Pork Wrap September 10

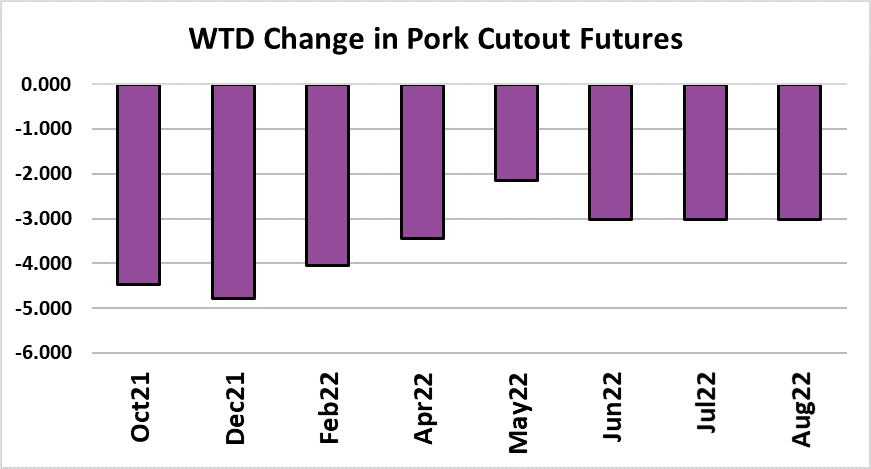

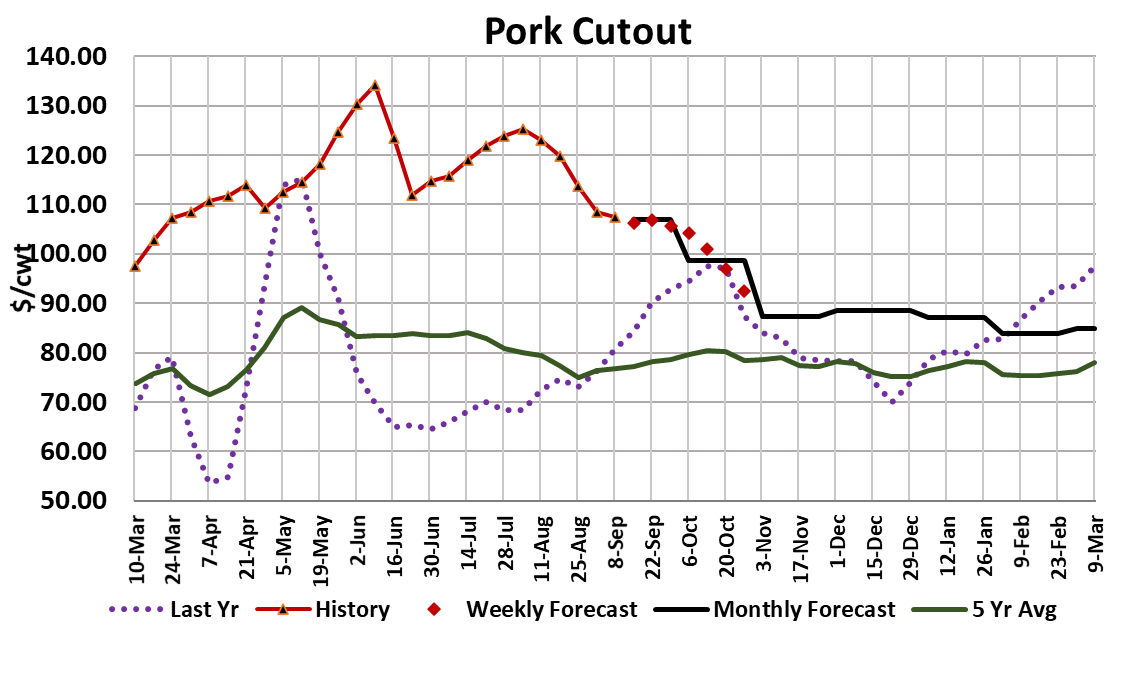

The pork cutout was down only a dollar on an average basis this week,

but by the way the futures market reacted, you would think it fell $10.

