Pork Wrap September 17

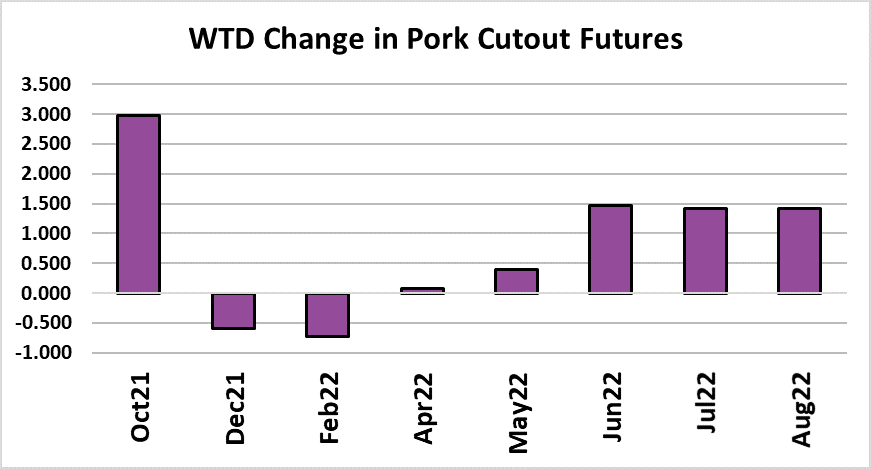

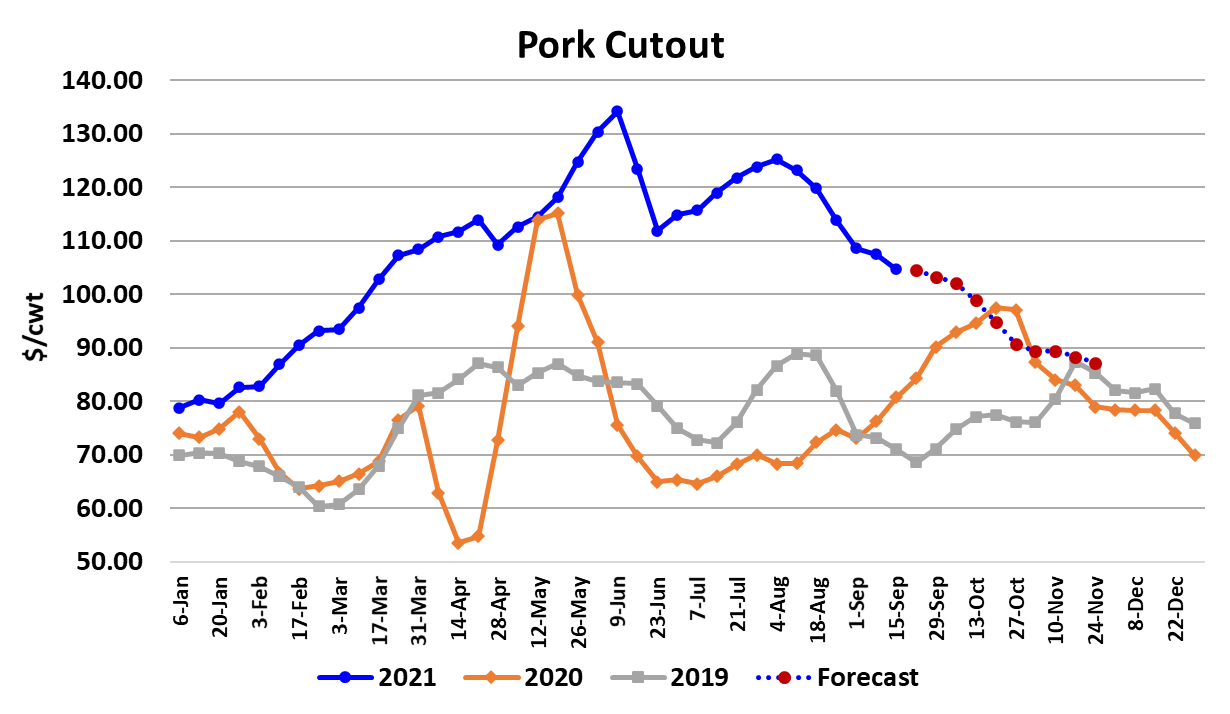

Both the cutout and the LHI were down about $2.75 on an average

basis this week, so packer margins didn’t change much. They

currently sit close to $17.50/head. The negotiated hog markets have

been moving steady lower, with the WCB down $6.15 this week and

the NDD down $4.56. Those declines haven’t been fully reflected in

the LHI yet, so it has some additional downside risk early next week.

