Pork Wrap September 22

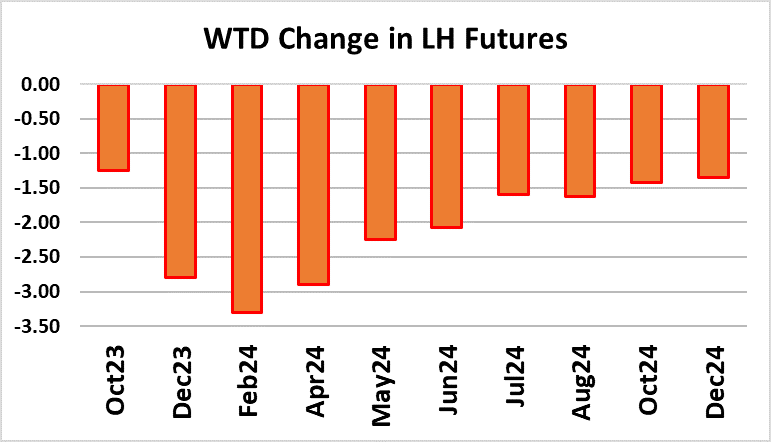

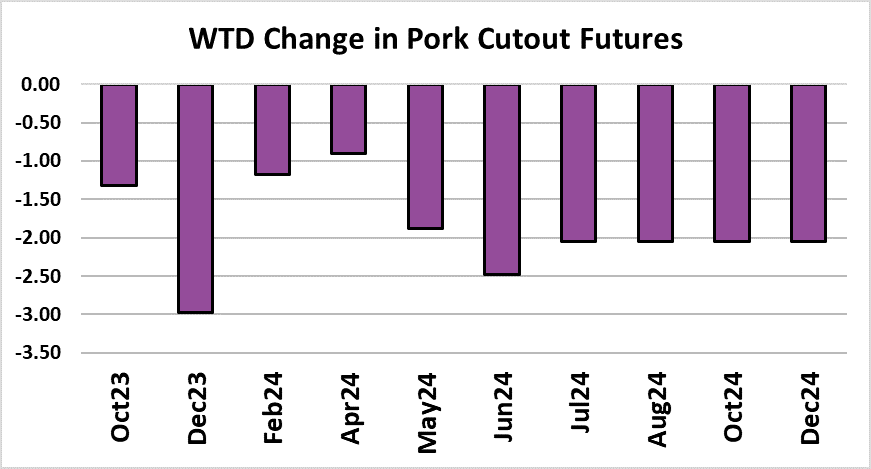

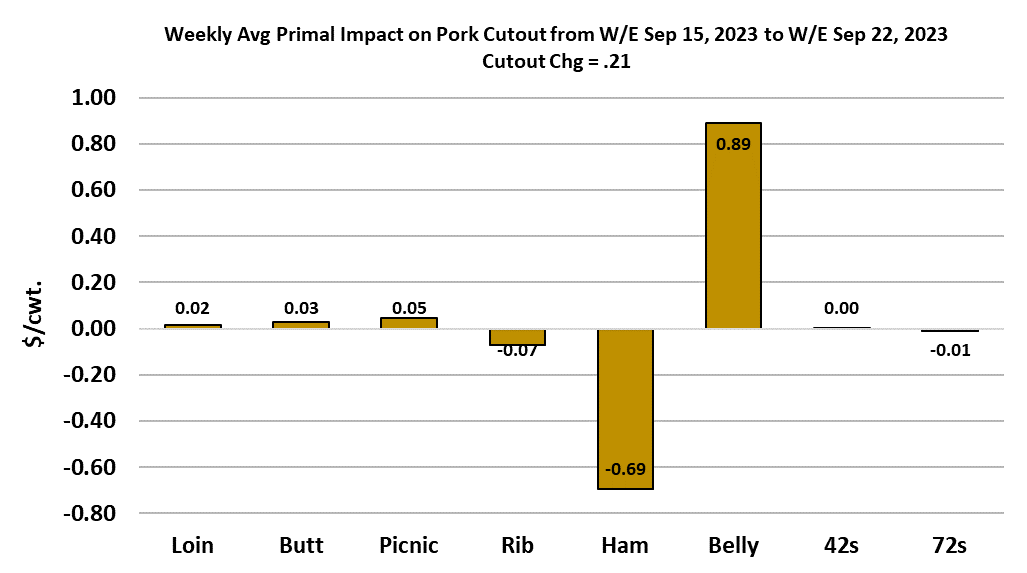

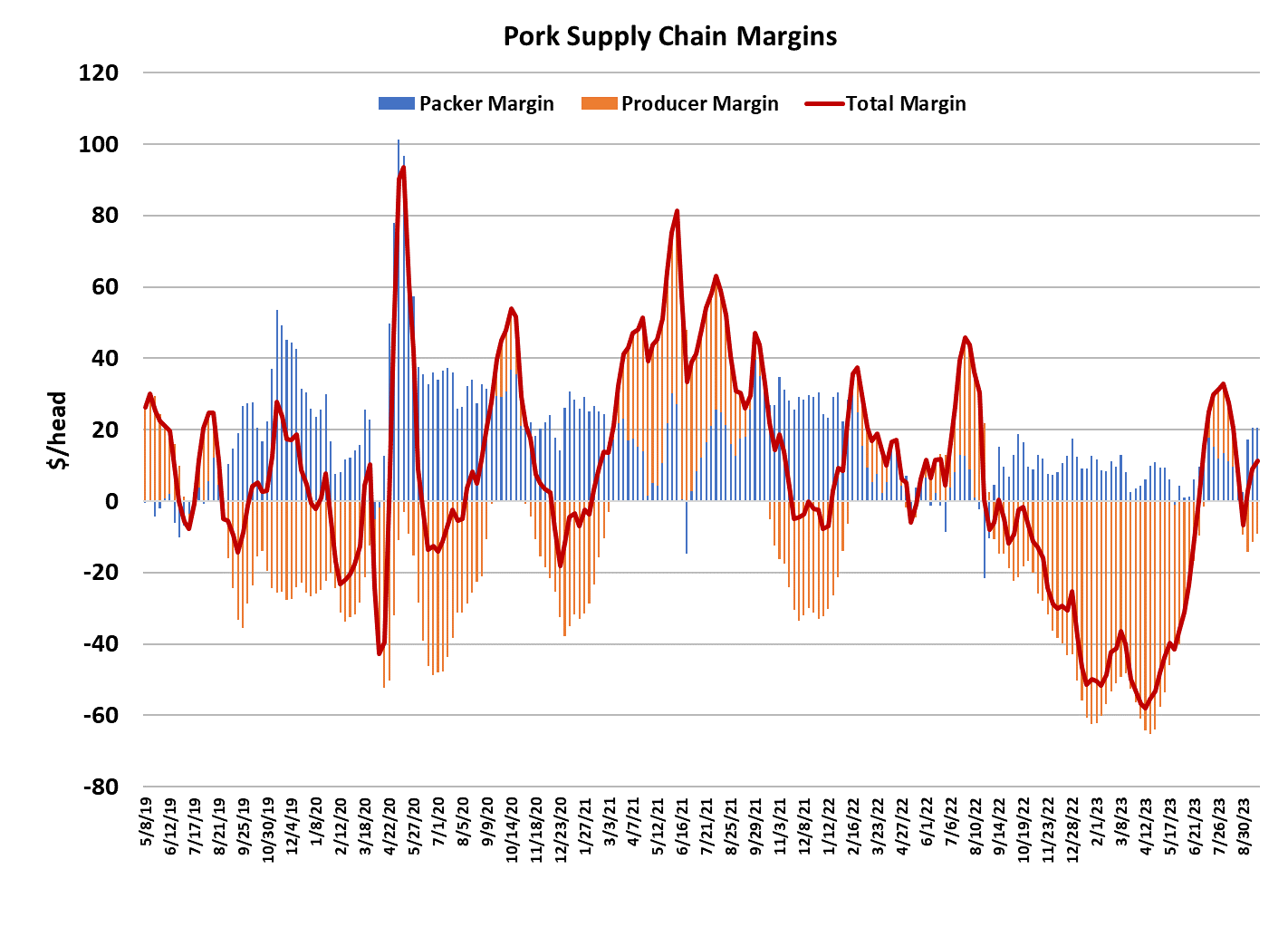

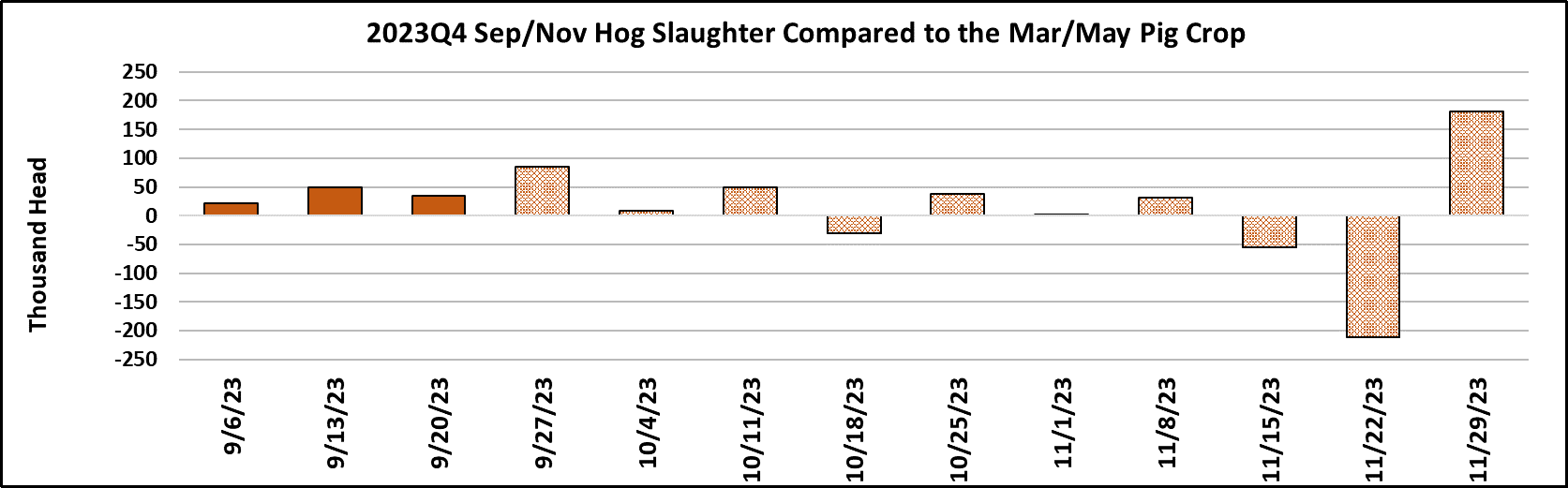

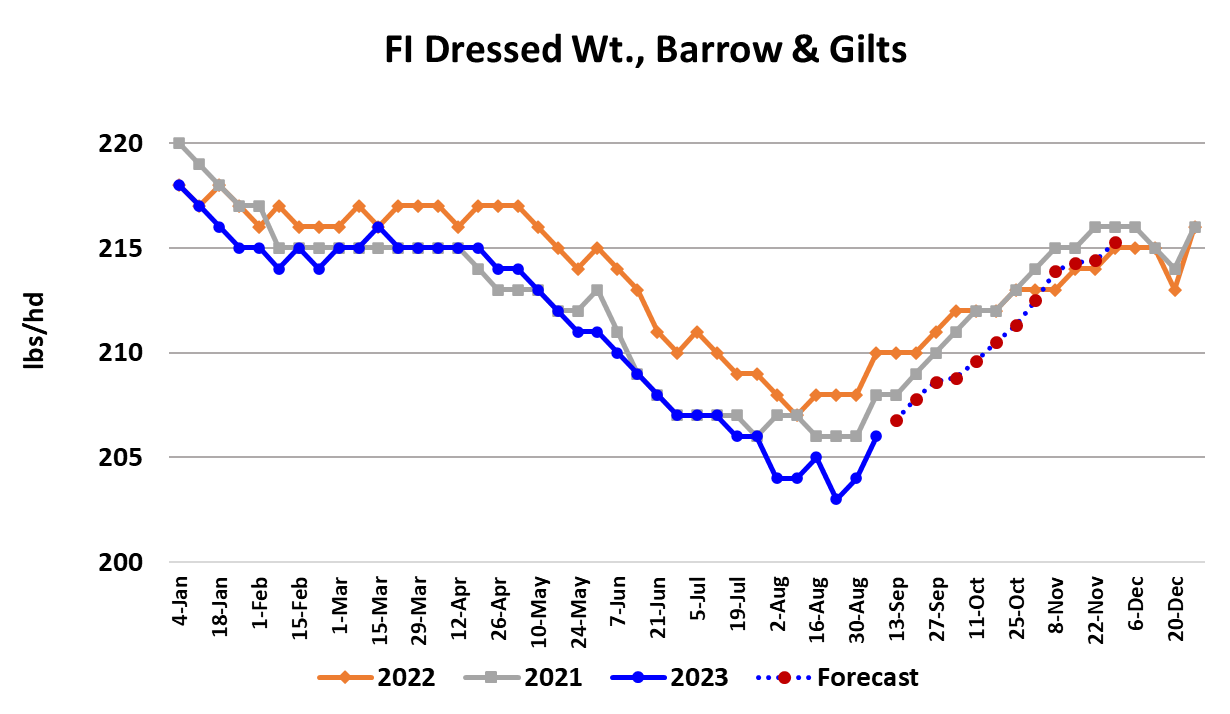

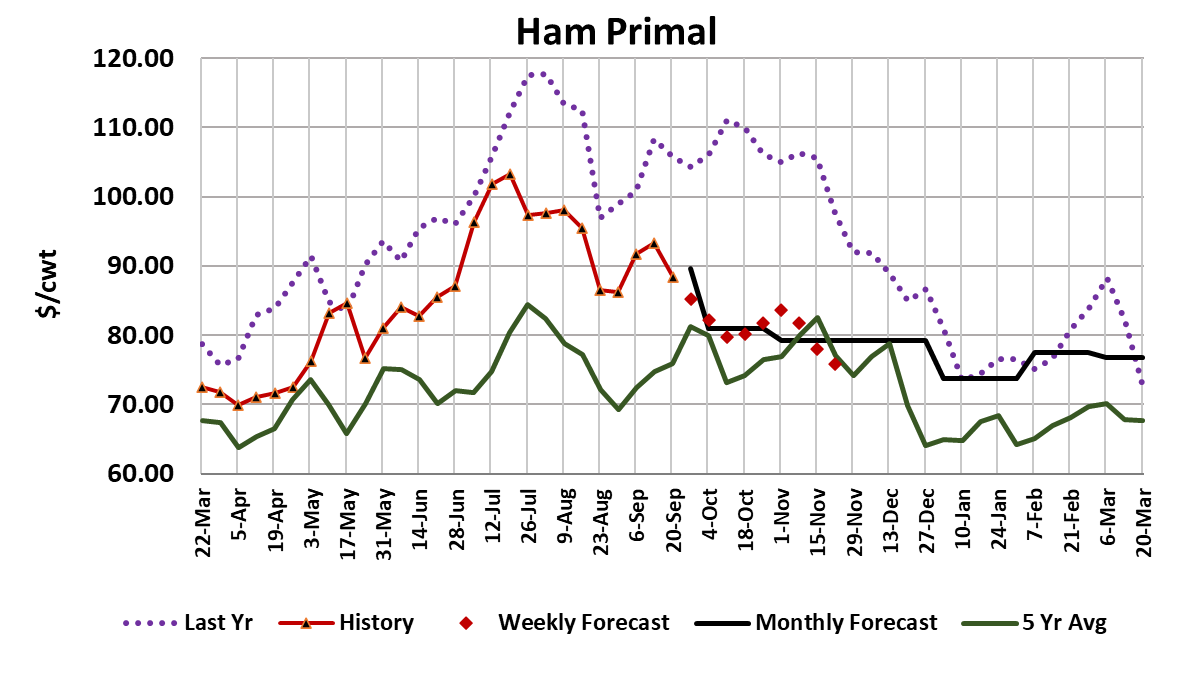

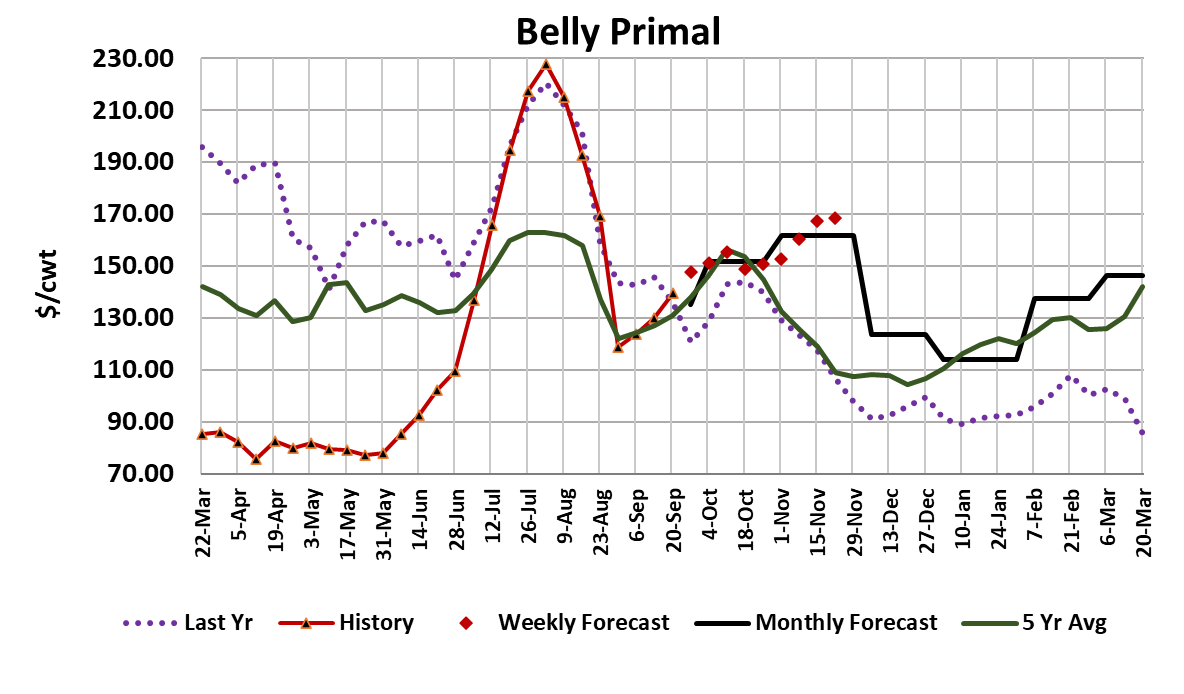

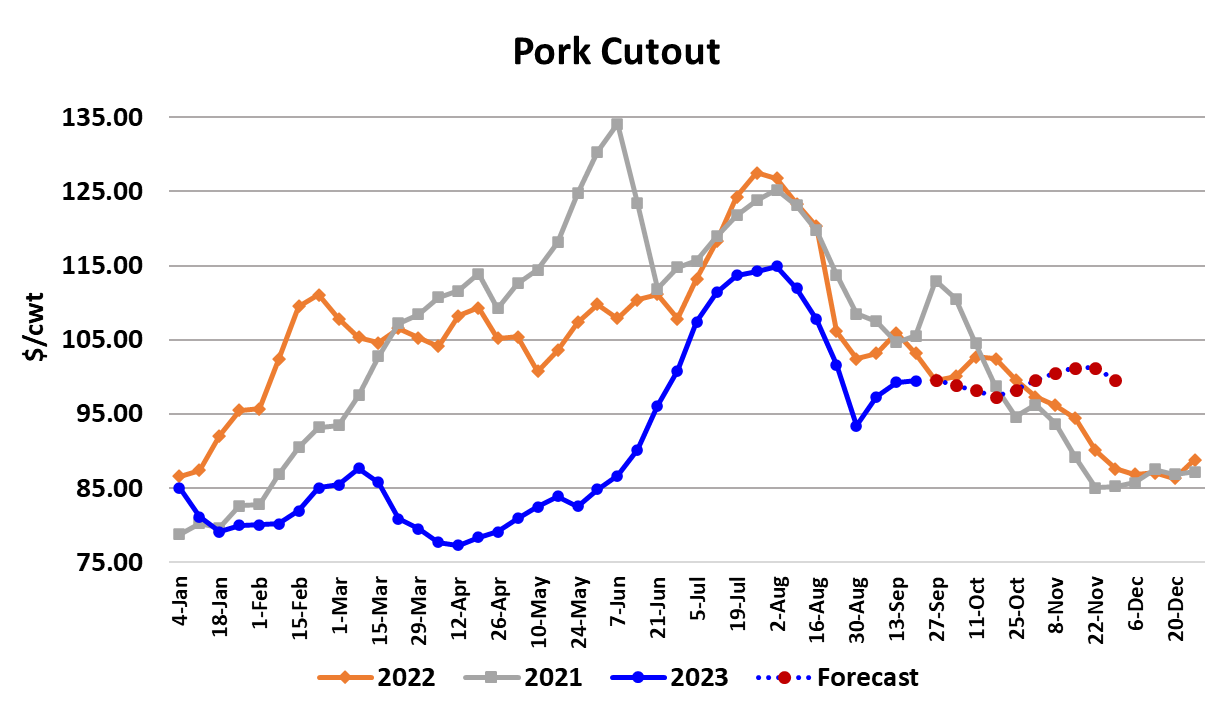

For the second week in a row, the pork cutout moved higher, advancing $2.05/cwt. on a weekly average basis to $99.36. Given that the cutout was stronger, there was little reason for packers to pressure cash hog prices and those were mostly steady, with the WCB negotiated market down only $0.18/cwt. on a weekly average basis. Nearby LH futures moved higher during the first two sessions of the week and then eased lower in the final three sessions. In the end, the Oct contract gained $1.60/cwt. for the week. Packer margins moved higher once again and I calculated them at $21/head