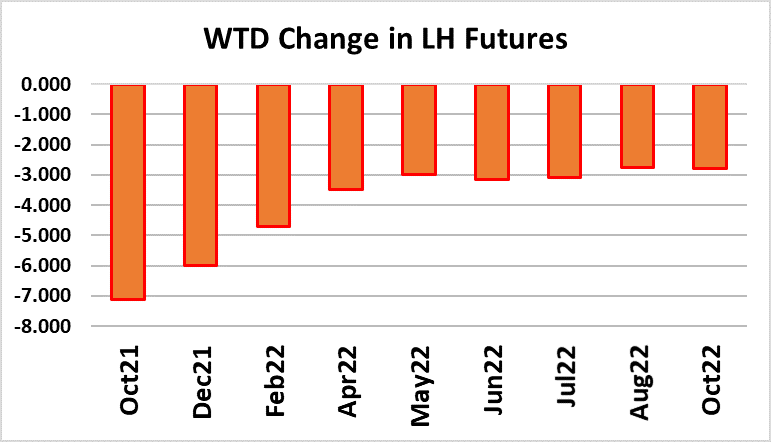

October LH futures were down every day this week, but the losses

really accelerated late in the week, and the contract dropped over $7 in

total. I think there was a contingent of traders that thought the cutout

would bounce in response to the short kills of the past two weeks, but

when that didn’t happen they became increasingly concerned about

what would happen to the cutout when kills return to normal next week.

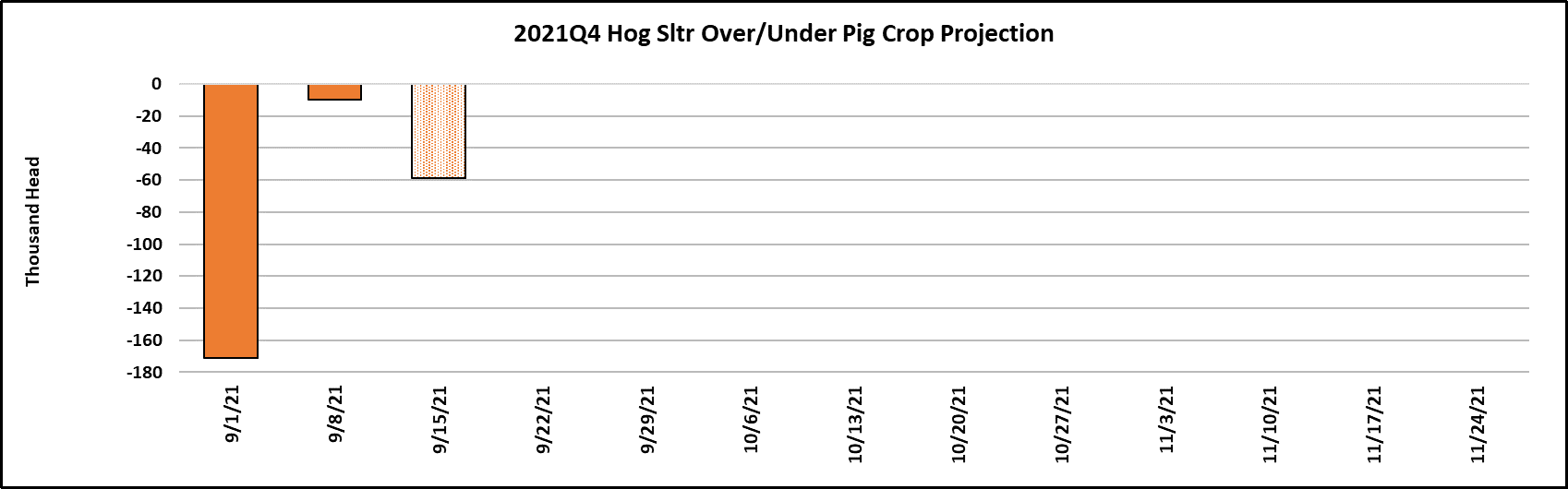

This week’s slaughter came in at 2.27 million head, and packers plan

to slaughter 370k tomorrow to compensate for Monday’s lost

production. Judging by the hog deliveries that packers have already

scheduled, it looks like next week’s kill will be over 2.5 million head.

Buyers can see that big production coming and will likely step back to

see how much price levels decline. Relative to the reported pig crop

however, this week’s kill looks small and next week’s should also fail to

match what USDA projected. Thus, through the first three weeks of the

Sep/Nov quarter, it is likely that slaughter will be about 250,000 head

below what the pig crop implied. So, the under-killing that we

witnessed all summer is continuing here in the fall. That is somewhat

bullish since the pig crop was estimated to be down 3.1% YOY and in

actuality it might be down as much as 5% YOY. If I simply go by what

USDA reported the pig crop to be, I’d have peak kills this fall right

around 2.68 million head—far below the 2.8 million head peak last year.

If USDA did indeed over-estimate the pig crop, then perhaps peak kills

might only reach 2.64 million head. So, in my mind, while the supply of

pork will certainly expand this fall, it is likely not to be nearly as

burdensome as what we’ve seen in recent years. If you combine that

with the thought that demand certainly looks like it will be a lot stronger

than in years past, it is hard to be overly bearish about the pork

complex this fall.