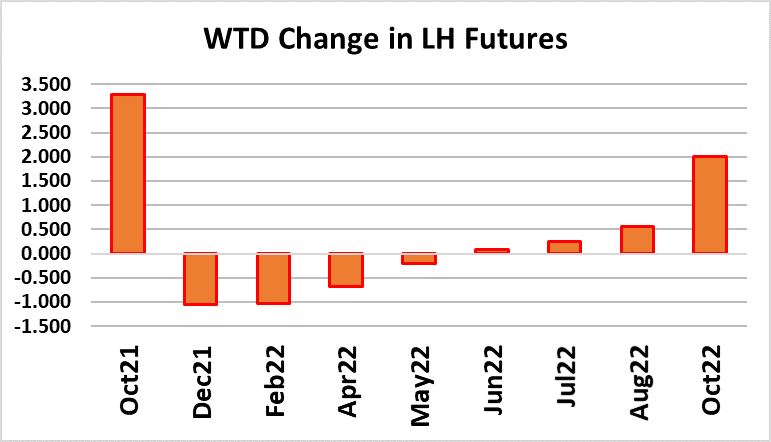

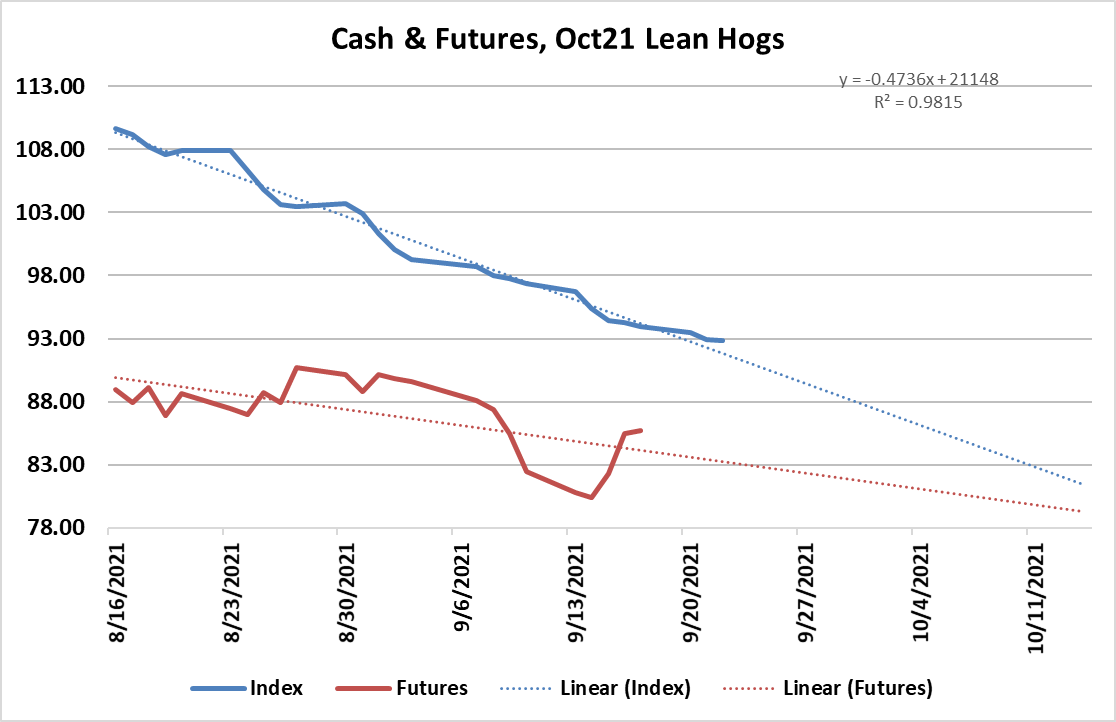

Nearby Oct futures rallied hard this week as traders came to realize

that they were projecting too much of a discount. The chart below

shows that the LHI has been on a steady downtrend since Oct became

the nearby and if we project that trend all the way out to expiration

(using the regression line), it would come in around $82.

However, in recent days the weakness in the cutout has tempered and

so far the cutout has managed to hold over $100. That should rightfully

make traders question whether or not the trend in the Oct contract is

going to persist at this rate. This week they decided it wasn’t and that

generated a $3+ gain in the Oct. The Dec contract got left behind as

Oct rallied and so the Oct/Dec spread ballooned out to almost $12 at

one point this week. That seems like way too much of a discount to put

on Dec in this type of market where demand is very robust. Now the

front seven contracts are all reasonably close to my estimate of fair

value. Be advised that fair value could shift next Thursday when we

get the next issue of the Hogs & Pigs report. I’m expecting the

government survey to show about a 1% YOY decline in all swine, but

about 2 million head more than were reported in the June report. A

good bit of that is seasonal. I’m forecasting the Jun/Aug pig crop

down 3-4%, although I think the risk is that it may be down less than

that. Those will be the pigs that are slaughtered in the upcoming Dec/

Feb quarter, so I’d expect relative tightness to persist in the hog supply

well into Q1.

