Pork Wrap September 30

The hairline cracks in pork demand started to grow a little bigger

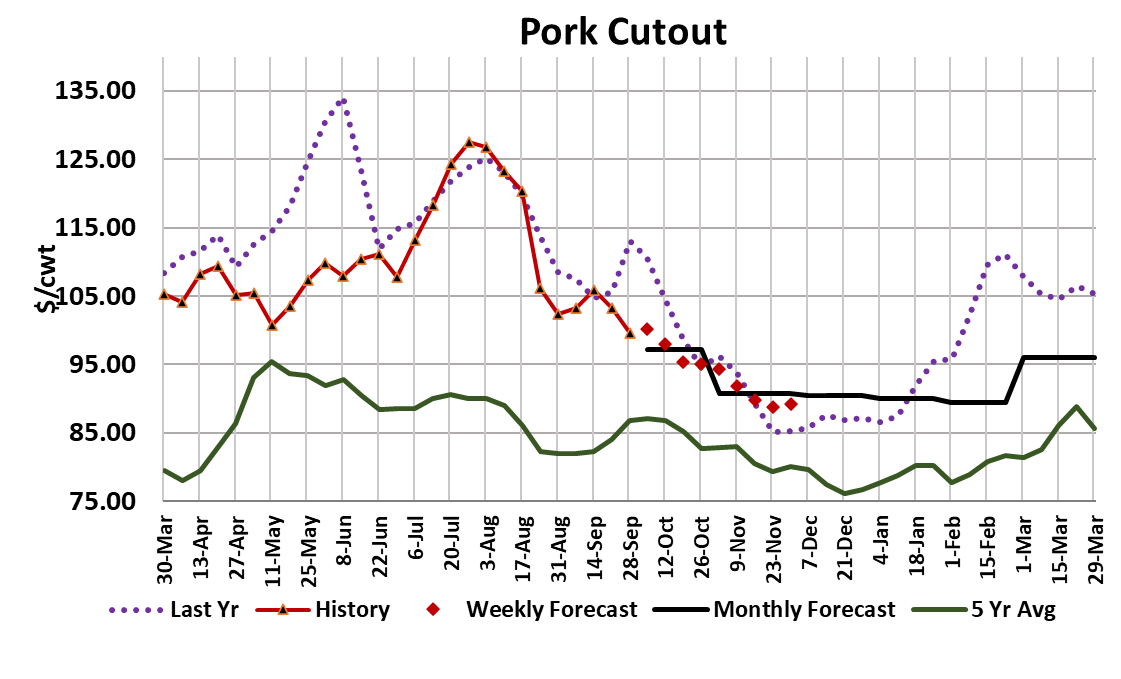

this week. The pork cutout dropped $3.68/cwt. to average

$99.53. That is the first sub-$100 cutout since the first week of

February. As is typical, the negotiated hog market followed the

cutout lower, and the NDD market lost $2.27/cwt. All of that

hasn’t yet been reflected in the LHI, so packer margins

compressed quite a bit, now close to $6.50/head, down from $10/

head last week. Once the LHI fully incorporates the decline in

the cutout and negotiated markets, I expect that packer margins

will move back over $10/head next week. The weakness in the

cutout was largely driven by lower belly pricing, with some help

from softer ham prices. Bellies just can’t seem to get any

traction. At the end of the week the belly primal was printing

$112/cwt., which was the lowest daily value since New Year’s

Eve, 2020. I guess that is a pretty solid sign that the elevated

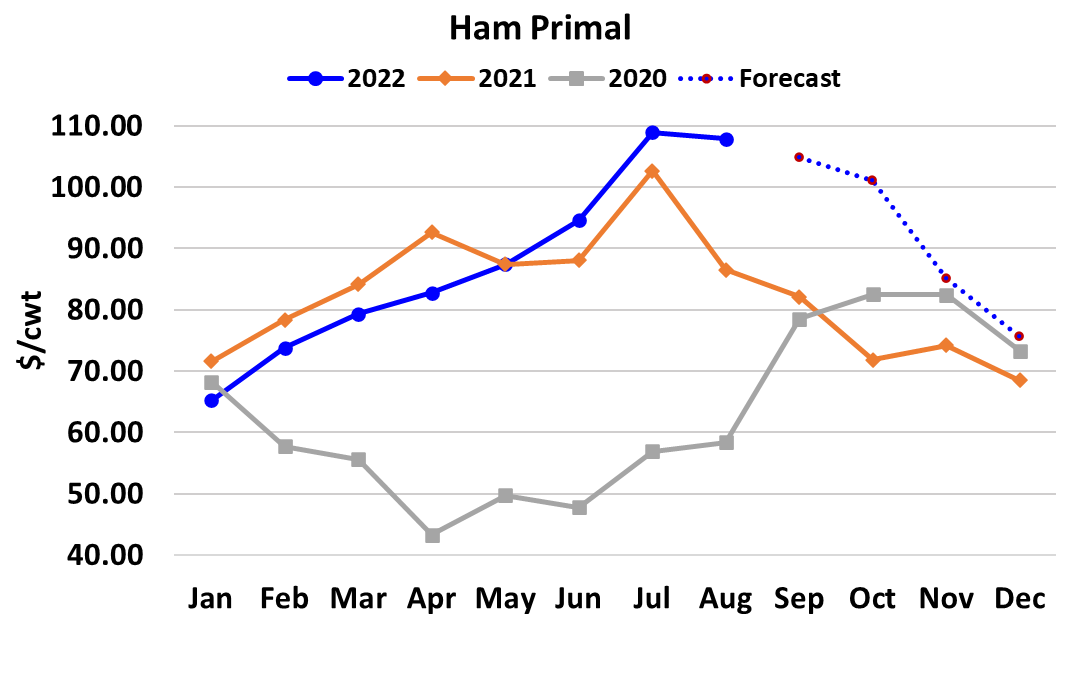

demand from the pandemic years is dissipating . Ham pricing

has remained very strong compared to the other parts of the

carcass, but even that has its limits apparently.

