Pork Wrap Wrap Jan 9

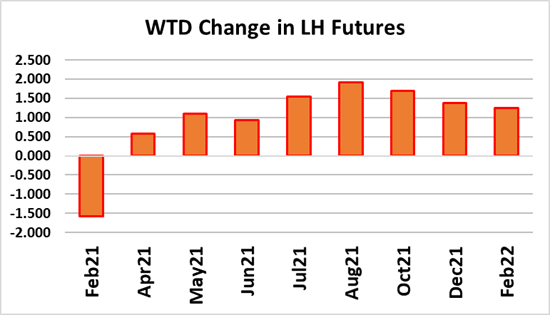

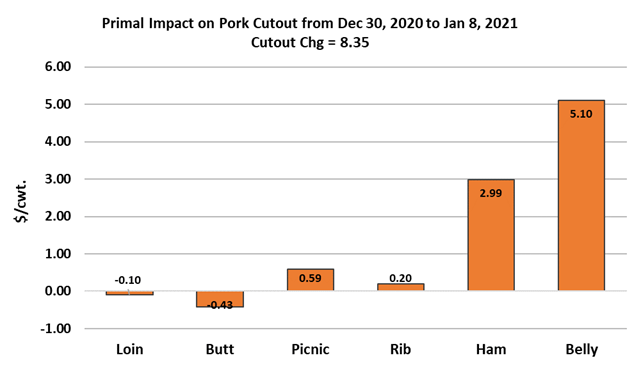

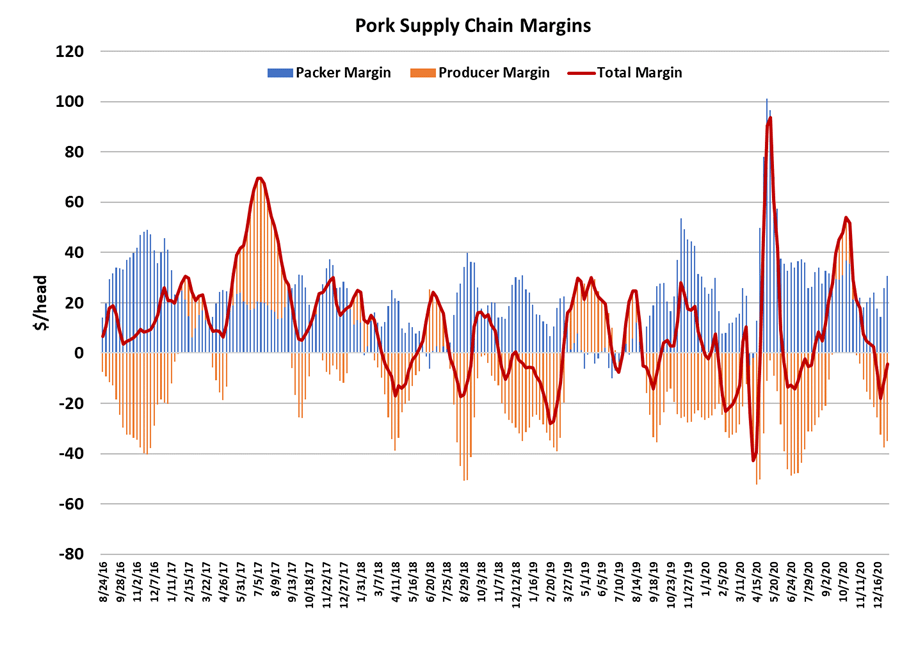

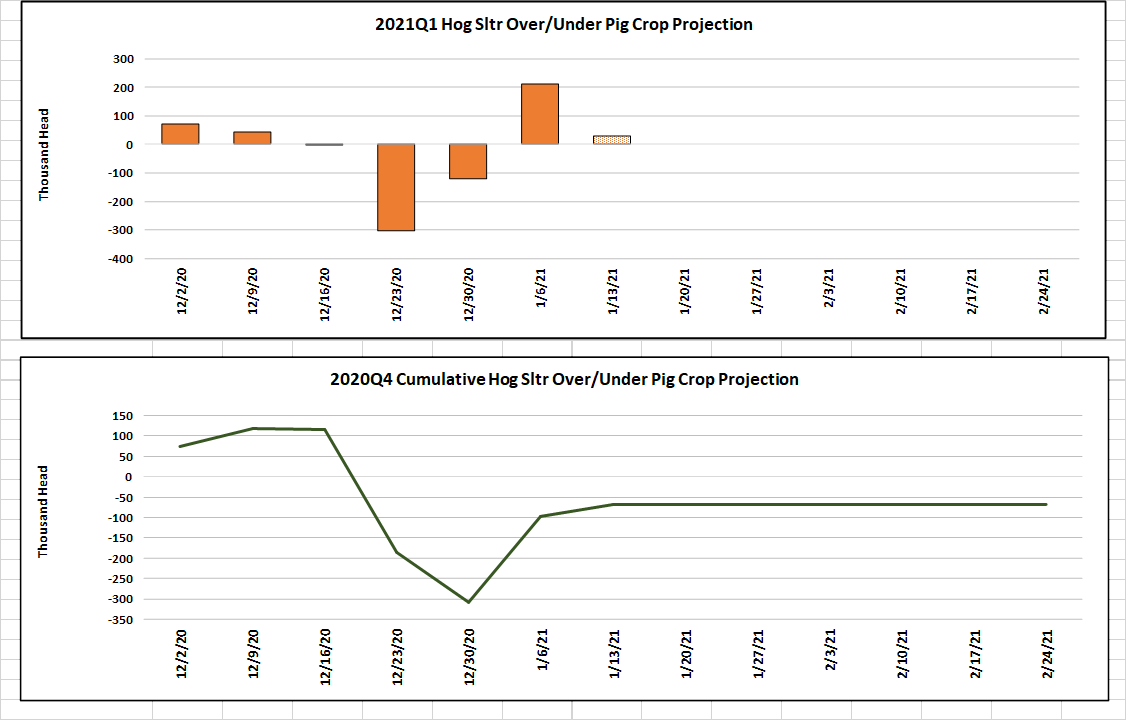

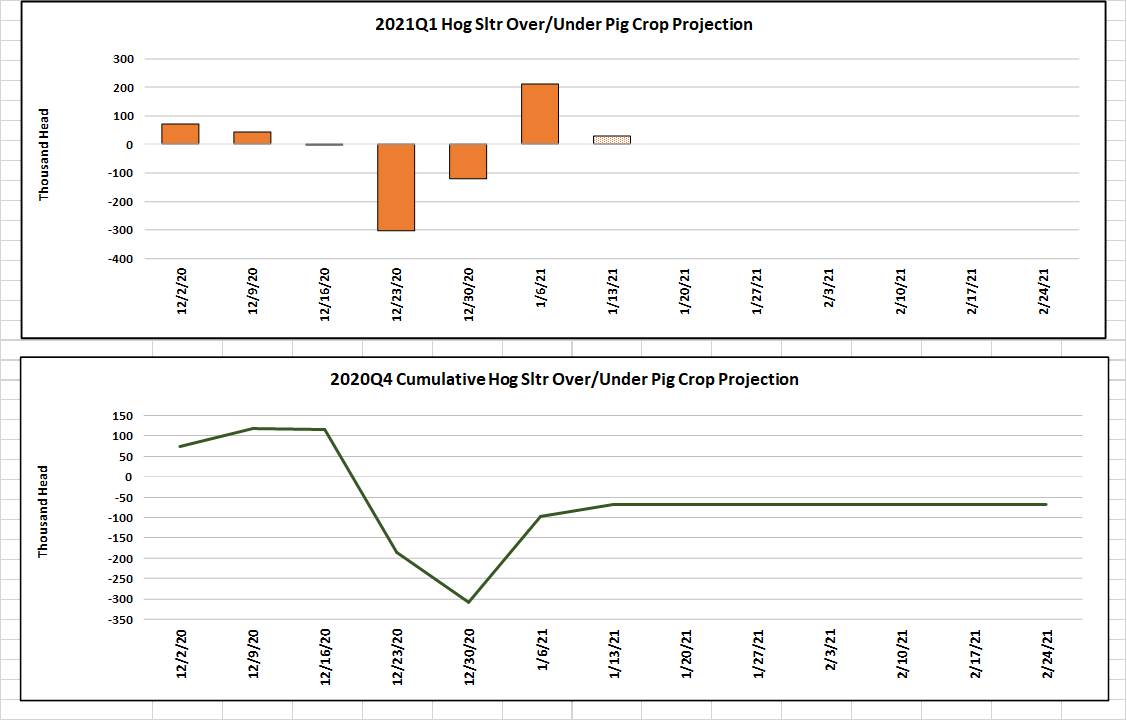

The first week of 2021 was rather quiet for the hog and pork complex. The cutout added a little over $2.40 on the week and the WCB cash market was up $2.74. So, things were generally moving higher, except for the spot Feb futures which lost over $1.50 on the week. Feb had gotten too excited on the last trading day of 2020, when it shot $2.67 higher. That was followed by a more modest gain on Monday, but since then the Feb contract has been slowly retracing its steps. Clearly, that trip up to $72 was excessive. The LHI is at $63.34 currently and has almost fully priced in the higher cutout in recent days as well as the stronger negotiated markets. It may have legs enough to reach $64 next week, but then what? In order for the LHI to reach the current level of the Feb futures, both the cutout and the negotiated markets will need to move a few dollars higher. That is possible, but Ifm not sure where the strength comes from. The move from the low $70s to $80 in the cutout was fueled by the bellies and hams as the chart below indicates. The belly primal has added over $30 in six trading sessions, so something is clearly going on there. Hams are a little stronger than they were in late December, but remain very volatile depending on how much boneless product gets sold on any given day. As I look across the other primals, Ifm forecasting most of them to work higher over the next few weeks, but my confidence in that forecast is shaky because Ifm seeing