Beef Wrap July 16

Cash cattle prices were a little higher this week, averaging

$122.56, up about $0.40 from last week’s average. We still have a

two-tiered market, with cattle in the North selling for a couple of

dollars more than those in the South. The beef market continued

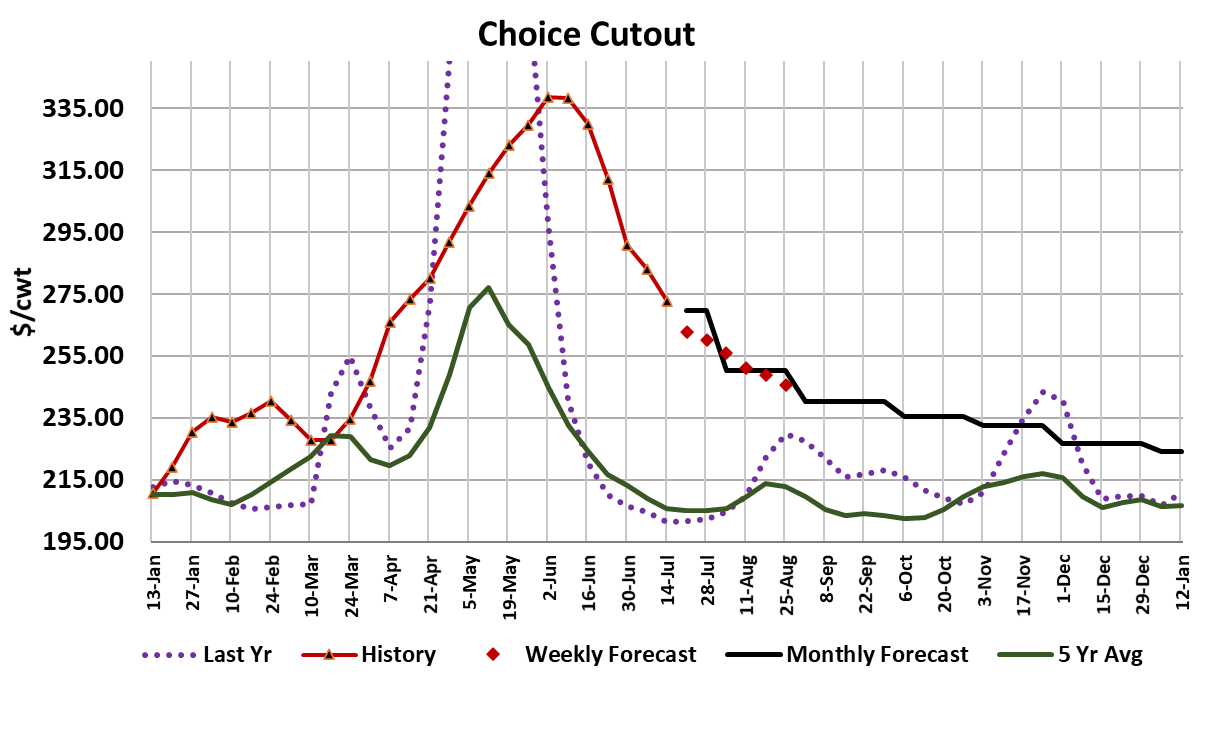

to move lower, with the Choice cutout dropping a little over $10

and the Select cutout off a little more than $5 on a weekly average

basis. In some respects, this week was just a repeat of what we’ve

seen over the past month or so—beef prices falling, cattle prices

steady and packer margins compressing after reaching absurd

levels this spring. I calculate margins this week at $467/head,

which is about $90/head lower than last week.

One has to wonder at what point packers will begin to feel the

need to pressure cattle prices. My guess is that won’t happen until

margins fall below $300. That is near the average margin packers

earned early in 2021 before the great beef price escalation began.

