Pork Wrap September 29

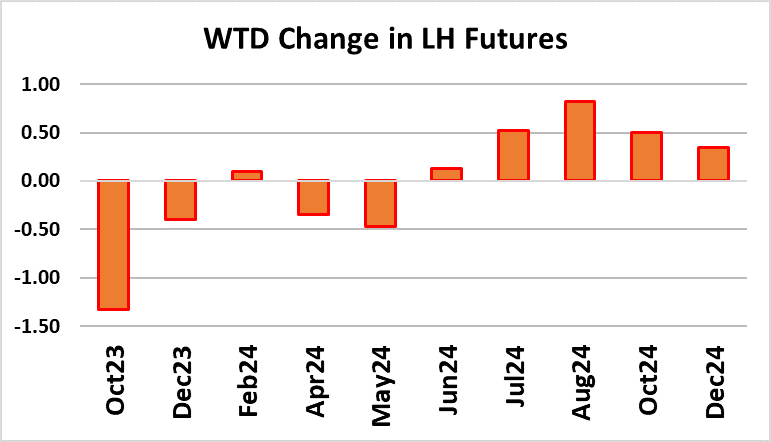

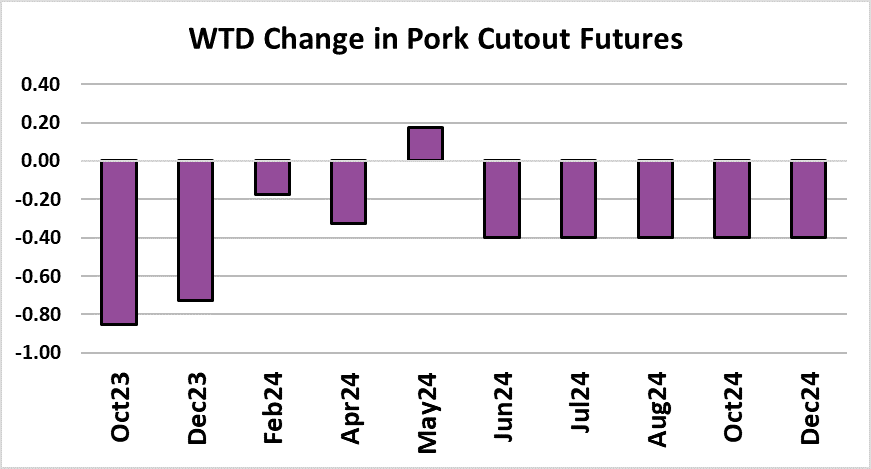

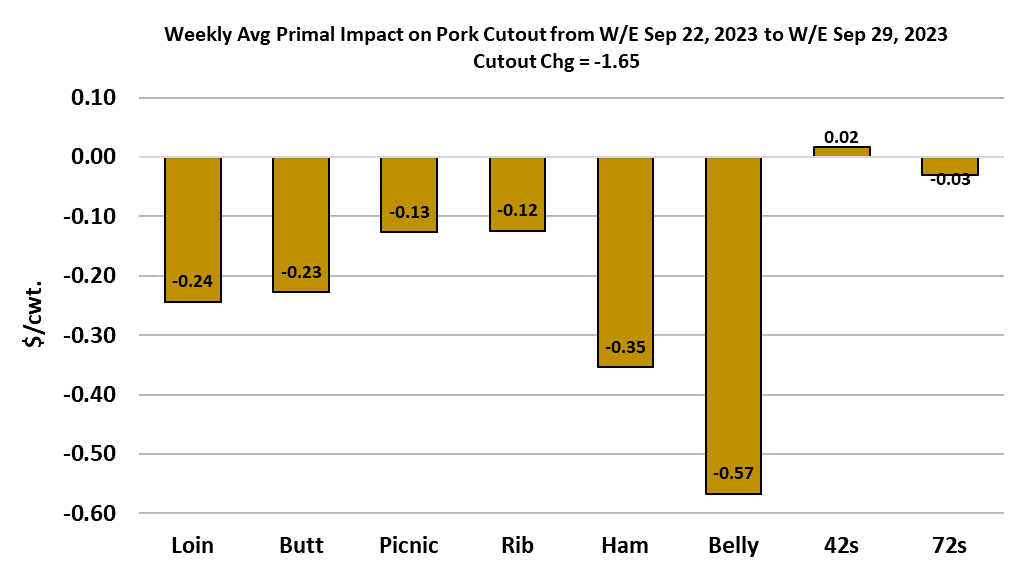

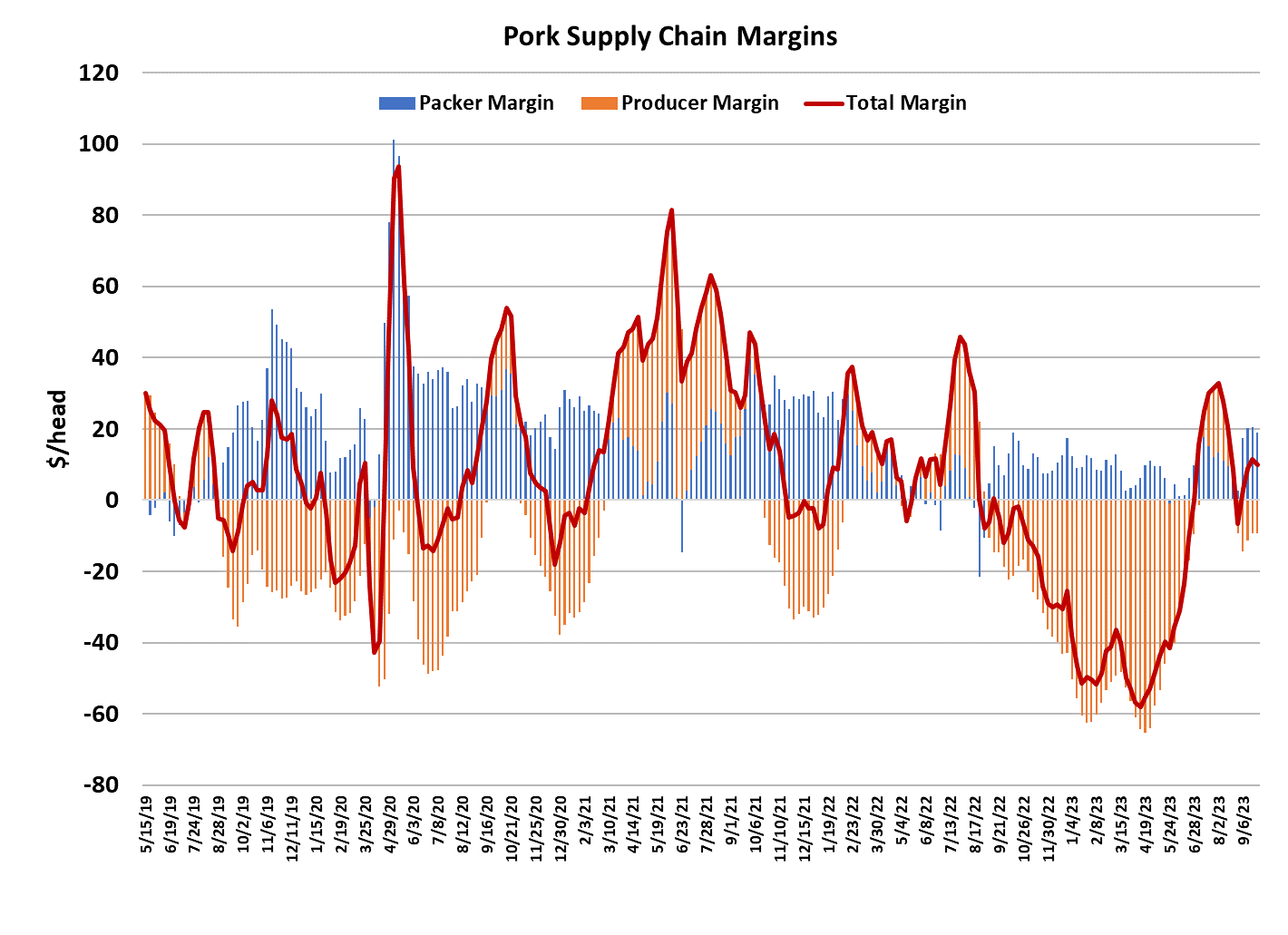

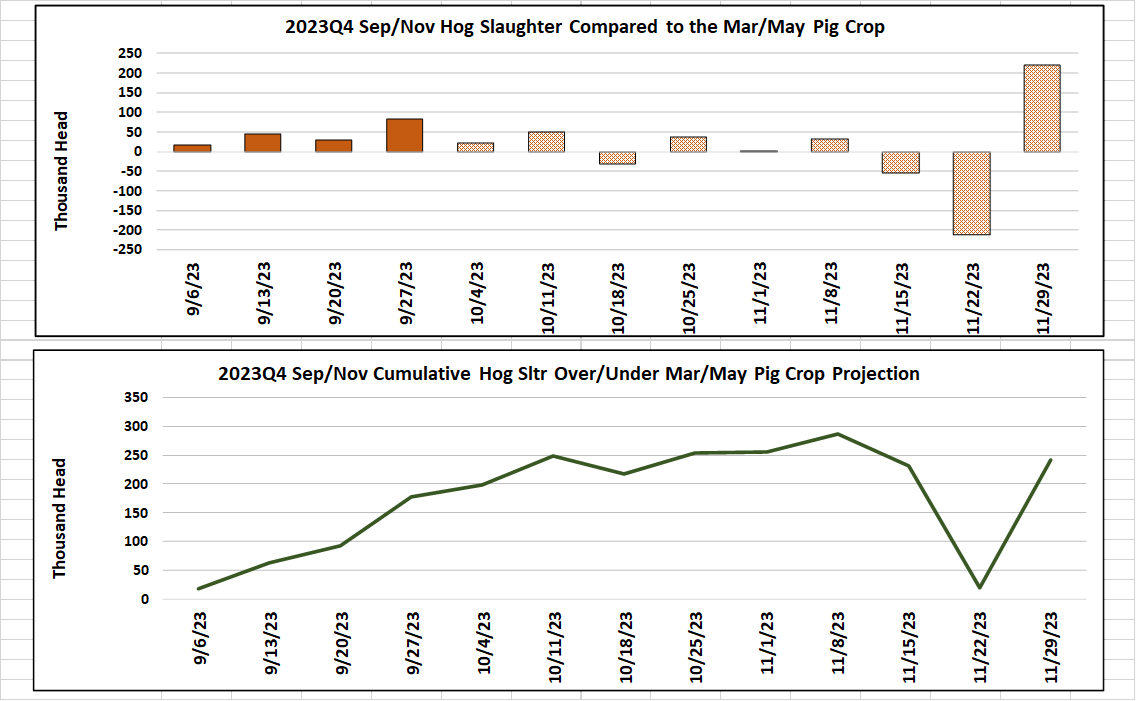

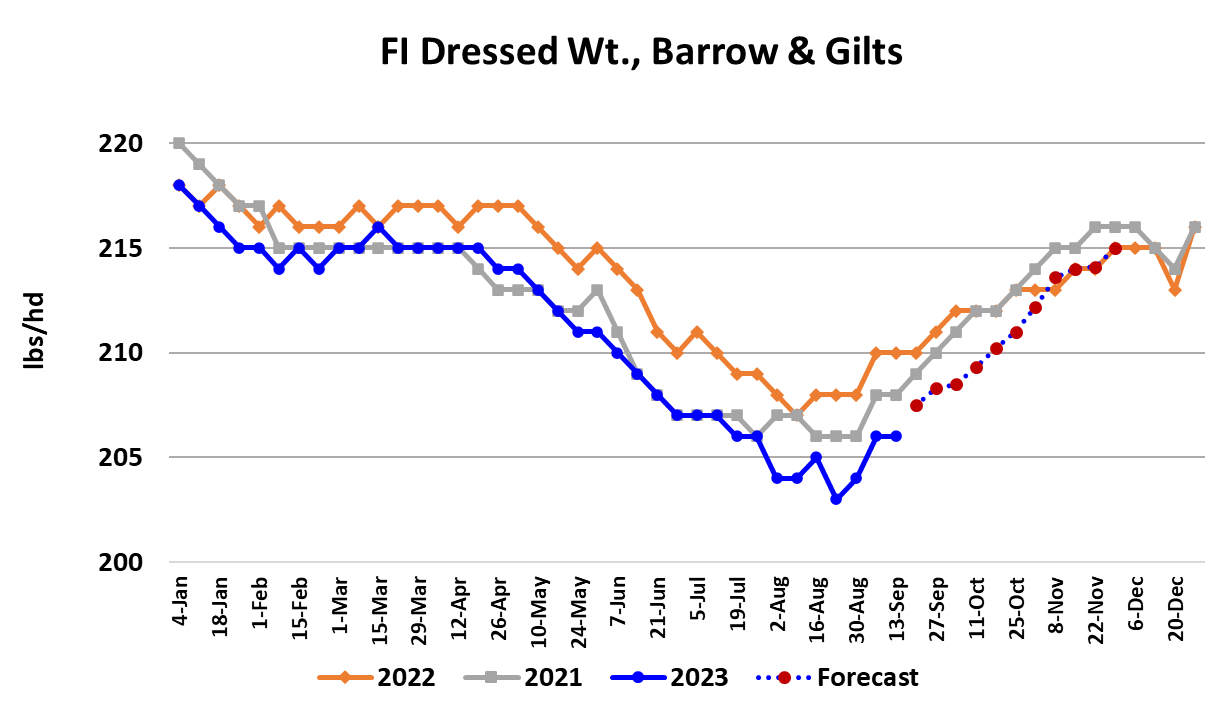

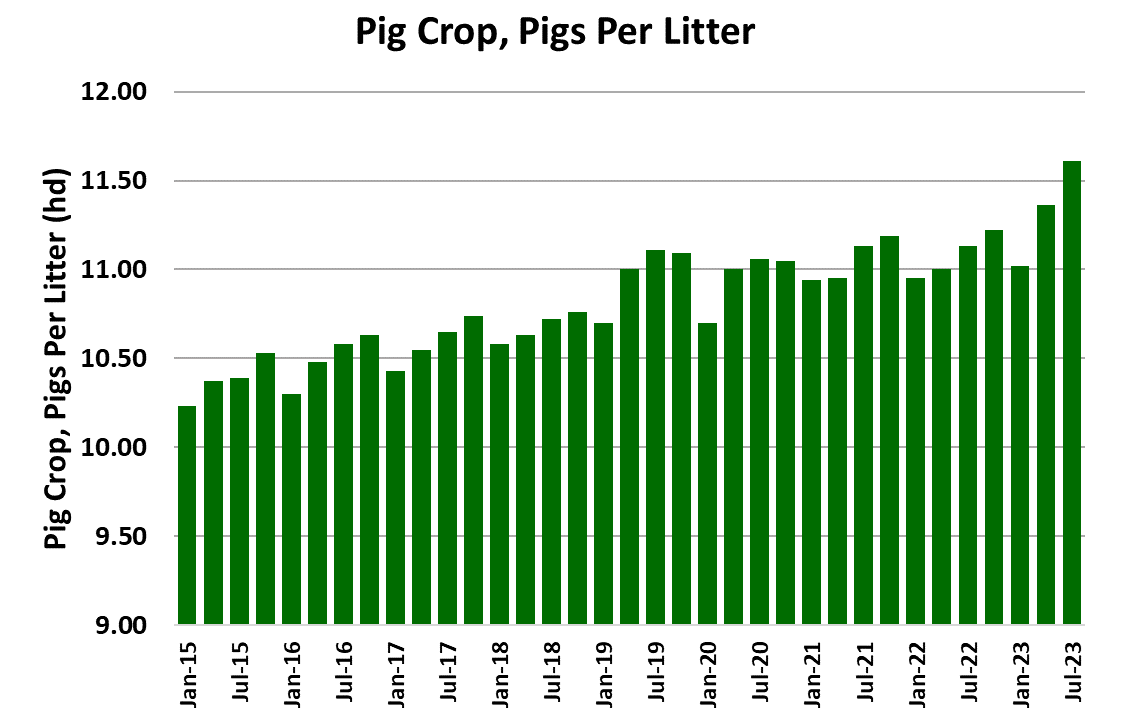

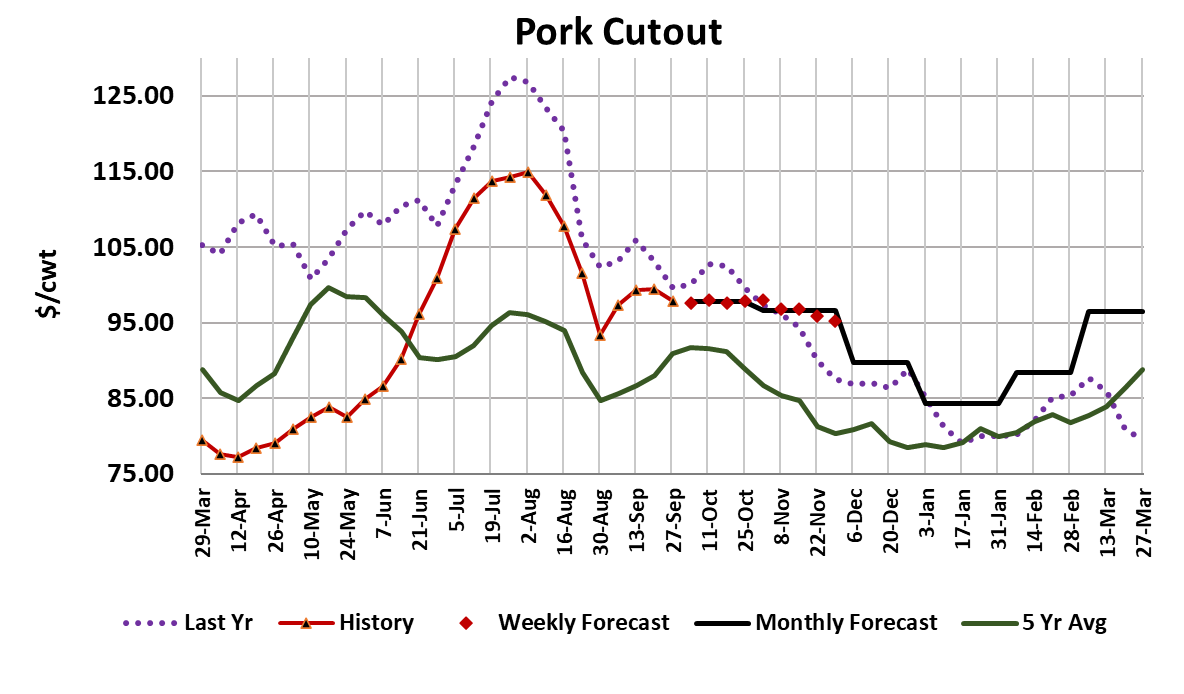

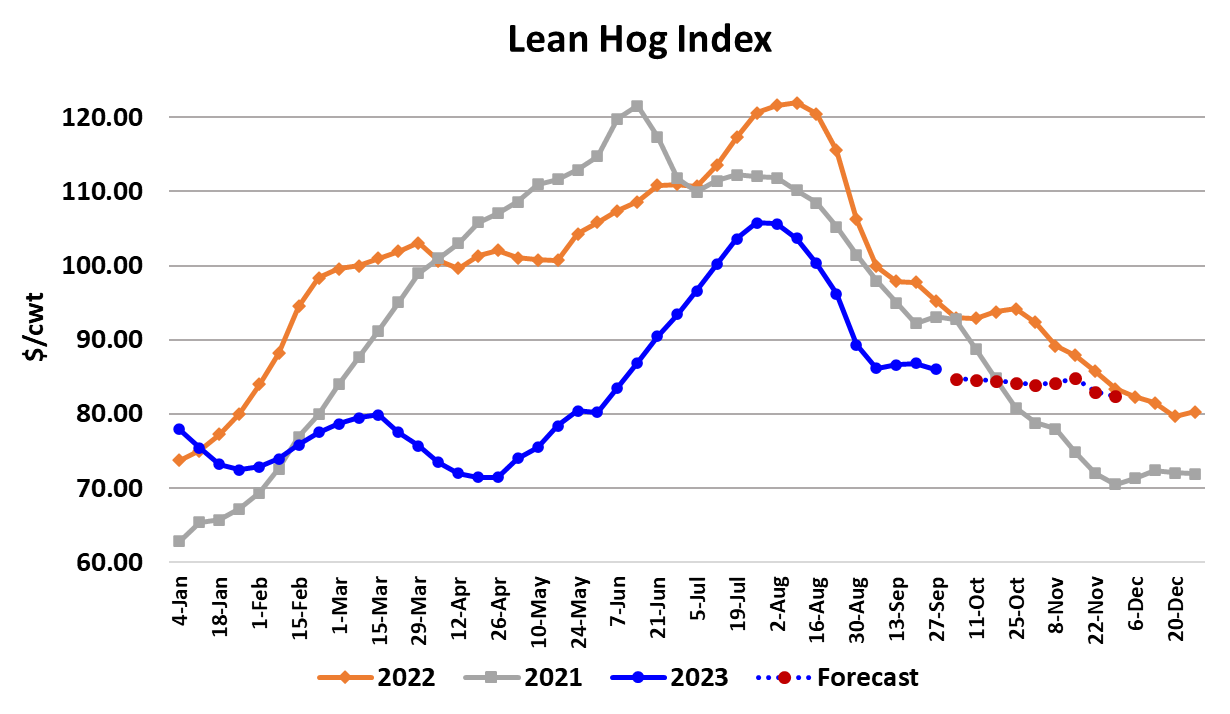

The pork cutout continued to ease lower this week, dropping $1.65 to average $97.81. That was a little faster decline than what we have seen in recent weeks, but still isn’t consistent with a market that is in trouble. Negotiated hog prices were lower also, with the NDD price dropping $2.31/cwt. on a weekly average basis. Packer margins remained healthy at $19/head, down about $1 from the week before. It is still unclear whether or not the Fed can do it, but It sure looks like the pork market is pulling off a “soft landing” this fall. All of the major primals were a little