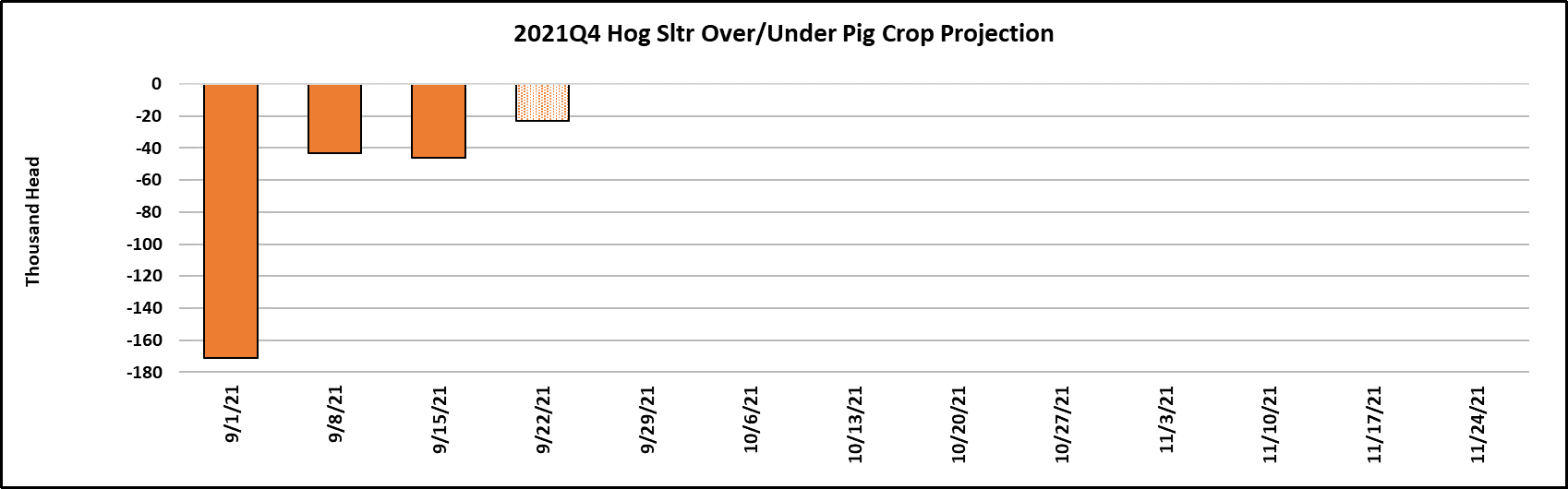

USDA is almost certain to make a major downward revision in the

previous Dec/Feb pig crop because slaughter levels that we observed

this summer came in way below what their survey suggested. That

trend has continued into this quarter and the chart below shows that

during the first three weeks of this quarter, slaughter has been about

250,000 head shy of what it should have been if the pig crop estimate

was on target. So there is reason to believe that hogs will be tighter

than advertised this fall, even though numbers will certainly increase

seasonally. This week’s kill came in at 2.54 million head—the biggest

kill since late March. By early October, kills should be running over 2.6

million head and moving toward a peak around 2.68 million head

around Thanksgiving. It is important to note that most of the expansion

in hog kills during the fall happens between Labor Day and the middle

of October.

From the middle of October to Thanksgiving the increases are

typically smaller. Hog weights are currently near their annual lows,

but will be increasing seasonally in the next few weeks. The

weight data does not provide any evidence that hogs are backing

up in the pipeline. In fact, I’d say that the weight data suggest that

the pipeline is quite clean. But we have been seeing packers

pushing negotiated hog prices lower with relative ease, so that

makes me wonder what is going on. It has crossed my mind that

pork plants may already be feeling the stress of not enough labor

and that is why packers haven’t had much trouble procuring hogs

at lower prices. If the labor problem is already arising, it should

start to show up in the form of widening margins.