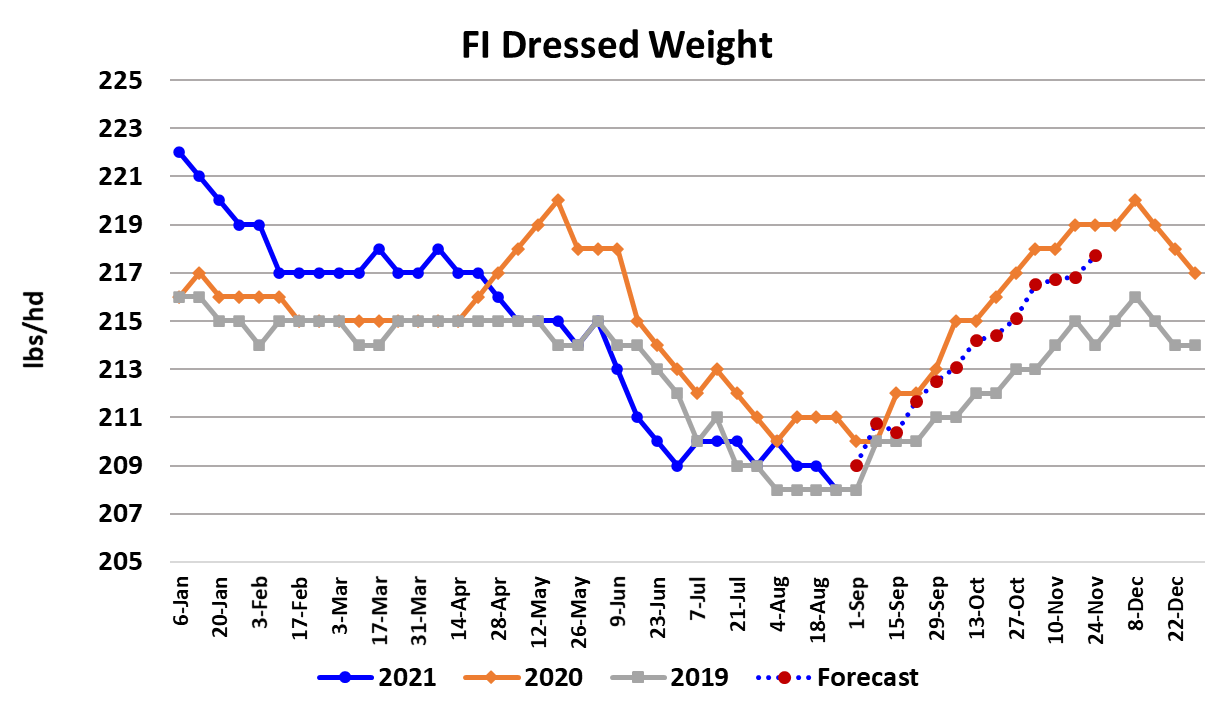

One of the mysteries in the past couple of weeks is how packers have

been able to persistently push cash hog prices lower when the weight

data suggests that hog producers are still pretty current. USDA

reported the all-swine carcass weight down another pound this week,

matching the low set back in 2019. So, the hogs are clearly not overly

heavy. Now, weights should increase from this point forward and that

will give hog producers less leeway in their marketing windows, but for

now it doesn’t appear as though we have backed hogs up in the

pipeline. This week cash base prices in the Western Corn Belt

averaged $90.28, down $3.36 and the LHI averaged $98.14, also down

about $3.30.

