Pork Wrap September 9

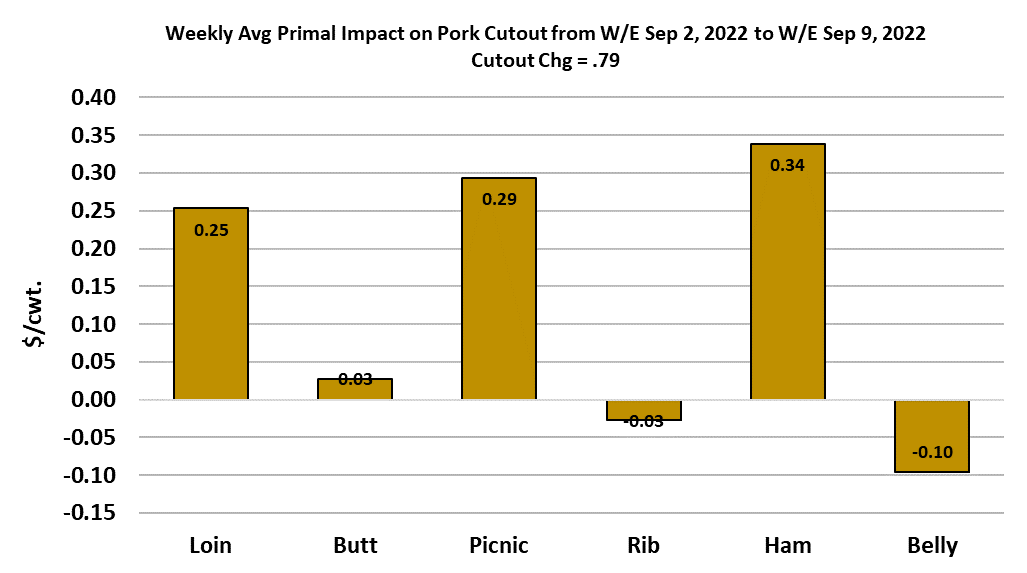

The pork cutout advanced a tiny bit this week, gaining $0.79 to

average $103.20/cwt. That gain stands in sharp contrast to prices in

the hog market, which were sharply lower. The WCB negotiated

market dropped $6.49/cwt this week and the LHI lost $5.80/cwt.

