Beef Wrap June 23

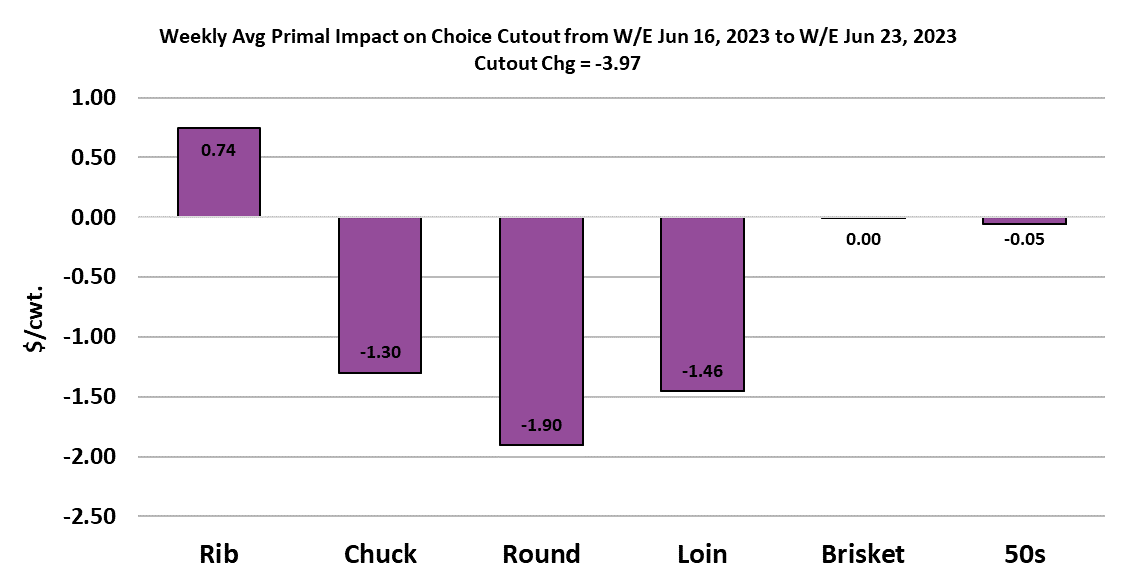

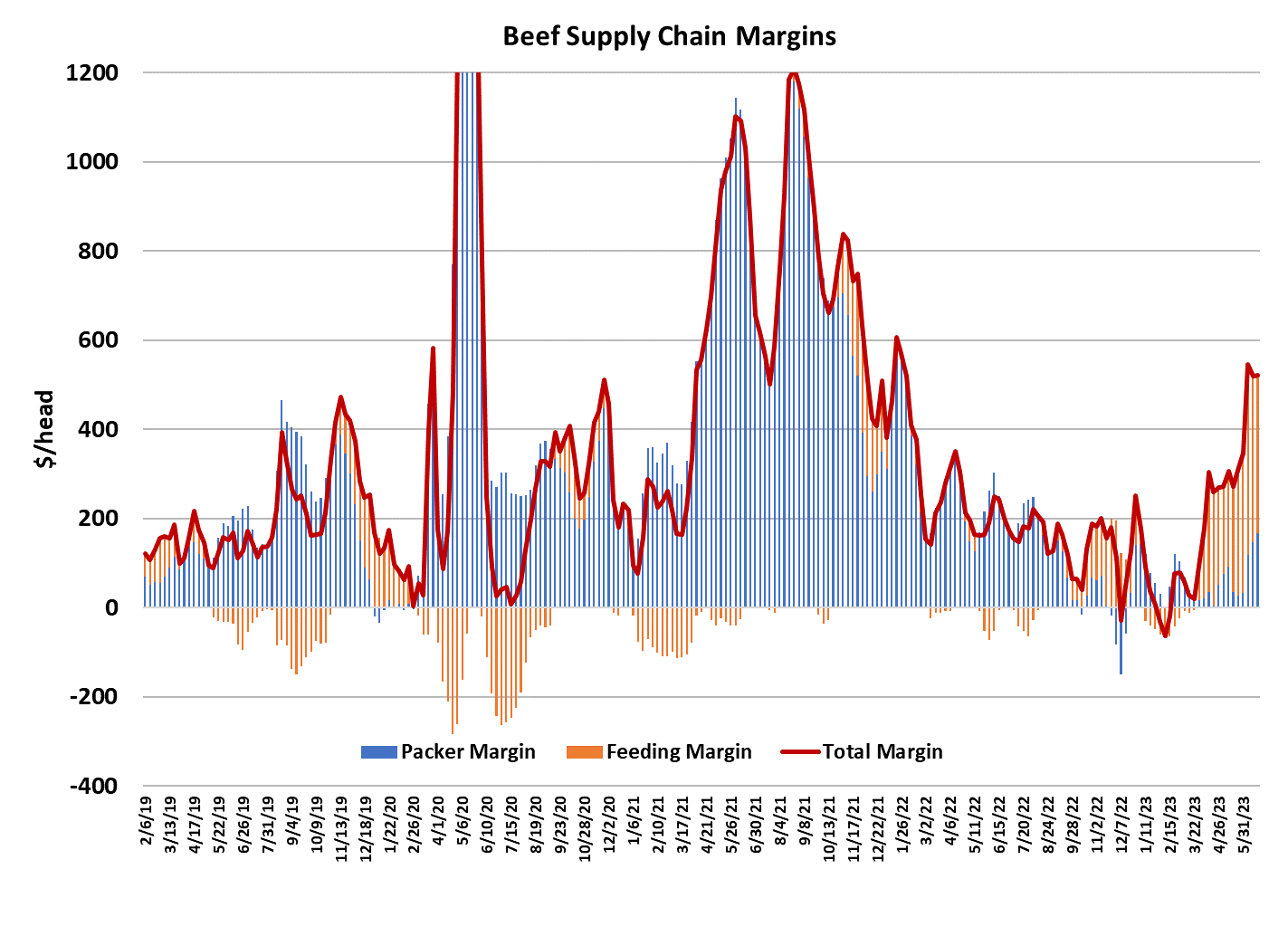

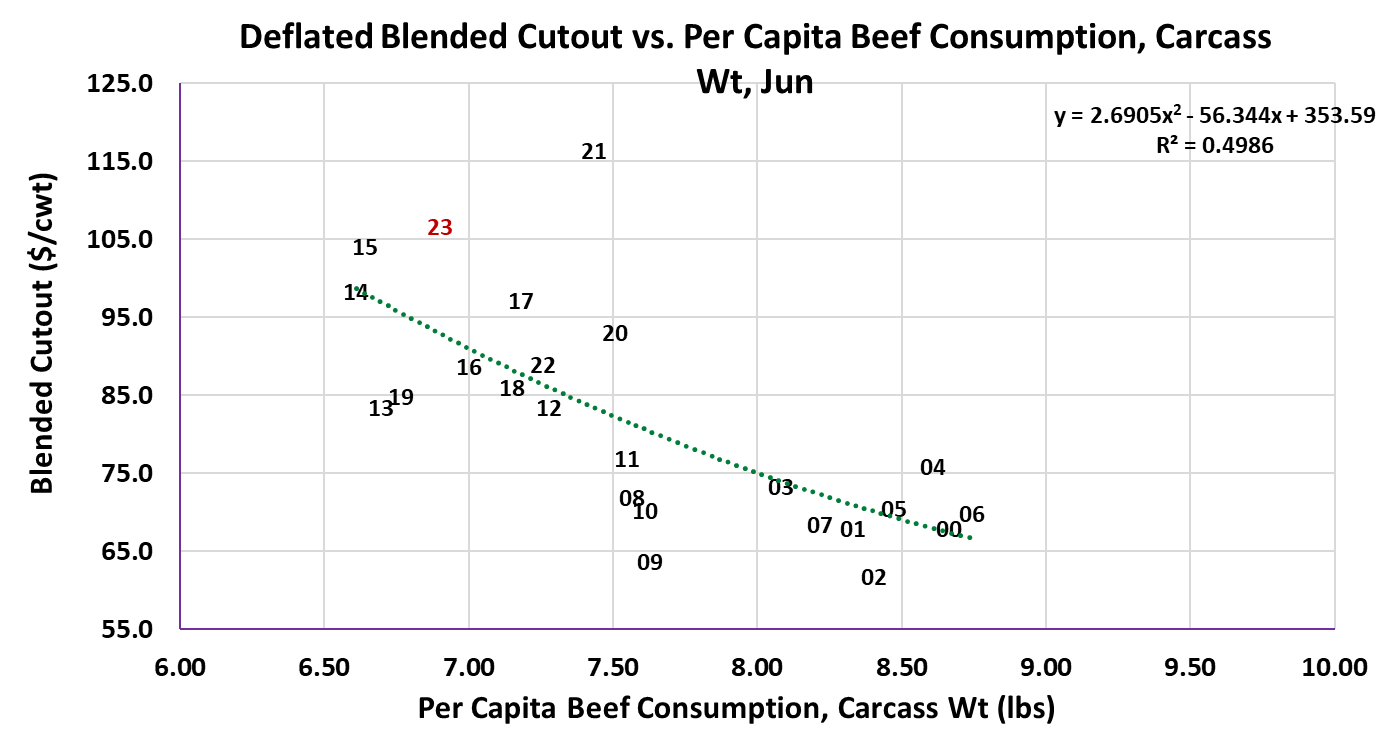

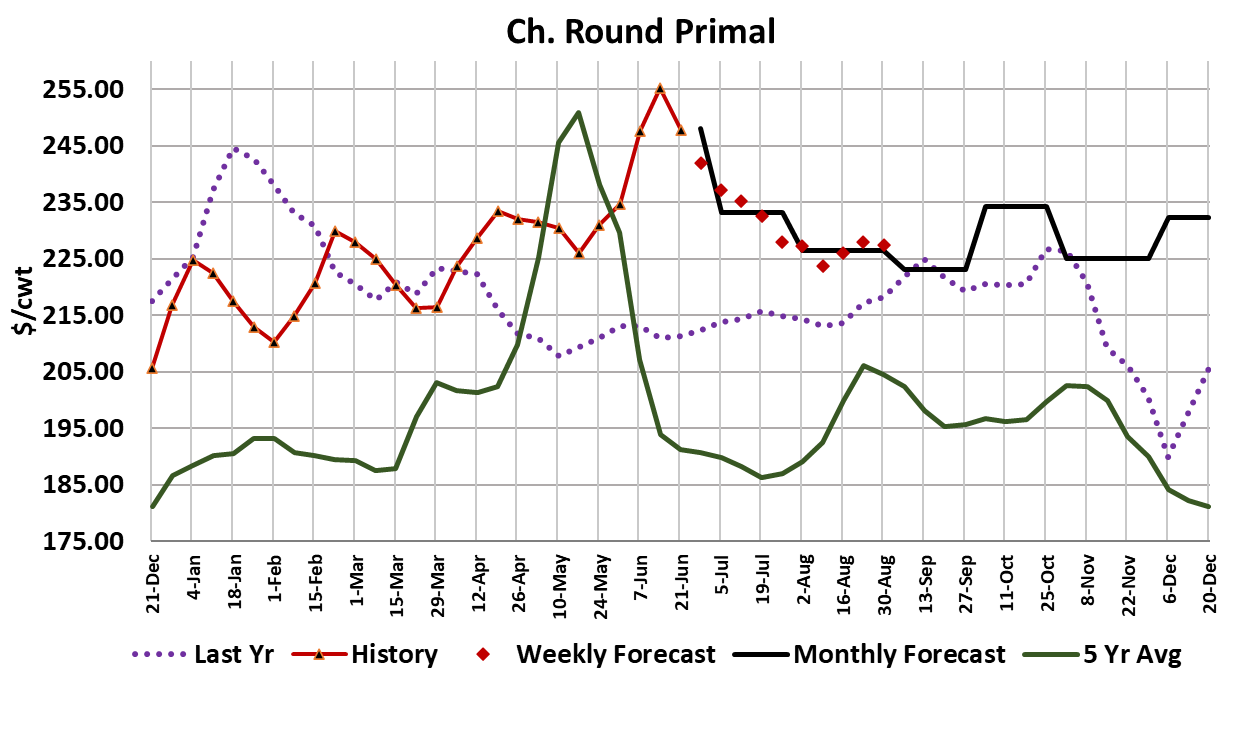

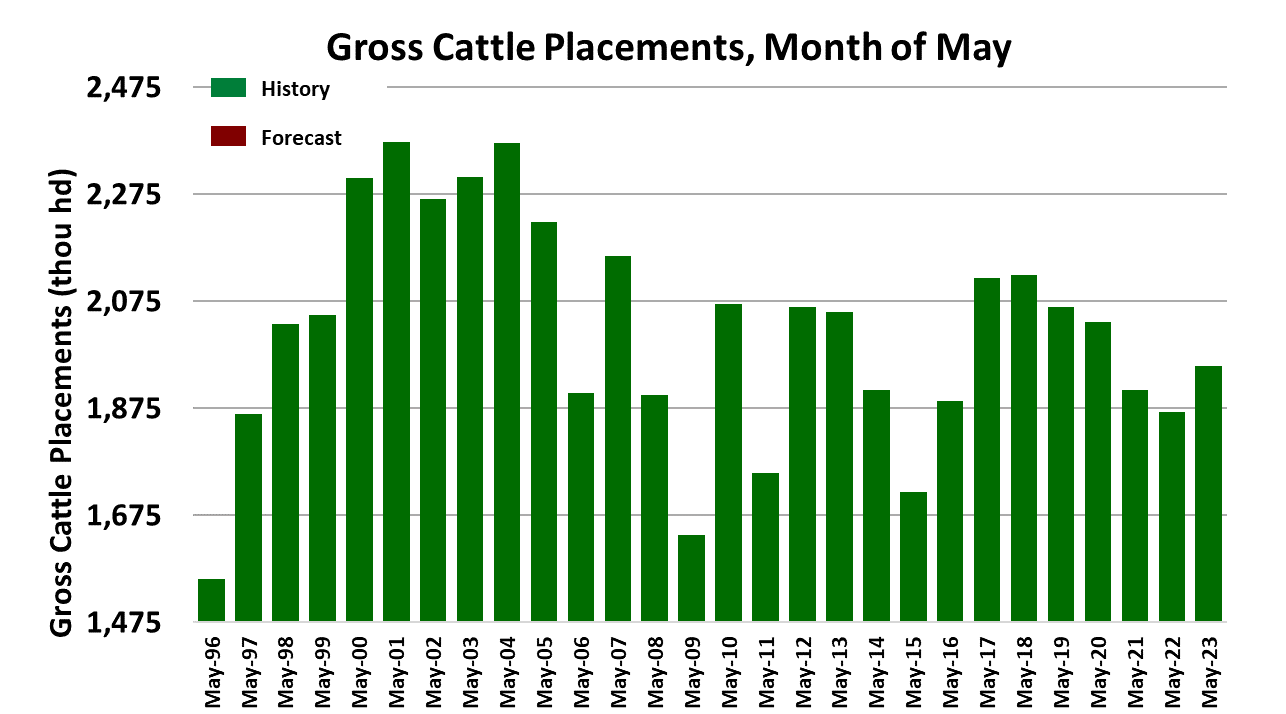

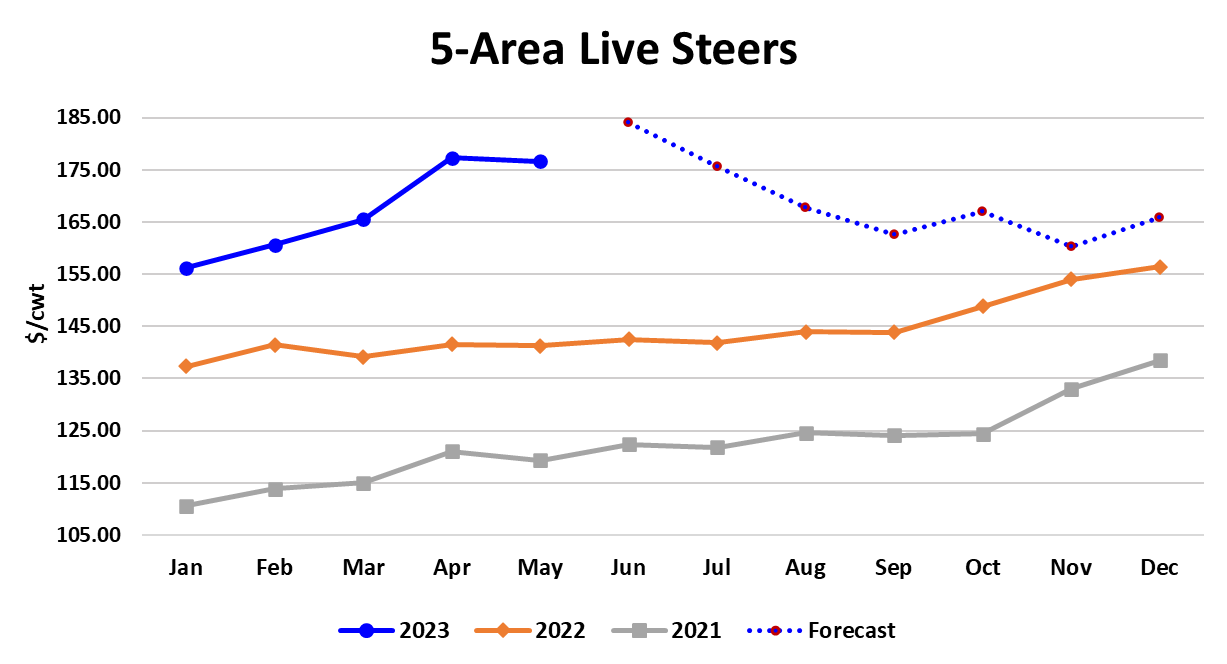

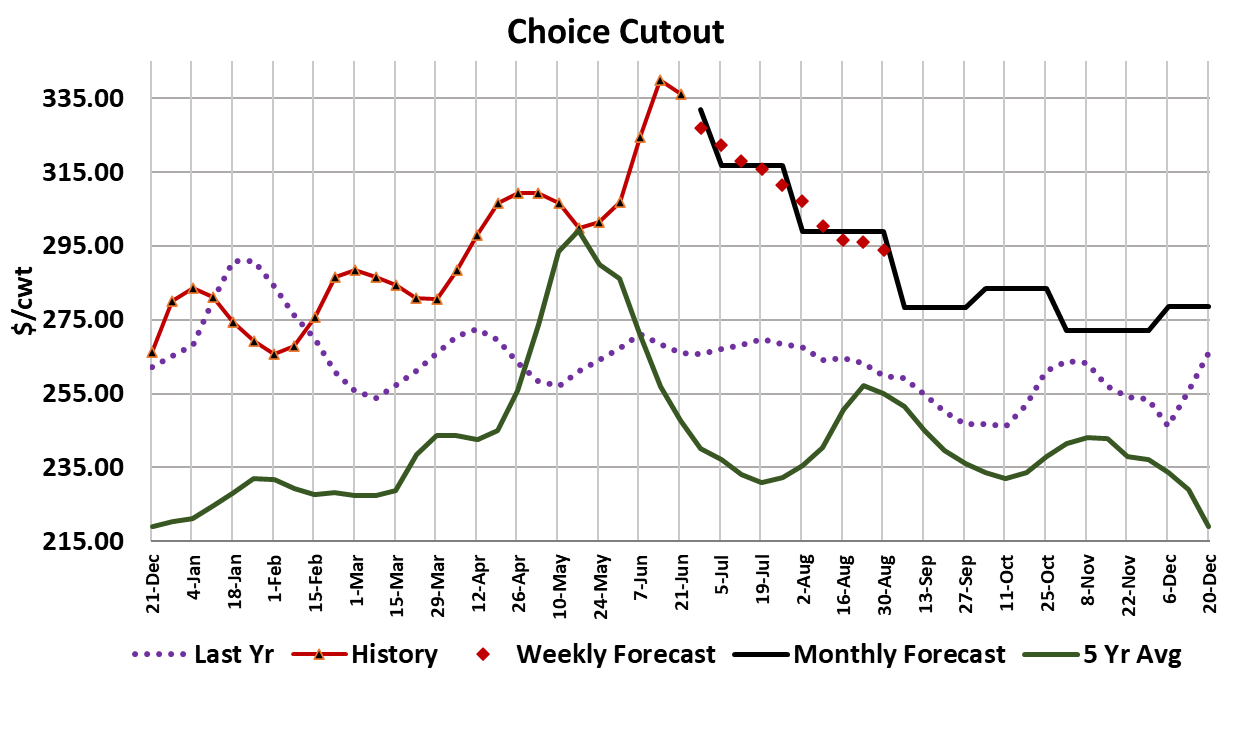

Cattle feeders were pretty quick to hit the bid this week, with sizable volume trading on Tuesday at $180/cwt. in the Southern Plains. Trade in the North followed on Wed/Thurs in the $183-184 range. Looking at average price levels, this week’s cash was $182.65, down about $2.30/cwt. from the prior week. That was probably not as bad as some in the feeding industry were fearing. Things were also better than expected on the beef side, with the Choice cutout down only $3.97/cwt and the Select cutout down $4.56/cwt on a weekly average basis. That left packers in good financial shape and I have this week’s margin at +$165/head—their best weekly margin since last July. I expect