lower on the week and that is consistent with a market that dealing with large production. The challenge will be even greater next week since this week’s slaughter clocked in at a whopping 2.6 million head. The March/May pig crop is pointing toward a maximum weekly kill around 2.61 million head this fall, probably in November, but the fact that we already have a 2.6 million head kill in September is a little concerning. The industry has overkilled the pig crop in each of the four weeks in the Sep/Nov quarter so far, with the total overkill amounting to 175k. That’s not a huge miss yet, but if the overkilling continues at this rate it will become a problem by late October or early November. This week, USDA issued its quarterly Hogs & Pigs report. While most analysts were looking for the report to show at least modest herd liquidation, producers surprised us all by reporting that as of Sep 1 the swine herd was actually 0.3% larger than last year. Producers did reduce the breeding herd as expected, reporting it down 1.3% YOY. One might wonder how the total number of hogs was up if the breeding herd was declining. The answer is that producers reported a huge 4.3% YOY increase in the number of pigs saved per litter. The only other time that we saw pigs per little increase by that much was in 2015 when we were comparing to 2014—a year where PEDv had greatly reduced the number of pigs saved per litter. The consensus was for a 1.9% increase in pigs per litter, so this was way bigger than what was expected. As a result, the recent Jun/Aug pig crop was reported up 0.4% when the consensus was for a 1.5% decline. Needless to say, the market wasn’t happy with this surprise and the front two contracts closed limit-down on Friday. From a producer’s prospective strong gains in pigs per litter is a good thing because it lowers their average cost of production. They are essentially “doing more with less”. From an industry-wide perspective however, this