Beef Wrap June 21

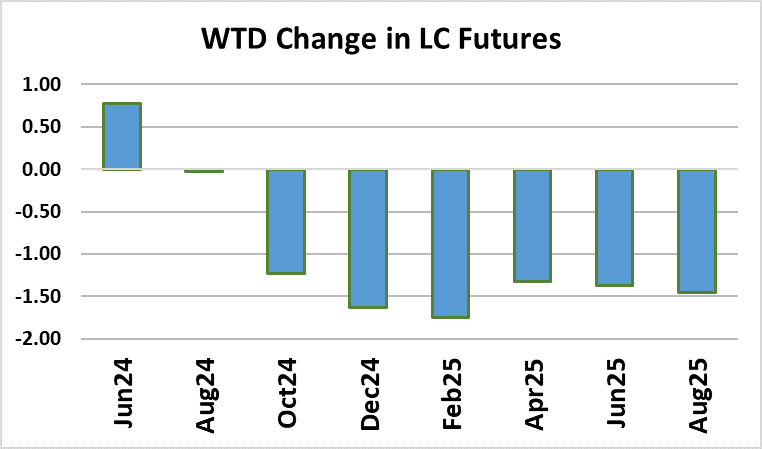

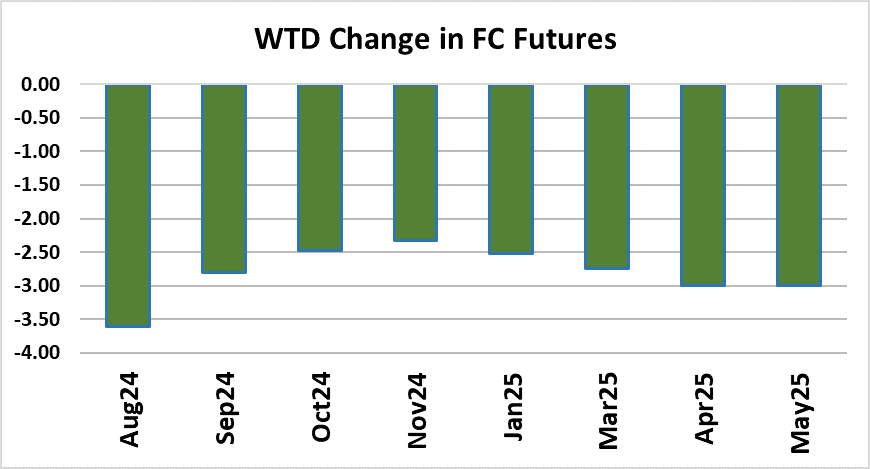

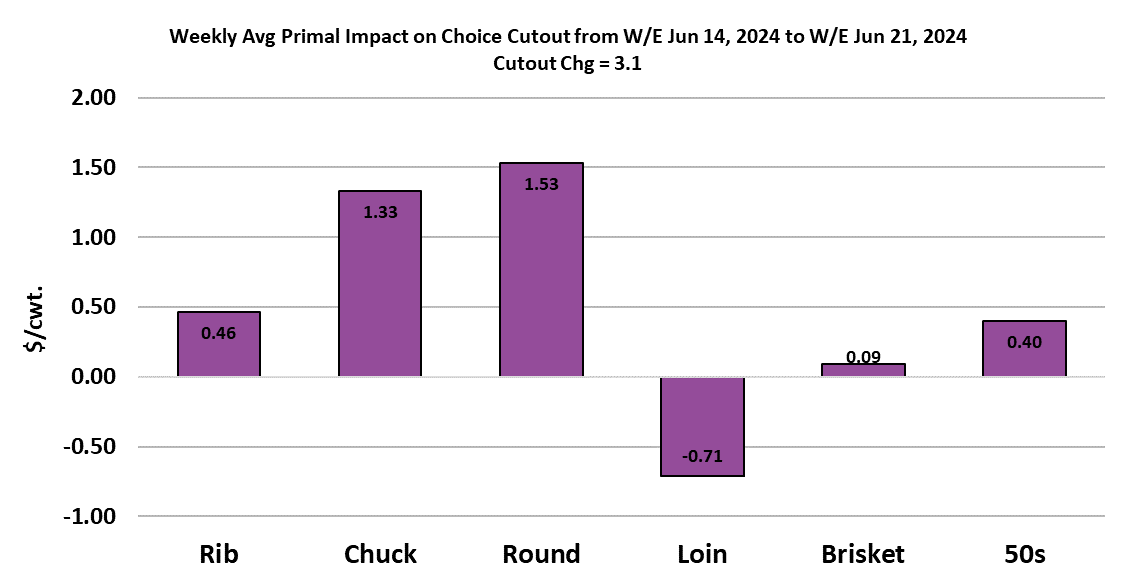

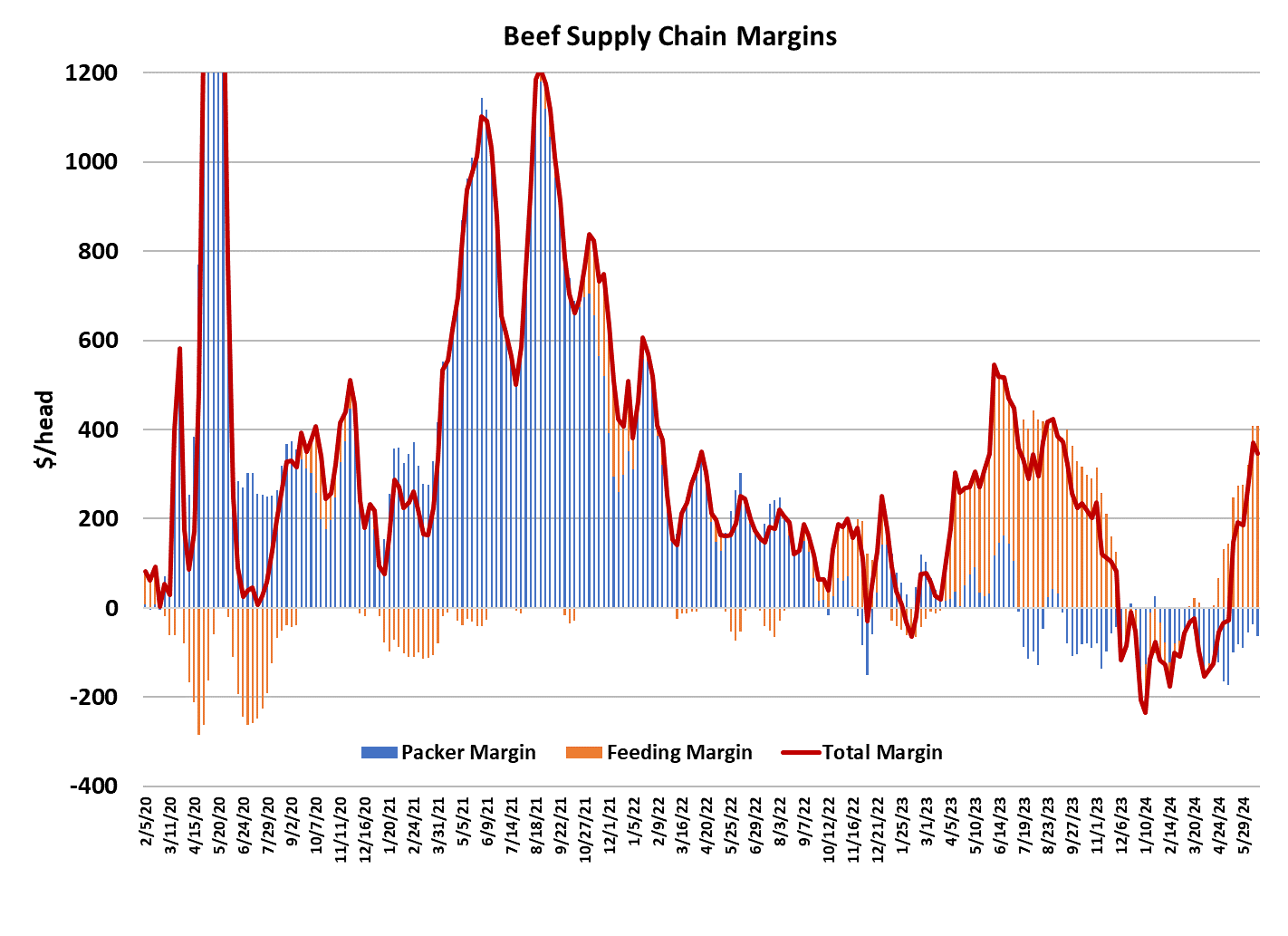

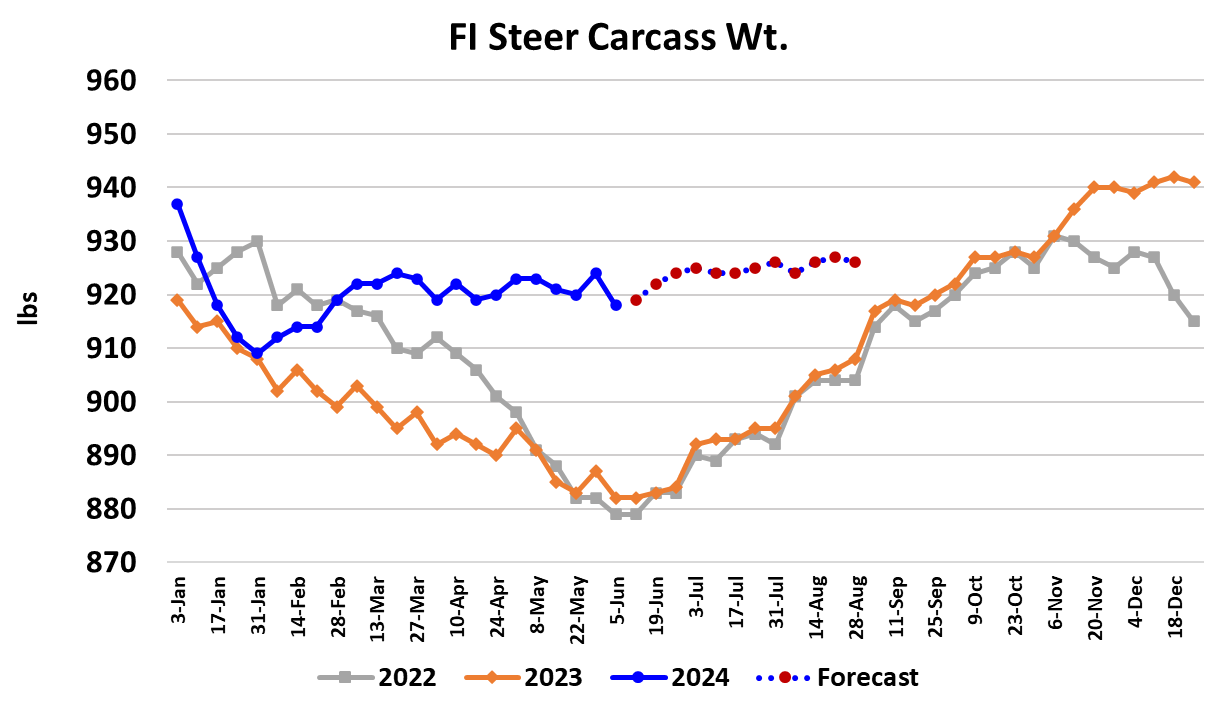

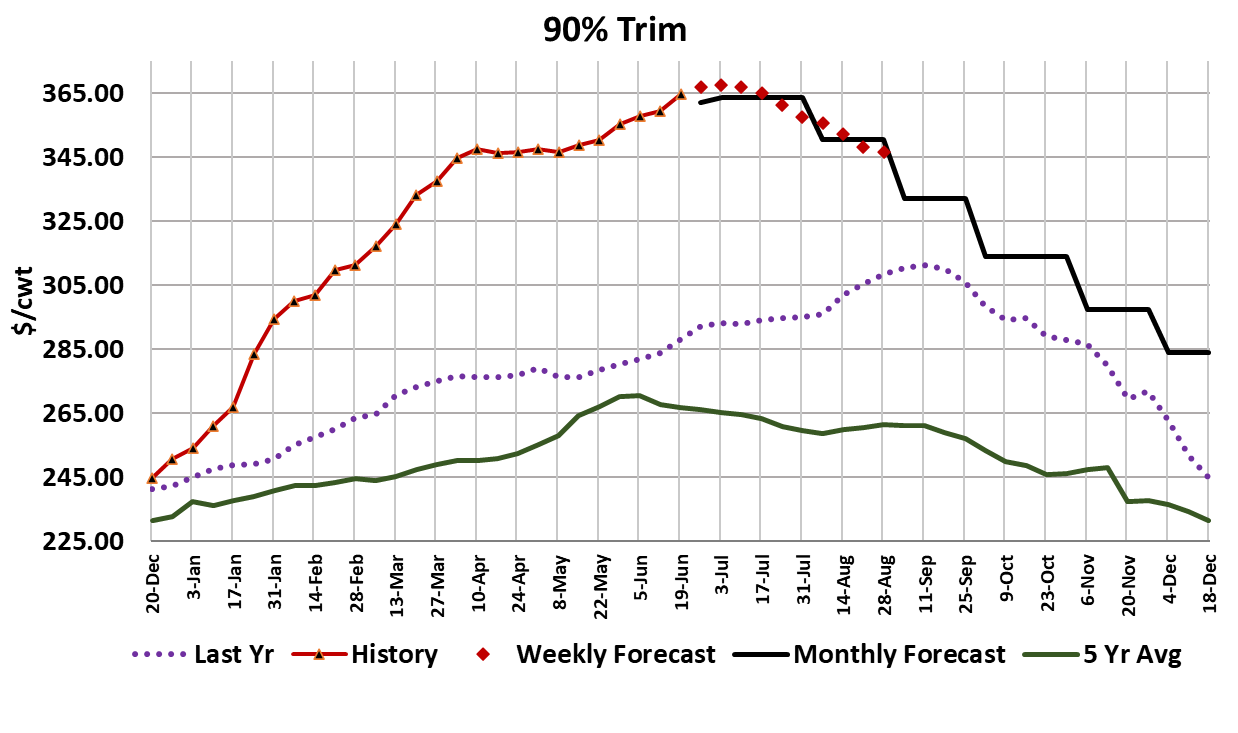

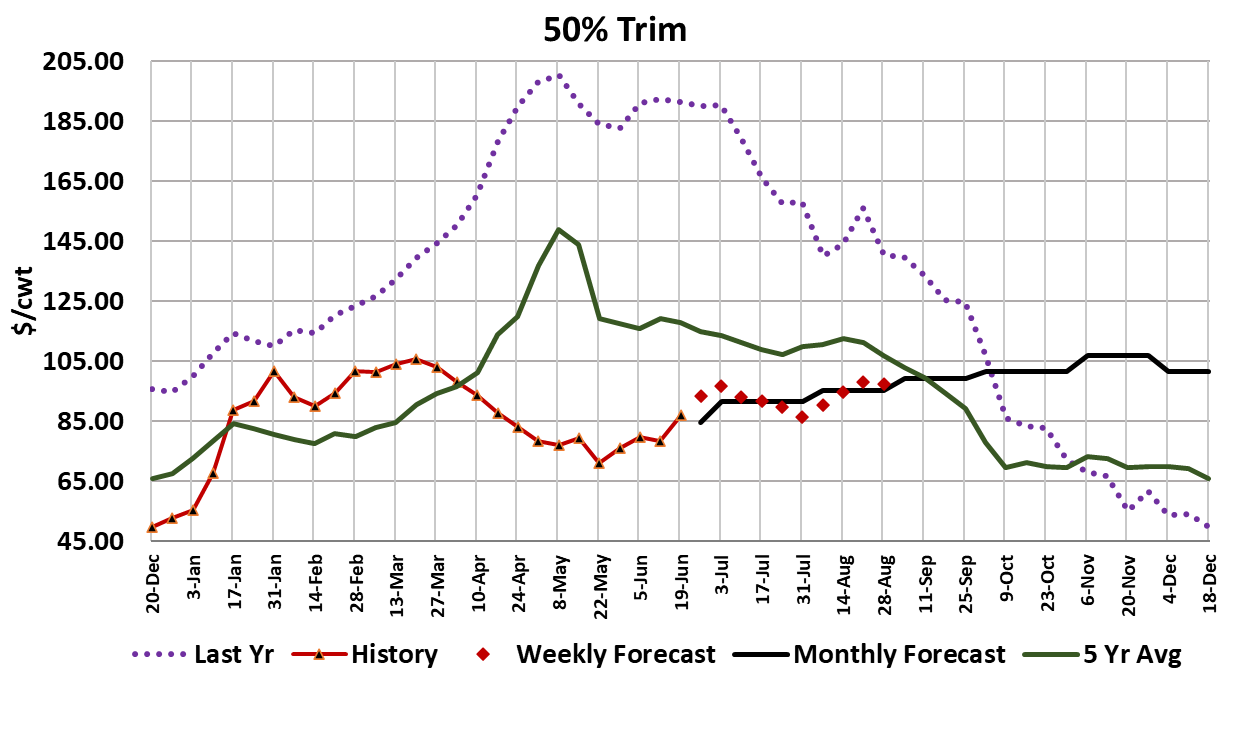

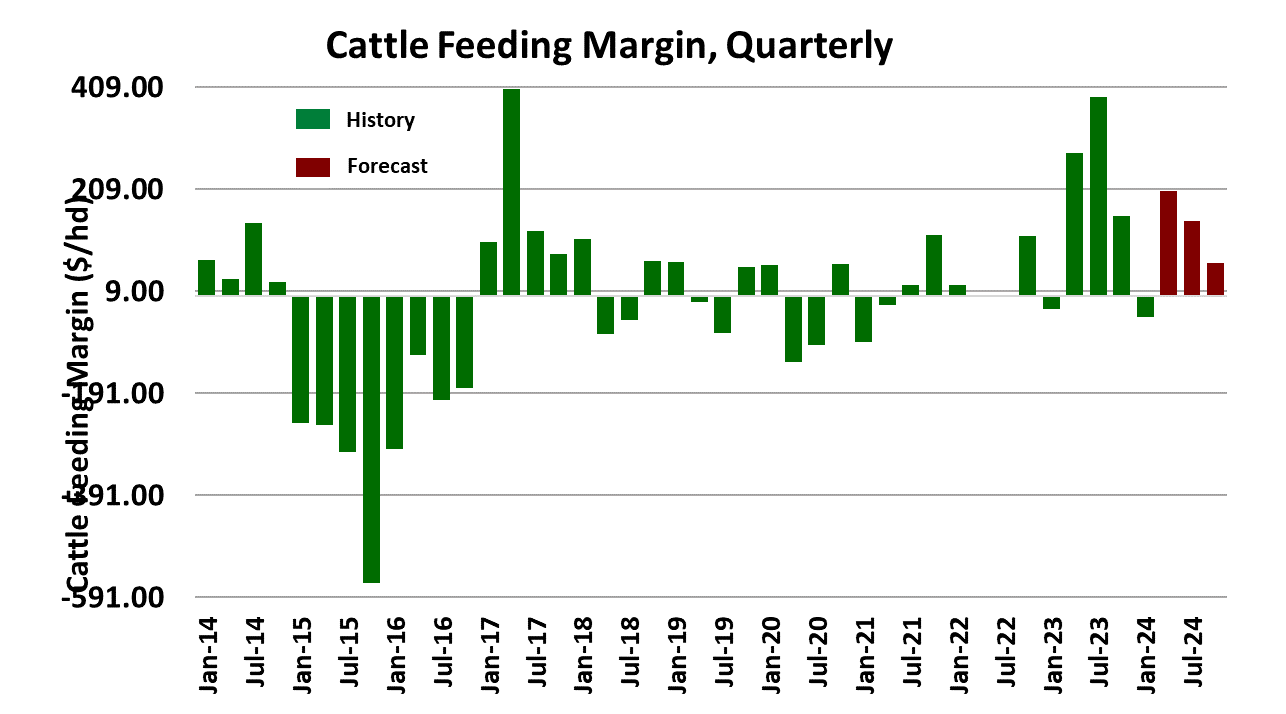

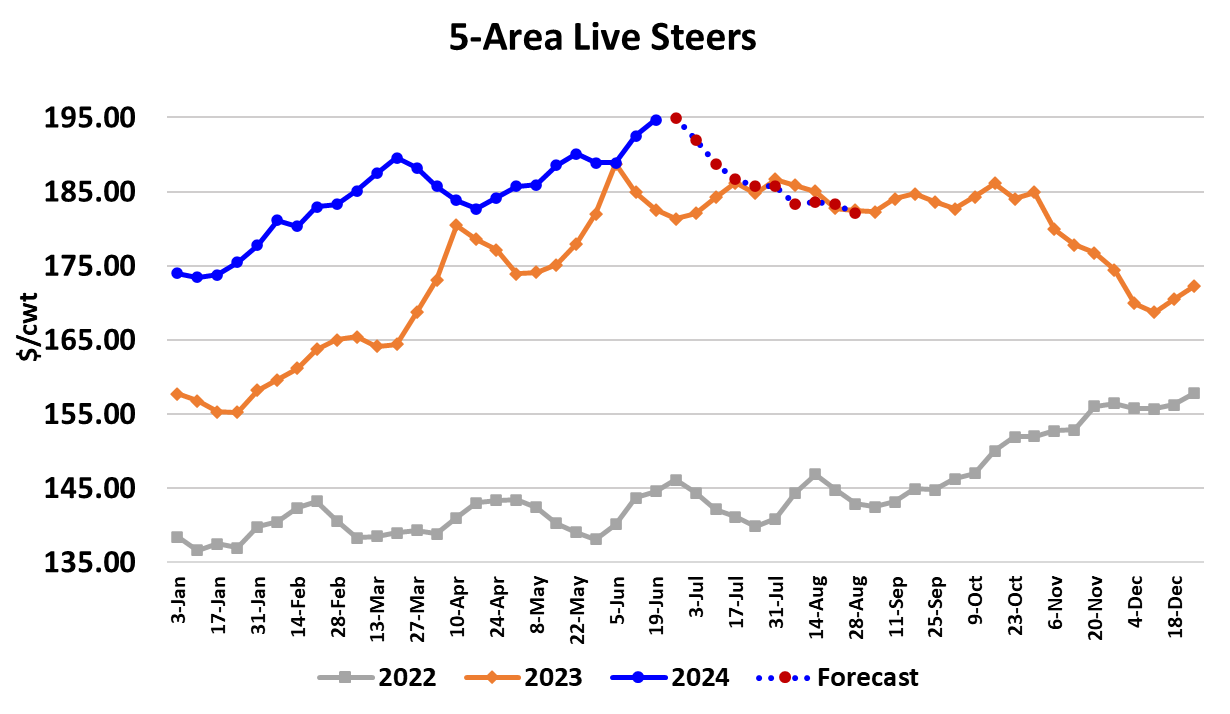

Last week cash cattle prices in the North exploded higher and this week it was the South’s turn to experience sharply higher prices. Trade happened late on Friday in both regions, but it looks like the bulk of the Southern trade happened at $189-190, up $3-4 over last week. In the North, live prices were in the $196-197 range, up $1-2 from last week. When all of the data is tabulated by USDA on