Beef Wrap January 9

This week’s cash cattle trade averaged $157.78/cwt., almost steady

with last week. Cattle in the Southern regions traded at about a $1/

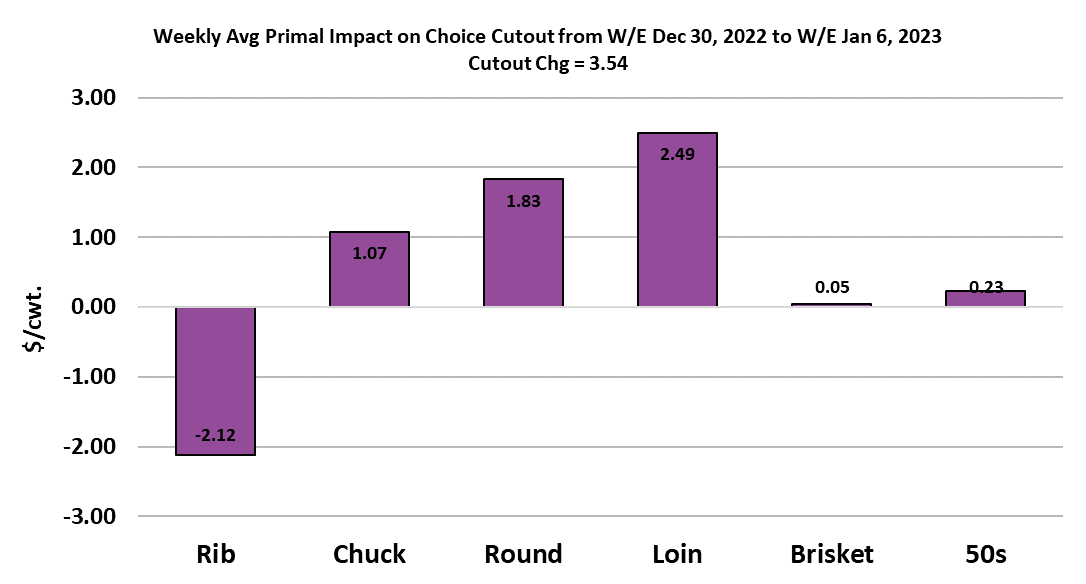

cwt. discount to those in the North. The cutout held up very well, with

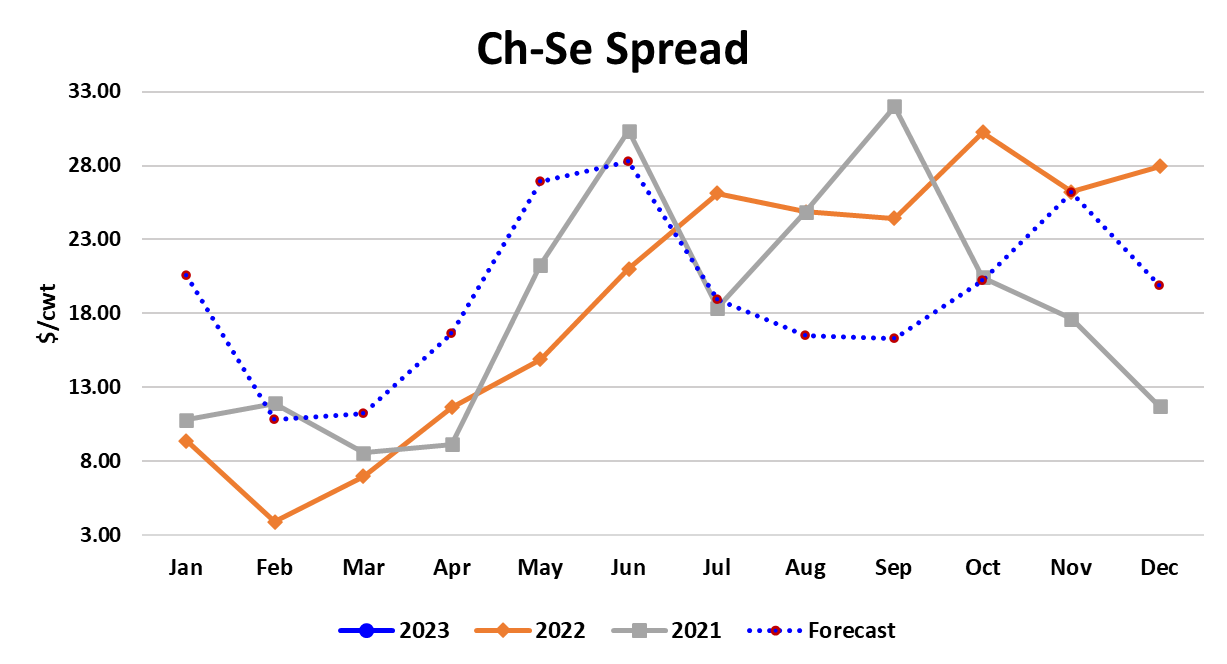

the Choice adding $3.54/cwt. and the Select gaining a whopping

$8.19/cwt. Packer margins stayed essentially flat with last week at

$77/head because even though the cutouts were rising, packers

were killing cattle they had paid up for the previous week. The most

impressive thing in the entire complex is the continued strength in

middle meat pricing. The rib primal only declined a little this week,

but the loin primal actually posted a gain. This is normally the time of

year when consumers and beef buyers are rapidly backing away

from pricey middles, but that hasn’t been the case so far. Perhaps

clearance on those items was better than expected over the holidays

and so that generated a lot of fill-in interest. If that is the case, then it

is just a matter of time before the ribs and loins move substantially

lower. The next major holiday for the middles is Valentine’s Day, but

we should see some erosion in demand before that arrives. End

meats are somewhat pricey too right now, but that is fairly common

for early January. The reduced kills of the last three weeks have

probably caused some short-term supply tightness that is supporting

prices. Packers will take care of any supply issues next week when

the kill returns to normal. For the past three weeks, the fed kill has

only averaged 426k. This week, which was missing the Monday kill,

came in at 429k and that needed a sizeable Saturday slaughter. I’m

looking for packers to push the fed kill into the 505-510k range next

week. It is hard to imagine that the cutouts won’t be pressured lower

under the weight of that production. Another thing that has limited

production recently is a sharp drop in carcass weights that started

with the polar vortex that hit cattle country during the week before

Christmas. USDA released the official weight data for that week on

Thursday and it showed steer weights down 7 pound from the prior

week. Normally in a holiday-shortened week (that Saturday was

Christmas Eve), we see carcass weights increase, so that big drop

was definitely an aberration that was likely due to the weather. Early

indicators are suggesting that when we get next week’s weight data,

it too will show a weight decline right in the middle of the holiday

period. However, from late December onward, the weather has been

much warmer across cattle country, so it is reasonable to expect that

weights will not continue lower at that rate of speed. In fact, the

weather forecast is projecting temperatures well above average in

the Midwest for the next couple of weeks. That should help dry out

feedyards and limit weight losses.