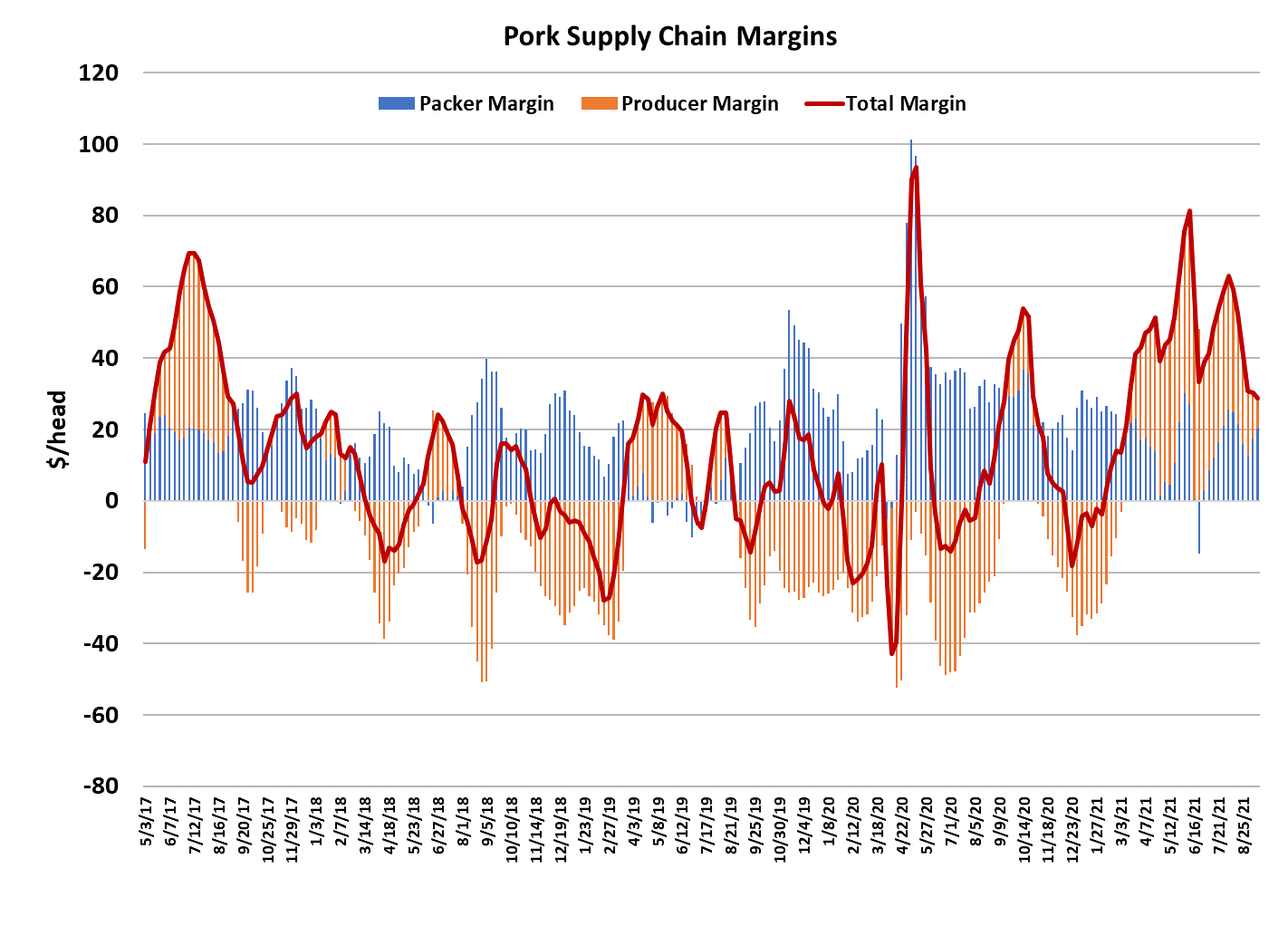

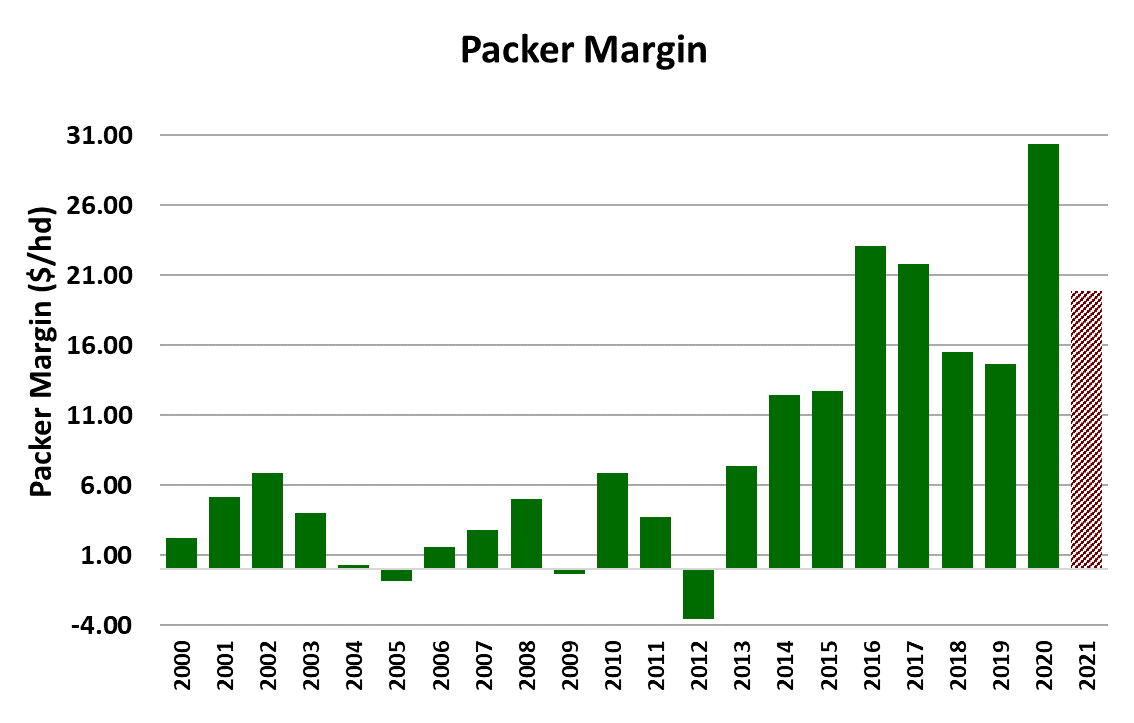

Margins are pretty good right now, but not exceptionally wide.

Going forward, we need to keep a close eye on packer margins as

an indicator of packing plant labor availability. I’ve included the

annual bar chart of packer margins below, same as I did for beef.

Pork margins haven’t gone exponential in recent years like they

have for beef, but it is pretty clear that something has been different

since about 2014. When packing margins expanded in 2014-16, it

attracted new capacity into the industry and that seemed to temper

margins for a couple of years and then the pandemic came along.

