Pork Wrap September 13

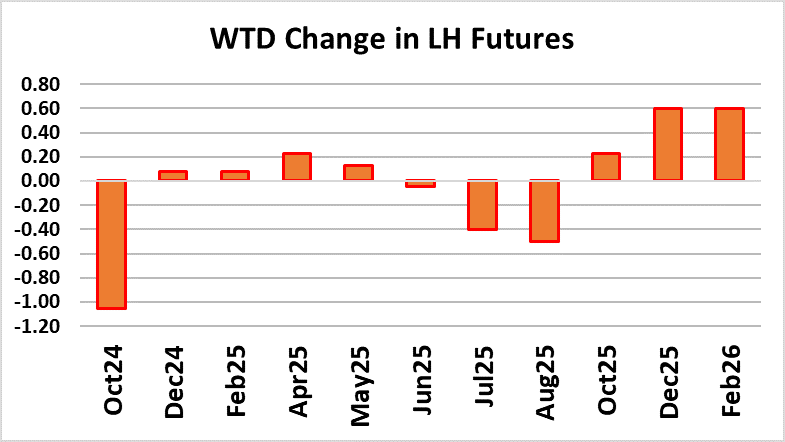

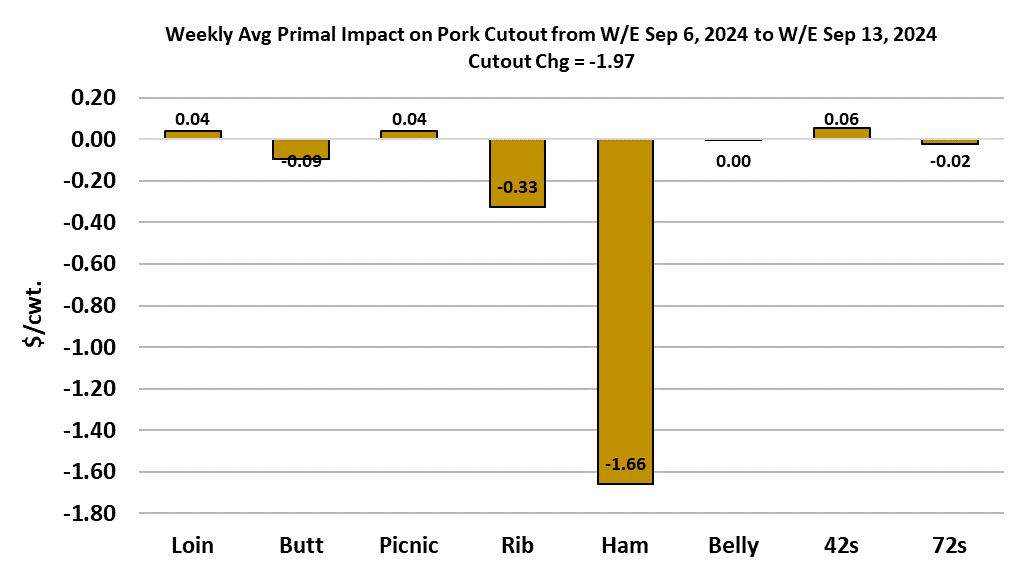

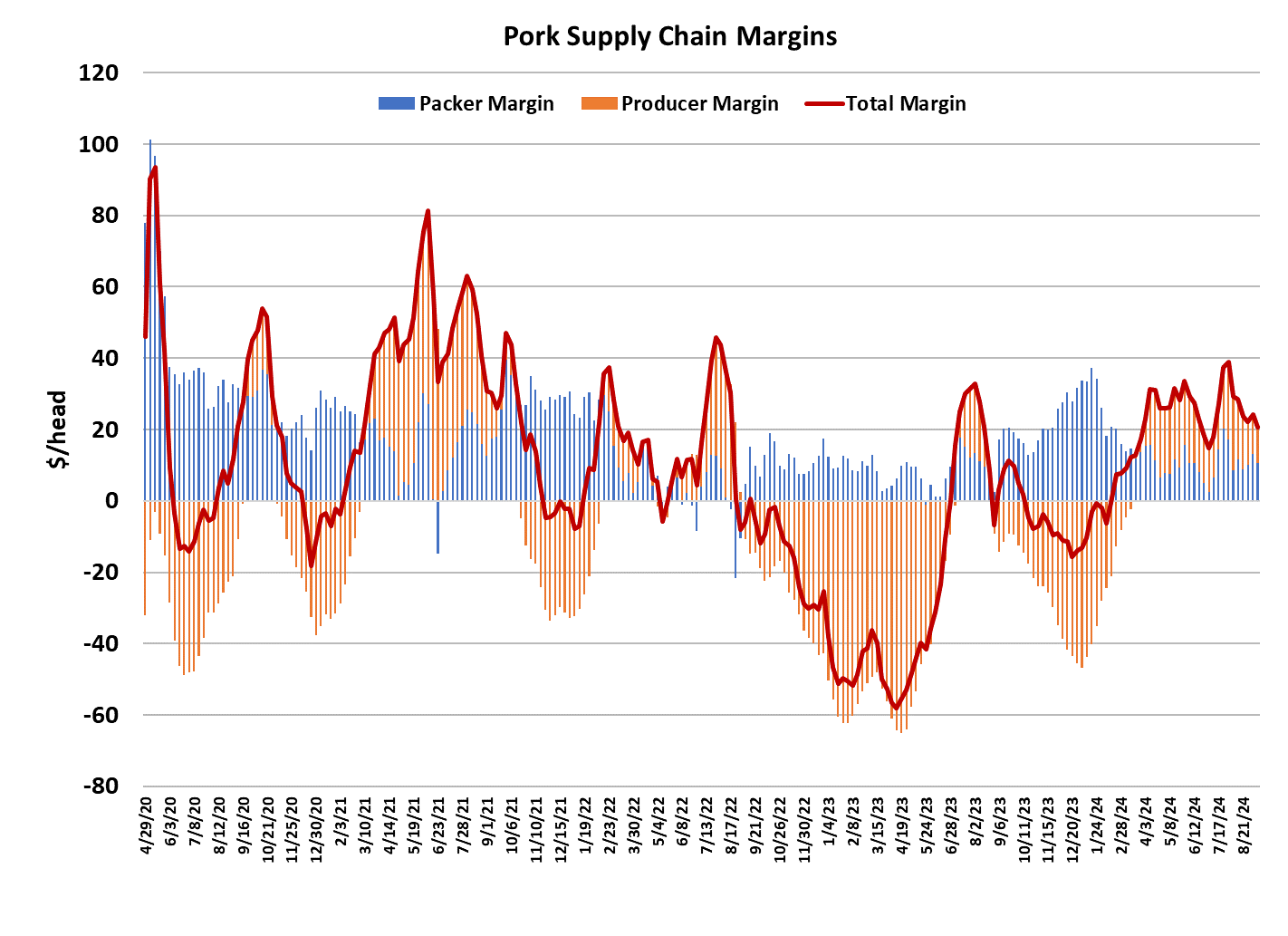

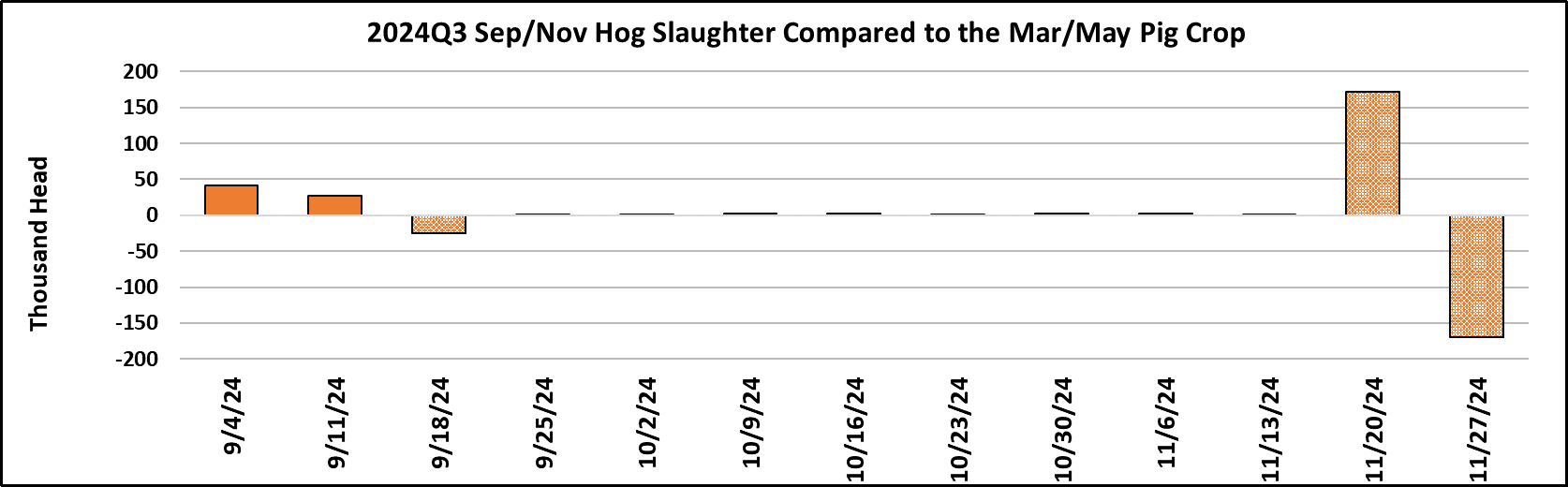

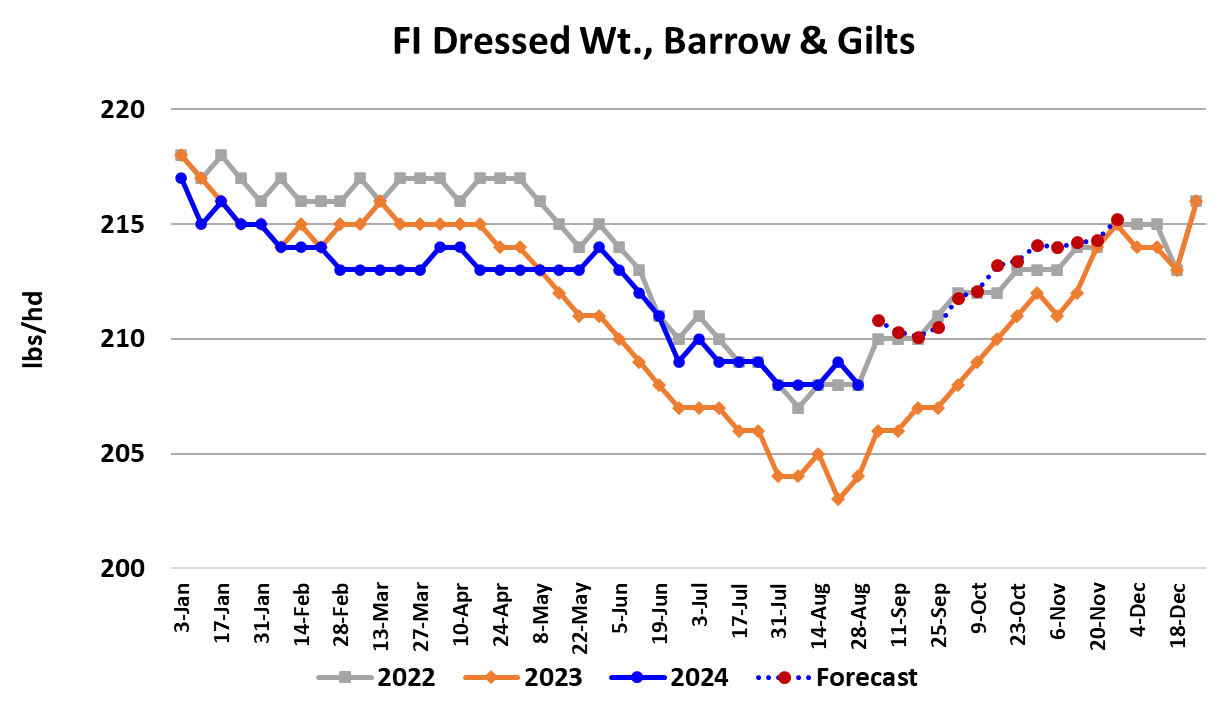

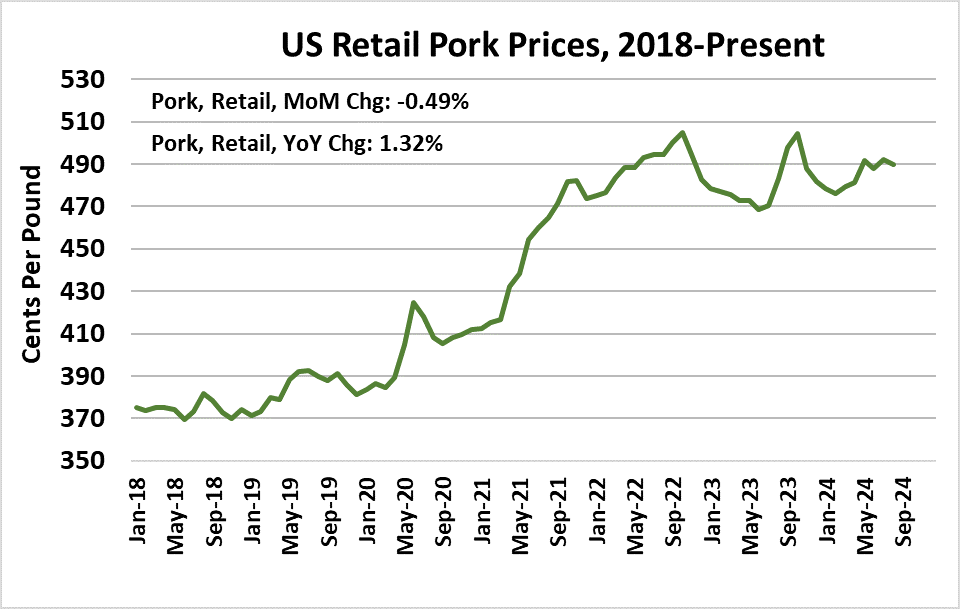

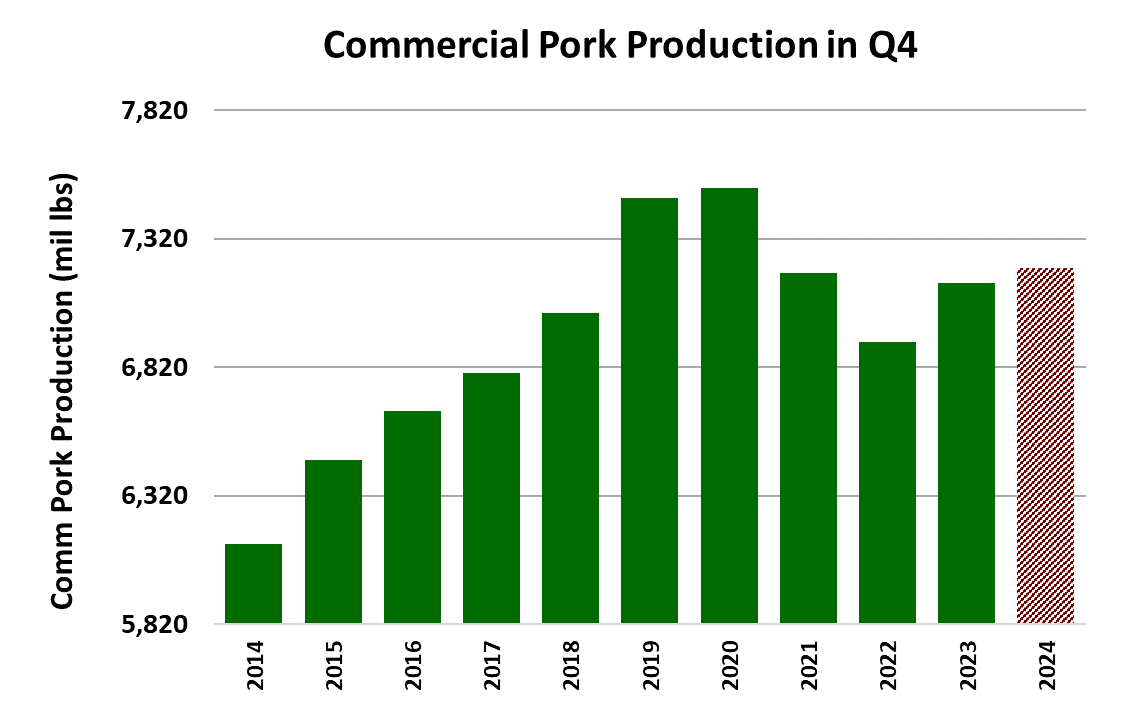

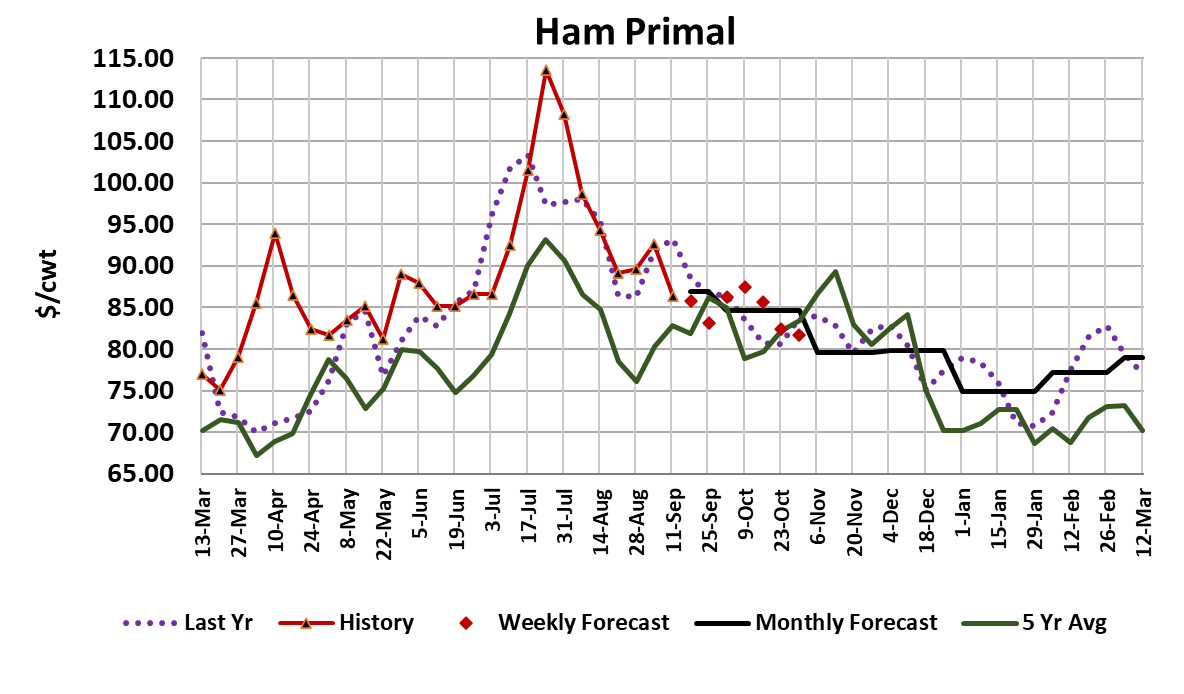

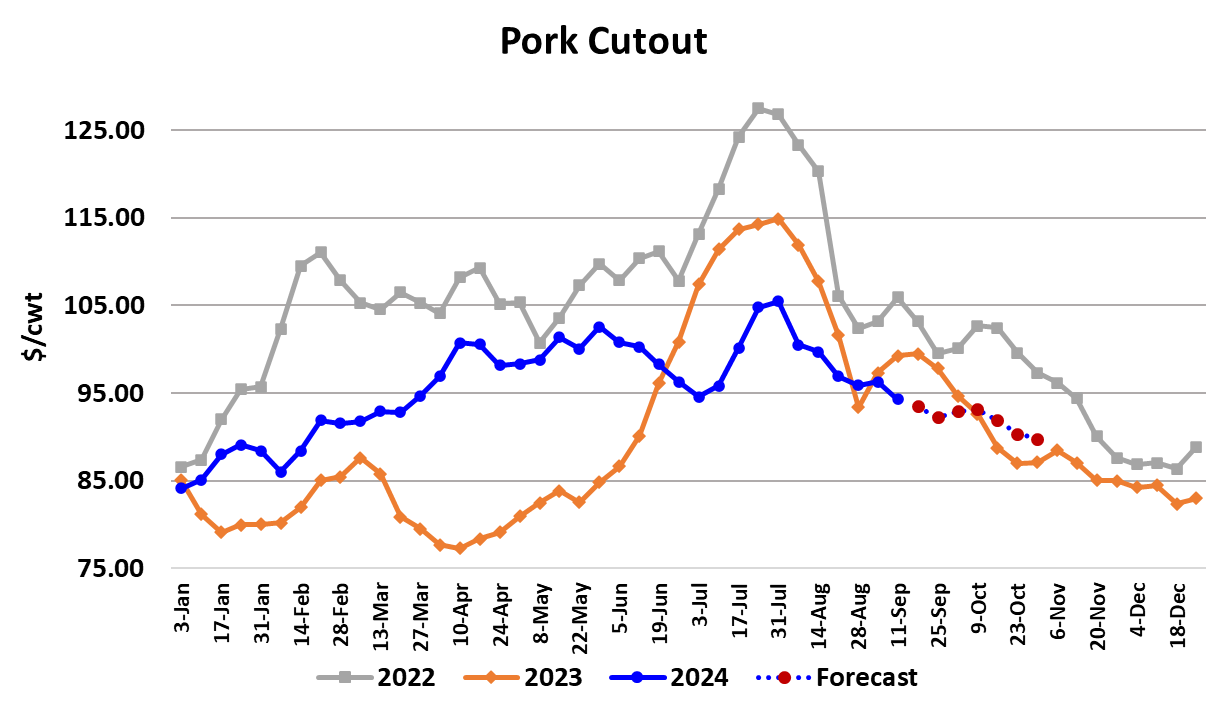

Prices in the hog and pork complex continued to leak lower this week, led by the cutout which lost a little less than $2 to average $94.30. Negotiated hogs in the WCB region were down $0.89 on a weekly average basis at $77.21. Packer margins compressed a little, now close to $11/head, down about $2 on the week. The lower pricing was widely expected as the industry ramped back up to full production following Labor Day week. The hams were the primal that exerted the most pressure on the cutout, while the belly and loin primals were close to flat on the week. The drop in ham prices