Pork Wrap September 03

The hog and pork complex continued on its downward trajectory this

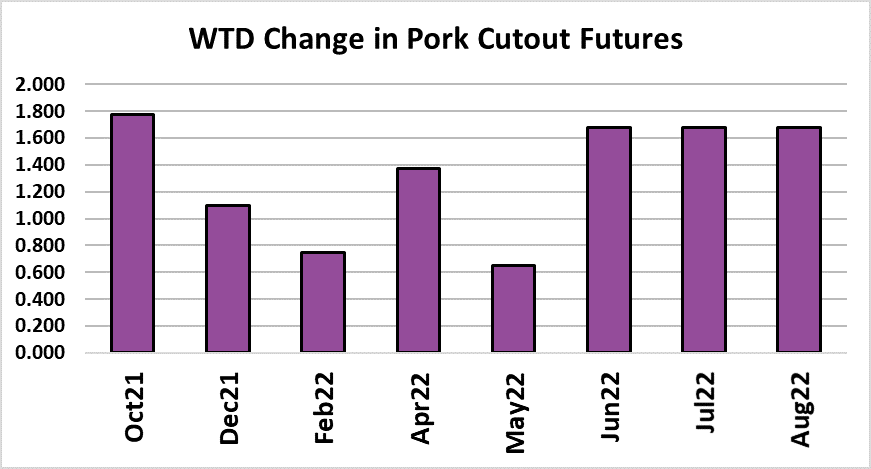

week with both the cutout and negotiated hog prices dropping

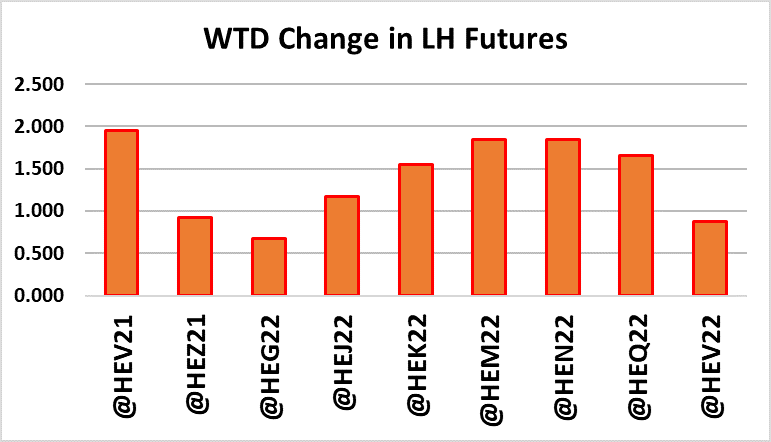

approximately $5 on a weekly average basis. Meanwhile, the nearby

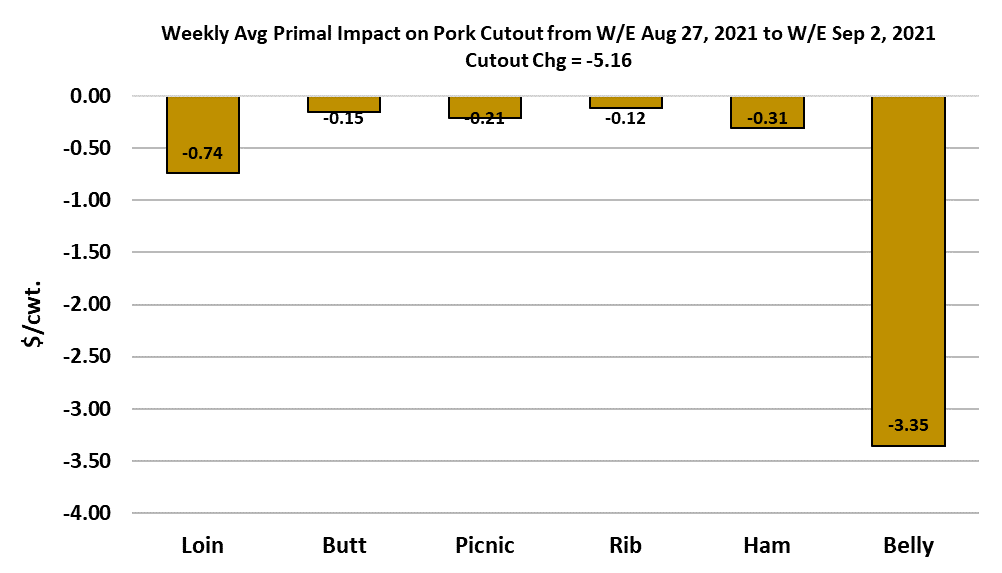

futures rose $2. Go figure. The problem in the cutout seems to be

almost entirely limited to the bellies, with the other primals holding about

steady on the week. Maybe that is why the futures market is reluctant

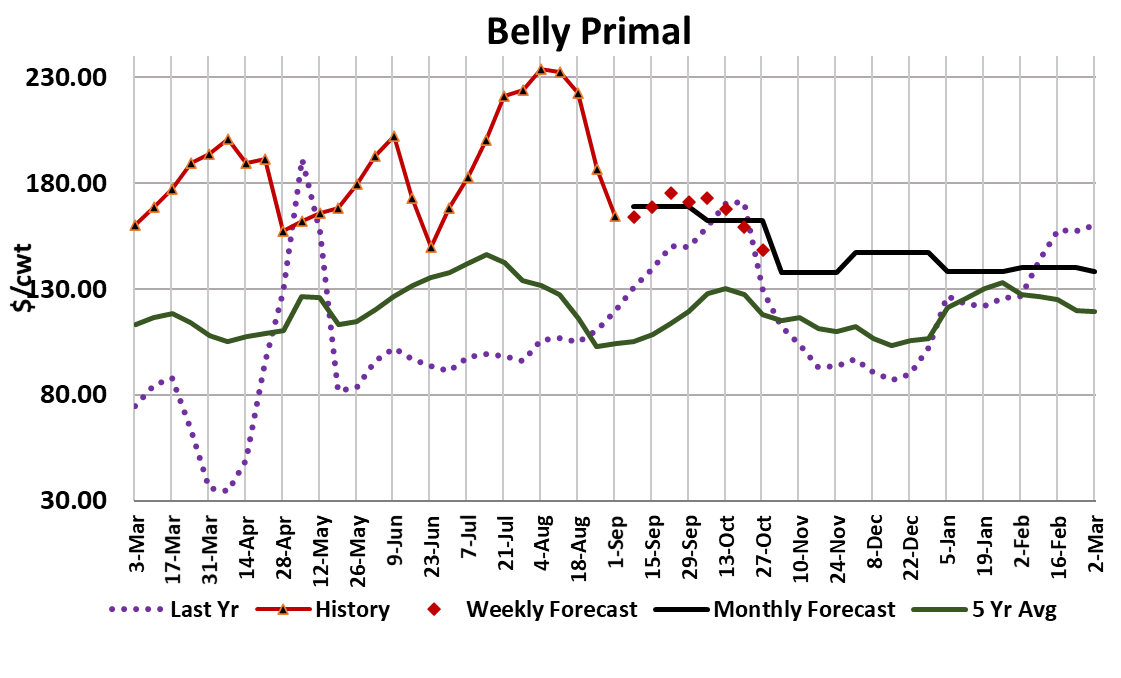

to follow the cutout lower. Traders know that bellies can turn on a dime

and normally downward belly price corrections happen over a period of

2-4 weeks and the move is often dramatic. The current down move in

bellies just completed its fourth week and is very close to the level where

the bottom was made back in the great June belly sell-off. After selling

off for a few short weeks, bellies often spend many more weeks grinding

higher before a new top is made. Maybe traders are banking on that

pattern repeating itself now.

My problem with that is that pork supplies are about to undergo a rapid

expansion moving from Labor Day to Halloween. That makes it much

tougher for any part of the carcass to post a stout rally. It is easy to rally

bellies in June when hog supplies are near their tightest, but it is a whole

different deal in the fall when supplies are growing week after week. My

guess is that bellies are approaching a near-term bottom, but the rally

phase won’t lift prices all that much. The bigger risk is that the other

primals start to come under pressure as supplies grow. The weather

forecast across the US for the upcoming Labor Day weekend looks quite

good although we need to keep in mind that some areas of the country

are struggling under the devastation wrought by Hurricane Ida, so those

areas probably won’t see much in the way of retail pork clearance this

weekend. Other parts of the nation probably will see good clearance.

Packers are expected to keep the kill light on Saturday in order to give

more employees a three-day weekend. That, in combination with

Monday’s no-slaughter, will tighten up pork availability early next week

and could result in a short-term bump in the cutout, but packers are very

likely to make up a good chunk of the lost production with a very large

Saturday kill the following week.

