Pork Wrap September 2

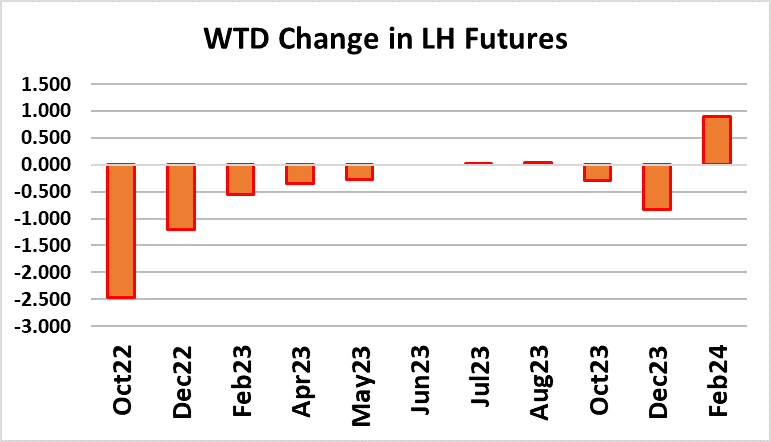

The hog and pork complex remained on the defensive this

week and the main feature was a huge $18/cwt drop in

reported negotiated prices. The WCB negotiated market

averaged $107.38 this week, down from a little over $125 the

week before. It isn’t all that unusual to see the negotiated

market follow the cutout down after a big drop, but it is

interesting that while USDA was reporting WCB base prices at

$107, the negotiated price that goes into the LHI calculation

was still around $125. Either there is a big delay in prices

flowing into the index or producers are getting some huge

premiums on top of the base price that has allowed that LHI

negotiated price to remain so high. This disconnect bears

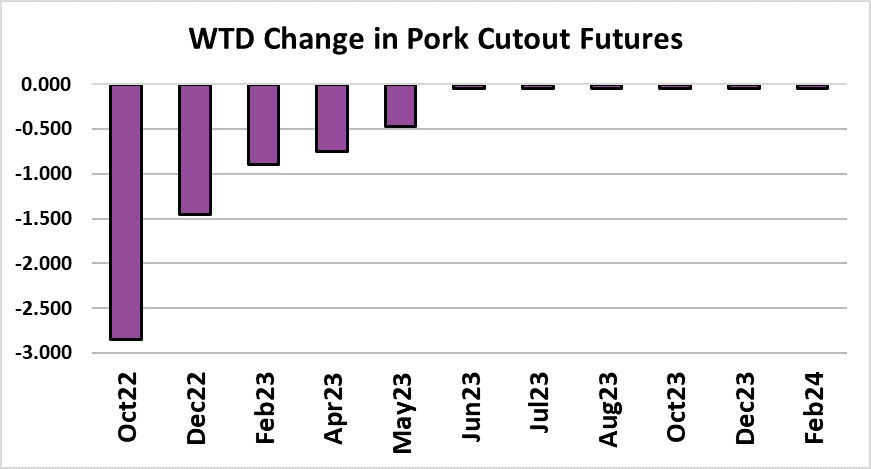

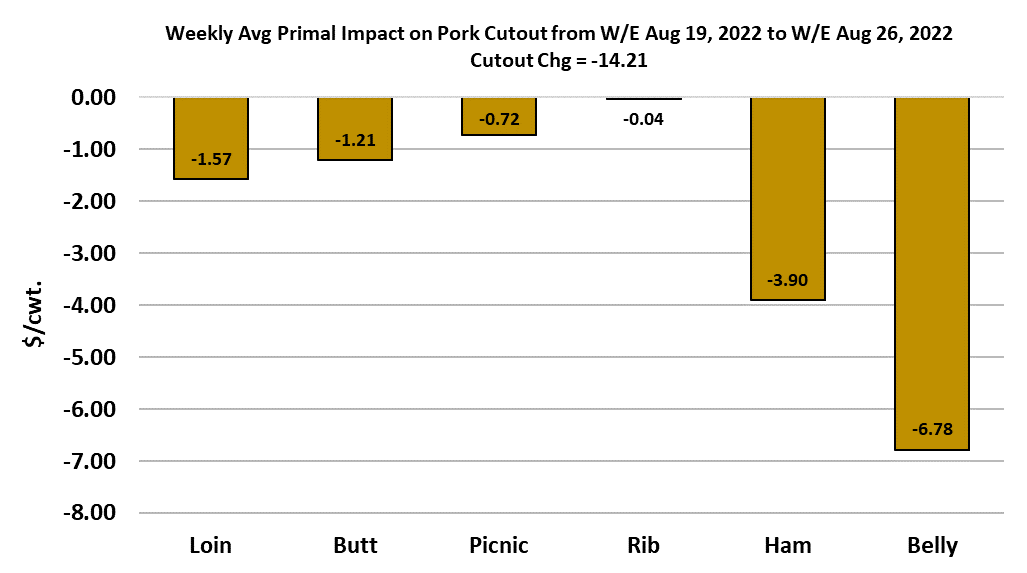

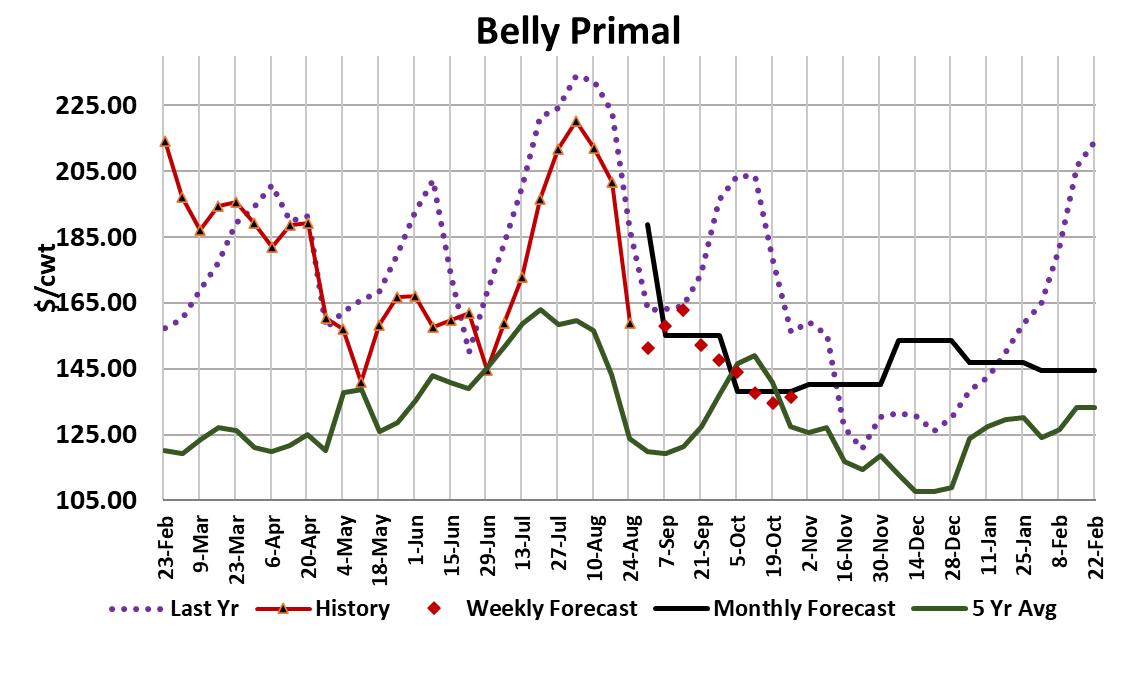

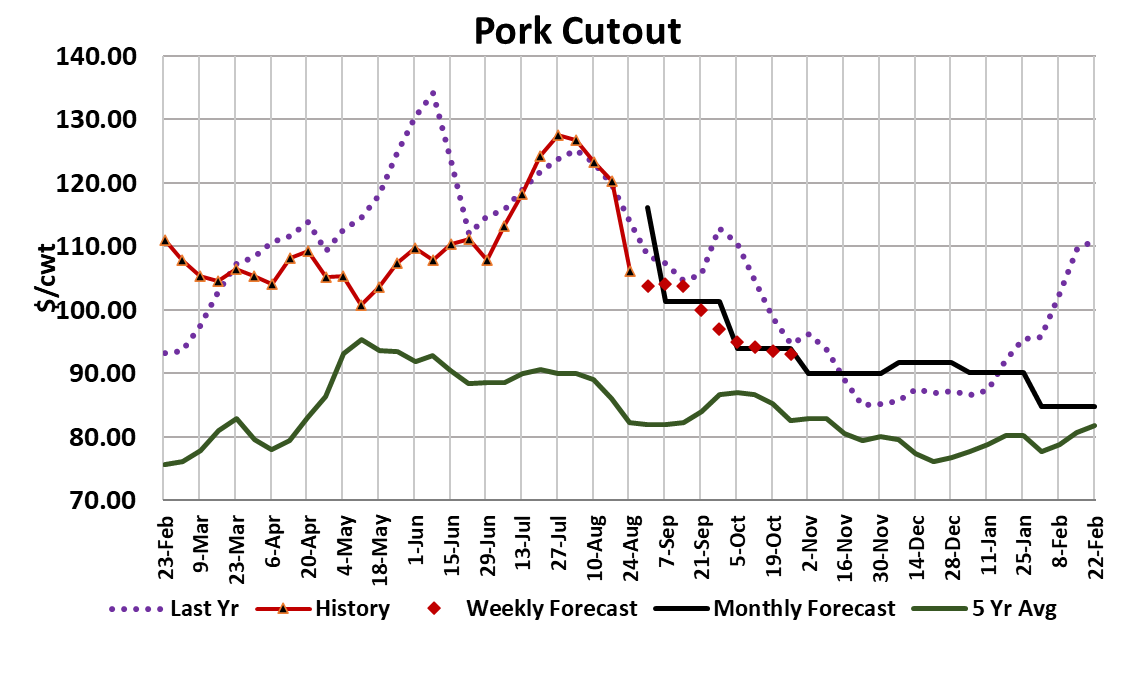

watching over the next couple of weeks. The cutout fell $3.71

this week to average $102.41 and we can see from the

attached chart that it was the bellies once again that drove the

decline.

Some of the retail items were lower also, but that might just

reflect the end of Labor Day buying and if clearance is good

over the long weekend, we could see those retail primals get a

nice bump next week. Hams were the bright spot in the pork

complex this week as prices first stabilized and then moved

higher as the week progressed. If the hams are finished going

down for now, then it could be difficult to get much further

weakness in the cutout, particularly if the bellies show some

life after the holiday. There is a school of thought that says