was accompanied by very large sales in the spot market, so perhaps packers got any unsold hams cleaned up this week and will start next week with a tighter inventory position. The forecast has the ham primal holding in the mid-$80s through September and into October. Processors will be busy working on hams for the Thanksgiving and Christmas holidays over the next few weeks and that should keep ham demand from slipping much beyond this point. Belly prices are still in a downtrend, but the rate of decline is very slow and expected to remain that way. The primal averaged $123.41 this week and may not dip below the $120 mark until after October arrives. Trims, which also fall into the “processing items” category were lower this week with the fat trim losing almost $14/cwt. While the 72s were down closer to $4/cwt. The forecast trajectory for both of those items is lower, but the losses should slow substantially once we move into October. Prices for the retail items should also slowly ease over the next several weeks as slaughter inches higher. I read pork demand as “just ok” at that moment, but it is still weak in a longer-run context. October is pork month, where the Pork Board typically offers incentives to retailers for featuring pork, and in some years that seems to be supportive to prices, but only marginally so. The idea is to use increased promotions at a time of year when slaughter is very large to help clear product through the supply chain and thus prevent a significant hit to wholesale pork prices and hog prices. The combined packer+producer margin got back on its downtrend after a steady print last week, confirming that we are likely still in a near-term demand downcycle. Retail prices for August were released this week and the data indicated a slight decline from last month, but retail prices are still about 1.3% higher than last year. Persistently high retail pork prices remain a headwind for consumer off-take, but so far it hasn’t