Due to very high corn and soymeal prices this summer, producer

breakevens on hogs are around $92/cwt. Producers are still

profitable until the LHI drops to about $91-92. I expect that to

happen in early October. As hog supplies grow seasonally,

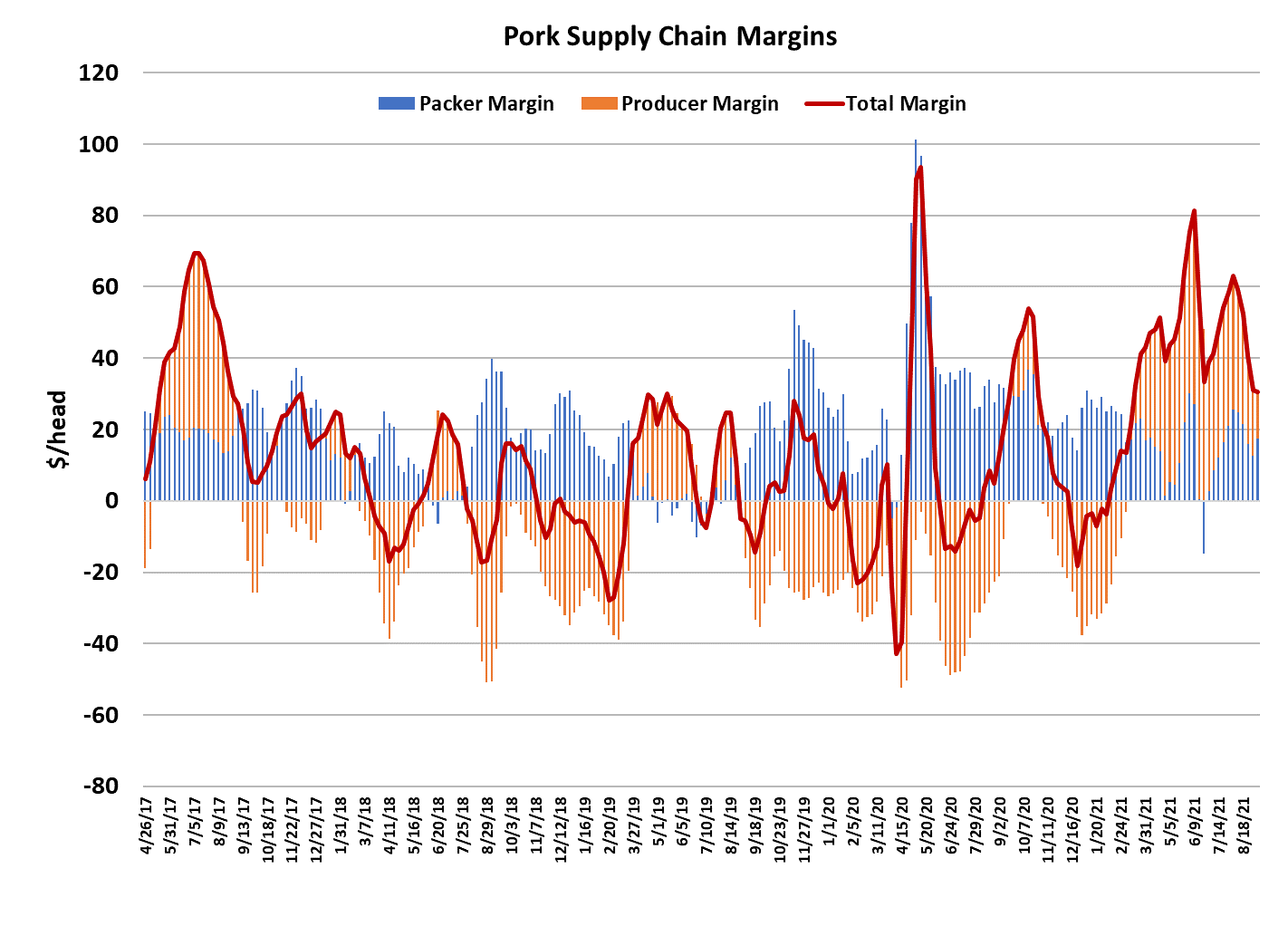

packers will have more leverage and their margin should improve.

This week margin was up about $5 to $17.50/head and by early

October that could be approaching $30 head. Sometime around

mid-October we will gain more insight into the labor situation in

packing plants because available hog supplies will start to test

packing capacity.

If the labor is there to get all hogs slaughtered, then packer margins

will probably hover in the “normal” fall range of $30-45/head.

However, if labor is insufficient to process all of the hogs, then we

could see packer margins balloon out to $70/head or more. On the

demand side, the combined margin chart is telling us that pork

demand is on the down swing at the moment, but this week’s

decline wasn’t very large. Could demand be making a bottom

here? Maybe, but I think the action in the futures is likely to spook

pork buyers onto the sidelines next week and that will show up as

further demand weakness in our analytics. We’ve been watching

the ham market closely for signs that it is near a bottom and, while

that hasn’t been confirmed yet, the declines in the ham primal have

been smaller in recent days, so a bottom might be close at hand.