that processors lighten up on their demand for raw materials

ahead of a holiday week and then come back strong after the

holiday to replenish the pipeline. That might explain why

bellies and trims were so soft this week and it may offer a clue

as to what will happen next week as processors ramp back up.

I’m forecasting the cutout to average a little over $2 higher

next week but feel like I might be too low on that. The belly

primal finished the week at $137/cwt and the weekly average

was $143/cwt. We have to go all the way back to January to

find bellies that cheap. I suspect that some buyers are eyeing

this as an opportunity, and we could see improved demand for

bellies next week. The attached chart puts the average price

for bellies this week right in line with its previous two low

points this year. This could act like a support level in the near

term, but I suspect that bellies will need to trade below that

level for a while during Q4 as seasonally large production

makes its way through the system.

Hams have been very resilient this summer and that makes me think

that this week’s small increase in the primal value could be followed

by another week or two of higher ham prices. Any processors that

haven’t secured their raw material commitments for Thanksgiving

and Christmas hams had better get busy in the next few weeks or

risk being constrained by a lack of smokehouse space and

processing capacity. Of course, the biggest thing that makes me

optimistic about seeing some gains in the cutout next week is the

short kills. Packers really pulled back on the Friday and Saturday

kills this week and that resulted in a 50k reduction from the week

before and produced a total kill of 2.35 million head. Next week,