Of course, there is always the possibility that the cutouts don’t

move low enough to push margins below $300/head. My forecast

has one more week of substantial decline in the cutouts and then I

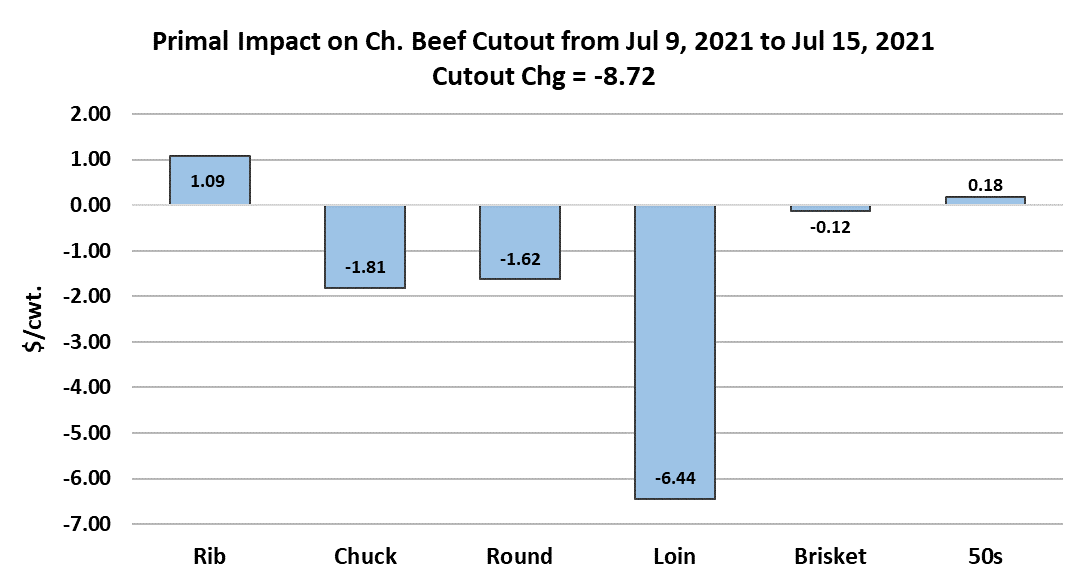

think that the rate of descent slows considerably. The chart below

indicates that it was primarily the loin primal that pushed the cutout

lower this week. Surprisingly, rib prices actually increased. I

continue to be concerned about the 50s, which finished today at

$129.11. While almost everything else has moved lower, 50s have

marched higher in recent weeks.

That makes me think that it is a supply issue, not demand, that is

moving the 50s higher. Carcass weights have been declining and

the DTDS is at -10. Further, early July saw restricted fed kills due

to the Independence Day holiday. So, those things could be

tightening up the 50s supply currently. However, last Saturday’s

kill was big and the daily kills so far this week have been solid, so I

would have expected some downward pressure on 50s, but

instead they moved higher. Maybe labor shortages in processing

plants are resulting in less trimming of cuts and therefore less fat

trim production. That seems reasonable, but we had labor issues

back in the spring and smaller kills than today, yet 50s traded in

the 70-90 cent range.