currently. That is a huge improvement over the low single digit margins that they were realizing back in late August after the bellies crashed. Speaking of the bellies, I’ve had to re-think my belly price forecast because it now looks like they have reached a near-term bottom and could work a little higher in the next few weeks. Hams have become the problem child all of a sudden. The ham primal averaged about $2 higher on the week, but there has been a considerable weakening in the price of 23/27 bone-in hams and I’m watching that closely for further deterioration. If the hams are starting to buckle under the weight of larger production, then that doesn’t bode well for the cutout and cash hog prices down the road. Those 23/27s printed $100 at the beginning of the week and by Friday they were below $90. I haven’t been expecting hams to be as strong this fall as they were last year when the ham primal value held above $100 from the beginning of September until the middle of November, but I also wasn’t expecting them to crater this soon after Labor Day. Typically there is strong demand from processors at this time of year as they prepare hams for the holidays. Maybe that demand will show up in the next few weeks and turn ham prices back higher, but there is always a risk that they keep sliding because production is going to be large and growing. This week’s slaughter clocked in at 2.53 million head, which was about 50k stronger than what the pig crop implied. It is very unlikely that we will see another weekly kill much below 2.5 million head until the week of Thanksgiving in late November. It seems to me that the market generally handles the big fall kills well when they first start, but as we get closer to November fatigue starts to set in from week after week of big production. So far, that seems to be the case this year as the cutout is holding in the high $90s. The retail cuts were all higher on a weekly average basis and that is a good sign. Perhaps