that cattle feeders will do the margin calculation also and realize that they are inflating packer profitability at the expense of their own margins. This week, cattle feeding margins dropped about $20/head to $350. Needless to say, with both margins still looking very strong, the combined margin is holding at very high levels. That is a sign that beef demand remains good, but consumers have yet to face the latest round of price increases. This week it was the end cuts and the loins that helped the cutouts lower. I was afraid that packers would have a hard time keeping chuck and round prices elevated after the initial run-up and that seems to be the case. The surprise in the beef area is the ribs, with that primal posting price increases in recent days. Funny, the ribs underperformed in the period leading up to Memorial Day and Father’s Day, and now once those are done, it looks like the ribs are going to overperform. It just goes to show that we can’t always count on seasonal tendencies. That has been especially true since the pandemic began. The attached scatter diagrams shows how well beef demand has performed in June, second only to the lights-out performance in 2021. If demand stays on its current trajectory, we will likely see both cattle and beef prices exceed my forecasts. I have had beef demand declining in the forecast for the past few weeks and have found myself having to raise the forecasts week after week as demand was better than expected. I still see the cutout working lower as we get deeper into summer, but perhaps the rate of decline won’t be as speedy as originally envisioned. Much will depend on consumer’s willingness to spend over the next few months. We learned this week that the start date for resuming repayment on student loans has been pushed back to October from August, so that buys a little bit of breathing room. Also, there has been more talk about US economy potentially avoiding a recession later this year and inflation is slowly