Pork Wrap September 16

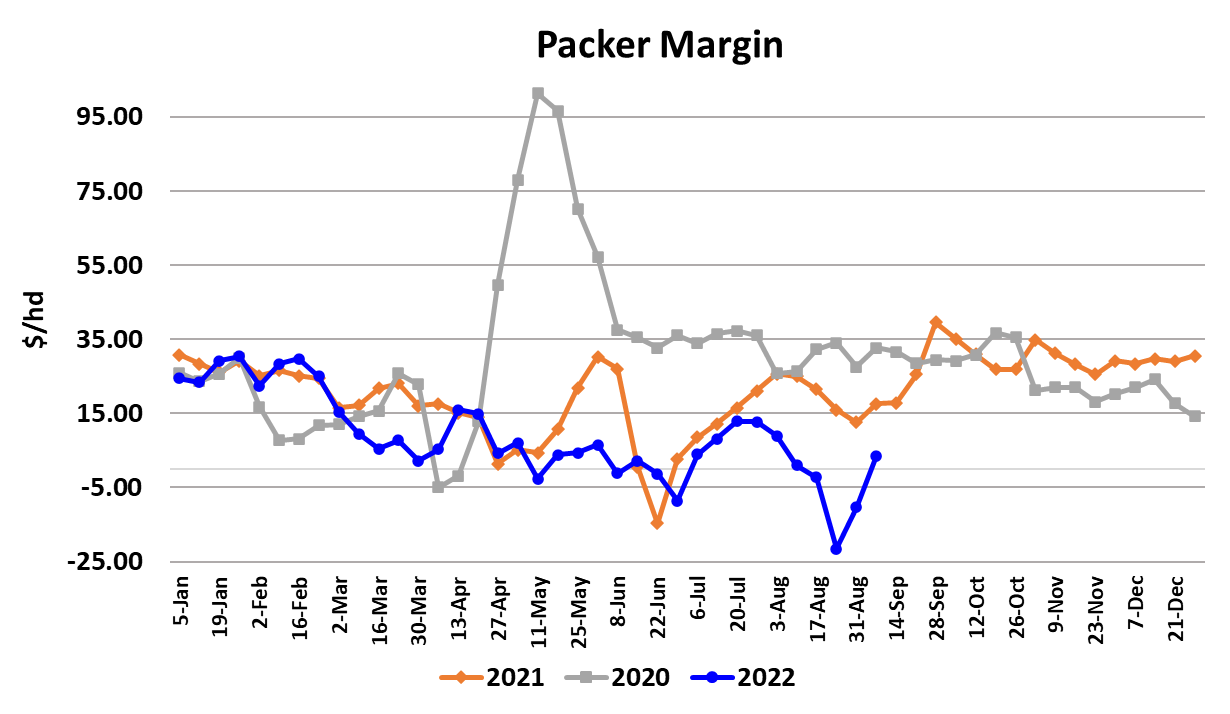

This was a constructive week for pork packers. They managed

to move the cutout higher while at the same time keeping some

pressure on the cash hog market. That helped to restore their

margins back to about $15/head, which is much more typical

for this time of year than the negative margins that they posted

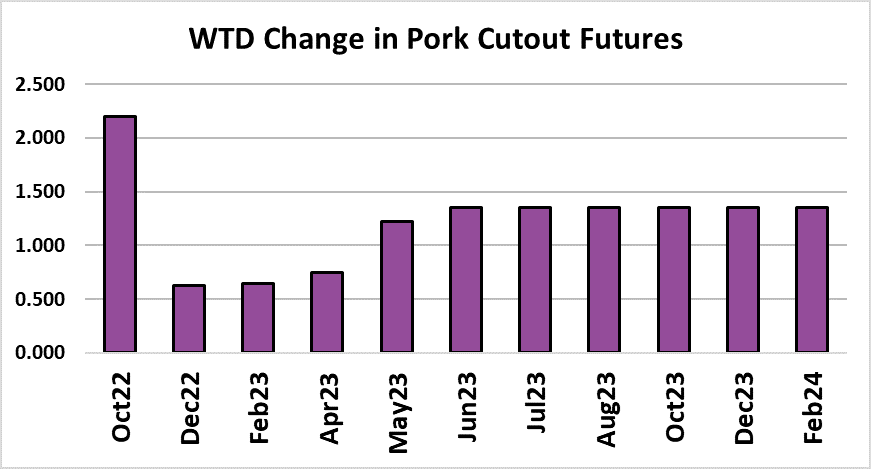

near the end of August. The cutout gained $2.72/cwt. to

average $105.92 and the LHI dropped $2.16 to average

$97.75. However, the average masks the fact that toward the

end of the week the LHI was starting to move upward and it

looks like it will print over $99 sometime early next week. That

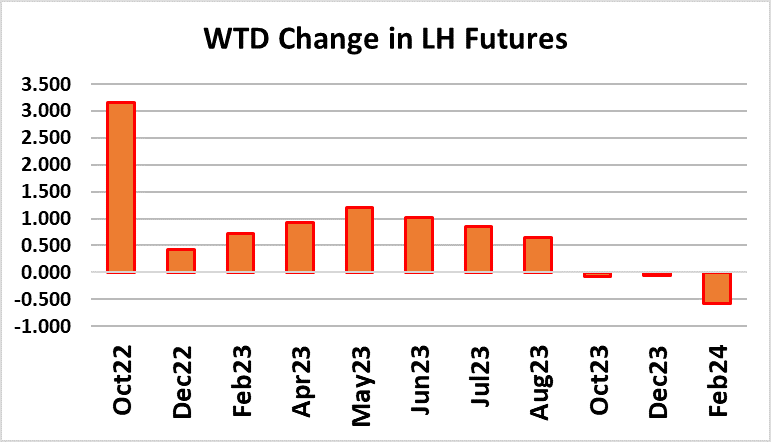

caused some nervousness for the shorts in the Oct contract

and as they covered, they pushed the Oct up close to $97 at

week’s end. It was rather impressive to see the cutout move

higher as the slaughter levels got back to normal after the

holiday. This week’s kill registered 2.47 million head, which

was a big increase over the 2.24 million head from the week

before.

