Beef Wrap January 13

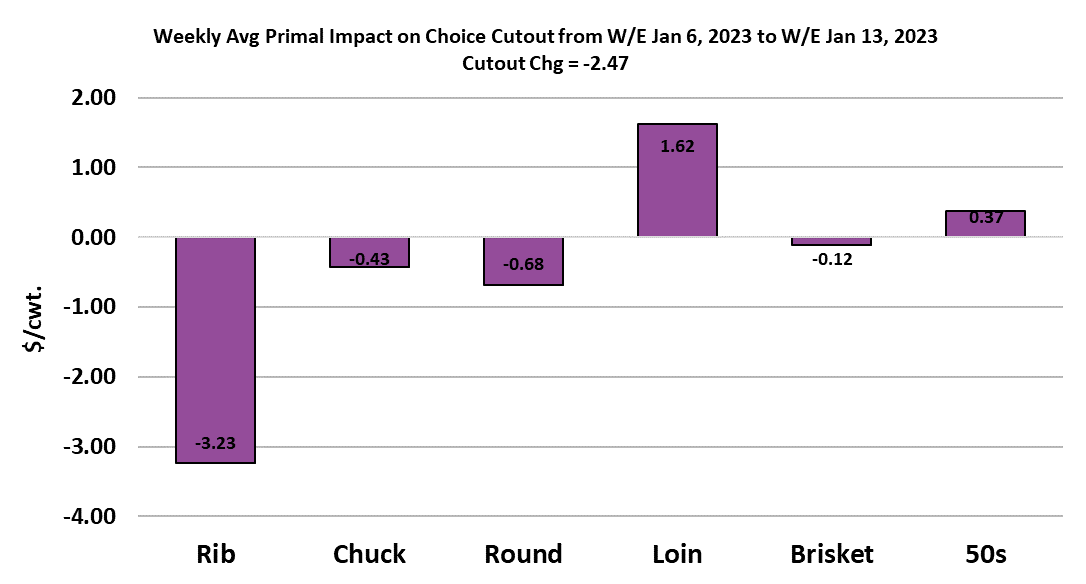

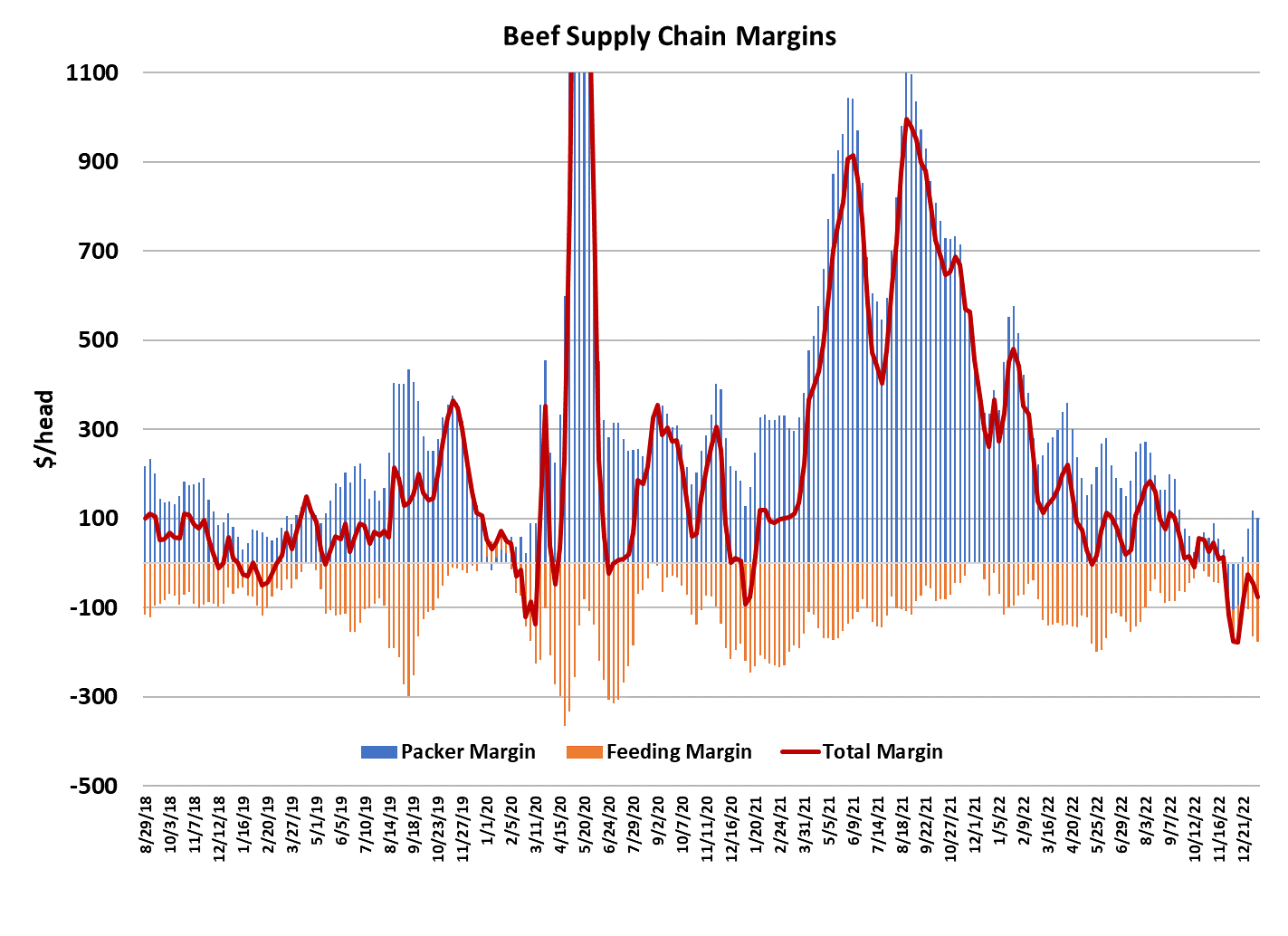

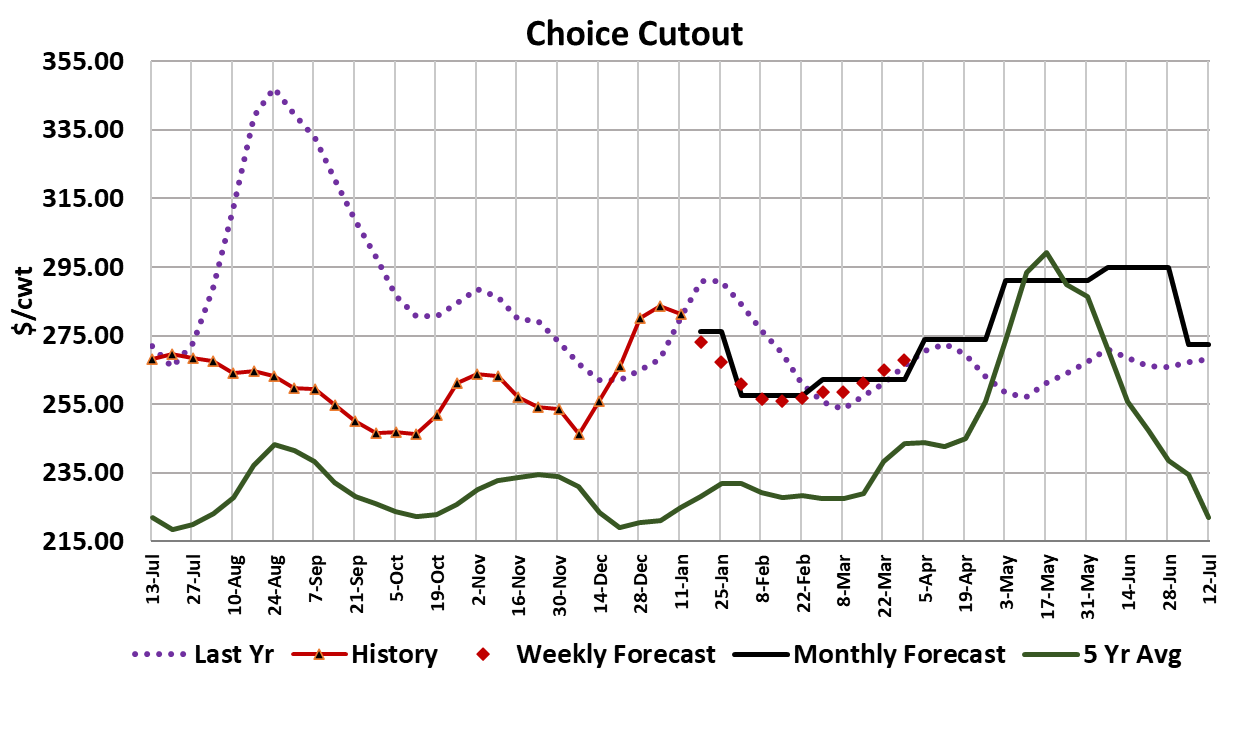

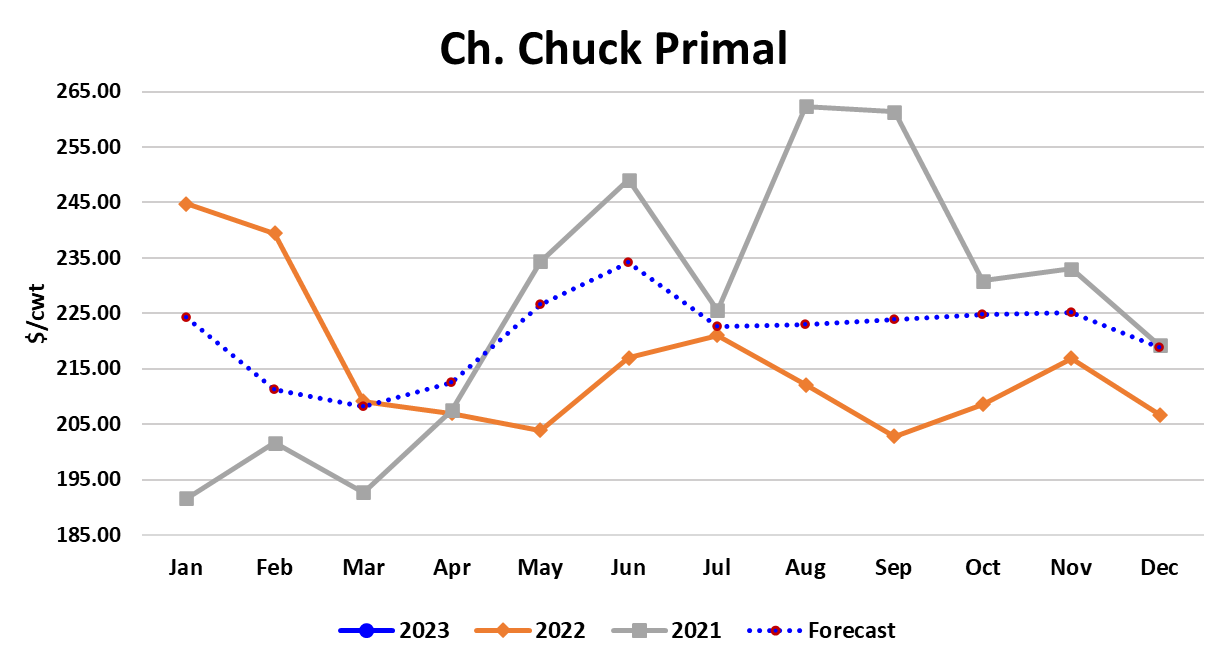

Packers finally had some success in halting the cash cattle market this week. When all of the transactions are tallied and reported on Monday, it looks like the average sale price will be close to $157/cwt., down about $0.75 from the week before. Cattle feeders held out until the end of the week for most of the trades, but in the end, their need to move cattle outweighed their need for higher prices. It is likely that some cattle got backed up in feedyards over the three short kill weeks surrounding the holidays and that led to the lower trade. This week also saw the beef market turn a bit lower. The Choice cutout lost $2.47/cwt. on a weekly average basis, but the Select gained $1.16/cwt. The rib primal finally started moving lower, but the loin primal was actually higher on the week. So there is still some work to be done there. End meat prices cooled off a bit too, probably as a result of getting back to full production. Packers seem to be a little cautious in ramping back up after the holidays, however. This week’s fed kill clocked in at 507k. The drastic improvement in packer margins over the holidays served as a stark reminder to packers that running aggressive slaughter schedules is detrimental to margins. Perhaps now they will dial it back a bit. They will need to scale back anyway simply because the number of market-ready cattle is scheduled to shrink from now through February as a result of past placement decisions. I’m forecasting the fed kill to move down to around 480k per week by early February and it could fall below 470k by the end of February. After that, supplies start to increase again and by early April we could see fed kills back over 510k per week. So, beef production should tighten up over the next several weeks but demand is typically pretty soft over that period as well, so smaller beef production doesn’t necessarily mean higher pricing. In fact, I’d argue that the demand effect will be more important and that we should actually see lower cutouts between now and the end of February. The current forecast has the Choice cutout averaging around $256/cwt at the end of February. That is a solid $25/cwt. below this week’s average. I expect most of the loss will come in the middle cuts, but the end meats may also see moderate price concession. Much will depend on how well consumer demand holds up.

