Pork Wrap September 6

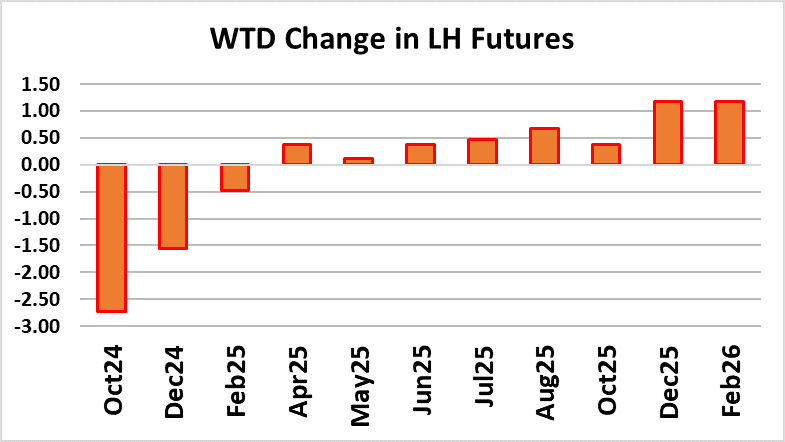

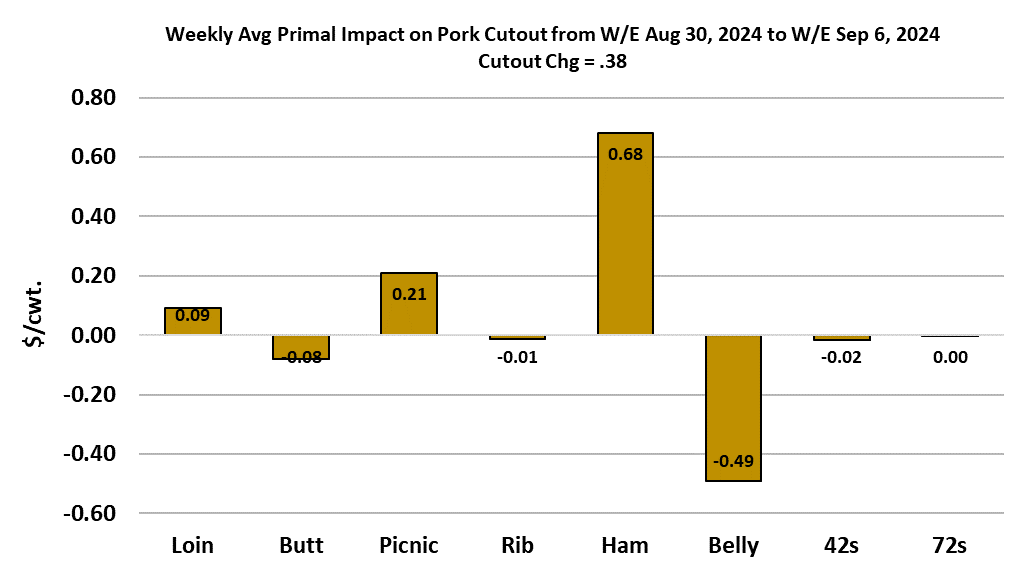

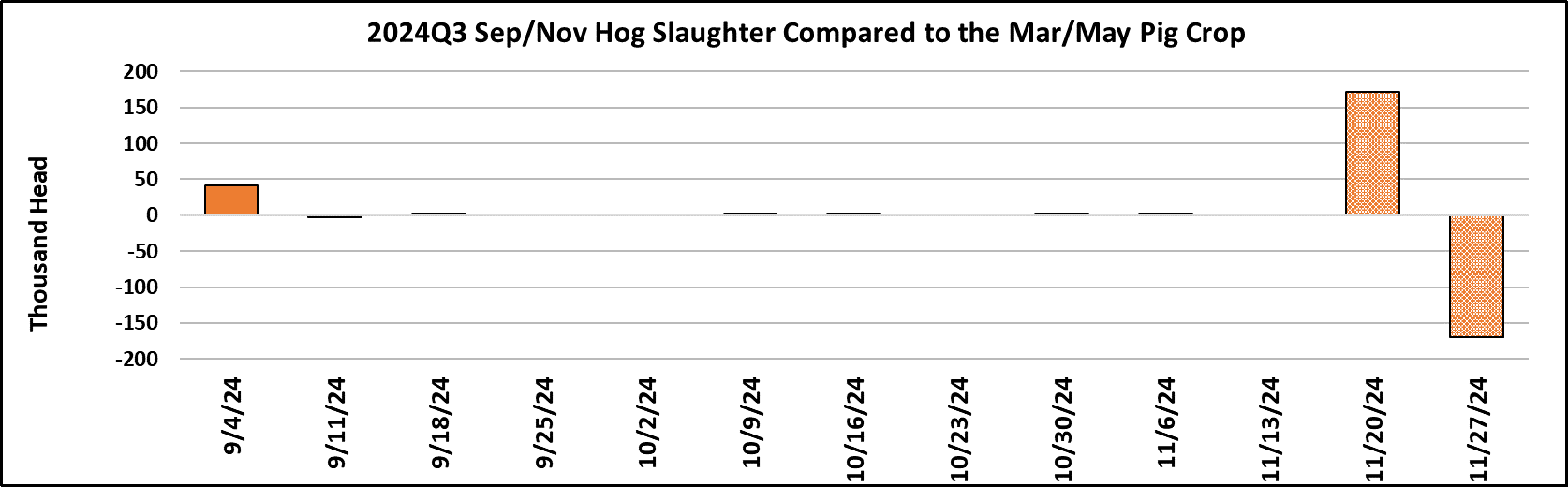

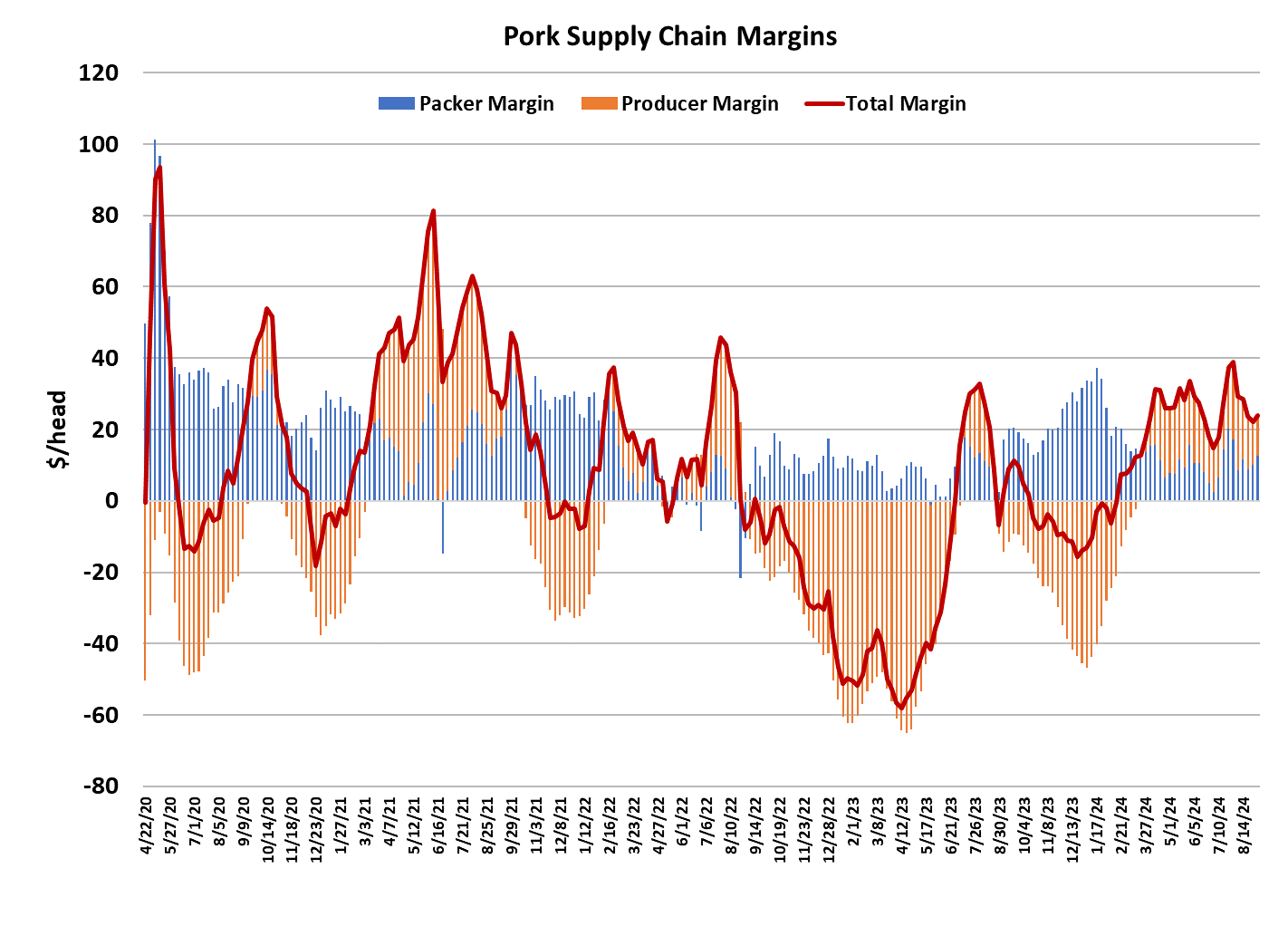

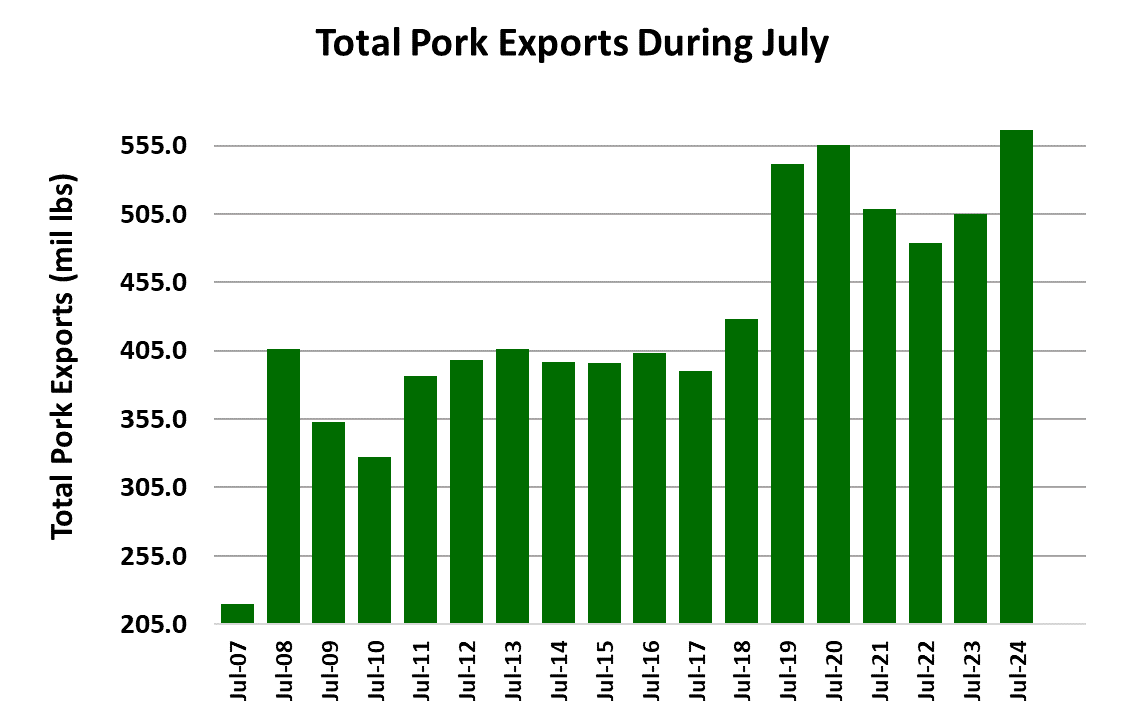

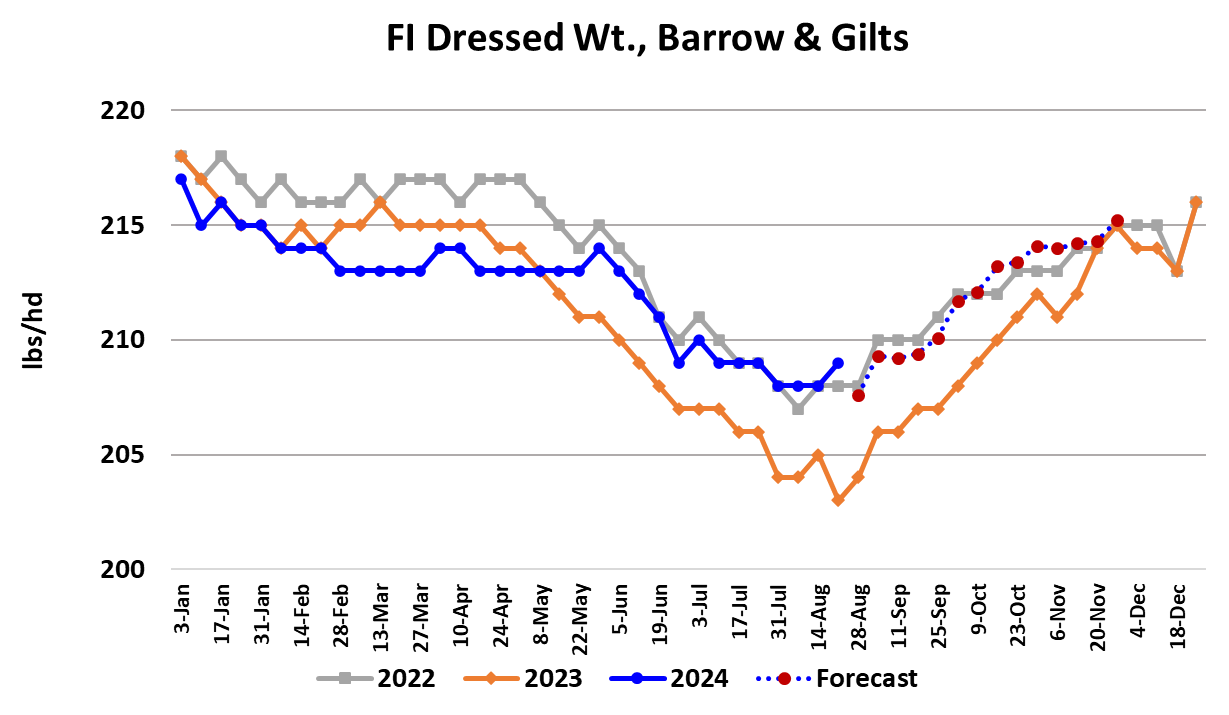

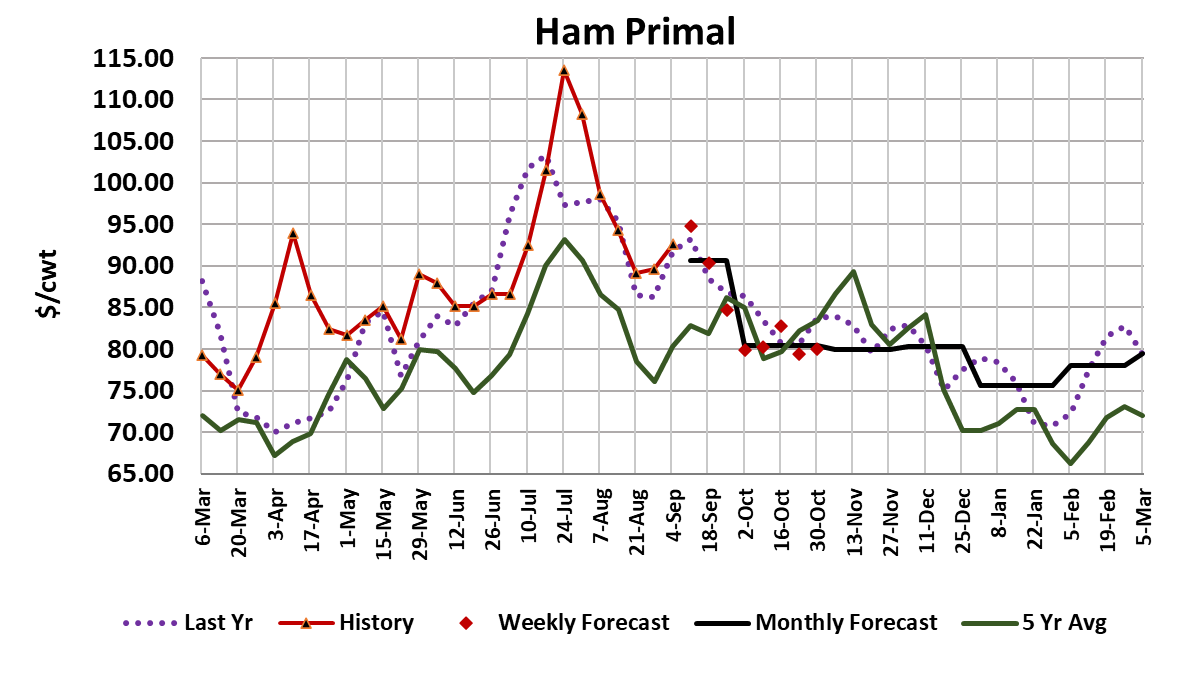

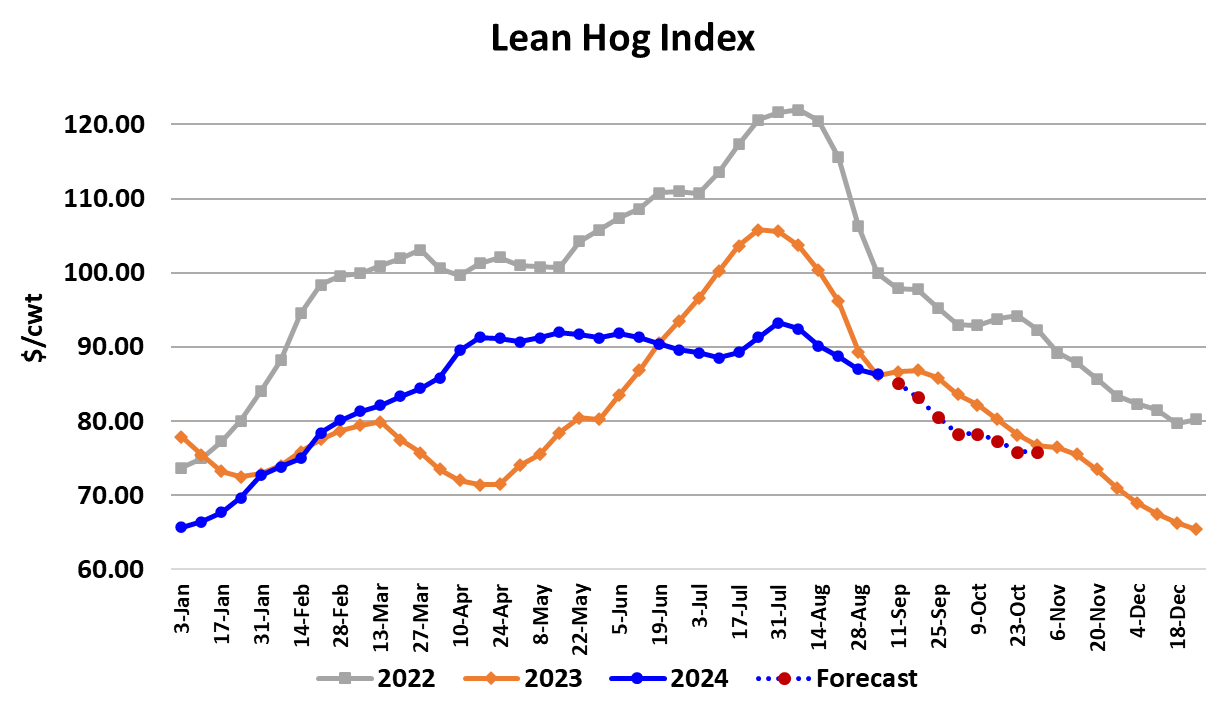

It was a flat week for prices in the hog and pork complex. The cutout gained $0.38/cwt as it averaged $96.27 for the short week. Cash hog markets were also steady, with the WCB negotiated price up only $0.05/cwt. In spite of this, the front month futures moved lower with the Oct contract dropping $2.73 in what was likely a correction from the sharp gains posted in the last couple of weeks. Traders just got a little carried away with the buying and had tightened the basis up too much for the amount of time remaining until expiration. After this week’s action, the basis is