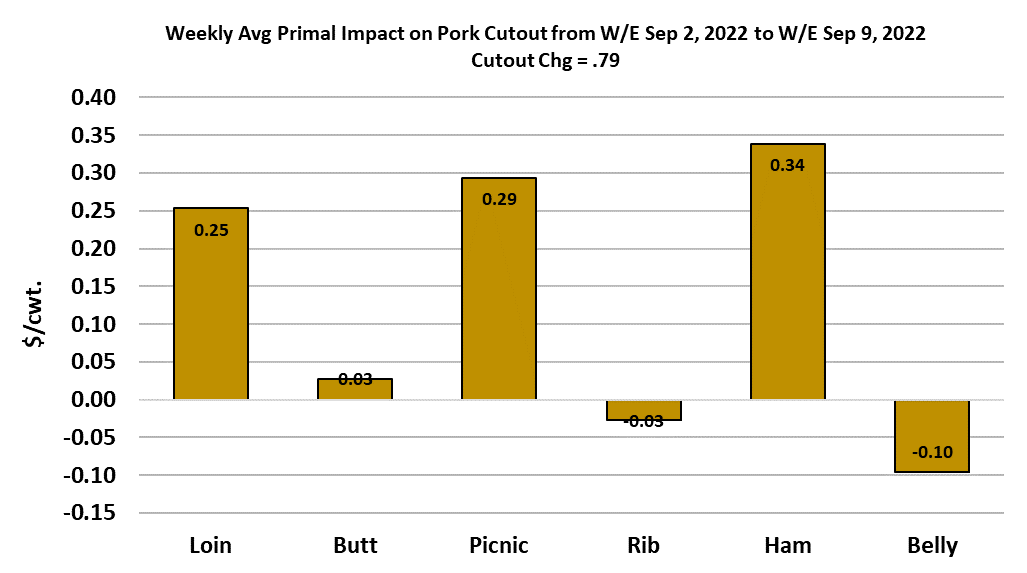

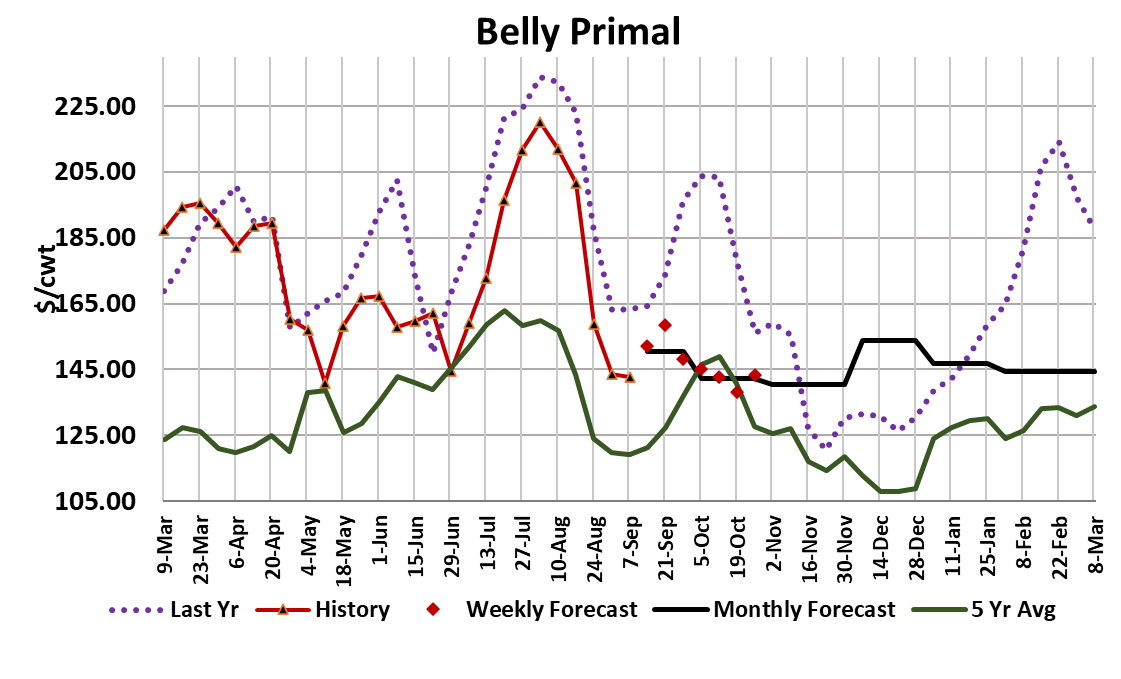

Hams carried the load once again, but there were also some

modest increases in most of the other primals. The belly

primal gained about $3/cwt. this week, which is a rather small

price movement in the belly world, so I think market participants

are still expecting bigger things out of the bellies in the next few

weeks. Bulls have been hoping that the hams and bellies

would join forces and shoot higher simultaneously, but alas, it

seems the belly is just fine letting the hams lead the way.

Processing demand for hams should be quite strong this fall as

super-high pricing on fresh turkeys make hams a more

attractive alternative. However, the window to get hams cured,

smoked, spiral-sliced and packaged in time for Thanksgiving is

narrowing.

That could lend a sense of urgency that keeps the ham market

supported until the early part of October. After that, a price

reset becomes much more likely. I’m forecasting two more

weeks of strong ham pricing before they break lower. I do think

that bellies will join the party eventually, but it is hard to know

just how strong the potential price increase will be. Belly slicers

often wait for November, when the biggest kills of the year

occur, to put bellies into the freezer for use the following spring.

However, if they start to sense that bellies might not get any

cheaper than current levels, we could see a flurry of buying

activity in late September or early October. The retail primals

should do better over the next couple of weeks as grocers start

laying in supplies for their pork month features.

So, it seems to me that the cutout should stand a good chance of

posting further gains in the next couple of weeks. Right now, I’m

forecasting the top close to $110 on a weekly average basis, but if I’m

wrong it will probably be because the hams and bellies strengthened

more than expected and lifted the cutout above $110. I made the

same changes in the demand indexes for pork as described for beef,

incorporating the CPI as to better account for the impact of inflation.

