Beef Wrap January 5

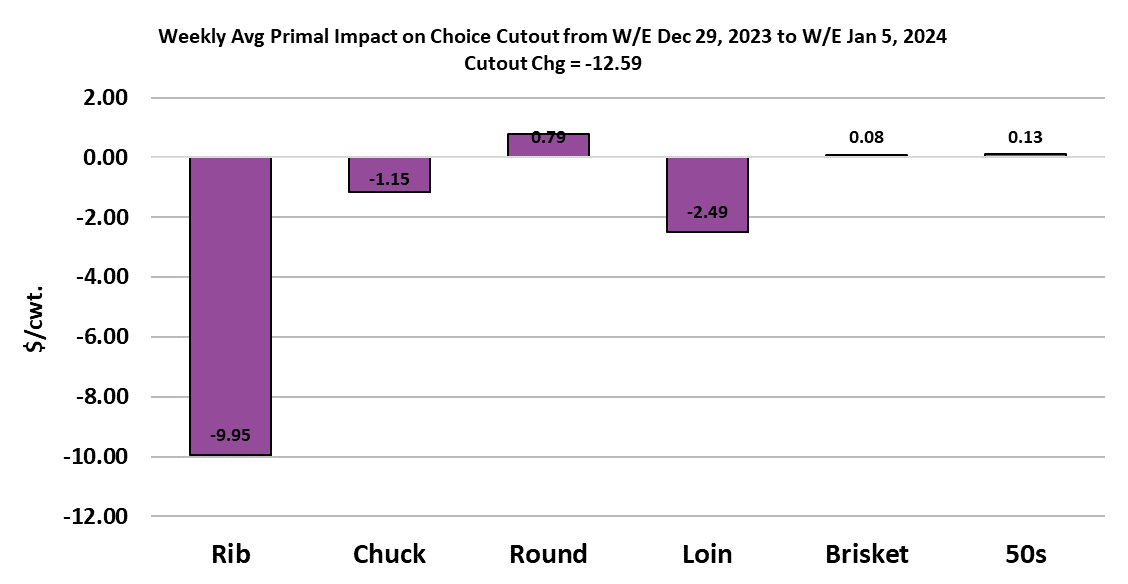

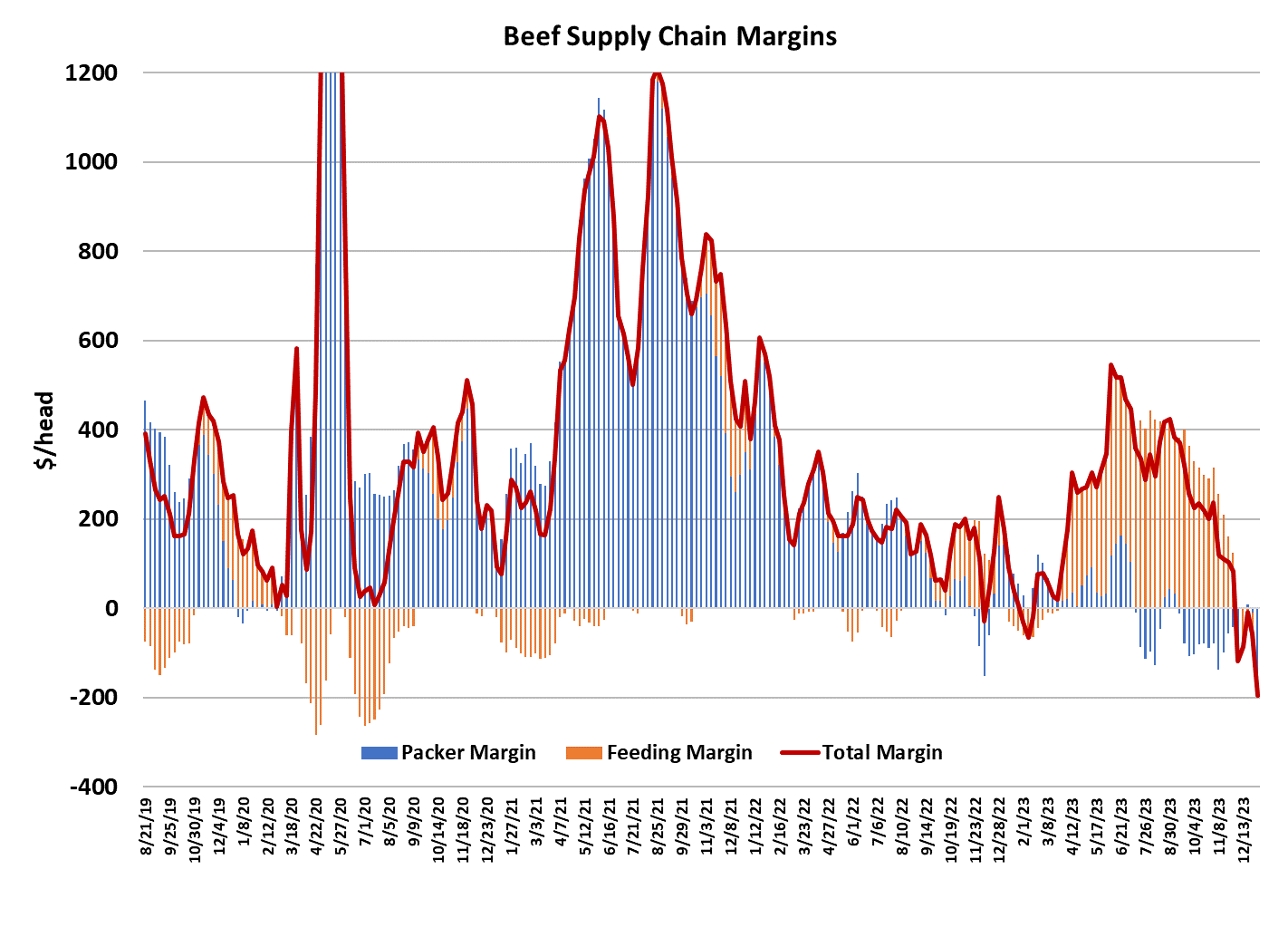

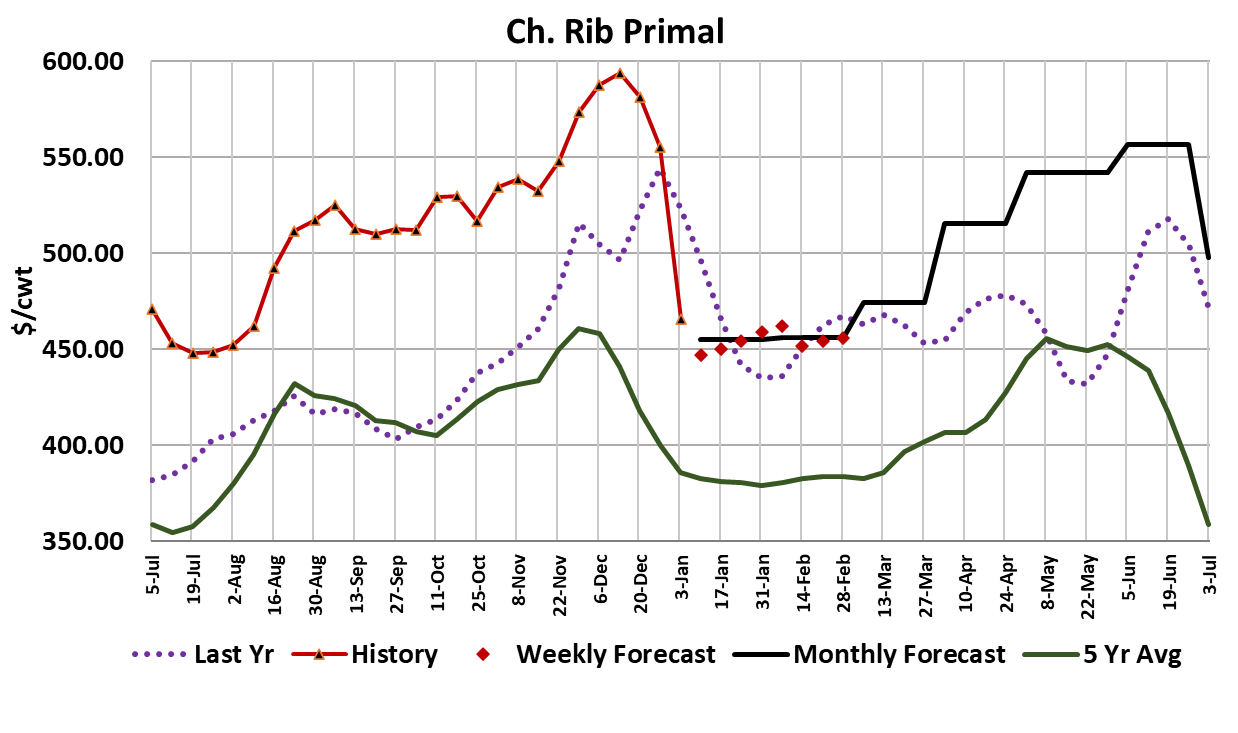

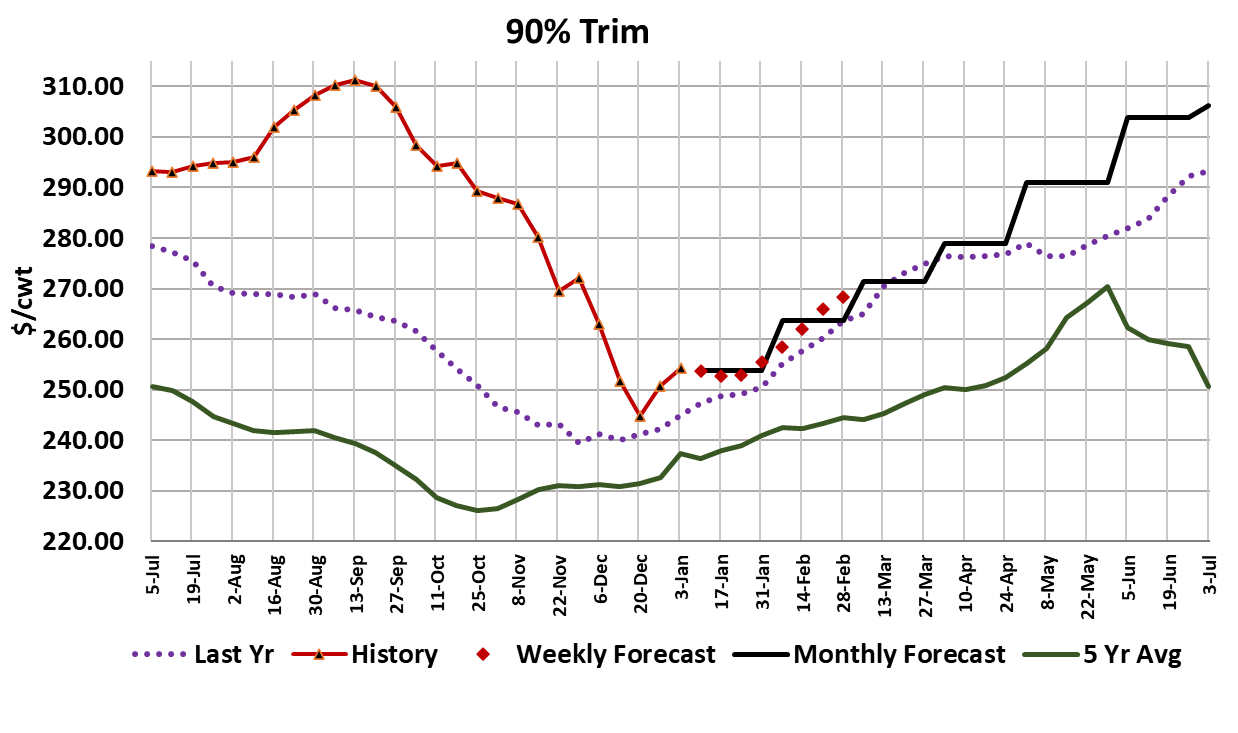

Cash cattle traded in North this week in the $174-175 range and while trade was a little slower to get started in the South, it looks like some trade late on Friday happened at a steady $173. Thus, the weekly average should be around $174.30, up close to $2 from the week before. This is the third week in a row that cash cattle prices have advanced $2. On the beef side, prices for beef ribs collapsed and that dragged the Choice cutout down $12.59 on a weekly average basis. The Select cutout was only down $1.26, but since Choice makes up roughly 80% of the product sold, the blended cutout was also down hard. With beef prices moving sharply lower and cash cattle moving higher, packer margins took a huge hit. I calculate this week’s margin at -$145/head, down from roughly -$10 the week before. So what is a packer to do when beef prices are struggling but they can’t seem to get cattle bought cheaper? About all they can do is slam the brakes on slaughter. However, as much as they might want to, cutting the kill sharply next week might not be feasible since there is probably a good deal of pipeline refilling that need to be done following the holidays. Next