Anyone needing immediate ship product for next week is likely already

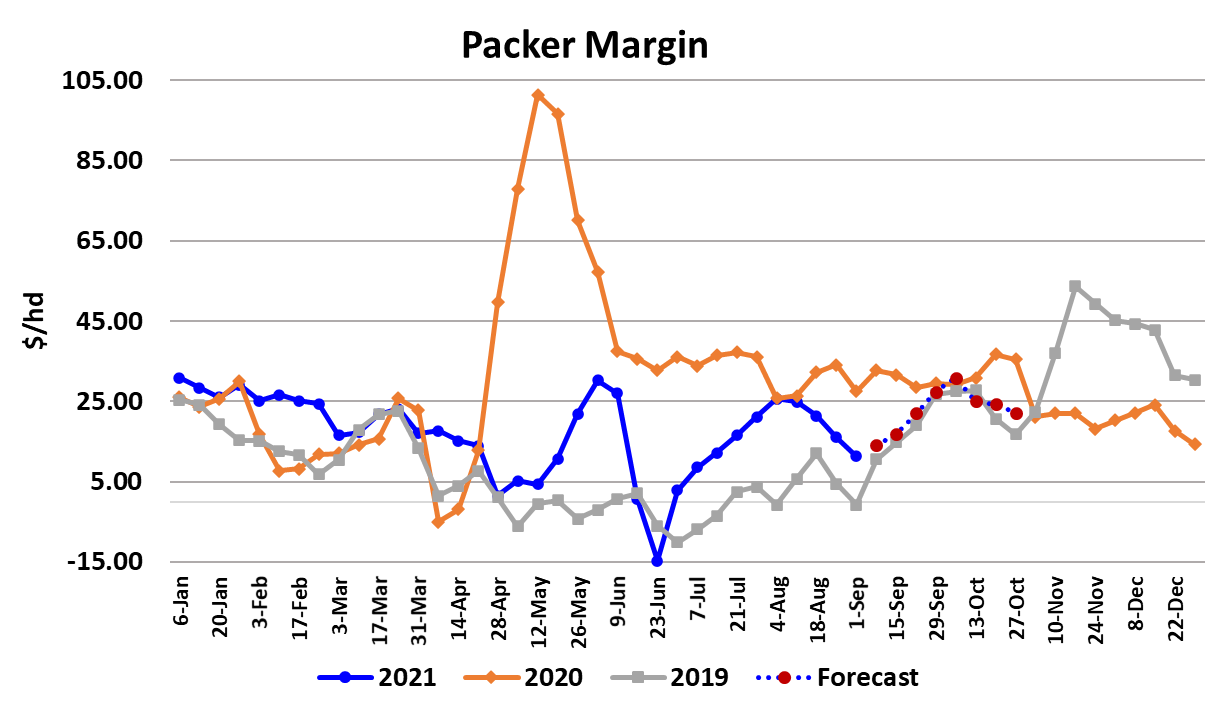

factoring that in. Packer margins fell $5 this week and now stand at just

a little over $11/head. I don’t think that packers are very happy with that

and thus will likely try to increase the pressure on cash hog prices next

week. Negotiated hog markets have lost over $10 in the last 10 days.

Some hogs will back up during the short kills ahead and that will make it

easier for packers to buy them lower next week. Barrow and gilt

carcass weights were reported down a pound to 206 pounds today.

That likely marks the 2021 bottom in weights are they should start to

trend strongly higher over the next few weeks as cooler weather and

freshly harvested corn ramps up their appetite.

The DTDS weights are still relatively low however, which suggests

that there is not any meaningful backup of hogs in the supply chain

at present. Hog producers are hoping that packers can find and

keep enough labor in their plants to get all of this fall’s hogs dead on

schedule. We will be watching the DTDS closely throughout the

balance of the year for signs that hogs are backing up. My sense is

that packers and/or second stage processors have already found

some additional labor or at least shifted some existing labor into

more value-added production over the past few weeks. The

difference between the core cutout and the printed cutout has

narrowed considerably since the middle of August and that tells me

that more value-added product is being produced and thus clearing

the market at lower prices.

Another piece of evidence in that direction is the price of pork 42s,

which have been falling like a rock lately. This afternoon they printed

$67 after being over $150 just two weeks ago. More value-added

processing means more trim production and that could at least

partially explain the rapid decline in trim prices. There is probably

also a demand-side effect as demand for products made with trims,

such as hot dogs, typically declines after Labor Day. I don’t want to

give the impression that pork demand is falling apart, because that is

not the case. Just the fact that we have a cutout over $100 at Labor

Day is an indication that demand remains way stronger than normal.

Beef prices are now declining and that retreat could accelerate

through September. That would weigh on pork prices also. The

weekly export numbers for pork continue to point toward a dismal fall

on the export side of the business.

China is no longer the roaring giant that it has been for the past

couple of years. A significant loss of export business this fall has the

potential to push prices lower even if domestic demand remains

strong. There are now several other countries that can land pork in

China well below the price that the US can achieve. I think that we

are going to be looking at a pork market this fall that slowly erodes,

but stays relatively high by historical standards. There will be some

brief updrafts in prices and post-Labor Day may be one of those, but

in general I’d expect the price depressing effect of growing pork

supplies and softer exports to outweigh any price enhancing effects

of strong domestic demand. Next week, watch those bellies because

as the bellies go, so go the cutout.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}