Pork Wrap September 23

This felt like a bad week for the hog and pork complex, but I’m not

sure that the story the data are telling is as bad as the futures

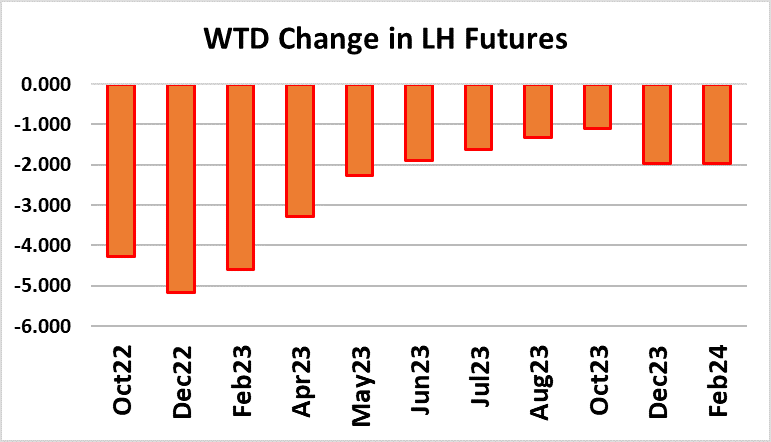

market implies. Certainly, traders turned bearish in a big way,

driving the front of the futures curve down $4-5/cwt this week.

