Beef Wrap July 23

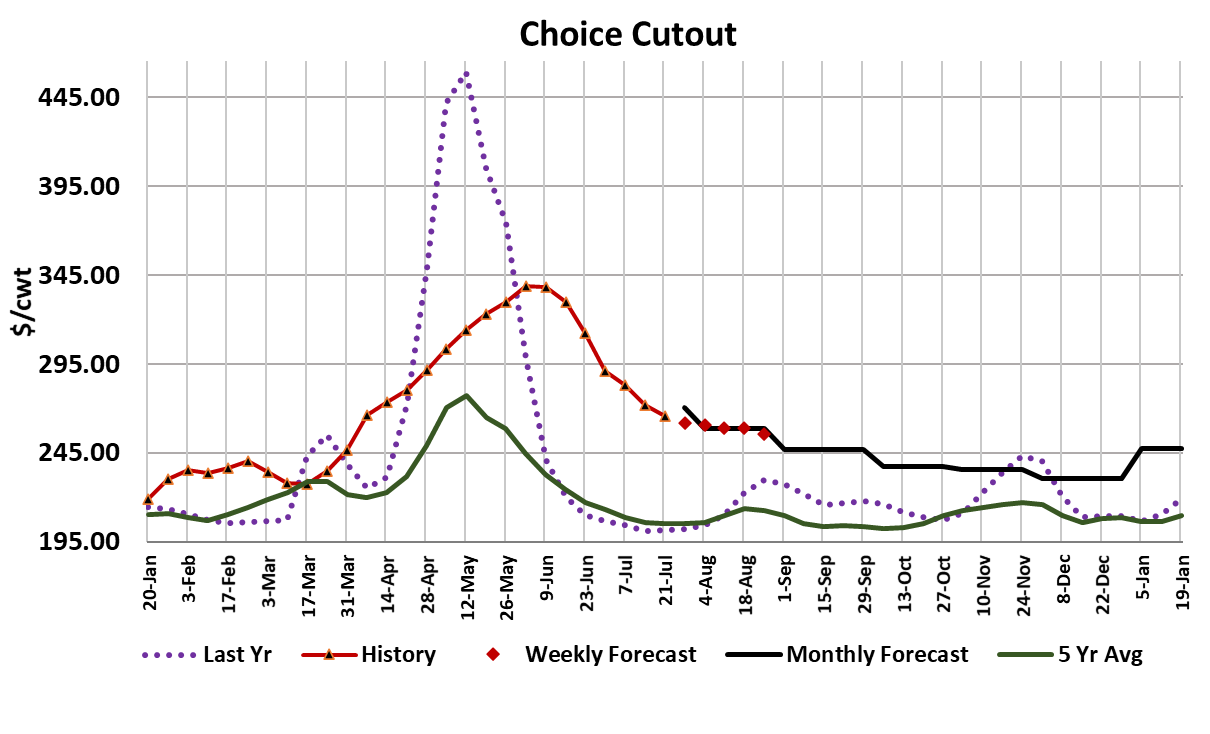

Cash cattle markets were mostly lower, with the average so far

this week at $120.21, down over $2.50 from last week’s

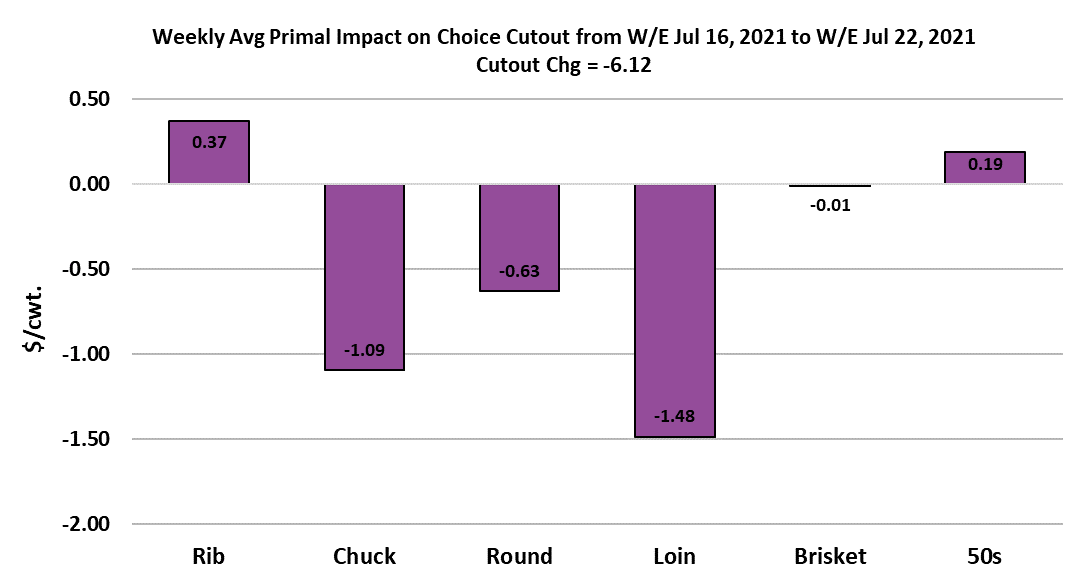

average. The cutouts also continued lower, with both down

about $6 on a weekly average basis. However, the cutouts did

manage to eek out small gains on Wednesday and Thursday,

which has some wondering whether or not the market is

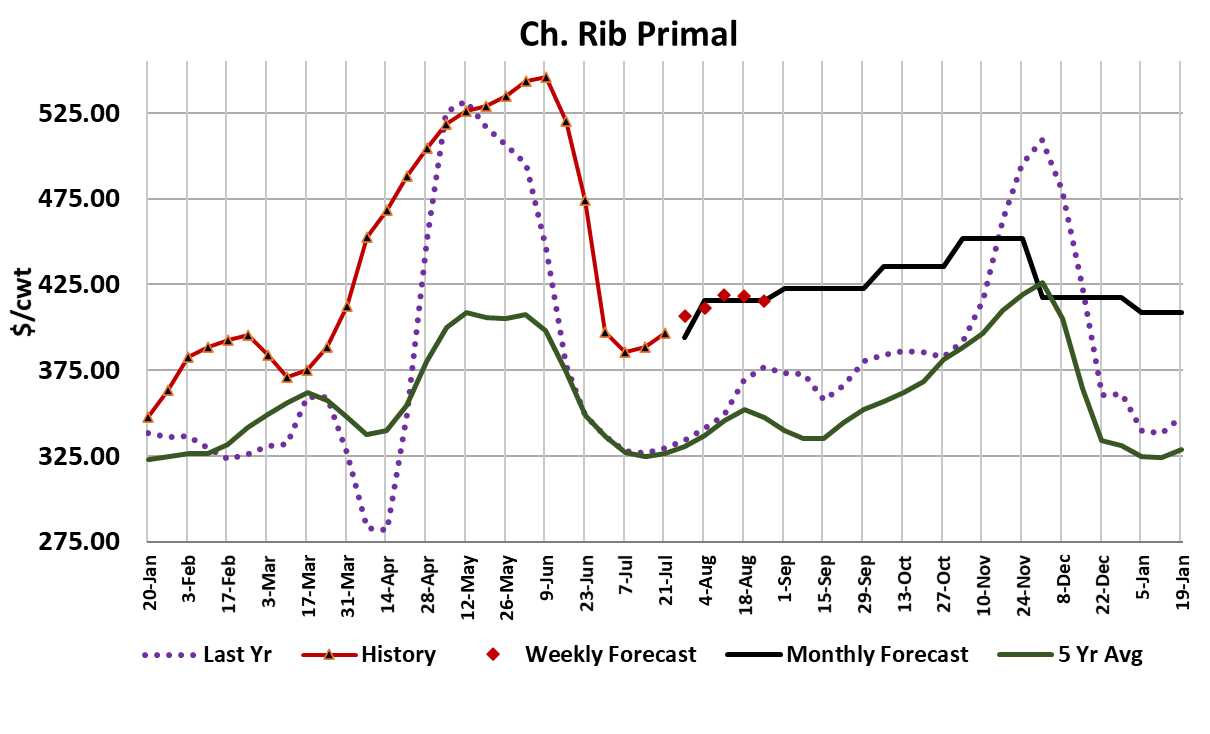

carving out a bottom and preparing to head higher. Ribs have

added value this week, along with the 50s, but the end meats

continued to be a drag on the cutouts. Retailers are likely in

the process of planning Labor Day features and beef middles

have to look pretty attractive after the prices they faced

heading into Memorial Day.

I see the ribs as having bottomed now and they should work

higher from now until November. Loins typically don’t follow

the same seasonal pattern—then trend lower right into the

holidays and those cuts remain on the defensive. End meats,

on the other hand, probably have further downside risk and that

will likely keep the cutout working lower, although at a much

slower pace than what we have seen in the past few weeks.