After next week, I’m looking for packers to slowly work the fed kill

lower and by the time February arrives it may only be around 490k

per week. That is based on past placement patterns that suggest

fewer market-ready animals during the Jan/Feb period than what we

saw in Q4. Of course, demand is usually weaker in the Jan/Feb

period as well, so smaller fed kills do not necessarily imply higher

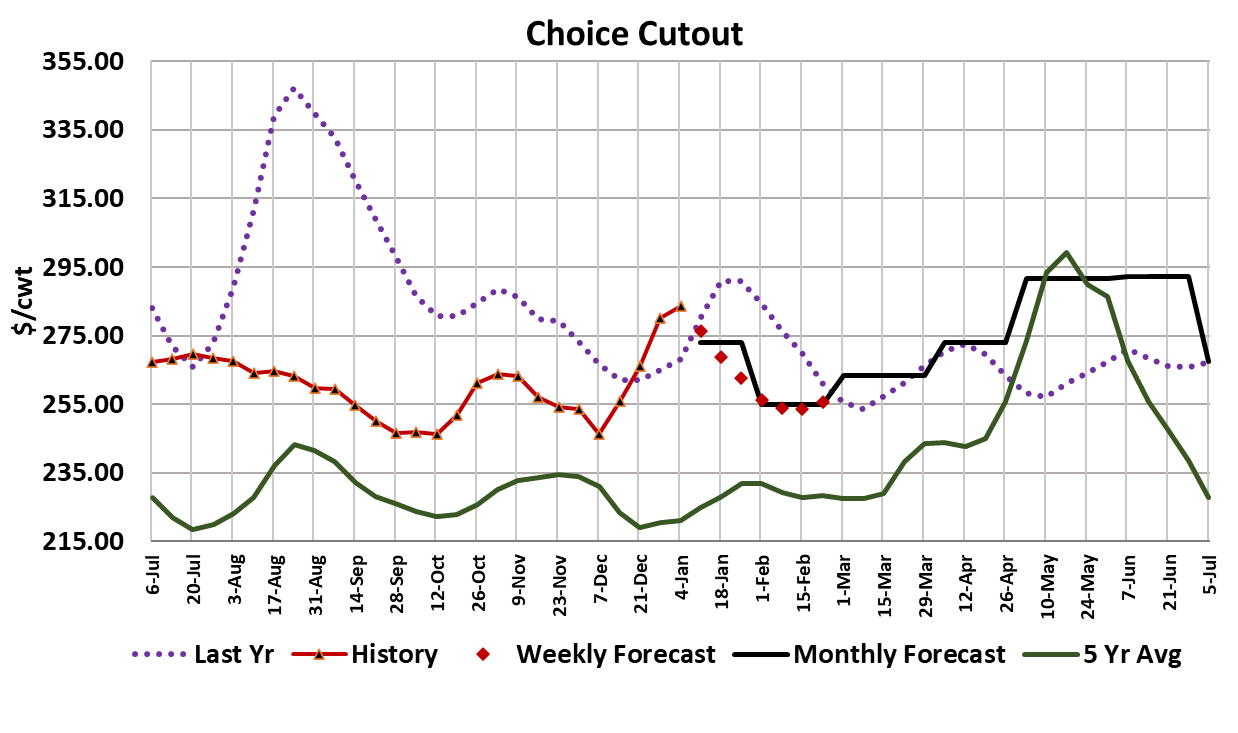

beef prices. In fact, beef prices look pretty high right now with the

Choice cutout over $280/cwt. Pork and chicken both offer better

values for retailers and they may lean in that direction for their Feb/

March feature activity. There is also a pretty good chance that

retailers will push their everyday pricing on beef higher in the next

few weeks in order to try and regain some of the margin that they

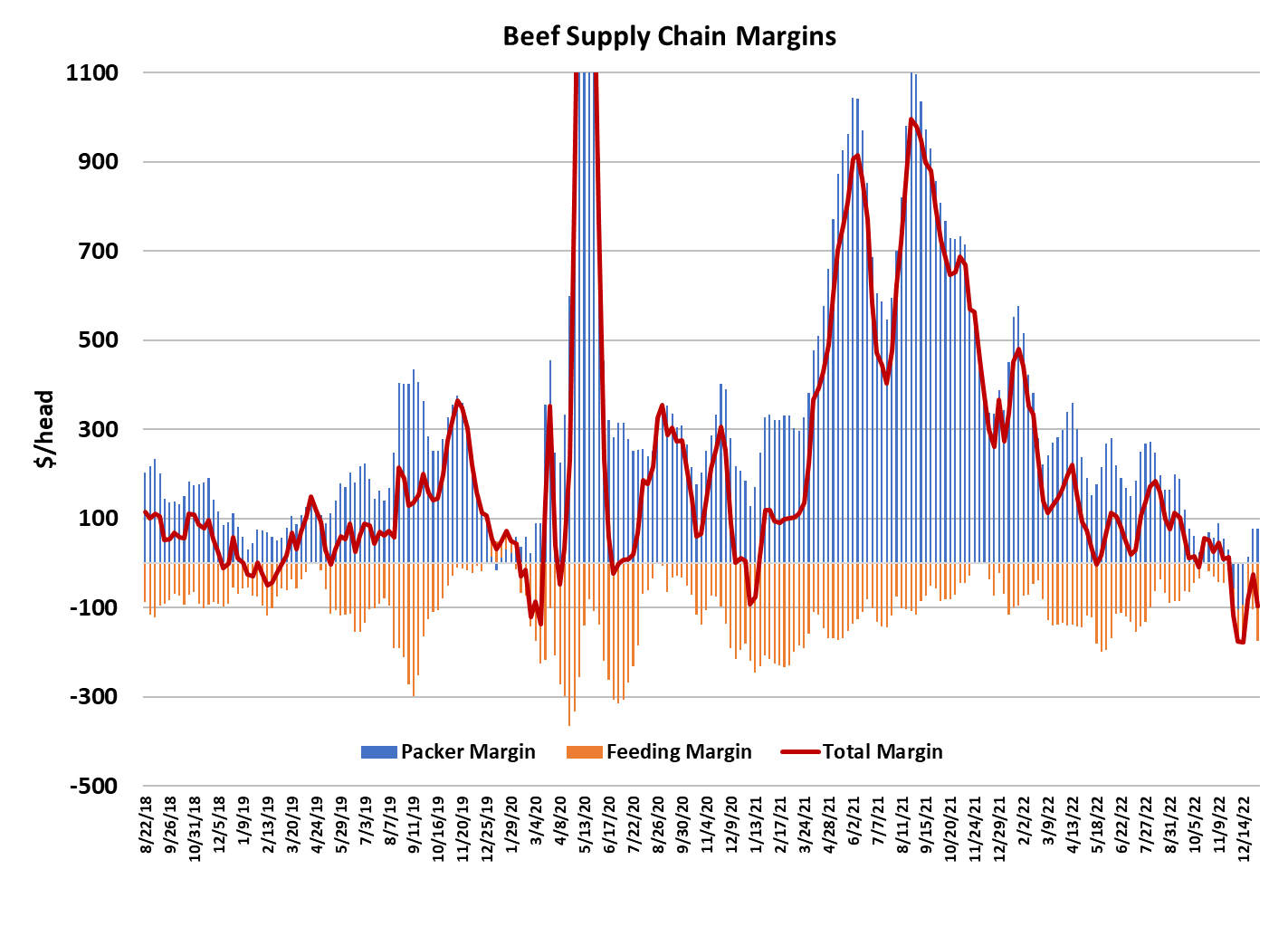

lost in December. This week’s combined margin chart tells an

interesting story. It looked like the margin was headed into an

upcycle, but now it has turned sharply lower once again. On the

surface that seems somewhat odd since the cutouts are still rising.

When I investigated the cause of the margin downturn, I found that it

is being driven by cattle feeding margins moving lower. The issue

here is that from late July until late August, cash feeder cattle prices

escalated from about $170/cwt. to $180/cwt and those are the cattle

that are now coming to market and the breakevens on those cattle

have risen much faster than spot cattle prices have. My margin

model shows that those cattle need to bring almost $170/cwt. to