Monday, I expect the 5-area weighted average to be just a shade under $195—another all-time record high. Futures traders don’t seem to believe that these high prices will persist as the Aug contract was actually slightly lower on the week. Jun is only one week from expiration and therefore must keep pace with the cash market, thus it is likely that Jun will gain several dollars early next week. However, today’s COF report threatens to spoil the bull’s party. It showed May placements up 4.3% YOY, compared to the average trade guess of a 1.3% decline. That’s a 5-6% miss and perhaps more significantly, it crosses the psychologically important zero line, i.e., placements were up when the forecast was for them to be down. Normally, that could be expected to trigger sharp selling in the futures, but is sharp selling really feasible when cash cattle prices are escalating rapidly? Perhaps traders will end up doing more of what they did this week, buying the front of the curve and selling the back months. The market is in a situation now where Jun24 is priced almost $3 higher than Jun25, even though everyone should be aware that available animal numbers will be much tighter next summer as the cattle herd continues to shrink. That is a sure sign that traders view the current cash market as an anomaly that won’t last. The fundamental forecast has cash prices declining moderately into August and then rising again in early fall, but the risk is to the upside in the summer cattle price forecast. The cutouts helped the bull’s case this week as the Choice added $3.10/cwt. on a weekly average basis and the Select was up $3.23. The main thing is that the cutouts didn’t crater after Father’s Day and that is a sign that beef demand is stronger than anticipated. Most of the support this week came from the chuck and round primals and it is very likely that is being influenced by the 90s market that just won’t seem to slow down. On a weekly average basis, fresh 90s were reported up $5.14/cwt. this week. What’s more, the 50s market added nearly $9/cwt. this week. It seems that most of the strength in fat trim pricing is likely coming from the demand side, since carcass weights remain relatively heavy. Summer is hamburger season in the US and now that the steak occasions have passed (Memorial Day and Father’s Day), attention turns to the grinds. However, interest in the middle meats