rapid increase in productivity could result in low hog and pork prices and more pressure on producer margins. Of course, the industry can fix the problem just by liquidating more sows in coming quarters, but often it takes a significant margin meltdown to send a strong signal to producers that more breeding herd liquidation is needed. After what producers went through this spring, another margin problem is the last thing they need. How in the world did productivity increase so much in such a short period? While producers were busy thinning down their breeding stock this summer, they likely culled the poorest performing sows and that raised the average for the herd as a whole. There also could have been fewer disease problems this year compared to last. Finally, the financial disaster that producers went through this spring probably had many of them working hard to improve efficiency through better management. There have been times in the past where productivity (pigs per litter and percentage of sows farrowing) posted some impressive gains (but never like this), and in those situations, the productivity gains persisted for several quarters in a row. So that is the fear this time—that we will get several quarters in a row showing strong productivity and thus the industry will be inundated with hogs. I was actually surprised that most of the 2024 futures contracts didn’t feel as much pressure today as the front of the futures curve because if we are on a runaway productivity train, that is more bearish for the 2024 contracts than it is for the front of the curve. The one saving grace is that the Jun/Aug pig crop, which will be slaughtered in the Dec/Feb quarter was only up 0.4%, so pork availability between now and February shouldn’t be all that different from what was experienced last year. Adding to the supply side issue is the fact that hog carcass weights are now trending seasonally higher. Fortunately, they are starting at a relatively low level and are four pounds below last year and two pounds below 2021. The forecast has them remaining below last year until near the end of 2023. Export demand still looks relatively healthy, so that can help siphon off some of this fall’s large pork production. I’m forecasting per capita pork availability in Q4 to be nearly equal to last year. With demand also expected to be similar to last year, I expect the pork cutout in Q4 to average pretty close to the $93/cwt. that was registered in both 2021 and 2022. In the near term though, it will be important to watch how well next week’s market digests this week’s big pork production. If it can do so with only a $1 or $2 decline like we’ve seen in recent weeks, then that will be evidence that pork demand is holding up well. If the cutout craters next week, that will be an ominous sign because we are only just getting started with the big kills this fall.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}