without a Monday kill, slaughter could total only 2.2 million head. So,

there is a short-term supply constriction that could be favorable to the

cutout. After next week, the Mar/May pig crop estimate suggests that

weekly kills should quickly eclipse 2.5 million head.

Keep in mind that most of the increase in slaughter between Labor

Day and Christmas typically happens before Halloween, so that will

be the period of greatest supply pressure on the market. The pork

industry tries to counter this by funding “pork month” in October,

where retailers can collect some financial incentives for featuring

pork aggressively. That seems to work pretty well since the average

change in the cutout between the end of August and the middle of

October has been +$4.70/cwt over the past 10 years. Last year, the

cutout dropped $4 during that period, but in 2020 it gained $21 and in

2018 it gained $13/cwt. So, it isn’t a given that the cutout is going to

collapse over the next six weeks, and it is hard to justify Oct LH

futures near $90 at expiration without further significant pressure on

the cutout.

Granted, the macro environment for pork demand probably is worse

this year than in the recent past, but that was the case this summer

too and demand held up way better than expected. It seems to me

that enough damage has been done to the hog and pork complex

and now it is time for some modest recovery. Next week, watch for

signs that buyers are finding value in bellies. Retail primals should

also perform well. If it becomes clear that the cutout is gaining

support, then I suspect the futures will jump with joy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}