The 50s market added another $10 this week. It does seem

that all sources of fat are seeing elevated pricing right now, so

there could be a demand side component to the strength in the

50s, but I also believe that the supply of 50s is being limited by

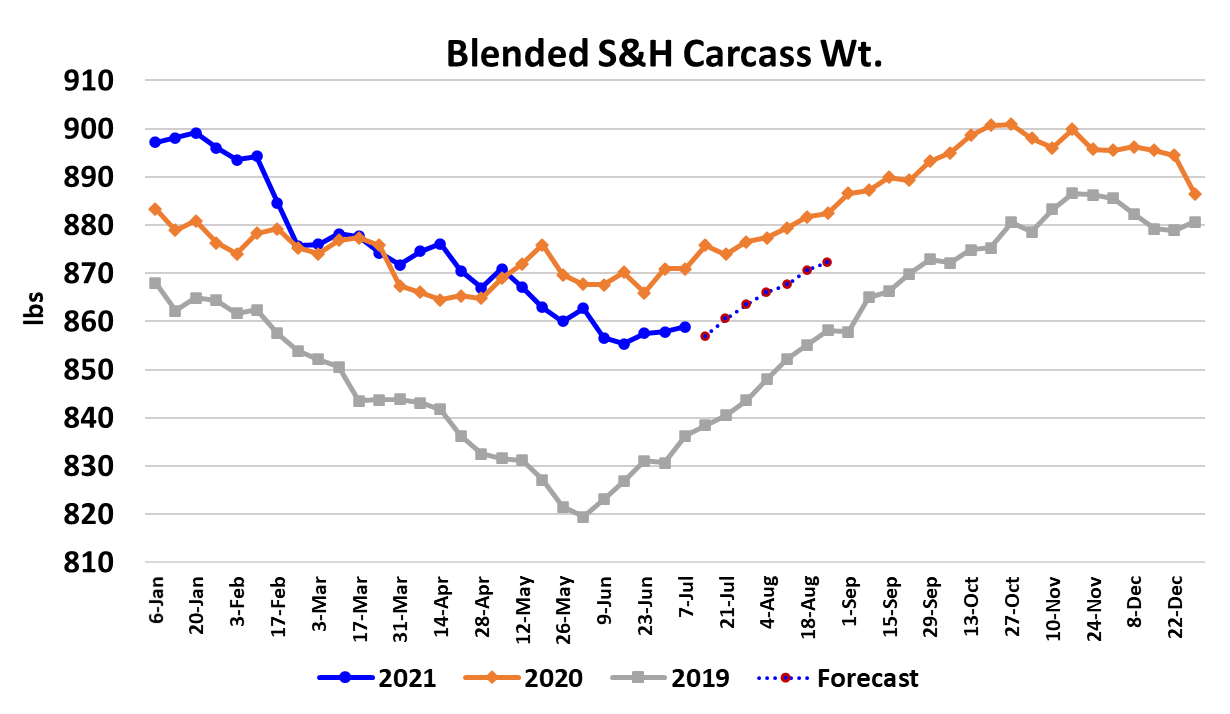

below-average kills and lighter carcass weights. Steer weights

were reported one pound higher this week, but should have

added more than that if they were on a normal seasonal track.

The DTDS plunged lower and is a reminder that carcass

weights are actually in pretty good shape this summer. So far,

that hasn’t translated into additional leverage for cattle feeders,

but it might help cash cattle prices before long.

The key will be keeping packers interested in putting together a

long string of decent-sized kills. Unfortunately, it is beginning

to look like this week’s fed kill may underperform expectations.

The current forecast is for 511k of fed cattle to be slaughtered

this week. That is well below the 525-530k that I think need to

be slaughtered in order to keep cattle from backlogging.

