Beef Wrap March 5

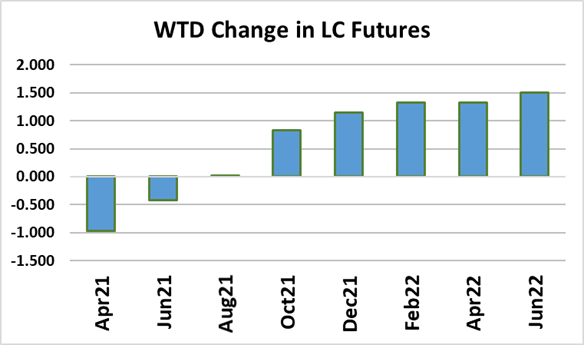

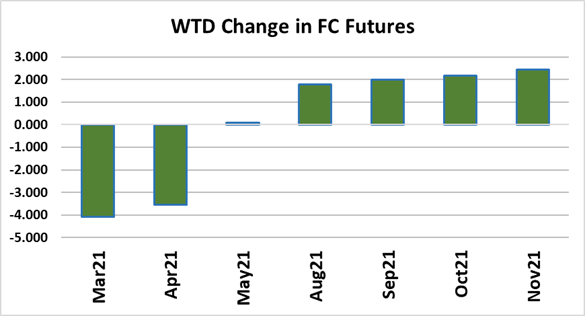

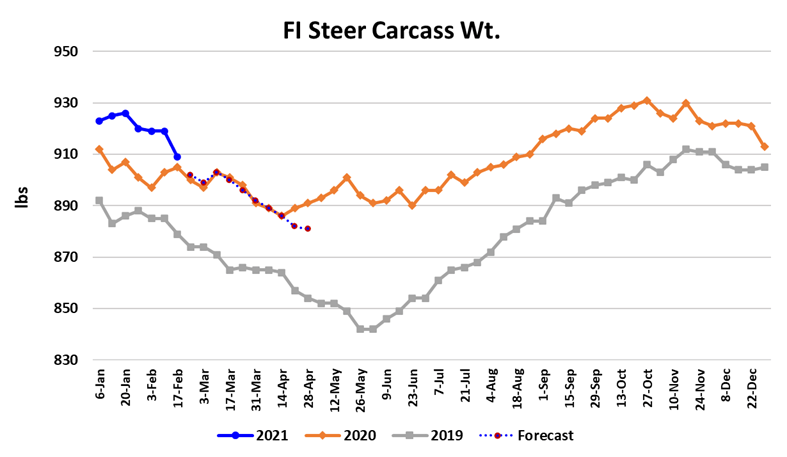

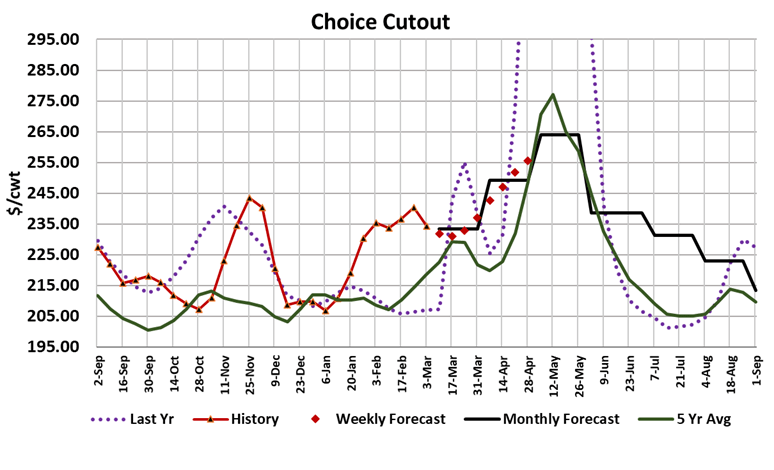

Another week with the cash cattle market stuck at $114. The cutouts are retreating now after posting a top in the week following the deep freeze. On a weekly average basis, the Choice cutout was down $6, while the Select was off more than $5. The decline in the cutouts was not unexpected and perhaps it is asking too much for the cash cattle market to advance in a week when the cutouts are down so hard. However, I think that this downdraft in the cutouts is going to be rather brief—perhaps lasting only another couple of weeks before spring demand starts to creep into the market and turn beef values higher. Packer margins fell to $327/hd this week and should compress further next week on a weaker cutout and steady cash cattle values. This week¡¯s fed kill registered 523k, considerably larger than the 500k or so that our flow model would have projected for this week. This extra kill is helping to work through the cattle that went un-slaughtered during the deep freeze week. I would look for a similar to maybe slightly smaller kill next week and then the kill could drop even further as the Cargill plant in Schuyler, Nebraska is scheduled to go down for a week of maintenance on March 18. Cargill will likely shuttle animals around to some of its other plants and that may keep the slaughter drop from being too severe. But what happens when we get to April and the flow model points to fed kills in the 470-480k range? Packers may actually be forced to compete for available cattle because by then cutouts should be rising again on seasonal demand strength and that will have packers eager to capitalize on that. The supply side of the market got some much needed good news this week when steer carcass weights recorded a 10 pound drop. That was caused by the artic blast a couple of weeks ago and some preliminary data suggest there could be another 6-7 pound drop in next week¡¯s data release. As it stands now, steer weights are only 4 pounds over last year and after next week they could be close to even with last year. That is quite a turnaround from last fall when weights were running 30-40 pounds over last year. Getting the carcass weights back in line is the last piece of the puzzle in the covid recovery process for the cattle market. Now, if cattle feeders can just resist the temptation to reload feedyards to the brim, they might actually stand a chance at turning a positive profit at some point later this year. Of course, the deferred futures have been bid up to really high levels and that will encourage strong placements as we move through spring and early summer. The next COF report