The LHI has now lost $15 in just 2 weeks. One might think that

would have futures traders shorting the Oct contract with both

hands, but I think they realize that the sharp drop in the LHI was just

a correction in response to the big drop in the cutout since late

August. In essence, hog prices are moving down to a level that will

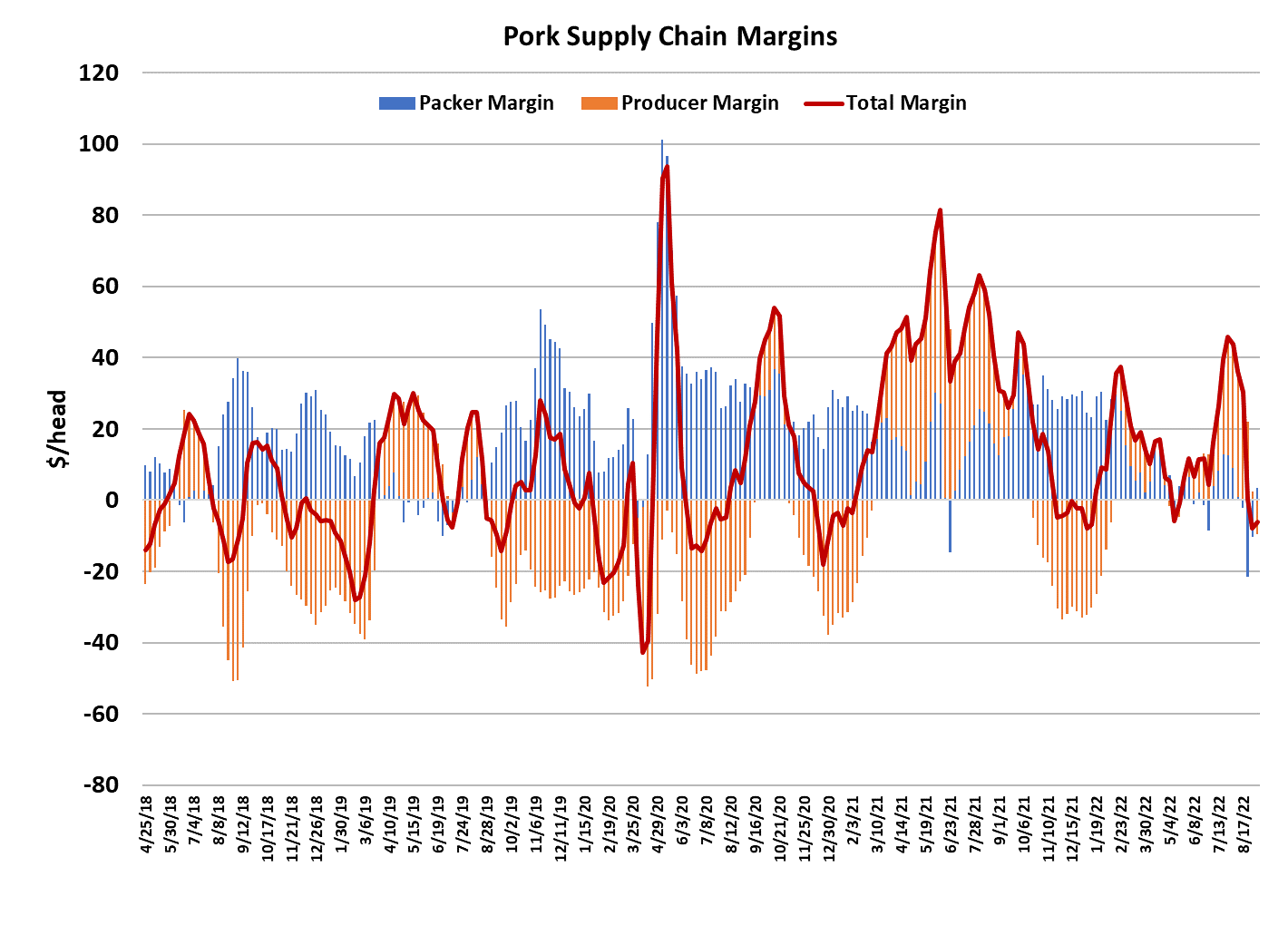

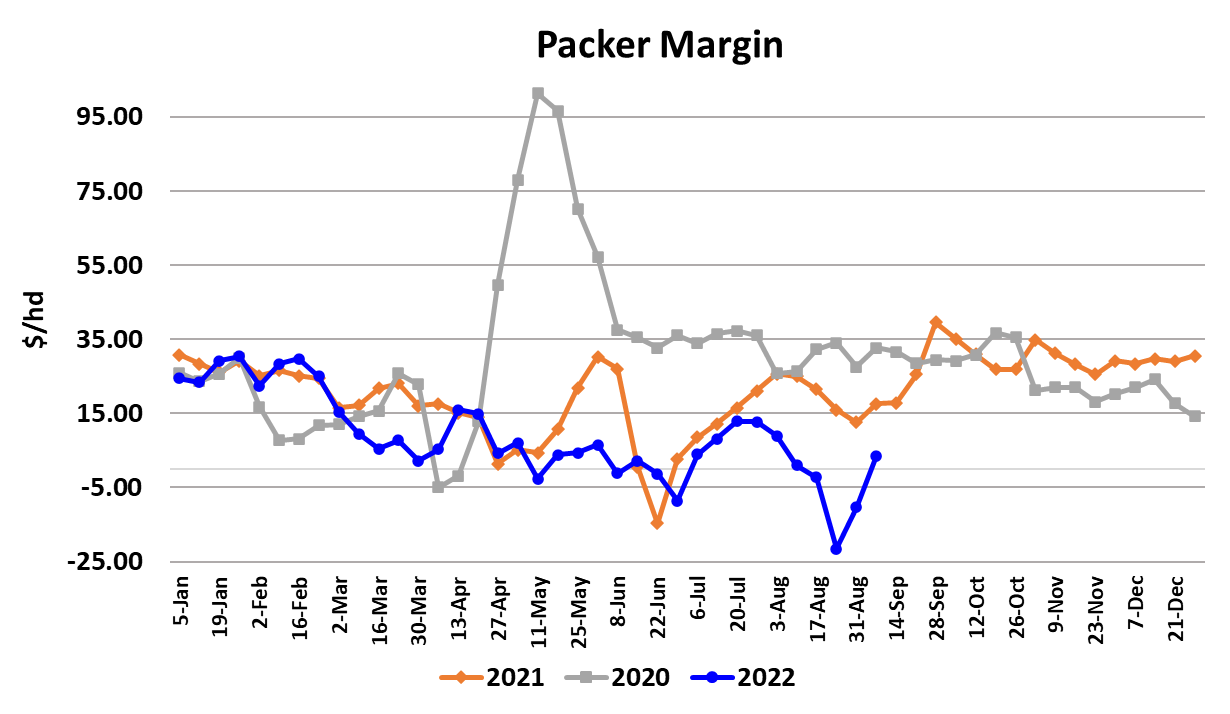

give packers a positive margin once again. I estimate this week’s

margin at about $3.50/head, which is a huge improvement over the –

$10/head margins they had last week. A typical packer margin at

this time of year is in the $10-15/head range and so the cash hog

markets might continue to slide until margins move to that level.

Most of that may be accomplished next week.

Why are futures traders not panicking then? I think it has a lot to do

with the cutout. It has been wallowing around in the low $100s for

almost 3 weeks now and there is a seasonal tendency for the cutout