Packers may surprise me with a big Saturday kill, but at this

point I’m betting on something relatively close to last

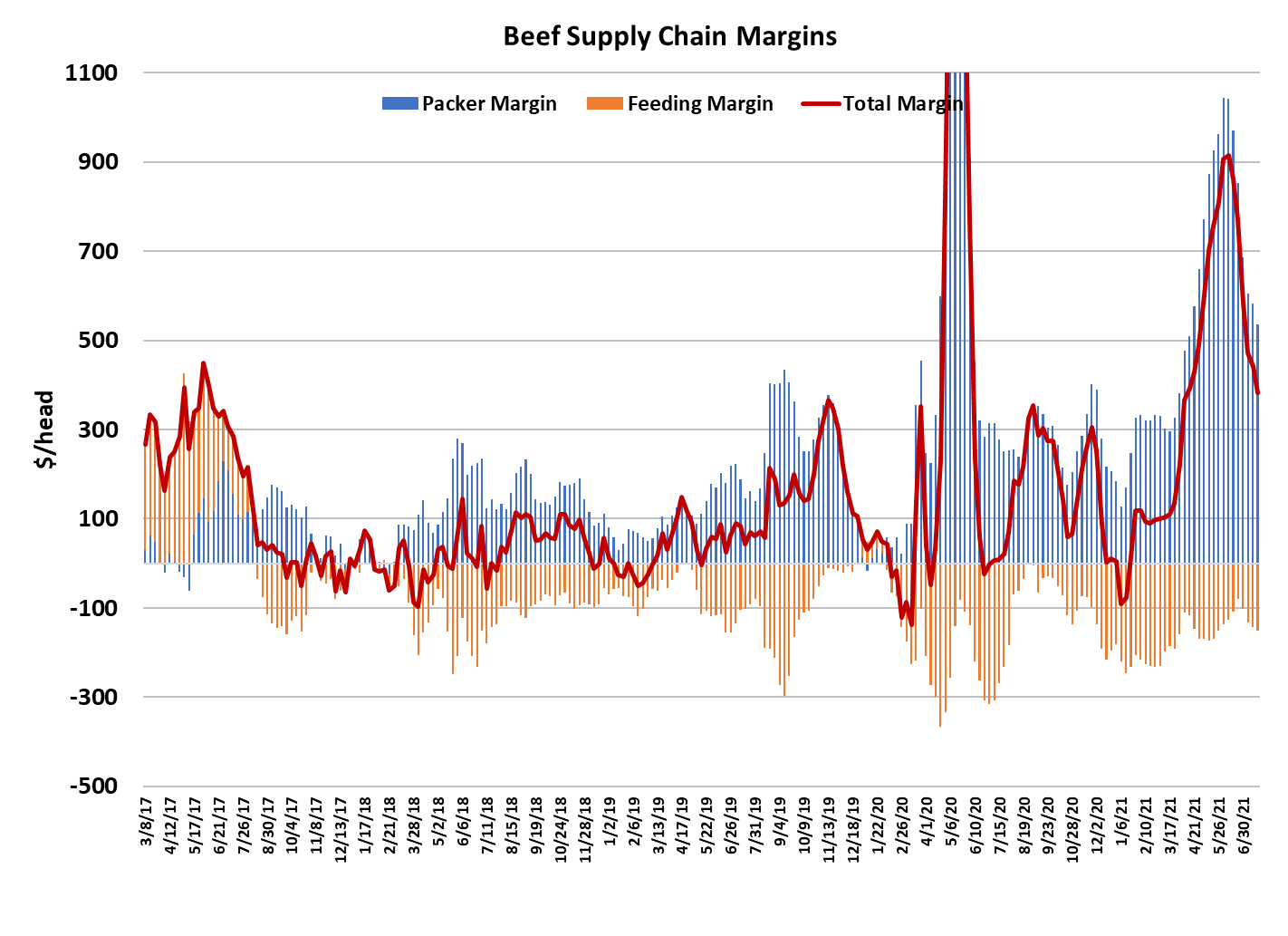

Saturday’s level around 45k. Packer margins moved lower

again this week, now at $535/head. They still have a long

way to go before they get back to normal and I’d expect the

rate of decline in margins to slow during August. One bright

spot in the beef complex this week was the weekly export

data, which showed nearly 40% improvement over last year at

this time. China continues to be a big buyer of US beef and we are also

seeing strong interest from Japan and Mexico. If exports

continue on this path, it will be worth several additional dollars

on the cutout this fall and winter and may help lift the cash

cattle market. Today’s cold storage report showed a 4.3%

drawdown in beef stocks during June and the inventory now

sits 7.4% below the five-year average. That is not nearly as

bad as the tight cold storage situation in pork, but it likely

means that the buyers will have to rely a little more on the

spot market this fall to meet their needs.

Next week, expect the cutouts to be lower again, but to a

lesser degree than in recent weeks as strength in the middles

helps to offset some of the weakness in end meats. Also

keep and eye on those 50s, because I can’t shake the feeling

that they are trying to tell us something.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}