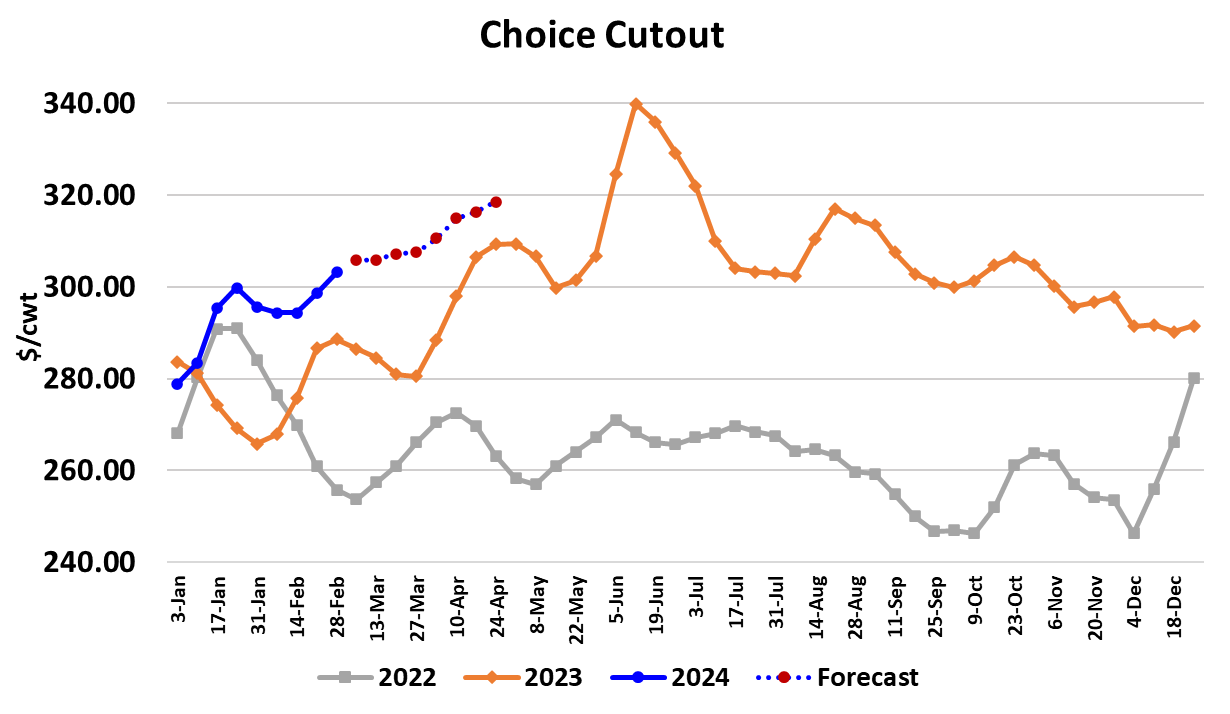

Packers slashed the kill last week in hopes of correcting their dismal margin situation and it worked to a small degree. The Choice cutout gained $4.68/cwt. on a weekly average basis and the Select cutout added $5.89/cwt. That was just a little more of an increase than was needed to cover the cost of the more-expensive cattle that showed up for slaughter this week. As a result, packer margins improved by about $7/head, but they are still $73/head underwater. However, the small kill wasn’t enough to help them with their cattle costs as the average live price this week was close to $183.40, about $0.50/cwt. higher than the week before. Packers let up off of the brakes just a little this week and the fed kill was 10k larger than the week before at 470k head. The non-fed slaughter, cows and bulls, was down 7.1% YOY at 129k. It does make one wonder if packers are capable of reducing the kill enough to bring their margins back into the black. Would a 450k fed kill do the trick, or how about 420k? One problem packers face is that their per-unit cost of producing beef soars when kills are very tiny because their high fixed costs have to be spread over fewer pounds of production. In addition, many packers have union contracts with their workforce that limit the number of weeks when they can run the plant less than 40 hours per week. So the answer may be no, packers can’t cut the kill enough to push their margins back above zero and hold them there. They will need to wait until better demand bails them out. That is coming in the next couple of months as the calendar turns to spring and the weather warms, but for right now the small gains we are seeing in the cutouts are the result of reduced production, not stronger demand. Packers are fortunate that they have a very small amount of booked business to deliver against in the next few weeks (see attached chart), or otherwise they might need to run bigger kills just to fill committed orders. The combined margin ticked lower this week after a modest gain the week before and it remains solidly in negative territory. That suggest that demand is still sinking seasonally, or perhaps treading water at best. This week it was the round primal that led the cutout higher, with the loin in second place. End cuts are no doubt getting some support from rapidly increasing lean trim prices, with some users finding it advantageous to grind items from the chuck and round rather than chasing after the 90s. I mentioned above the that the non-fed kill was down a little over 7% YOY this week, but since the beginning of the year, non-fed slaughter is down a whopping 16.5% YOY. Some of that may be attributable to the super-frigid temperatures in early January, but certainly not all of it. So why is non-fed slaughter running so light lately? Well, first of all, it is important to recognize that last year’s drought was forcing lots of cows to slaughter and so part of the reason that this year’s totals look so much smaller is because the non-fed kill last year at this time was exceptionally large. However, now that the drought has subsided in most of the cattle regions, it appears as though pasture will be abundant this spring and summer so that is likely prompting some producers to keep cows that might otherwise have gone to slaughter. If that’s true, it could be the very first inklings of a herd stabilization, or perhaps even a herd rebuilding effort. To be sure, significant herd growth won’t happen until cow-calf producers start retaining heifers to add to the breeding herd and there is no evidence of that so far. Perhaps we will see that start this spring if the rains keep coming. Domestic 90s prices averaged over $311/cwt. this week and that is about $48/cwt. stronger than last year at this time. Fat trim is pretty rich also, averaging just over $101/cwt. this week, but that is about $22/cwt. below last year’s level. There have been reports that foodservice business has been cooling since the first of the year, which may mean that consumers are finally starting to curb their spending. So far, that hasn’t shown up in the macro level data though. Cattle feeding margins have improved a bit since January and are now running only about $35/head in the red. Their breakeven price is running close to $186, which isn’t too far off of the $183.50 cash trade that we saw this week. Feeder cattle prices are very high and so many feeders are likely opting to keep the cattle they have and make them heavier rather than rush them to slaughter. That could help “spread out” the fed cattle supply and thus limit the effects of any backup that recent small fed kills may be causing. However, there is danger in that strategy because if the seasonal demand boost is slow in coming, cattle could get very heavy and that usually leads to a sharp reduction in cash cattle prices as producers find they must market cattle at whatever price the packer is willing to offer. This week, steer weights were reported up two pounds and that is the second week in a row where carcass weights have moved counter-seasonally higher. The attached chart shows just how odd that is compared to the normal seasonal trend of declining weights. If weights don’t decline at least a little in next week’s data, my worry about backing cattle up will increase. It seems likely that we will continue to see more of the same in the cattle and beef markets over the next few weeks, with packers keeping the fed kill very low and thus generating higher beef pricing by constraining production. Cattle feeders will see the cutouts rising and figure they are entitled to higher cattle prices as a result. Like a game of musical chairs, the music will stop suddenly one day, probably with little warning, and leaving somebody with no good options. That’s when prices could make a sharp correction lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}