resulted in backlogs along the supply chain. With big Q4 production on the horizon, it sure would help if retail prices would decline at a faster rate than what was recorded in August. It seems that at present, the hams are the most price-volatile part of the carcass as everything else (except perhaps fat trim) is content to just slowly ease lower. That should make the forecaster’s job a bit easier because if he calls the hams correctly he is likely to also make an accurate call on the cutout. Of course there is always the risk that bellies could take a sharp step lower, but that hasn’t happened in a quite a while and with the belly inventory in cold storage running about 17% lower than last year, there is some room for cold storage to act as a “shock absorber” for prices, with users stepping in to buy the dips in the spot belly market in order to build stocks as a hedge against higher prices next spring. This week’s swine slaughter totaled 2.57 million head, which exceeded the forecast and was about 27,000 head larger than what the prior pig crop suggested. That makes two weeks in a row now where the kill has been moderately larger than the pig crop. If USDA’s pig crop estimate was correct, then the max weekly kill this fall should be around 2.68 million head—only about 100k more than this week. We are now at the point where most of the big increases in slaughter have already occurred and from here forward gains in the kill should be rather small week-to-week. As a result, the supply side pressure on prices shouldn’t be excessive going forward and that might mean that the cutout can continue to loose only a dollar or so per week. I’ve got next week’s kill forecast at 2.55 million head, with the cutout projected to average about a dollar lower. In two weeks, USDA will release another Hogs & Pigs report and I expect it will show the breeding herd down 3.2% YOY and the total swine herd almost flat with last year. The productivity increases that have been so prominent in the past few quarters should slow down and I’m projecting the pigs per litter variable to be about 1% higher YOY. The pig crop should be down about 0.7%, which isn’t a very big drop, and signals that there should be plenty of hogs around in the Dec/Feb quarter when this Jun/Aug pig crop heads to slaughter. Producers seem to have lost interest in paring back their herds and that attitude is at least partly being fueled by corn prices that are much lower than last year. They will also probably continue to feed hogs to heavier out weights this fall keeping carcass weights about 2-3 pounds stronger than last year. All of this points to ample pork availability over the next few months. Next week, look for more of the same—modest declines in most primals and a cutout that averages a dollar less than this week. Negotiated hog prices should also continue to ease, helping packer margins to expand slightly.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}