That action was precipitated by growing dark clouds on the

macroeconomic front and a couple of weak prints from the belly

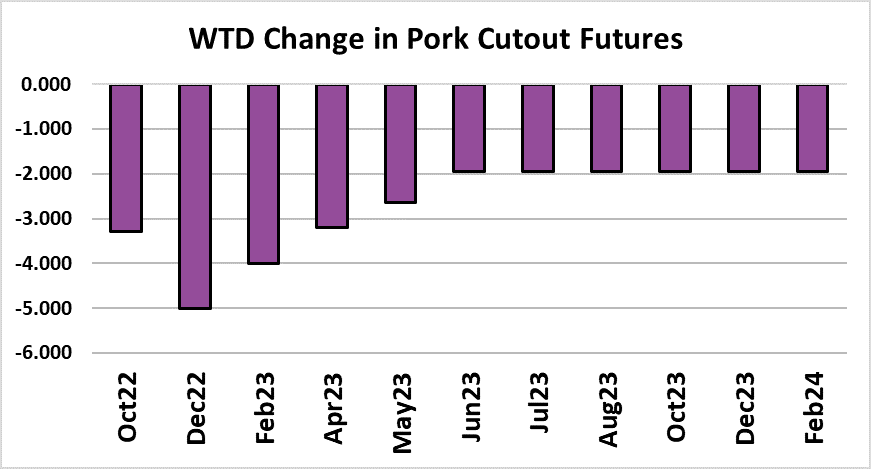

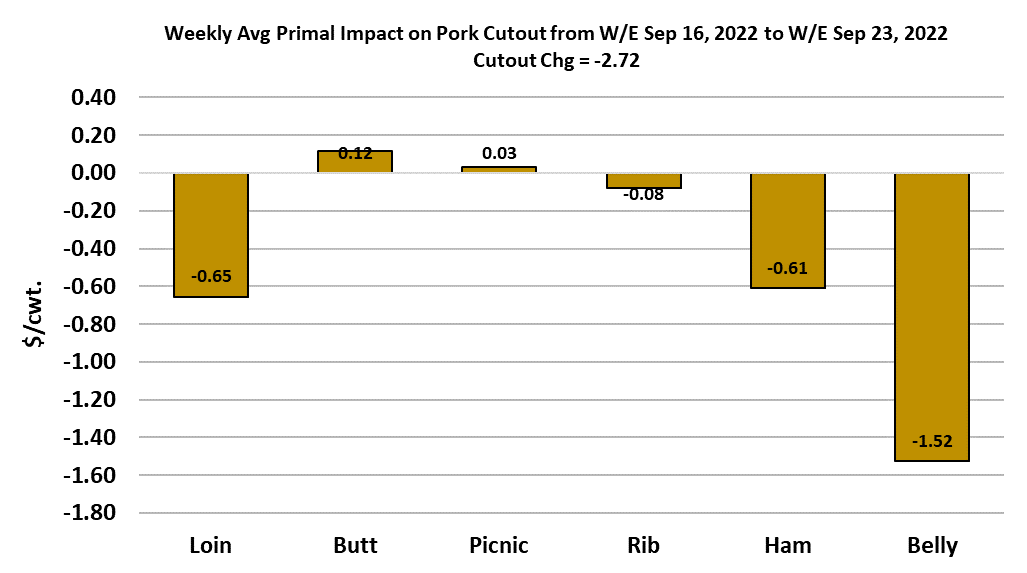

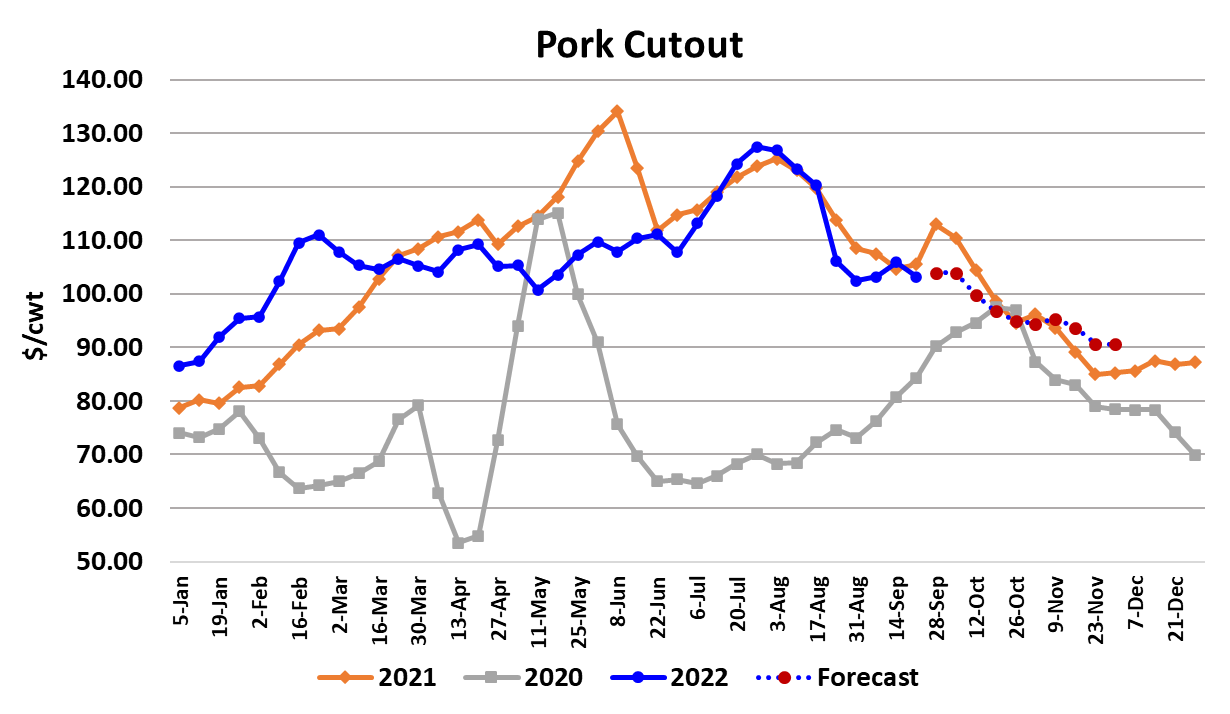

primal. In the end, the cutout was down $2.72/cwt. on a weekly

average basis, but the Lean Hog Index was about $0.10/cwt higher

on the week. Negotiated hog markets were steady-weak with the

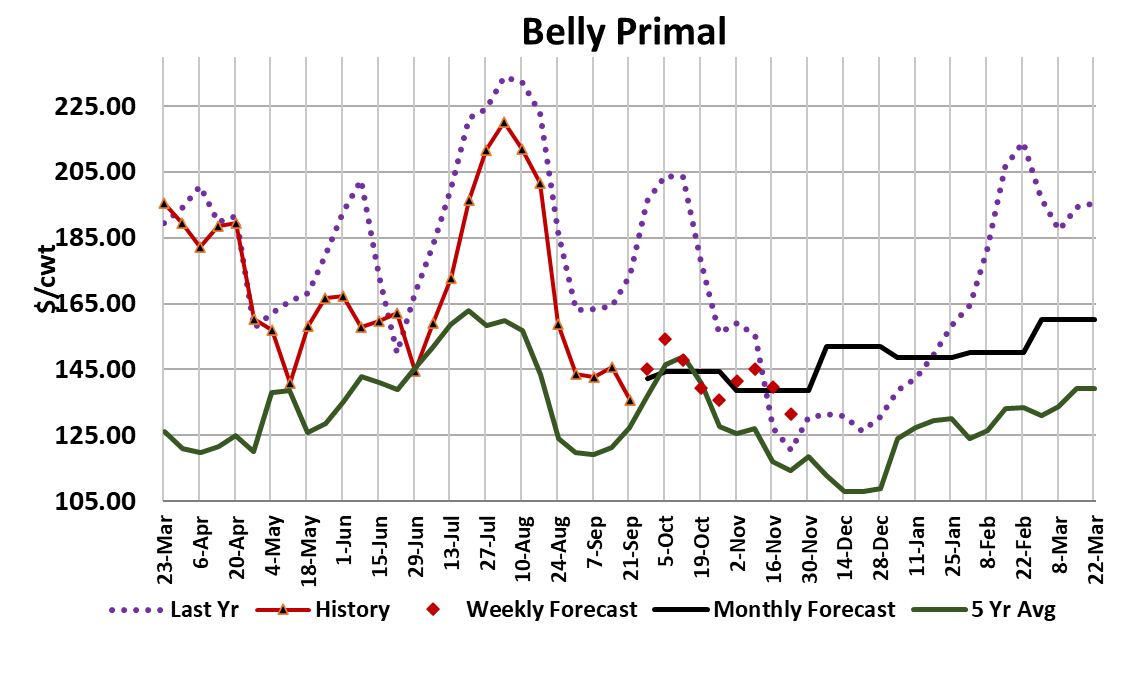

WCB up $0.76 and the NDD down $1.04. The attached chart

indicates that it was definitely the bellies that applied the most

pressure to the cutout this week. So, what is going on with the

bellies? The first thing to note is that belly prices have been

steady-soft for 4 weeks now and that is something that almost

never happens.

They are normally moving either up or down. This week the belly

primal broke through the $145 level that had acted as support in

the past two price downdrafts, so it is now at its lowest level of the

year. Last year, the lowest belly prices were observed just ahead

of US Thanksgiving, when kills were near their annual highs. That

makes sense. Does that mean that belly prices are just going to

keep trending lower between now and Thanksgiving? Probably

not. Last year, bellies made a low near the middle of September

and then rallied hard to the middle of October. I suspect that we

are going to see another early October rally this year, but it

probably won’t reach last year’s level because demand isn’t nearly

as strong as it was last year. Those users that put bellies into the

freezer during the fall months will likely be tempted by the fact that

belly prices are at the lowest level of the year right now.

USDA released the cold storage numbers for the end of August

this week and it showed belly stocks at 32.5 million pounds, which

was about double the 17 million pounds that were in cold storage

at the end of August last year. That is another reason that any fall

belly rally is not likely to reach last year’s level. However, 17

million pound in storage last year was unusually low and the 32

million pounds from this year is much closer to levels that we saw

in 2018-2020. The peaks and troughs in belly pricing are largely

driven by retail feature activity and retailers tend to do the same

thing year after year, so I think it is a good bet that we will see

bellies garner some modest price strength in the next few weeks.

The ham primal was down about $2.50/cwt. this week, but there

still seems to be good interest in bone-in hams and thus I suspect

that while hams may keep slipping lower, the decline will be very

gradual. Of course, pork availability is growing week-by-week

now as hog supplies increase seasonally and that likely to keep

the cutout from having a lot of upside potential in the next couple of

months.