really large production in the next few weeks. Recall that USDA revised their estimate of the Jun/Aug pig crop up almost a million head. In early December I had noticed that the weekly kills were coming in larger than what the pig crop would suggest. Now after the revision, those early-December kill levels don’t look so out of line after all. The chart below illustrates this and also highlights how small the 2 holiday week kills were. This weekfs kill was enormous, registering 2.85 million head. The Saturday kill alone was 391k. Packers were able to piece together this huge kill without boosting the negotiated market too much. Maybe they are working to clear out some of their own hogs this weekend. If that is the case, then it could create a bit of an air pocket in the negotiated market next week. This big production will need to start clearing the market next week and it seems to me like it could weigh on the cutout. Traders are already somewhat disappointed that the cutout hasnft done better following the short kill weeks. Carcass weights have been running strongly over last year for most of the fall, but in the last three weeks of data, they have worked lower and are now only about 2 pounds over last year. Producer-owned hogs are still much lighter than packer-owned hogs at present. As with cattle, it seems strange to me that barrow and gilt weights dropped a pound in the week of Christmas. The IA/S. MN liveweight data doesnft show near the drop that the carcass weight data shows for December. Overall though, Ifd say the supply side is moderately bearish currently, mostly due to the big kill this week and the significant upward revision to the Jun/Aug pig crop. The demand side, on the other hand, looks pretty good. The combined margin has turned higher finally, and is now almost back to the zero line. It probably has several more weeks to move higher. Today, ERS reported November pork exports up 1.5%, which was quite impressive given how large last yearfs number was. With all of the holiday disruptions, it has been difficult to make much sense of the weekly export data in December, but I’m expecting Dec exports to be down about 6% when we get that data early next month. So the demand side looks moderately bullish. Supply bearish, demand bullish, hmmm, maybe the two will largely offset and we will get pricing not all that different from where we are now. Packer margins this week moved back out to $30/hd. Just 2 weeks ago they were at $15/hd. Look for packers to try and protect that margin better this time. If the cutout rises, then the negotiated markets can rise also, but if the cutout declines, packers are likely to try and take a few dollars back out of the negotiated hog market. The deferred futures were a little higher this week. Traders there are watching the corn market as it approaches the $5 mark. Theoretically, high grain prices can eventually cause producers to reduce production (either by scaling back the herd or reducing the feeding period) and that eventually results in higher hog and pork prices. In reality, the impact of corn prices on hog and pork prices is difficult to discern because there are so many other variables moving around. But, as long as corn is going up I think it is reasonable to assume there will be some upward pressure on the deferred hog market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}