Pork Wrap September 08

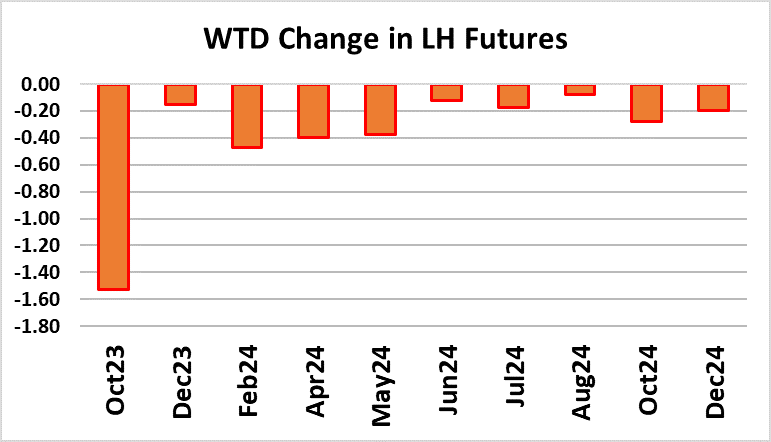

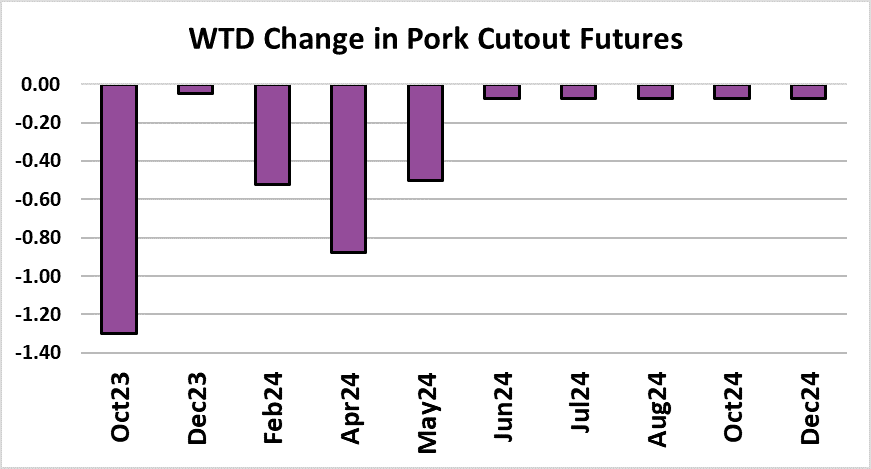