to increase in the second half of September as buyers gear up for

pork month features in October. That, plus the fact that they are

seeing hams strengthen and bellies at such a low level that it seems

like some strengthening in that primal is eminent. That gave

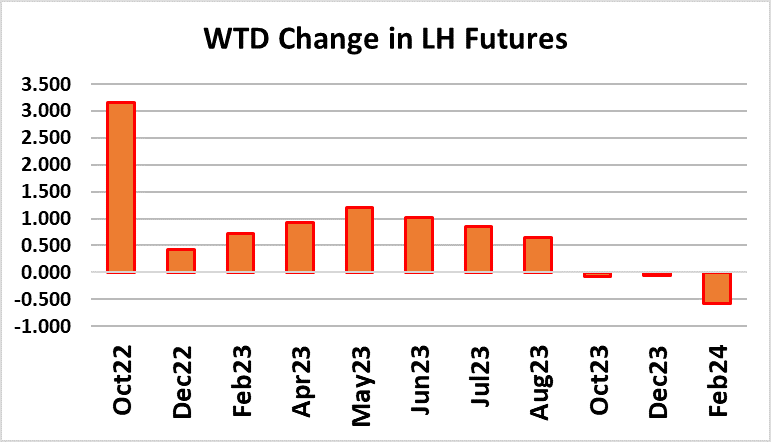

futures traders enough confidence to add a little over $3 to the Oct

contract this week. The shift in the basis has been dramatic.

Shortly after Aug expired and Oct became the front month, the

futures were trading at a $26 premium to the LHI. Today, that

premium is only about $6. Keep in mind that the Oct contract has

five weeks left to trade. After watching the basis narrow almost $7

per week over the past three weeks, traders now think that the basis

will only narrow about $1 per week for the next five weeks. That

seems pretty bold.

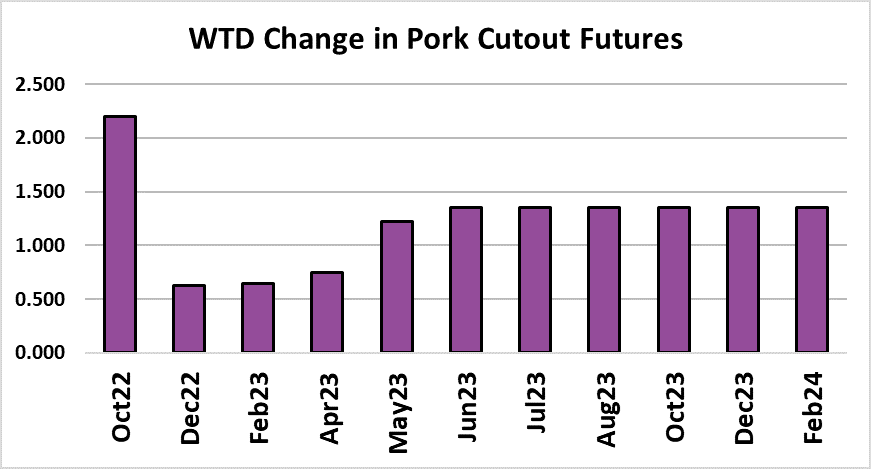

Last year at this time the basis for the Oct contract was almost $15.

