Beef Wrap December 22

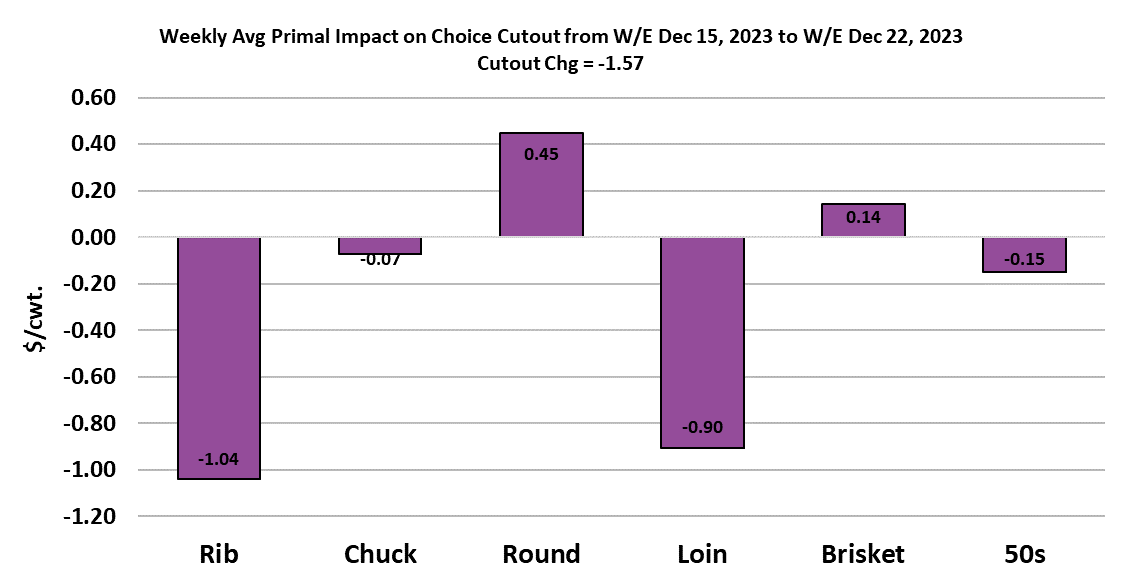

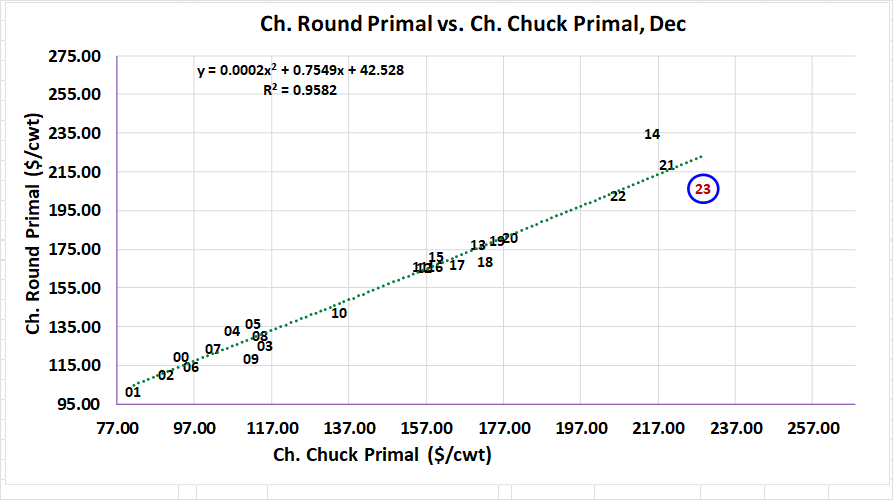

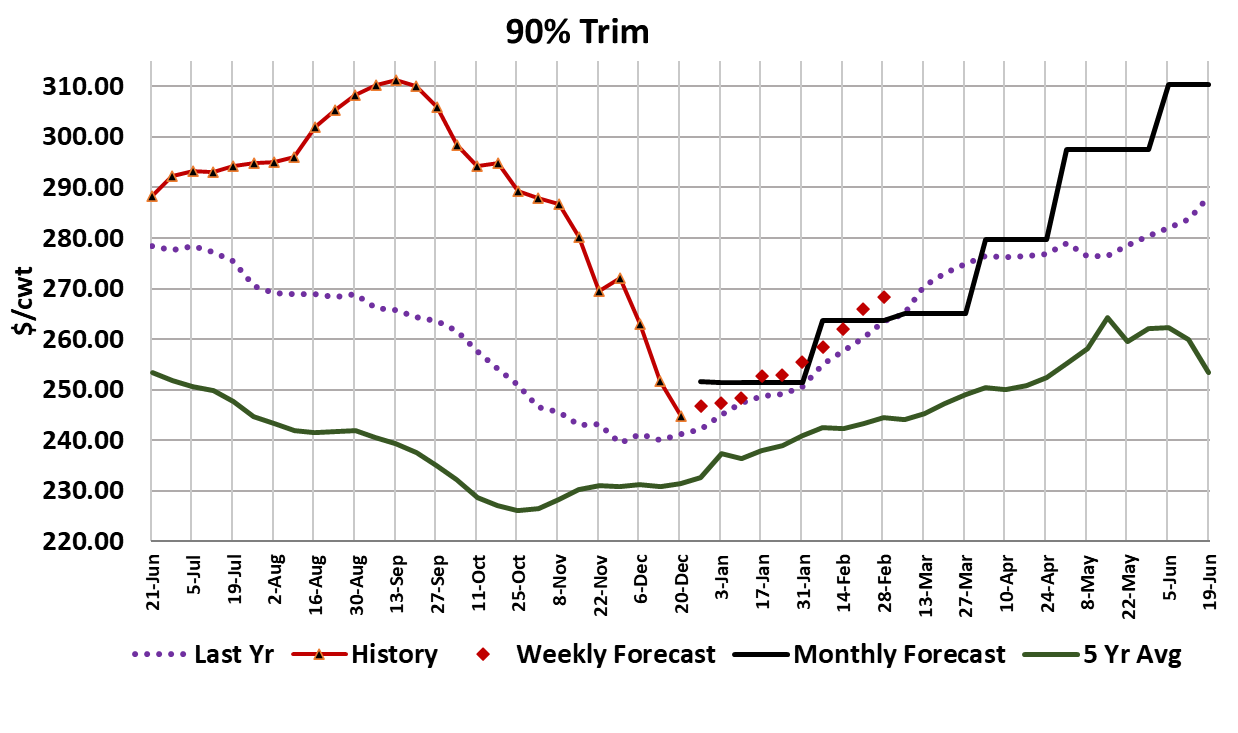

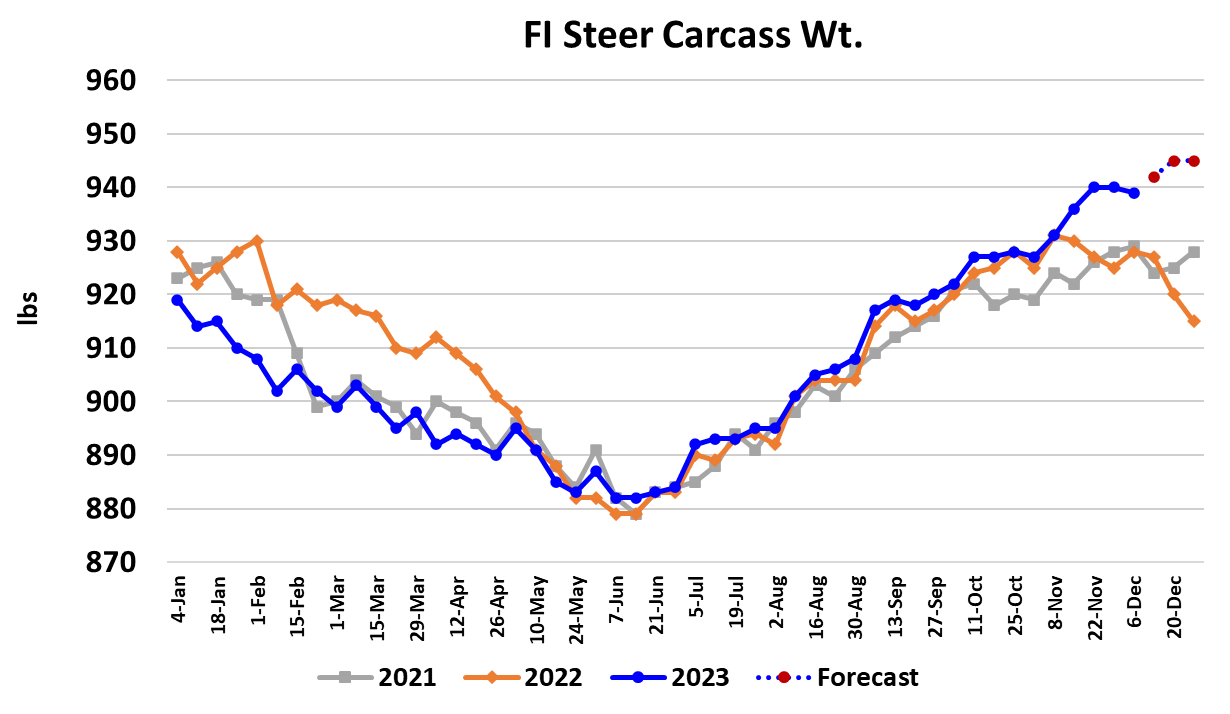

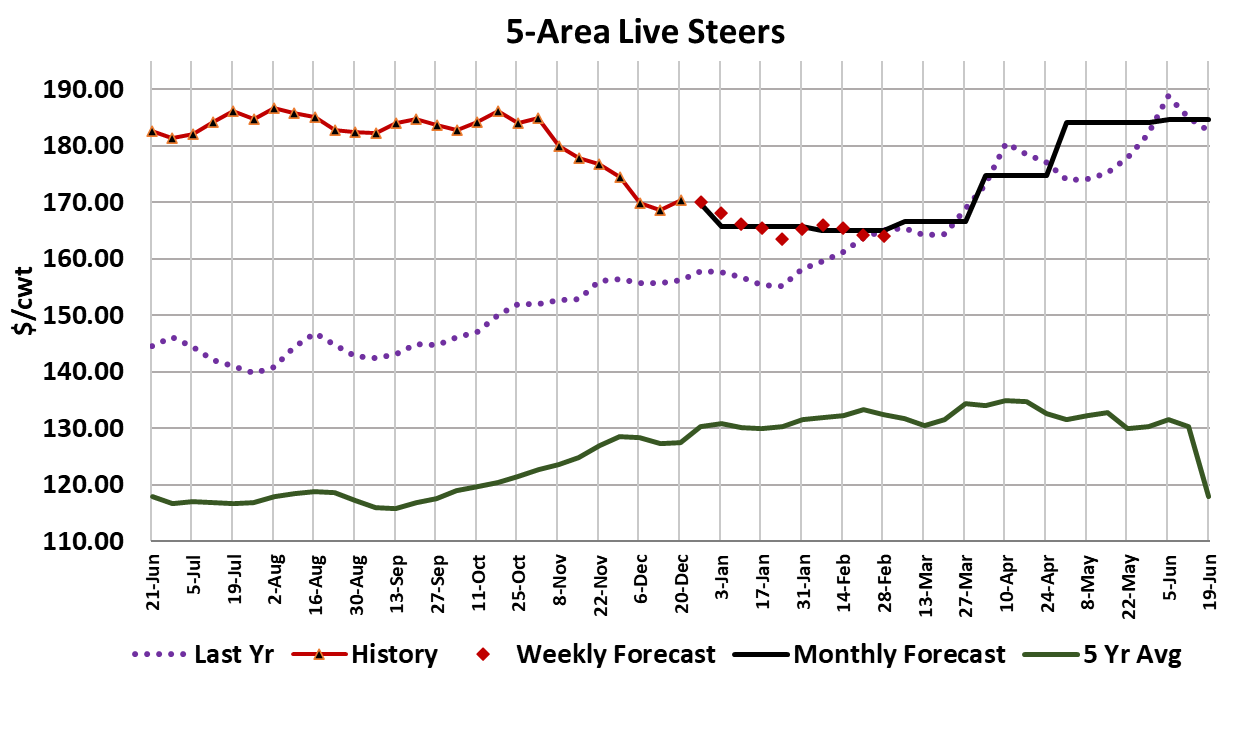

The beef markets were mixed this week, with the Choice cutout losing $1.57/cwt. on a weekly average basis while the Select cutout added $2.88. Cash cattle traded a little higher, with the weekly average expected to be around $170.35. That would be up $1.64 from last week’s average. Beef prices are starting to look a little shaky, particularly for the Choice middles. It was the rib and loin primals that exerted the most downward pressure on the cutout this week. This is the time of year when demand normally transitions from middle meats to end meats and grinds during January. However, last year the seasonal break in rib prices didn’t really get going good until about the second week of January. It’s hard to tell if that is going to be the case again this year, but normally I would be looking for rib prices to be coming down in big chunks by the end of December. As the middles pass the baton to the end cuts in January, it will be a good test of the strength of demand for lower-valued beef items. For the past year, it has been clear that demand for high quality middle meats has been off the charts, but demand for lower-valued