will be released two weeks from today and I¡¯m guessing that it will show February placements up 1.4% YOY. Fortunately, February is a small placement month and so a small increase on a small number doesn’t amount to a whole lot of additional cattle. I¡¯m more concerned about how big placements might get in the March/April/May period. On the demand side, we have domestic demand working lower after a phenomenal performance in Jan/Feb and the combined margin chart below verifies this. We have also seen the daily demand scatters move lower in recent days. My fundamental forecast has the Choice cutout declining perhaps another $5-10 before turning higher as the spring demand starts to kick in. The chart below shows the loins as the biggest drag on the cutout and that is not too surprising at this point in the calendar. Towards the end of March, retailers should start gearing up for their post-Easter features and beef is likely to have a prominent role in those ads. Of course there is always the risk of the pandemic fading (which we recognize would be bad for beef demand) before the spring grilling season can kick in. Vaccination activity in the US has really ramped up following the deep freeze and we might be surprised at how quickly we get to a level that has people more comfortable mingling and traveling again. Congress is still haggling over the next round of stimulus and it is a doozy at 1.9 trillion dollars. As it stands now, the bill would put $1400 in the pockets of every taxpayer making $80k per year or less. I think that the bill will pass within the next two weeks and checks will be mailed out quickly after that. The stimulus funds will put quality beef within the reach of lower income individuals and so may provide an offset to any loss in demand that might come from upper income individuals heading out on vacations as the pandemic subsides. I¡¯m betting that spring is going to see strong beef demand, particularly for the middles. Demand in the second half of the year might not be so rosy. The failure of the cash cattle market to advance any in the last four weeks is causing the futures market to lose faith. The Apr contract dropped another dollar this week and is now about $7 off of the highs that were posted back in the middle of February. Traders haven¡¯t punished the Jun contract nearly as much and it is almost as if they haven¡¯t given up on stronger pricing this spring but rather are just pushing it further back in the calendar. Currently index funds are busy rolling longs out of Apr and into Jun, so that is further depressing the Apr contract. Next week, watch those carcass weights and how fast the cutouts work lower. Both will tell us a lot about how long this soft spot in the market will last.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}