After making that change for beef, it became apparent that the

pandemic-induced demand bubble has fully dissipated, but the

attached chart for pork indicates that there is probably still some of

that elevated demand left in the pork complex. The chart indicates

that I’m forecasting a rather big drop in pork demand for Q4 and I’m a

little nervous that maybe I’ve got demand dialed down too much over

the next few months.

That means that the risk to my cutout forecasts lies to the upside in

Q4. We are rapidly approaching the next release of USDA’s Hogs &

Pigs survey on September 29. I’m projecting further modest

contraction in the herd, with both the breeding herd and total swine

numbers down about 1% YOY. I see the Jun/Aug pig crop down only

half a percent however, as productivity improvements should be in the

cards. Even so, if this would mark the seventh quarter in a row where

the pig crop posted a YOY decline. Once China resolved their ASF

problem, it appears the need to continue growing the US herd

diminished. Speaking of exports, USDA finally got caught up on their

weekly export data after 4 weeks of darkness due to system issues.

When the data finally saw the light of day, the news wasn’t good for

pork.

Total exports for last two weeks have averaged about 10% below

where they were during the middle of summer, when pork prices were

much higher. The attached chart indicates that export volumes are

still lagging last year by a significant amount and the comparison will

get even tougher in Q4. As a result of smaller YOY exports and larger

imports, it looks like per capita domestic pork availability was modestly

higher YOY in Q3 of this year, even though pork production was

almost equal to last year. The same could hold true for Q4 if recent

trends continue. For now however, supply concerns take a backseat

because the combined margin has confirmed that a new demand

upcycle has begun and with a little help from the bellies, that should

support the cutout in the near-term.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}