Beef Wrap June 16

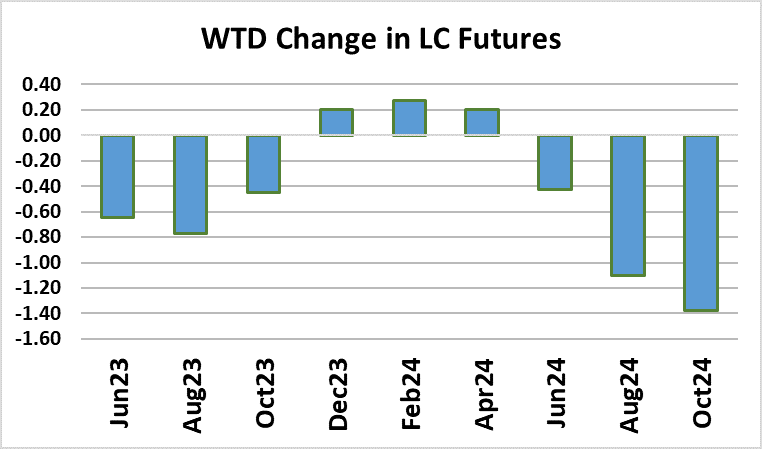

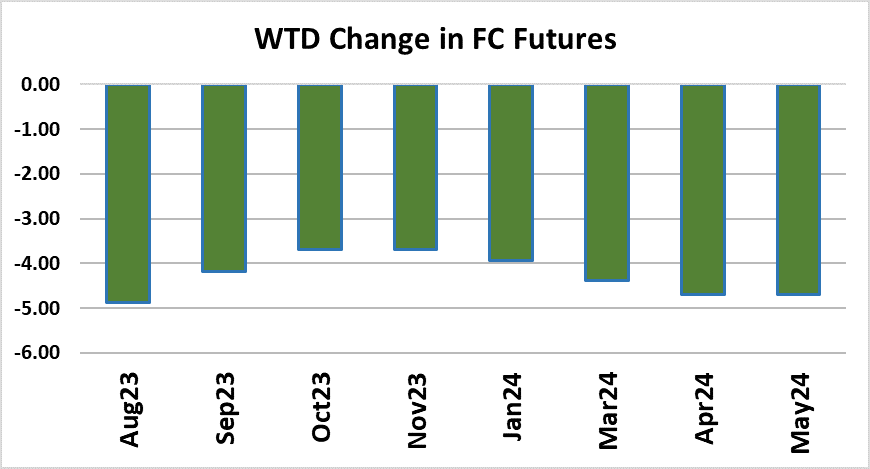

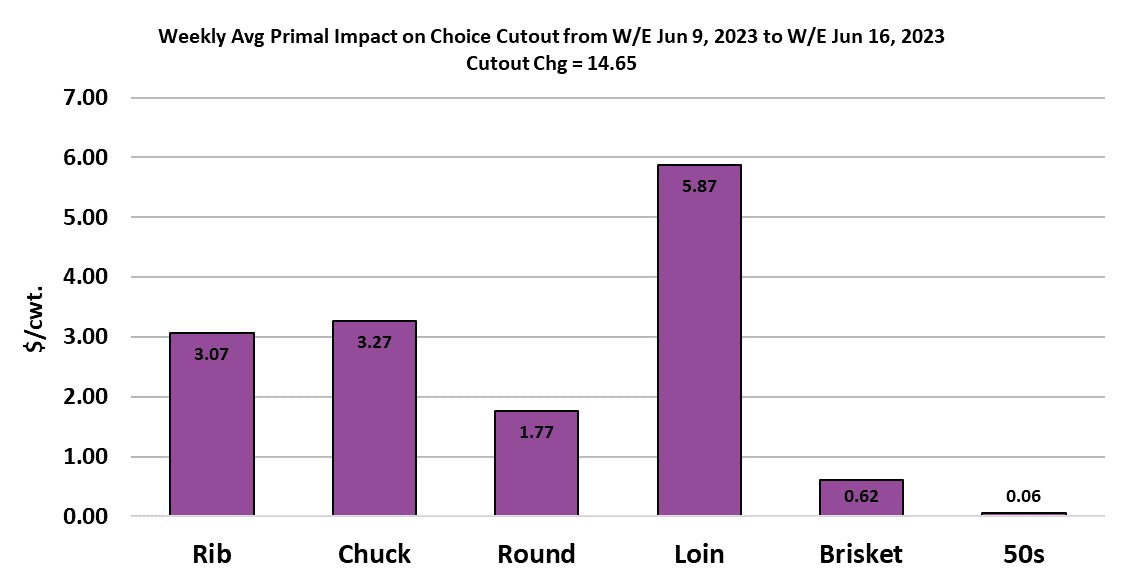

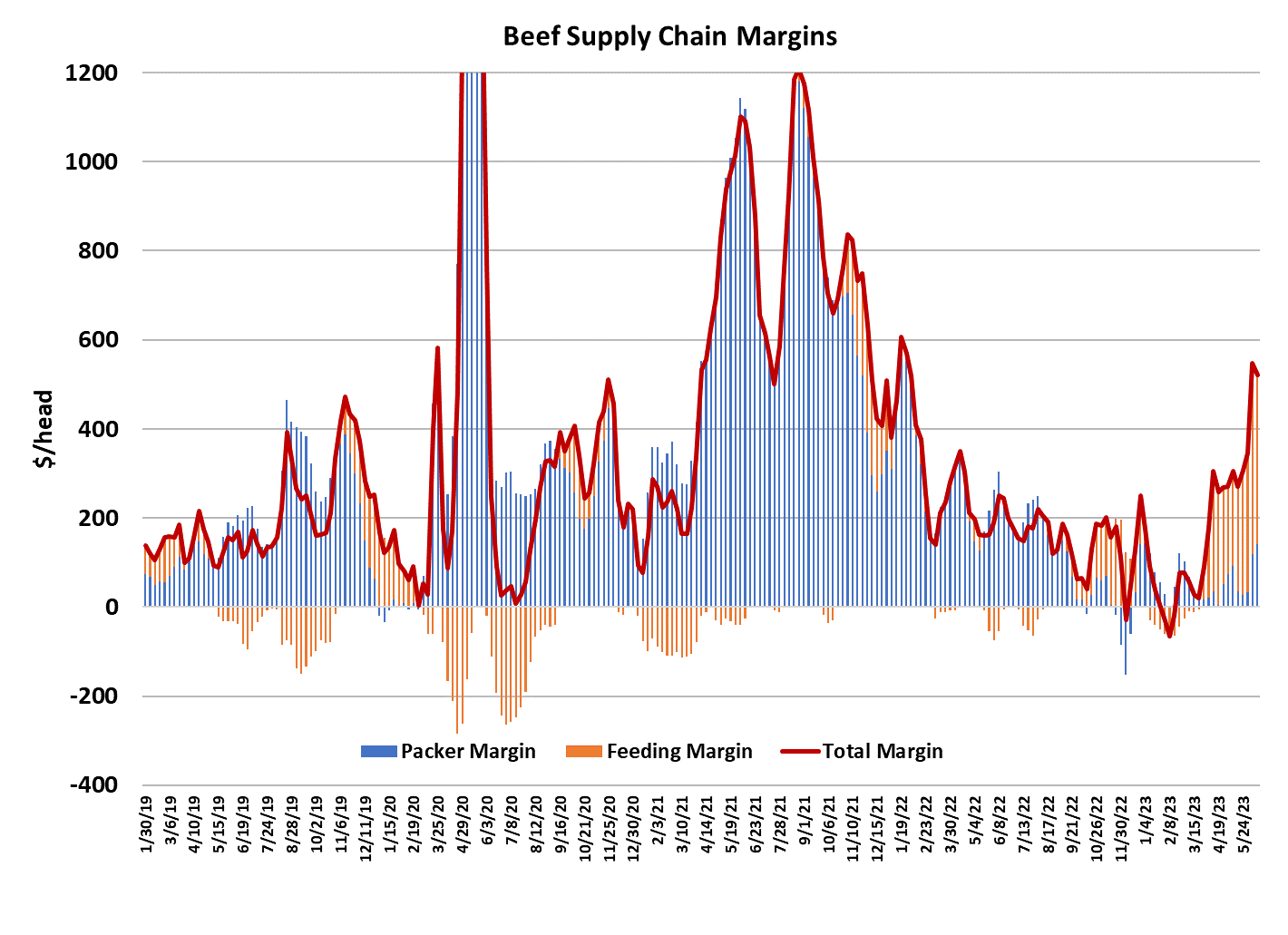

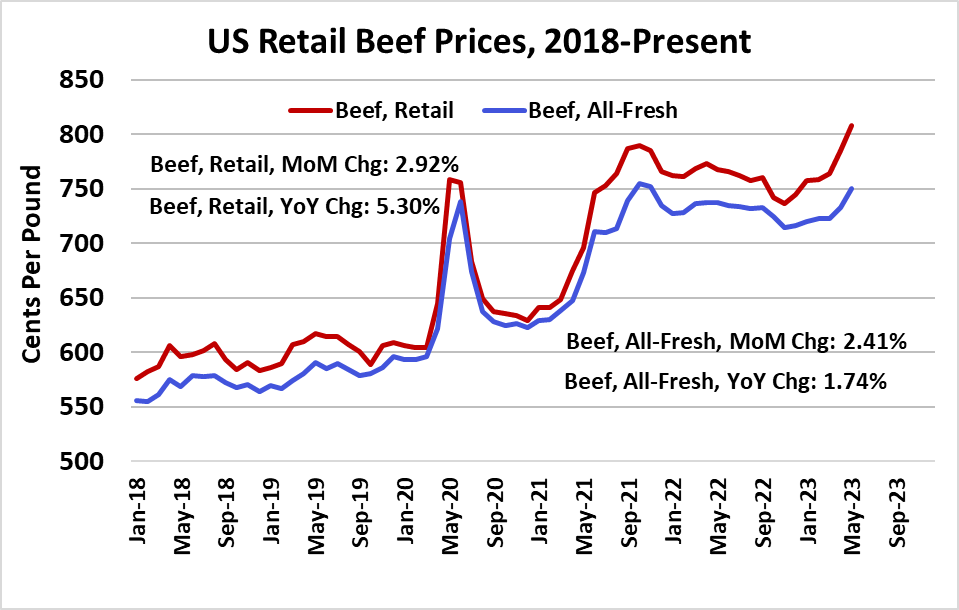

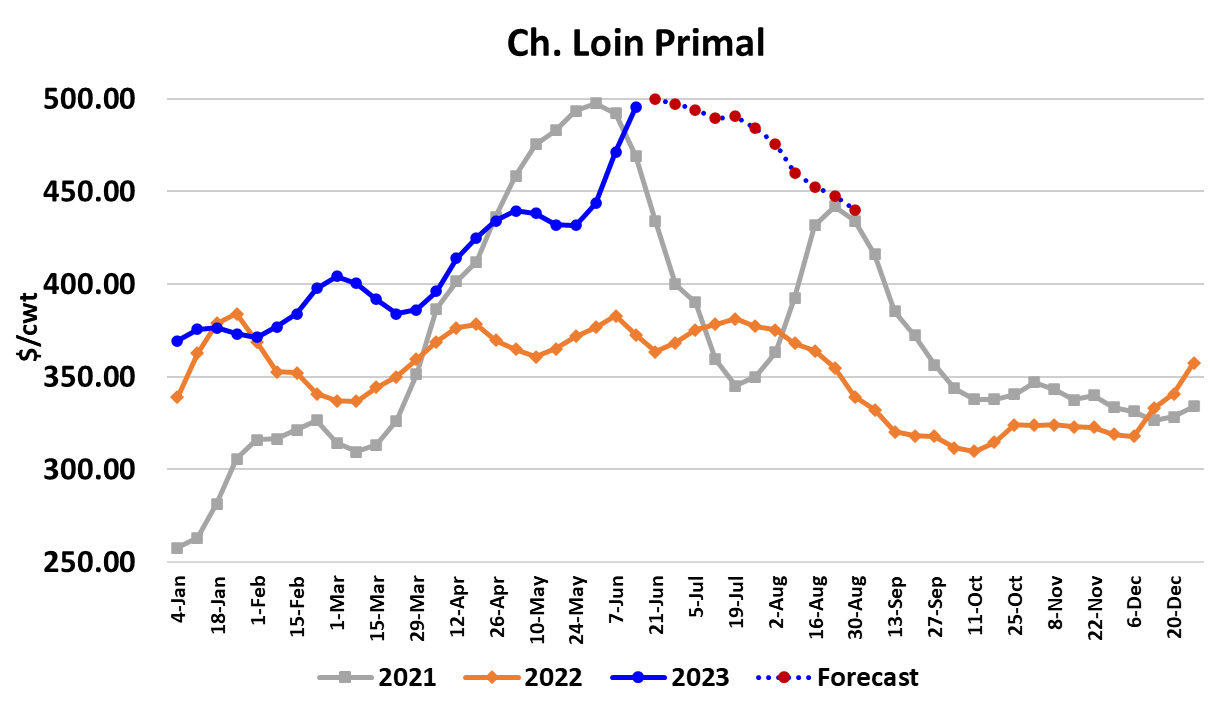

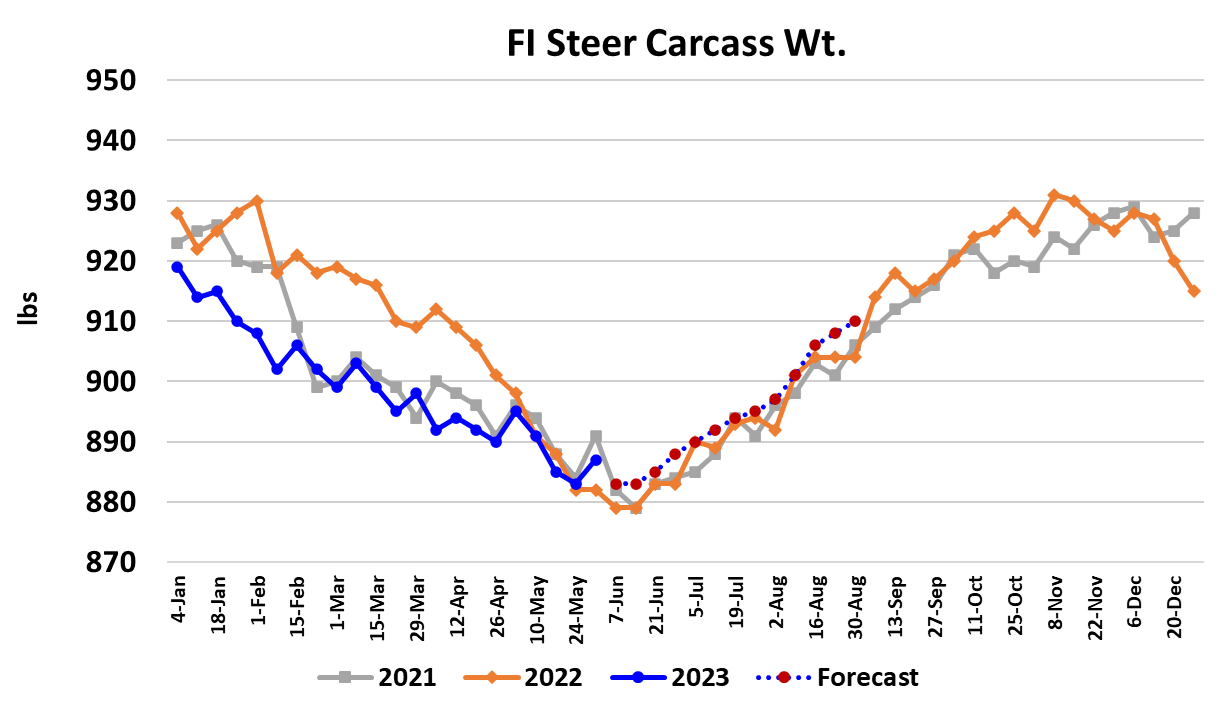

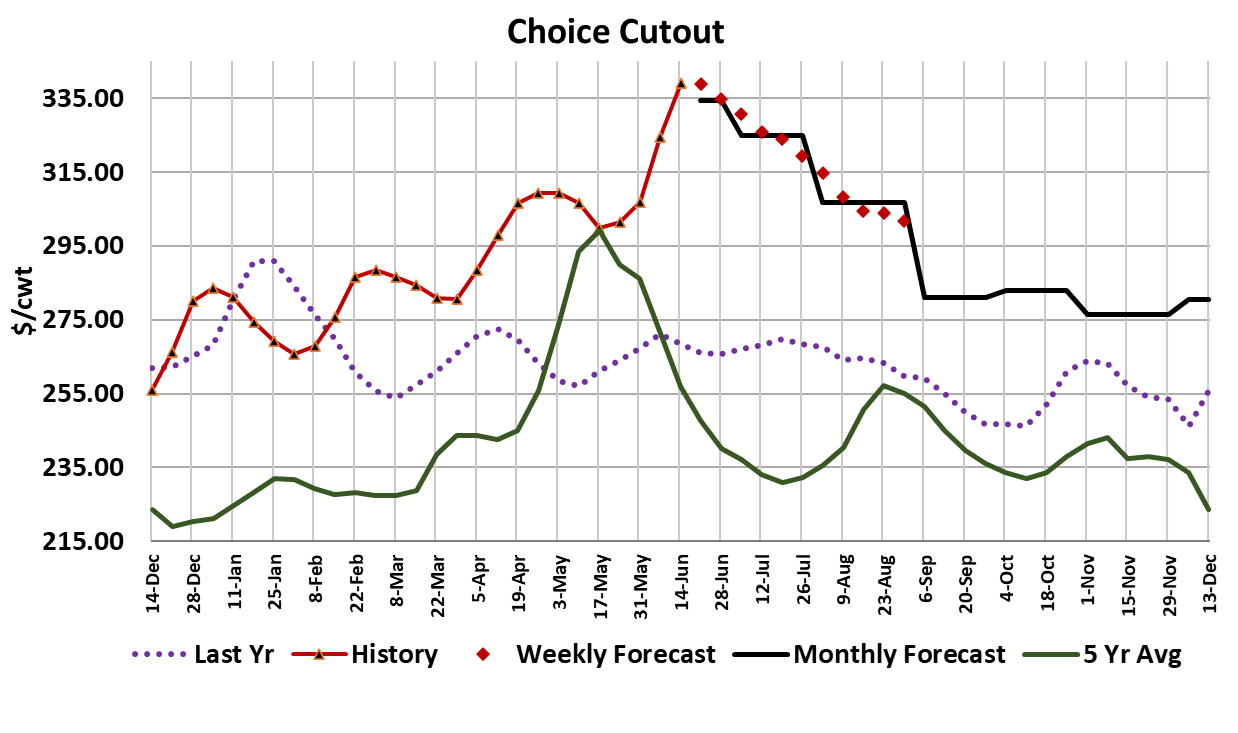

The beef market remained red hot this week, but the cattle market cooled a bit. Through Thursday, the Choice cutout had gained $14.65/cwt on a weekly average basis and the Select cutout had added $8.13/cwt. Near-term beef demand has been strong as buyers scrambled in response to recent price increases, but that short-term improvement in demand is likely to start fading soon. In the cattle market, packers got some help from the futures board, which sold off hard early in the week and thus set the tone for a lower cash trade. As of Thursday, live trade in the Northern areas was being reported in the $185-186 range, which was down $4-5 from last week’s top near $190/cwt. Cattle feeders in the South have been more hesitant to accept lower money and there has been almost no trade in that region so far. Southern cattle feeders passed on $182 bids earlier in the week and my guess is that they will end up trading in the $183-185 range, steady to $2 lower than last week’s $185. It is easy enough for cattle feeders to see that the cutout has kept rising and that makes them think they should get higher prices for their cattle, rather than lower prices. I don’t think that cattle feeders in either region are being pressured by large cattle supplies just yet, particularly after packers bought big volumes last week, that should have left feedyard pens somewhat bare. Feeders know that soon packers will have burned through their inventory and will need to be back in the spot market. It seems like feeders in the Southern areas are content to let that happen. A little dip in cattle prices after such a meteoric rise in the past few weeks wouldn’t be all that surprising, but if it is happening because of the futures and not because of too many cattle physically in the yards, then the softer pricing may not stick around for long. Time will tell, but our flow model does point to increasing supplies of fed cattle as we move deeper into summer. I am projecting this week’s fed kill to come in around 495k, which would be about 15k larger than last week and pretty close to what available supplies should support. Packer margins are really good right now, so it wouldn’t be too surprising to see them increase the kill in the next couple of weeks in an attempt to capitalize on that. I project this week’s margin close to $140/head and if packers get cattle bought cheaper this week as expected, then next week’s margin could be close to $170/head. Needless to say, packers are not all that upset about the way the market has played out recently. It shocked a lot of observers that cash cattle prices rose almost $15/cwt in three weeks, but packers are loving it because they have been able to push beef prices