hasn’t really fallen off as expected, because the rib primal gained over $4 this week and is now about $50 higher than it was in early May. Grilling season may have gotten off to a slow start this year, but it looks like it may stretch deeper into the summer than what is typically seen. It has been an impressive run for the cutouts over the past month or so, but unfortunately for packers, it has been an even more impressive run higher for cash cattle prices. I calculate this week’s packer margin at about $60/head in the red and when those more-expensive cattle show up for slaughter next week, there is risk that packer margins will be more than $100/head in the red. Cattle feeders, on the other hand, have considerable jingle in their pockets these days with margins now running slightly over $400/head. The combined margin chart is starting to look a lot like it did last summer, when cattle feeders earned huge profit and packers struggled to break even. This week’s fed kill came in at 504k, which is very close to what I’d estimate it should be based on past placement patterns. It is interesting that packers are not making any noise about cutting the kill, even though their margin situation remains dismal. That is likely because they sense that demand has picked up considerably since spring and thus don’t want to rock the boat by shorting customers. I think we can expect to see fed kills continue to run over 500k in the non-holiday weeks right through July. That should help feedyards regain some currentness and also limits the downside risk in cash cattle prices. FI steer weights dropped six pounds this week, but I don’t think that means they are going to suddenly start to trend lower. Instead, I see carcass weights holding in a mostly sideways pattern through the summer. Since we are now past the point in the calendar when weights start to increase, if weights move sideways over the next couple of months, the YOY gap will close considerably due to last year’s weights rising seasonally. At some point in August, I’d look for weights to start trending higher again and then keep a 10 to 15 pound premium over last year as we move toward Q4. Next week, look for the cutouts to slip modestly and that may provide an opportunity for the cash cattle market to take a breather, perhaps holding steady at this week’s level.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}