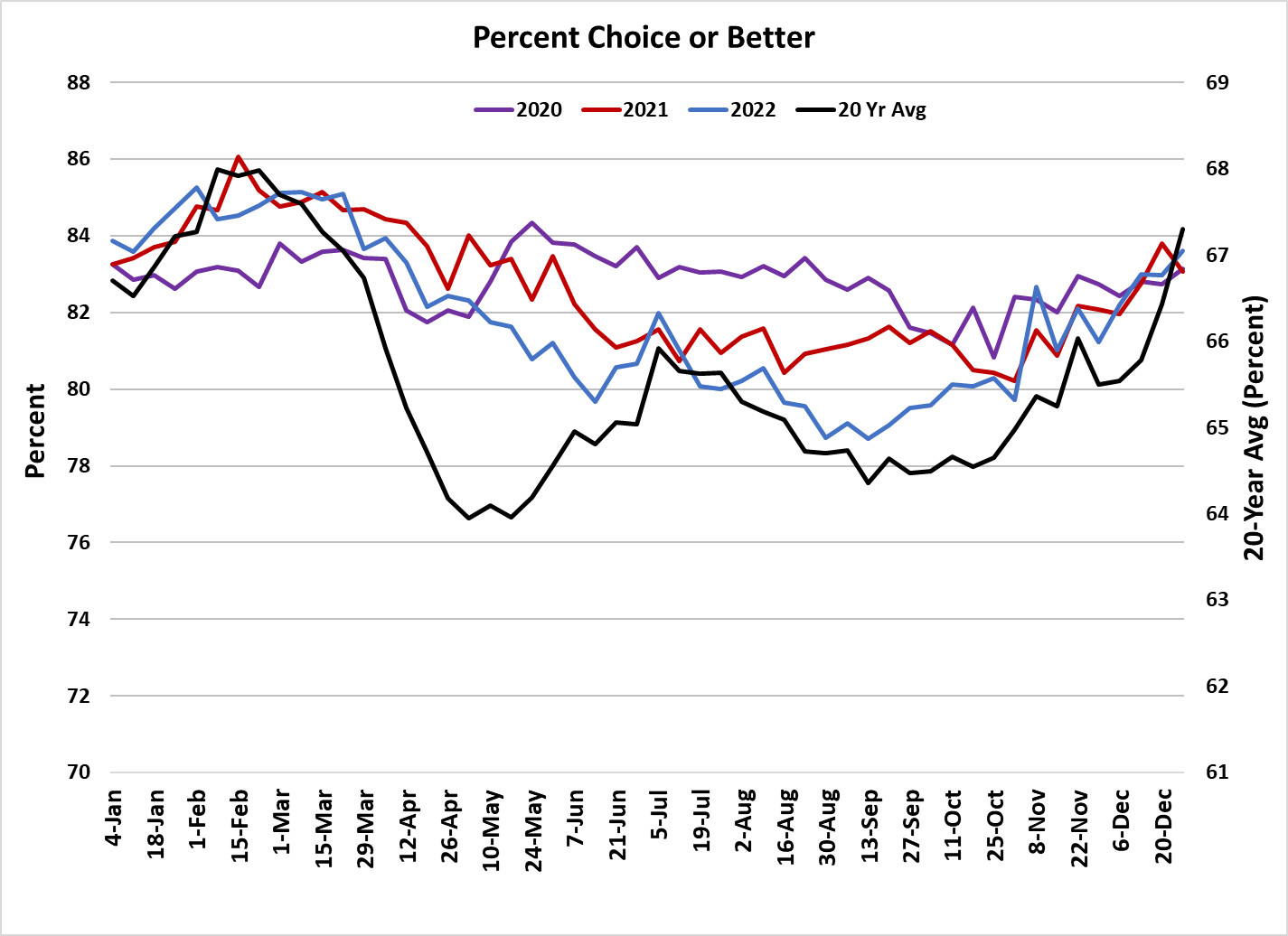

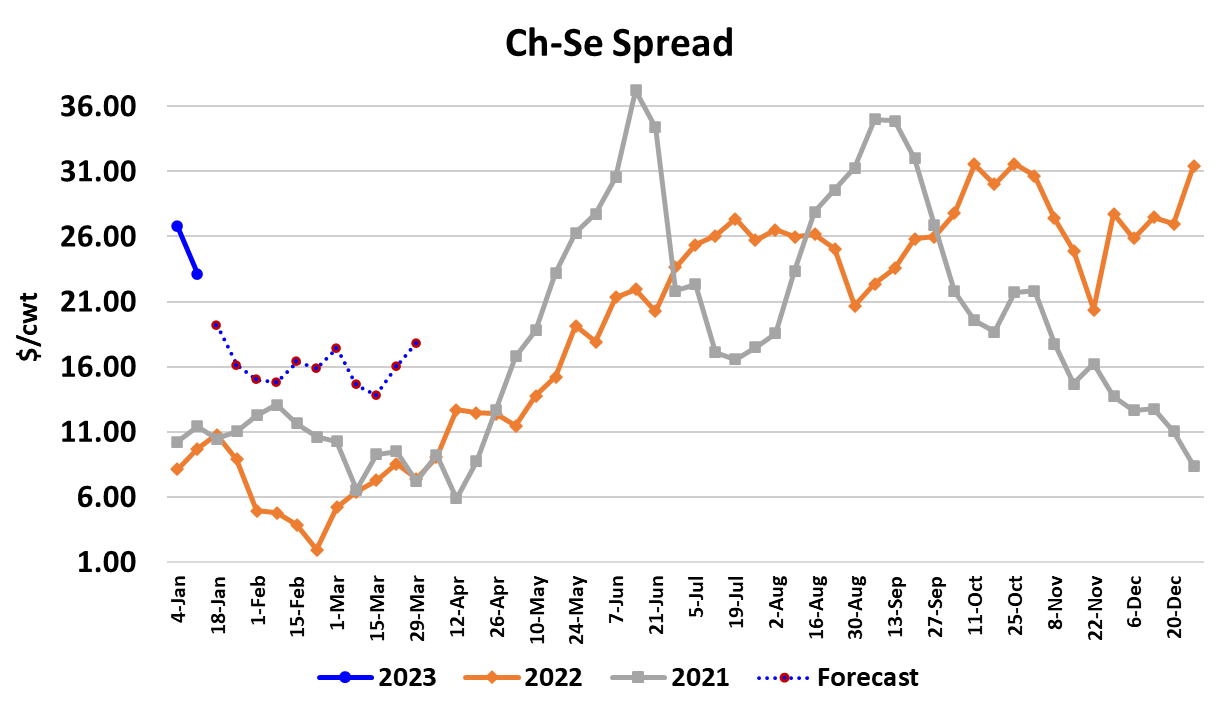

This week’s CPI number indicated that inflation cooled a bit more during December, so if that trend remains intact, it will be beneficial to beef demand. USDA reported retail beef prices for December this week and the “all fresh” beef price was up almost two cents from November at $7.16/lb., but that was 2.4% below the previous year. So, beef at retail is still pretty pricey and after that sharp increase in the cutouts during December, retailers might be reluctant to take pricing down very much in Q1. In addition, pork seems to have hit a huge demand air pocket over the past few weeks and thus pork pricing is now at levels that will make it much more attractive for retail features in Q1. Chicken is cheap too. Maybe, in the near future, beef will catch a big downdraft in demand just like pork. It is hard to say, but I don’t see a lot of positives for beef demand in the near term and that is why I suspect the demand effect will more than negate any support that smaller beef production might provide. The combined margin is back on its way down also, so there is one more thing in the bear column for beef demand. I’m also a bit concerned about international demand for US beef in Q1. China, which has become the third largest destination for US beef, is awash in covid right now and we have already seen beef shipments to China decline. That could easily extend for several more months. It has been difficult to discern much from the weekly export data because it gets pretty goofy over holiday periods. The next release of the monthly export data from ERS will come on Feb 8 and I’m expecting it to show December exports down almost 5% and if that is correct, then 2022 exports as a whole would be up only 2.8% from last year. That would still be record large exports, but it is well below the rosy forecasts from earlier in 2022. Cattle grading has improved a good bit in recent weeks and in the last week of 2022, the Choice and better percentage was a bit stronger than in either of the previous two years. That is a dramatic change from back in September when the grade was well below those years. That should help meet consumers demand for high quality beef and eventually lower the Choice-Select spread. It also may be a sign that feedyards have lost some currentness. Steer weights were reported 12 pounds lower over the two-week period that covered the holidays. That was a bit unusual since normally weights tend to rise when the kill slows. It is likely that the severe cold snap just before Christmas helped take some weight off of the cattle, but since the first of the year the weather has been rather mild across the production areas, so I wouldn’t look for those dramatic weight losses to continue. Weights should still move lower seasonally, but only by a couple of pounds per week. It doesn’t look like we are going to have a “weather market” this year. Next week, watch for further erosion in the cutouts and potentially some more pressure on cattle prices as a result. Futures have seemed a little defensive recently and if the cutout starts to come down in big chunks, I suspect traders will be pretty quick to sell.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}