receding. So, I’d have to say that the macro picture does look a little bit better for the second half of 2023. Whether or not that will be enough to hold demand at the levels we are seeing right now is an open question. My guess is that demand will fade some anyway, because it looks like wage gains are not keeping pace with inflation, thus consumers’ spending power is eroding. On the supply side, this week’s fed kill was close to 511k, up 17k from the week before. That might be just a tad more than what the available supply can handle, but not much. The flow model has been telling us for some time that cattle availability should improve moving through June and into July. Next week, I expect the fed kill to reach 520k, as packers will probably do a strong Saturday kill in order to prep for losing the following Tuesday’s kill to the July 4 holiday. However packers will be buying for a short kill, so they might not need to be very aggressive in the spot market for cattle. They will also soon have access to their formula cattle for July. That said, I get the feeling that feedyards are still more current that most people think. Steer weights were down five pounds in this week’s FI data and the will likely be steady or lower next week. The DTDS weights have been dropping like a rock also. Everyone, including cattle feeders, expected cash cattle prices to decline after they rocketed up to $189 a couple of weeks ago. In the two weeks since then, cattle prices have averaged $7/cwt lower, so expectations have been met. Maybe cattle feeders will look at those strong packer margins and question if there is any need for cattle to continue lower. I’m forecasting the cash cattle market another $1-2 lower next week, but I wouldn’t rule out steady. Today’s Cattle on Feed report showed May placements up 4.6% YOY, which was 2.6% greater than the consensus forecast. That might put some pressure on the futures Monday morning and if futures stay lower throughout the day, that could be all it takes to set the stage for a lower cash trade later in the week. Often, the early-week futures trade will set the tone for cash cattle trading later in the week. However, the COF report is probably not as bearish as it seems because we were comparing against relatively small placements in May, 2021. So futures traders may shake it off quickly and return to focusing on the near-term fundamentals, which don’t look overly bearish. The weekly export data was better than expected on Thursday, but that might just be a one-week anomaly, so I don’t want to read too much into it. Let’s see if exports can hold strong next week. In all, the market seems to be in pretty good balance right now. Beef prices should continue to work slowly lower as kills expand into July. Cattle prices should follow beef lower, but there is reasonable chance that cattle prices could bump higher periodically if feedyards maintain currentness.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}