end cuts and grinds has been less certain. Of course, the supply side will have something to say about price levels as well and it looks as though cattle and beef supplies should be ample at least through Q1 and partially into Q2. The current forecast has chucks trading sideways through Jan/Feb, but rounds are projected to track higher and that should restore the normal price relationship between chucks and rounds. At present, rounds are running cheap relative to chucks. We also need to keep an eye on the lean trim market, because it is sending out some cautionary signals at present. The 90s traded lower again this week and are well past the point in the calendar when they start to exhibit seasonal firming. This is an item that was trading well above last year through out 2023 and is now almost dead-on with last year’s level. Could it be telling us that demand for manufacturing beef is getting soft? If so, that won’t be helpful to the chucks and the rounds. The current forecast has the Choice cutout working down into the mid $270s during January, holding that level in February and then moving higher as spring approaches. I am counting on both softer demand and ample beef availability in Jan/Feb to produce that result. This week’s fed kill registered around 486k, as packers eased up on Friday and Saturday. Next week, the fed kill is expected to be near 425k as there will be no production on Monday, but packers are likely to run a strong Saturday kill to help make up some of the lost production. Packer margins are set to slip back into the red next week as the more expensive cattle they bought this week show up for slaughter. If the ribs break and take the cutout lower as anticipated, the red ink could get pretty deep for a few weeks. That is not the type of environment that encourages large kills and so I’d expect packers to throttle back on the weekly fed kill during January. That has the potential to create a big problem because supplies of market ready cattle should increase during Q1 and if the kill doesn’t keep pace, cattle could start to backlog fairly quickly. For the past couple of weeks, it has looked like futures traders weren’t taking the idea of a cattle backlog very seriously, but after this afternoon’s Cattle on Feed report, that fear might become more prominent in their calculus. USDA reported marketings during November were 7.4% lower than last year and that likely continued into December. At the same time that marketings were way down, placements into feedyards were stronger than expected. USDA pegged Nov placements to be down only 1.9% YOY, while analysts had been looking for a 4% decline. Thus, both marketings and placements should be bearish compared to pre-report estimates and that is likely to generate some selling in the futures on Tuesday. With this week’s cash market approaching $171 and the Feb futures settling around $168, there is no incentive for cattle feeders to delay marketings. They will likely come out after the holidays looking to move some cattle and packers, likely seeing red margins, might not have an appetite kill very many. Oh, and by the way, did I mention that the weather in the Plains states has been exceedingly mild for this time of year? Cattle should be gaining very well and that might make them ready to market ahead of schedule. So it still looks to me like the potential for backlogging cattle in Q1 is still pretty high. Steer carcass weights declined one pound this week, which wasn’t very impressive and odds seem strong that they will make one more push higher before the end of the year. Next week, look for the cutouts to trade lower as the middles start to come undone. Cash cattle stand a good chance of trading higher, not because cattle are scarce, but just because we rarely see cash cattle prices decline in the week between Christmas and New Year’s. But if packers pay up again for cattle they run the risk of even poorer margins after the holidays and that might require an even harder stomp on the brakes when it comes to kills in January.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}