retailers are finally going to lean more on pork in their ads in place of more expensive beef. I tend to think of the retail cuts as setting the base for the cutout and the processing items (hams and bellies) providing the more substantial price swings that ultimately determine the cutout’s direction. It is a good sign that the base seems to be firm right now. It is a little concerning that slaughter in the first couple weeks of the Sep/Nov quarter has been higher than what the March/May pig crop implied, but the miss hasn’t been huge so I want to see a couple more weeks of data in order to ascertain whether or not we are going to have more pigs than advertised this fall. Sow slaughter continues to run high so I’m pretty confident that some herd liquidation is underway and we will get more information on that in a couple of weeks when USDA issues its Hogs and Pigs report. It seems that the 2024 futures are not adequately accounting for this fall’s breeding herd liquidation. Barrow and gilt weights moved higher this week and there are indications that the data for next week will show an even bigger increase. That means that the seasonal bottom in hog weights has finally been made and weights should increase through December. As with cattle, the de-trended and de-seasonalized carcass weights are at very low levels right now, which suggests that producers are keeping current on their marketings and there is little risk of hogs backing up in the pipeline over the near term. On the demand side, the combined margin moved higher again, building on last week’s gains, so that suggests a new demand upcycle has begun. However, that doesn’t remove the concern about ham demand. The turnaround in the combined margin was mostly driven by the stabilization in belly prices and moderate gains in the retail items. Hams still have the potential to crash the party. My price forecast currently anticipates a cutout near $93/cwt. in mid-December when the futures expire and, while that is about $7 higher than what the Dec cutout futures are currently expecting, I think it is do-able especially since I have Q4 pork demand dialed down from recent levels. The attached scatter diagrams makes that point. Light carcass weights and hog slaughter at or below last year should be sufficient to support a cutout in the low $90s unless demand just turns awful or the pig crop estimate turns out to be way too low. Since the number of hogs going to slaughter this fall should be close to last year and packing capacity is the same also, it is reasonable to expect packer margins to be similar as well. Exports should be a bit stronger than last year and that may be the difference-maker that permits a low $90s cutout in December. Time will tell. Next week, watch those hams. If they continue lower it could be an ominous sign, but I’d say there is at least a 60% chance that they regain their footing and all will be well.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}