now back to +$6 (cash over futures), which is more in line with historical norms. However, given that the cutout was actually higher this week, there is risk that the buying interest will emerge once again if prices in the pork market don’t show some easing early next week. This week, the bellies softened a bit, pulling downward on the cutout, while the hams strengthened almost enough to offset the damage done by the bellies. The retail items are holding up better than expected and that has prompted me to raise the near-term forecasts for those items somewhat. In a surprise move, the 42% trim was up almost $5 on the week and the 72% trim was almost unchanged. That may reflect renewed interest from processors after the holiday as they refilled their raw material pipelines. Packer margins increased to $12.60/head, up from around $10 the week before, but are still a bit below normal for this time of year. Going forward, we should continue to see good gains in packer margins and they will likely cross the $20/head level by the middle of October. Producer margins are in the process of easing seasonally, but they dropped only marginally this week and are now near $11/head. The combined margin ticked up a little this week, but I’m not ready to call it higher in the near-term. My guess is that once the industry gets back to full production next week, producer margins will start to move lower at a quicker pace and that will renew the downward pressure on the combined margin. I do believe that demand is slowly fading a bit here in early September, but this week that was probably masked by the small production as a result of the holiday. Speaking of small production, this week’s kill clocked in at 2.33 million head, which was a little larger that what I was forecasting coming into the week. Packers managed to put together a very strong Saturday kill at 