The key difference lies in the cutout. Last year, in the second week

of Sep, the pork cutout was at $107 and the pork cutout futures for

Oct expiration were trading near $98. So, traders expected the

cutout to keep falling. This year, the pork cutout is at $103 and the

Oct cutout futures are also at $103, which means traders aren’t

looking for any further erosion in the cutout. That makes a big

difference to expectations for the LHI. Now, of course, traders could

be really wrong in assuming that the cutout will hold steady for the

next five weeks, but the current pricing environment for the primals

suggests that a steady, or perhaps even a modestly rising, cutout

between now and the middle of October is possible. It has been

very encouraging to see the ham primal turn higher and everyone

knows that it is very difficult to move the cutout significantly lower

without help from the hams.

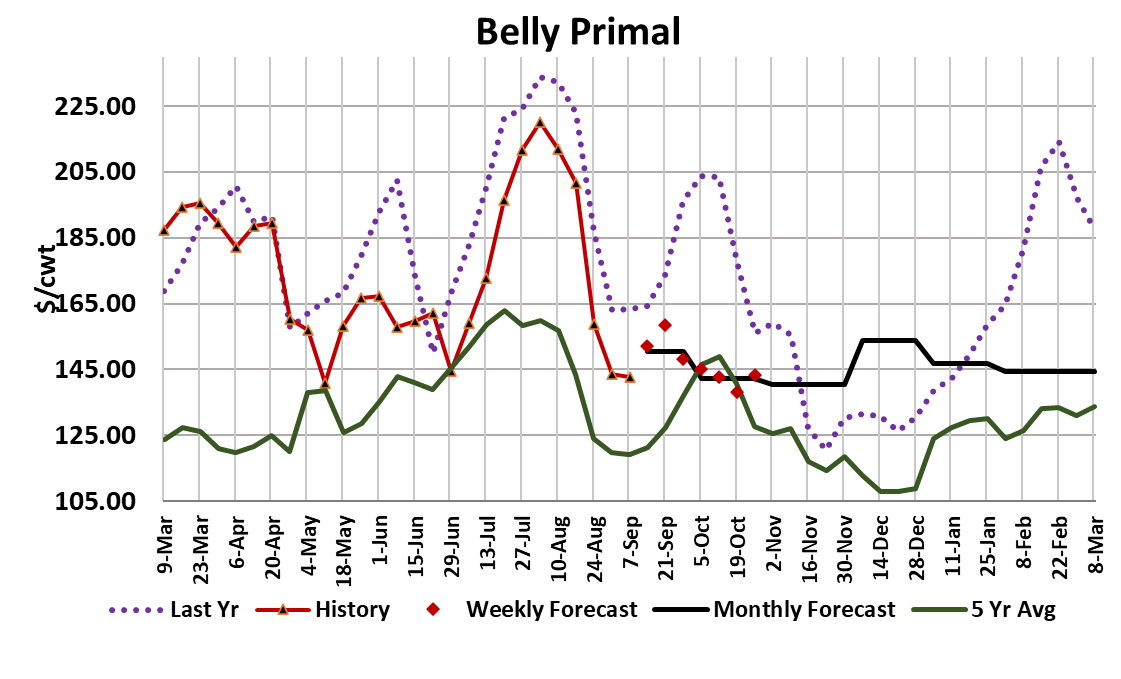

Bellies are the other big cutout mover and after freefalling the past few

weeks, the belly primal seemed to stabilize this week (down less than $1

from the week before). Everyone also knows that the one thing bellies

rarely do is stay flat. They are either moving up or down and often in a big

way. It looks like it is time for some recovery in the bellies and if that

happens then the cutout likely moves higher. My forecast has the cutout

inching back up to $105 or so over the next couple of weeks, mostly on

gains in bellies. Hams, I think are going to stall in the low $100s on the

primal, but not ease much in the near term. Eventually, the cutout will be

pressured below $100 as production increases seasonally, but I think it

stands a decent chance of remaining above $100 until near the end of

September. My call for the cutout at Oct expiration is around $96, so the

current level of Oct cutout futures is probably too high, but that might not

become evident for several more weeks. And, there is always the chance

that the bellies and hams will garner more strength that I currently have

dialed in and thus help move the cutout back toward $110.