Sometimes escalating 50s prices precede a jump in cash cattle

prices, so that is important to be aware of. I am projecting this

week’s fed kill at 522k, which is a little smaller than what I gauge

as necessary to keep the cattle supply current. Steer carcass

weights were reported one pound higher today, so perhaps

weights have now bottomed. Next week, I expect carcass

weights to post a big gain because the data will reflect slaughter

during the week that contained the 4th of July. We continue to

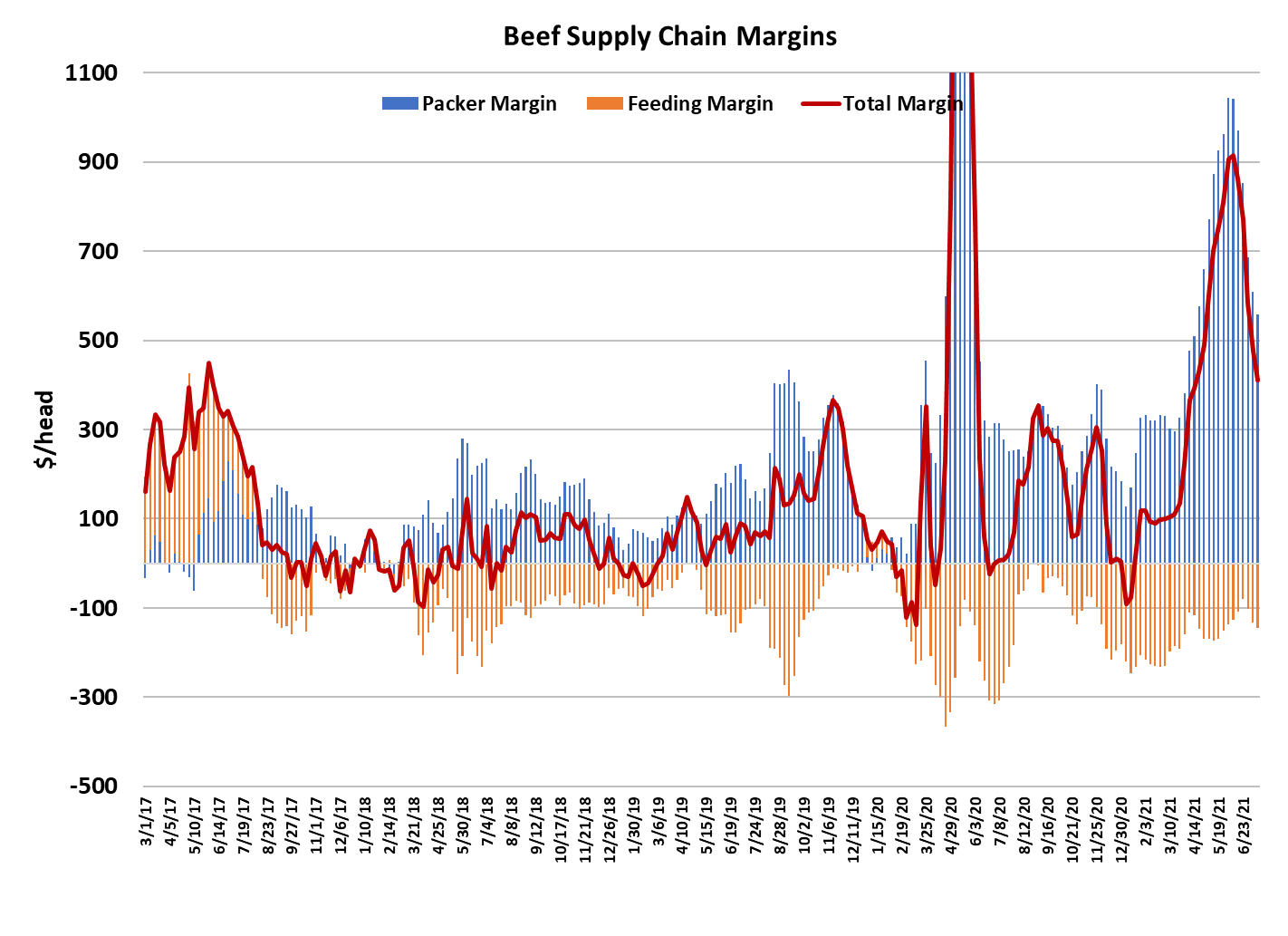

see domestic beef demand erode and that is illustrated by the

combined margin chart below. It still has a way to go before it

gets back to “normal” levels, however.

Retail beef prices for June were reported this week and they were

up 7.2% from May. At $7.46/lb, they are only slightly below the

levels posted last spring when COVID shut packing plants and

wholesale prices soared. Now that consumers are beginning to

see the true cost of beef in the grocery store, it will cause them to

purchase less and that is showing up as weaker domestic

demand. Retailers will need to lower retail prices in the coming

months in order to “buy back” some of the demand that is

currently being lost. Retailers are notoriously slow to lower retail

prices, so that important adjustment might take several months.

Export demand looked strong in the official May data that was

reported earlier this month, but the more timely weekly data has

shown some softening in exports. China is still taking a large

amount of US beef and that is probably the difference maker as

far as exports go.

Without this newfound business out of China, beef exports would

be looking rather dismal right now. The futures market seems to

be just marking time and waiting for something significant to

change in the cash markets. All of the remaining 2021 contracts

appear to be locked in a sideways trading pattern. Next week,

expect more of the same—declining beef prices and near steady

cattle prices. Also, watch the 50s for signs that the current strong

rally is nearing an end..

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}