395k. Next week, we can expect the daily kills to run close to 485k during the week and there should be enough slaughtered on Saturday to bring the weekly total close to 2.54 million head. That sharp increase in production is likely to put some downward pressure on most cut prices, but if it doesn’t take at least a couple dollars off of the cutout, I’d consider that a strong demand signal and a bullish indicator for the futures, which seem to be anticipating some renewed softening in the cutout. Barrow and gilt carcass weights bumped a pound higher this week in what was likely the first step in the seasonal turn higher. The forecast has carcass weights gaining about 6-7 pounds over the course of the fall and early winter until they plateau near the end of the year. If I’m wrong, I may be under-estimating how much weight gain will come about due to cooler weather and freshly-harvested corn being introduced into rations. Harvest is just getting underway in the Midwest and it looks like this will be a bumper crop that could result in sub $4/bu pricing for the first time since 2020. As a result, producers will have a strong financial incentive to put a few extra pounds on hogs this fall. The international trade data for July pegged US pork exports at 567 million pounds, which was a 12.3% gain over last year. Before we get too excited about how strong exports are, it is important to consider that the pork cutout during July was 7.2% lower than last year and $17-22/cwt lower than in 2021-22. As a result, we shouldn’t be too surprised that lower prices encouraged stronger purchases from overseas. The forecast has total pork exports continuing to run stronger than last year for the next several months, but the YOY percentage change is likely to run in the low single digits and by the time the end of the year arrives, I’d look for 2024 exports to clock in about 3-4% better than in 2023. Thinking about price movements during September, it is logical to expect lower hog and pork prices as a result of weekly kills expanding rapidly. However, often times it doesn’t work out that way and in some years we have actually seen prices increase over the course of September. That seems to be more likely in years like this one where the summer market never got very heated price-wise. Slaughter in August fell well below what the prior pig crop projected and if that continues in the fall, it will be price supportive. This week’s kill was a little larger than what the pig crop suggested, but I want to see more weeks like that before I conclude that USDA didn’t over-estimate the pig crop that the industry is now slaughtering. Next week, look for the cutout to be down a couple of dollars and negotiated hog prices to be off $2-3/cwt.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}