week, when the more expensive cattle show up for slaughter, packer margins could easily be $250/head or more in the red. In situations like this packers often tell beef buyers that they need to raise beef prices because they have been forced to pay more for cattle. Sometimes that works and sometimes it doesn’t, but the times when it works are typically high demand periods like prior to Memorial Day or Christmas, when buyers absolutely must have product. I don’t sense that is the case here in early January and so packers may find themselves powerless to stop the bleeding. However, there are plenty of signs that feedyards have lost currentness over the past couple of months and so packers may find some success if they have the discipline to pull way back on the kill for a couple of weeks. This is the time of year when retailers turn their focus to end meats and grinds, so those are the best candidates for improving the cutout over the next two months. This week the chuck primal traded a little lower and the round primal a little higher, so on balance the end cuts did little to help packers. Briskets have been the only “end” item gaining ground recently, with that primal up almost $40/cwt. since the middle of November. Lean trim prices have finally stopped going down, with the 90s averaging about $4 higher this week to $254. Perhaps seasonally improving demand for grinds will help keep the 90s on an upward trajectory from this point forward. For the past month or so, it seems that demand for lower-valued items like chucks and grinds has been softening and now that the ribs have collapsed post-holiday, there is risk that weak demand for ends will be exposed. The next big holiday for middle meats is Valentine’s Day and there could be some re-strengthening in the ribs near the end of January as buyers prep for that event. This week’s slaughter was tempered by the New Year’s holiday on Monday, but packers ran a bigger-than-normal Saturday kill in an attempt to cover some of the shortfall. I estimate the fed slaughter this week to be around 435k, which is about 40k more than the fed kill during Christmas week. Next week, look for packers to resume killing in the 490-500k range as they finish refilling the beef pipeline. The flow model suggests that we need to see fed kills in the 500-510k range during January to keep from adding to the backlog of cattle in feedyards, but I’m not sure packers are willing to go there. I feared the scenario that the industry is now in: rib prices collapse, throwing packer margins deep into the red, right at the time of year when large supplies of cattle are becoming market ready. That would seem to be the recipe for tumbling cattle prices and we very well may see that materialize later in the month. Steer carcass weights were reported up one pound this week, marking a new all-time record high. We are long past the point in the calendar when weights should have turned lower, but here they are still moving higher. That should work to the packer’s advantage when trying to reverse cattle prices in the weeks ahead. There have been a couple of snow events in the Plains recently, one in the North last week and one in the Southern Plains set to run through this weekend. That has the potential to take some weight off of feedyard cattle, but the winter weather hasn’t been frequent enough to declare this a “weather market”. Of course, that could still develop over the next few weeks, so it is worth keeping a close eye on temperatures and precipitation in the Plains. Another snow event that might create more trouble for the beef complex is one that is scheduled to dump 1-2 feet of snow on the population centers located in the Northeastern US this weekend. That could limit fill-in buying for a few days. Next week, watch for signs that end meat demand is improving and thus ready to help support the cutout through this difficult period. Also watch the daily kills for signs that packers are reducing the kill in order to limit the damage to their margins.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}