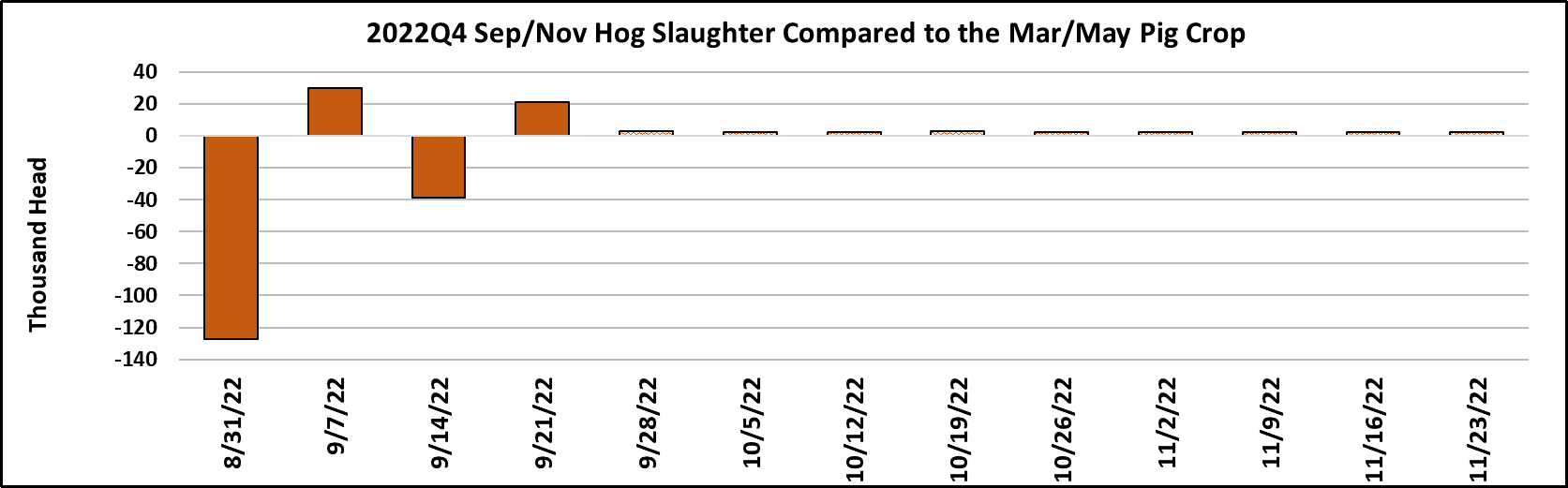

This week’s kill registered 2.54 million head and was just a little over

what the pig crop implied. So far this quarter, kills have been a little

lower than what the pig crop suggested, but to a much smaller degree

than what we saw this summer. According to my model, the Mar/May pig

crop implies a peak kill this fall right around 2.61 million head and if

USDA was a little high on the pig crop, as it seems so far, then maybe

the peak kill will be just below 2.6 million head. That isn’t very far from

what was killed this week, so the bulk of the supply increase has already

occurred and yet the cutout has managed to stay in triple digits. That

suggests that pork demand is holding up pretty well. However, the

cumulative effect of 2.5-2.6 million head kills week after week will

eventually start to wear the market down and some “pork fatigue” is likely

to set in. That is how we will end up with a cutout bottoming in the low

$90s or upper $80s during November or early December.

My current forecast has the cutout holding around $103 for two more

weeks and then working lower towards $95 by Halloween. Of course,

both beef and chicken prices are working lower at present and that will

increase competitive pressure on pork, but many retailers already have

pork slotted in for October features due to the financial incentives offered

by the industry, so it might not matter until we get closer to November.

The combined margin ticked down a little this week, but it is hard for me

to believe that it is going to move substantially lower given that it is

already below zero. I’d see this week as a head-fake and expect it will

post some gains in the next couple of weeks to resume the uptrend.

Packer margins averaged about $9.50/head this week and I’m

forecasting them to remain below $15/head through October.

I realize that is smaller-than-normal for that time of year, but we have less

hogs this fall than we did last year and the same amount of packing

capacity chasing after them. So some margin compression should be

expected. There is no sign that hogs are backing up in the pipeline.

Barrow and gilt weights were reported 2 pounds higher this week, but the

data are for the recent short kill week, so I wouldn’t expect that type of

increase to repeat. Weights will continue to move seasonally higher from

now until early November. There seems to be a growing consensus that

tougher macroeconomic conditions lie ahead for both the US and many

of its trading partners. Depending upon the severity of the downturn, it

will likely be a negative for pork demand, but in the early stages of a

potential recession, trading down by consumers could keep pork demand

afloat better than expected. I already have dialed in further demand

weakness into my Q4 price forecasts, so that’s already factored in and I

still end up averaging about $90 in both November and December. My

fear is that I may be too pessimistic on demand. Next week, watch for a

rebound in the bellies and keep an eye on the hams for further softening.

Any strength in either of those primals is likely to precipitate a rally in the

front of the futures curve.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}