We know that supplies will be increasing seasonally from now until early

December, so the real unknown is how demand will perform this fall. In the last couple of years we have seen strong demand surges around late Sep/early Oct and that may be part of what traders are counting on. The

combined margin ticked higher this week and is in the right zone to be

indicating a bottom. I want to see another week of data before declaring

the bottom is in, but it does look as though the market could be entering a

upcycle in demand soon. This week’s holiday-shortened kill registered

2.24 million head, with packers killing 317k on Saturday in an effort to make up some of Monday’s lost production. Next week’s full kill could be close to 2.5 million head, so there should be more product available and that is a big reason that I don’t have stronger cutout increases dialed in. However, once we hit that 2.5 million head mark, further slaughter increases should be relatively small and our peak slaughter in late November should be close to 2.6 million head.

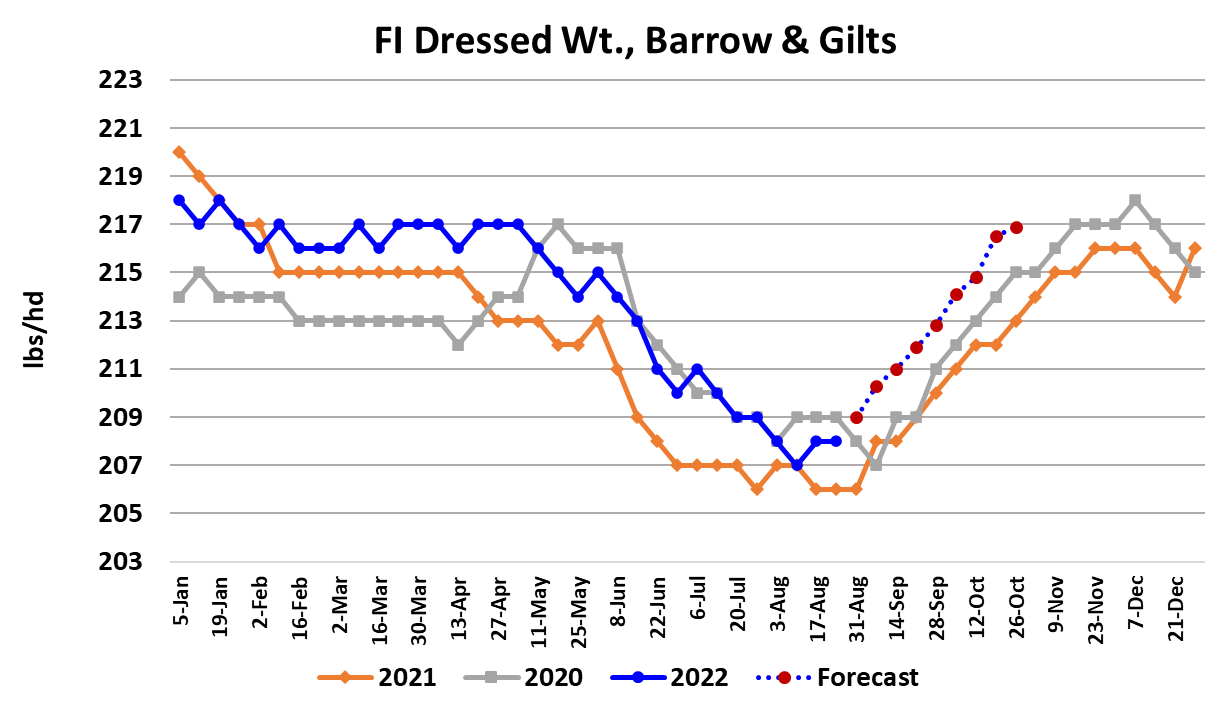

Hog weights are on the rise seasonally, but are not out of line with past

years and it doesn’t look like hogs are backing up in the pipeline. So, if

demand can hold up enough to get the market through the next couple of

weeks without serious concession in the cutout, then it will escape the

biggest escalation in supply. And, it is always possible that USDA overestimated the Mar/May pig crop like they did for the Dec/Feb pig crop that was killed this summer. The dark spot in the complex comes from

international demand, which is still struggling. The ERS export totals for

July were down almost 5% YOY and my guess is that August will be down

a similar amount. The slowdown from China has left a big hole in export

prospects. Next week, watch for signs of price recovery in the bellies since

that is the single biggest thing that could help the cutout and strengthen the bulls. Expect further weakness in negotiated prices as the market adjusts to provide packers with a more-normal margin for this time of year.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}