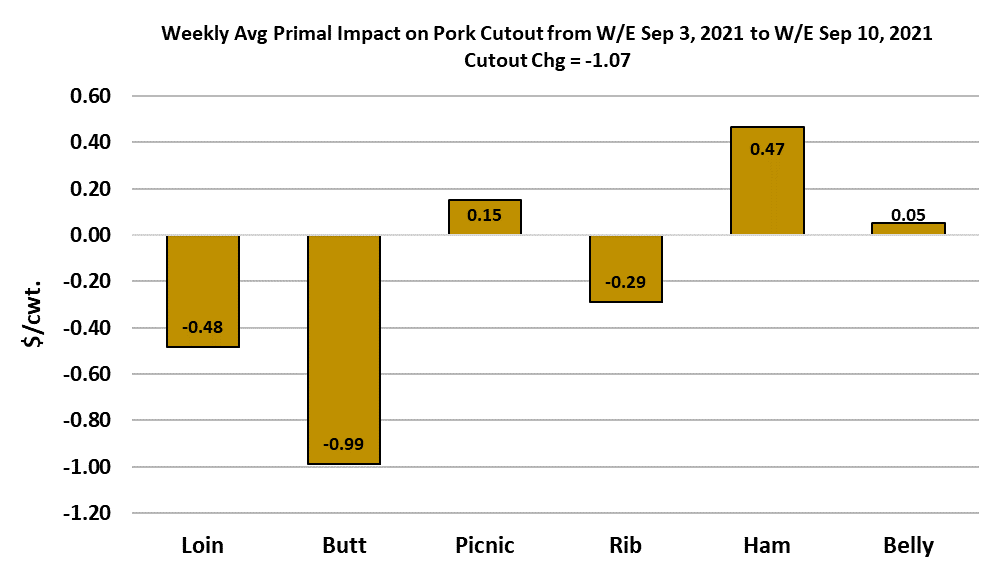

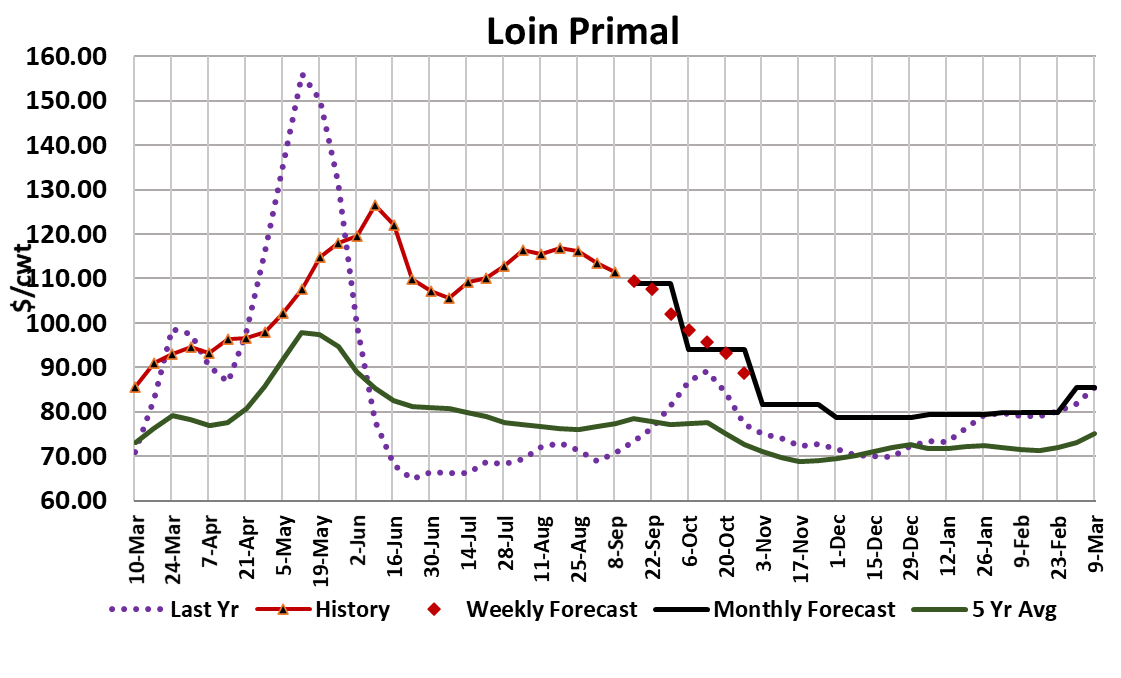

This week it was the retail items that weighed the most on the

cutout (chart below), while the bellies and hams actually provided a

tiny measure of support.

Pork volume was strong this week, so perhaps packers will come

into next week well-positioned. Much will depend on how pork

buyers react to this week’s sell-off in the futures. The magnitude of

the futures drop was reminiscent of what happens when an “ASF in

the USA” rumor is circulating, although no evidence of that has

surfaced. My guess is that the futures will rebound early next week

but are not likely to add more than about half of what they took off

this week. Next week, watch those retail cuts to see how they hold

up under the pressure of a big Saturday kill and a full production

week. Beef prices are now declining quickly, so pork’s advantage

in the fight for retail ad space will be diminished.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}