breakeven. Obviously, cattle are trading well below that. Did cattle

feeders pay too much for feeder animals back in August? Yes, it

appears so. Will that prevent them from over-paying for feeders

again? Not likely. They are slow learners. But at least they are

getting reminded that, so far, it hasn’t worked very well to pay $180+

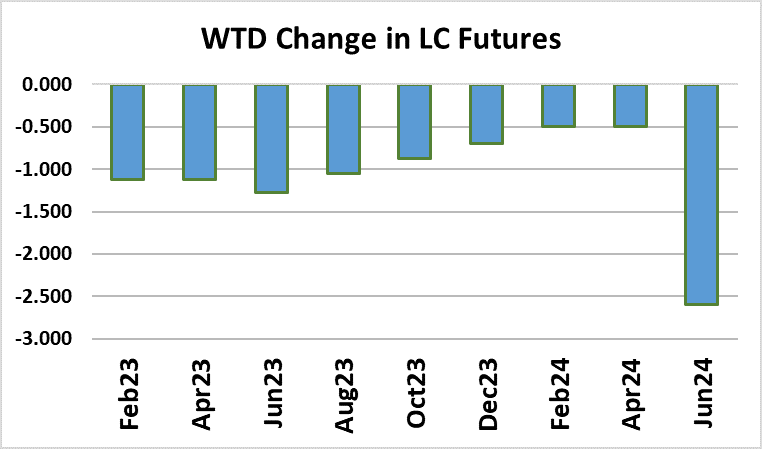

for feeder animals. And now the futures market is telling us that they

will be paying $207 for feeder animals this fall. It will take some very

high fat cattle prices to make that work financially, certainly a lot

more than the $168 the April 2024 LC are trading at. Heck, $168

fats wouldn’t be enough to cover the cost of feeders they paid $180

for, much less $207. The point is that something is seriously out of

whack here. It was the same way last spring, with fall FC futures

trading way above where they eventually settled. However, these

high breakevens will keep cattle feeding margins in the red for a long

time and that means they won’t take very kindly to packers

suggesting lower prices for fed cattle. There is probably a day of

reckoning coming in the not-to-distant future when the cutouts

tumble and packers want to buy cattle cheaper, but cattle feeders

resist mightily. Next week, watch for the cutouts to turn lower as the

industry gets back to full production. Packers might not get cattle

bought cheaper because they have some margin to give, but it won’t

take much to put them back in the red as well.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}