Margins for 2021 look like they will be about a third lower than they

were in 2020. Domestic pork demand remains very good, but

slowly working lower. The combined margin is still trending lower,

but the trajectory has softened recently. In times past, the

combined margin would almost always go negative before it turned

higher, but I’m guess that in the current environment, it will turn well

before it moves into negative territory.

Exports are the weak link in the pork complex. Movement to China

has softened considerably and other destinations are not picking up

the slack. That has industry observers concerned and may explain

why such a big discount is being assigned to the Dec contract.

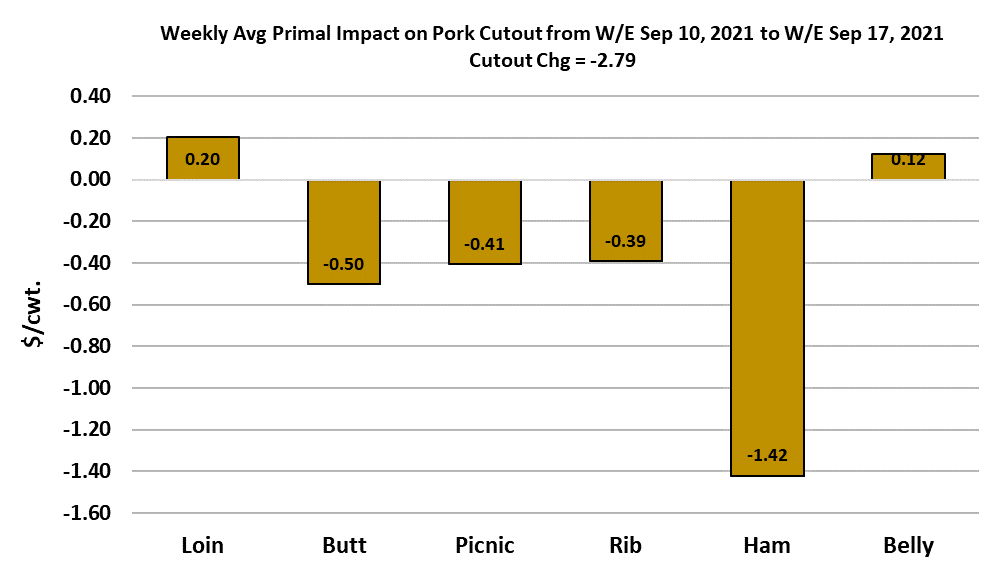

This week the hams were the biggest contributor to the softer

cutout, but they appear to be close to a bottom and wouldn’t be

surprised to see them rally soon. Although consumer demand at

retail is very good, I suspect that prices for the retail cuts will

continue to track lower as kills expand this fall. Bellies and hams

are more likely to provide support. The forecast has the cutout

slowly working lower, but not breaching the $100 mark for at least a

couple more weeks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}