upward even faster than the gains in cattle pricing. USDA reported federally inspected (FI) carcass weights for steers up 4 pounds, but that data was for the week that included Memorial Day, so some increase is normal. I’d look for weights to tick a little lower next week, but after that, weights should start to slowly work higher in normal seasonal fashion. That works in beef buyer’s favor eventually, but it takes a while for the impact of heavier carcass weights to materialize as lower beef prices in the marketplace. In the two weeks around Memorial Day, beef production averaged about 485 million pounds per week, down from about 520 million pounds per week in the middle of May. That goes a long way to explaining why packers seem to have had little trouble pushing beef prices higher. However, by the end of June, weekly beef production could easily be back in the 520-525k range and thus it makes sense that beef buyers will have more leverage and beef pricing should move lower. Thursday afternoon, the Choice beef cutout stood at a little over $342/cwt and while I don’t see a lot of upside from here, I do think that the move lower will be gradual and am not forecasting the Choice cutout to move back below the $300 mark until September. From a demand perspective, I’m a bit wary of August, when millions of Americans will have to restart their student loan payments and that could be a negative for protein demand across the board. Further, beef demand always seems to sag somewhat after Independence Day and retailers will probably be taking a hard look at pork and poultry to drive features in July and August, so there is reason to expect beef demand to cool as we move deeper into summer. This week, all primals were higher through Thursday, but the loin was the star performer. Fat trim is holding in the low $190s, but as the kill picks up over the next few weeks, softer pricing is forecast there. USDA recently released their retail prices for May and one series climbed to an all-time record of $8.08/lb. It is very likely that we will see further increases in retail pricing when the June and July data are reported. Beef is quickly becoming a luxury good. Corn futures have been ripping higher lately as the forecast hasn’t been rainy enough to satisfy traders that the crop is going to get off to a good start. Cattle feeders probably should pay attention to that and adjust what they are willing to pay for feeder cattle accordingly. Cash feeder cattle prices have been on the rise and the FC Index is now near $228, only $6 below where the Aug FC futures settled this afternoon. That seems like an awfully narrow basis with so much time to go until Aug expires. Next week, packer will need to reload their cattle inventory and cattle feeders will be waiting for them. As a result, I wouldn’t look for the cattle market to lose a lot of ground beyond what it gives up this week. Beef cutouts should top and start to ease on better availability, but don’t expect prices to quickly deflate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}