The primal printed down $1 on a weekly average basis, but bonein hams were starting to stumble near the end of the week. Even

the retail primals were looking a little shaky at times this week.

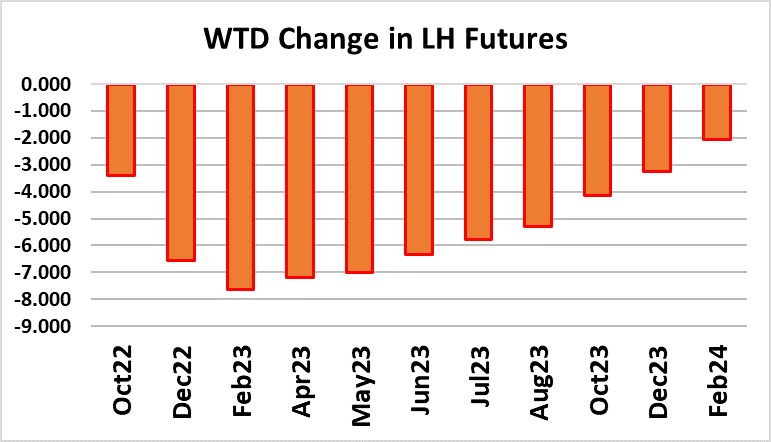

The futures market did not like any of this, and we saw the Dec

contract lose over $6/cwt this week. The more deferred issues

lost even more. All of this demand softening was happening

against the backdrop of worsening macroeconomic indicators

which fostered big losses in the stock market. That certainly

won’t help consumers to feel better, or spend more on pork. The

combined margin continued lower this week and if we look

closely at the chart, we see that prior to the pandemic years, it

wasn’t unusual for a demand downcycle to reach -$20. It looks

like that is where we may be headed again. Another sign that

demand isn’t what it used to be.

So where does the cutout go from here? Bellies are certainly

long overdue for a rally, so maybe that will materialize next week

and help lift the cutout some. Hams don’t look like they have

much gas left in the tank, so bellies or the retail primals will need

to step up if the cutout is to recover. More likely, growing

production and softer exports continue to slowly press the cutout

lower. The fundamental forecast since the end of August has

had the cutout hovering in the low $100s and then stepping down

through the $90s during October. Everything seems to be going

according to plan. I don’t think that we are going to see

widespread demand improvement across the carcass that lifts

the cutout higher.

Instead it will probably be more like whack-a-mole where one primal

pops up for a bit but that gets offset by weakness somewhere else. The

end result is a cutout that slowly fades lower under the weight of

seasonally-increasing production. The fundamental forecast has the

cutout working from near $100 today down to the mid-to-high $80s by

the end of November. This week’s slaughter came in at 2.53 million

head, which was almost dead-on with what the pig crop predicted. By

early November, kills should be running close to 2.6 million head per

week. That would be about 1.5% below last year, but keep in mind that

weights are a little heavier than last year, so actual pork production

might not be down that much. Further, softer export markets this year

compared to last and the prospect for a much stronger dollar to attract

bigger imports, raises the possibility that pork availability might be nearly

as large as last year. We got our first look at hog supplies for the Dec/

Feb quarter this week when USDA released the results of its Hogs &

Pigs survey. The Jun/Aug pig crop was reported 1.1% smaller than last

year, so we should expect slaughter during the Dec/Feb quarter to

be down a similar amount.

USDA reported the total US swine herd down 1.4% and the breeding

herd down 0.6% YOY. So the industry is still slowly contracting. If

producers didn’t expand much during the boom times of the pandemic,

there is little reason for them to expand now that the good times are

coming to an end. USDA’s survey results were only a tiny bit smaller

than what I already had dialed into my models, so the impact of the

report on my price forecasts for 2023 was minimal. Barrow and gilt

carcass weights were flat at 210 this week, but they should be up

another pound in next week’s data release. There is still nothing in the

weight data that raises concerns about producers not keeping up

with their marketing schedules.

However, because the number of market ready hogs are the

largest of the year during Q4, packer leverage increases over

producers and we should expect to see packer margins grow and

producer margins shrink. That means that if the cutout struggles,

packers have more power to push cash hog prices down in order to

compensate (more power than they would in say, the summer).

Although I fully expect packer margins to grow as we move deeper into

Q4, I think they will be a bit smaller than last year because last year

packing capacity was constrained by labor availability and this year the

labor situation is much better. That means we have more capacity

chasing fewer hogs and thus margins should be a narrower than last

year. Next week, watch for some further slippage in the cutout unless

the bellies rebound significantly. Also look for a bit of a rebound in the

futures if the fear can fade a bit and traders come to realize that they

might have overdone it to the downside this week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}