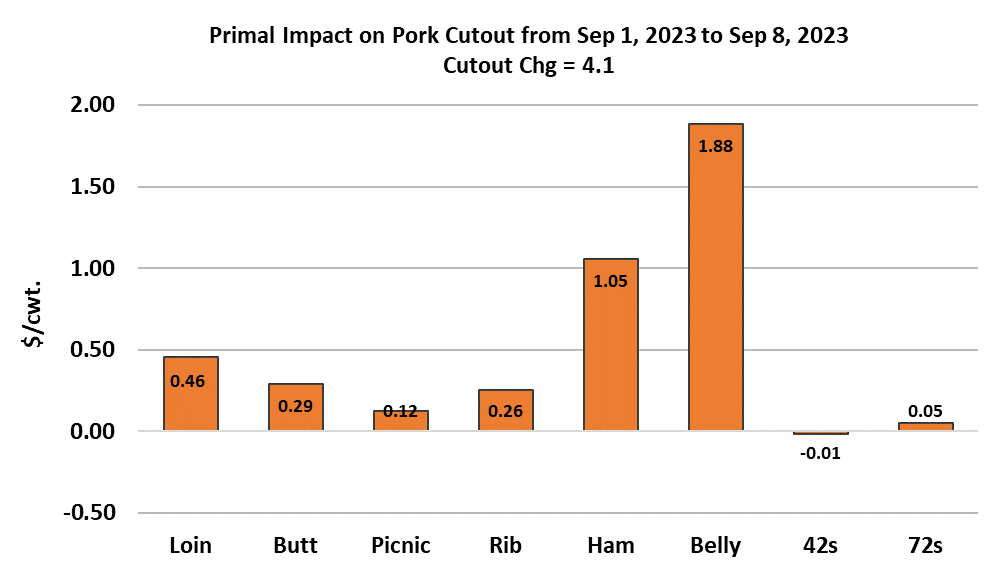

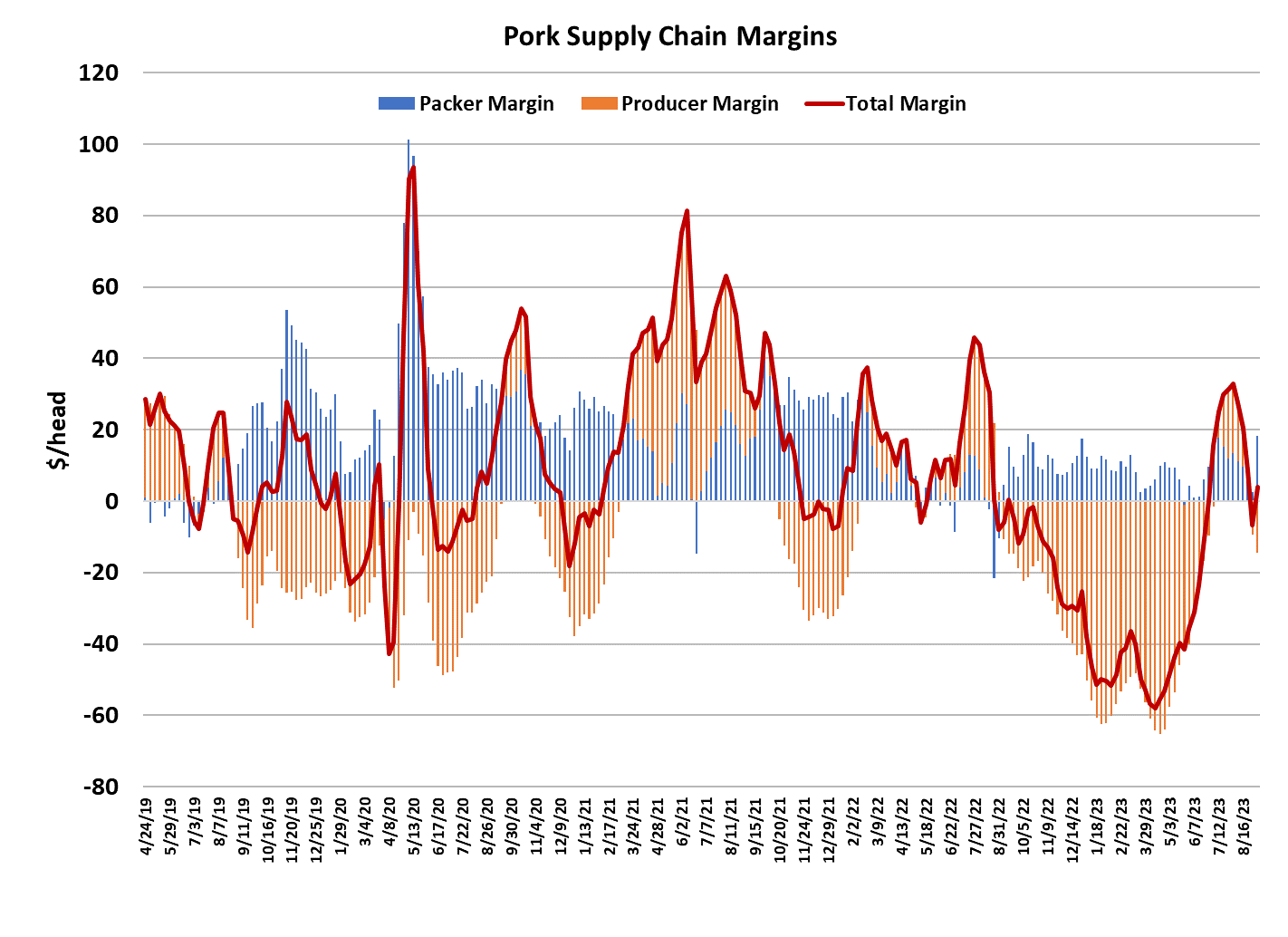

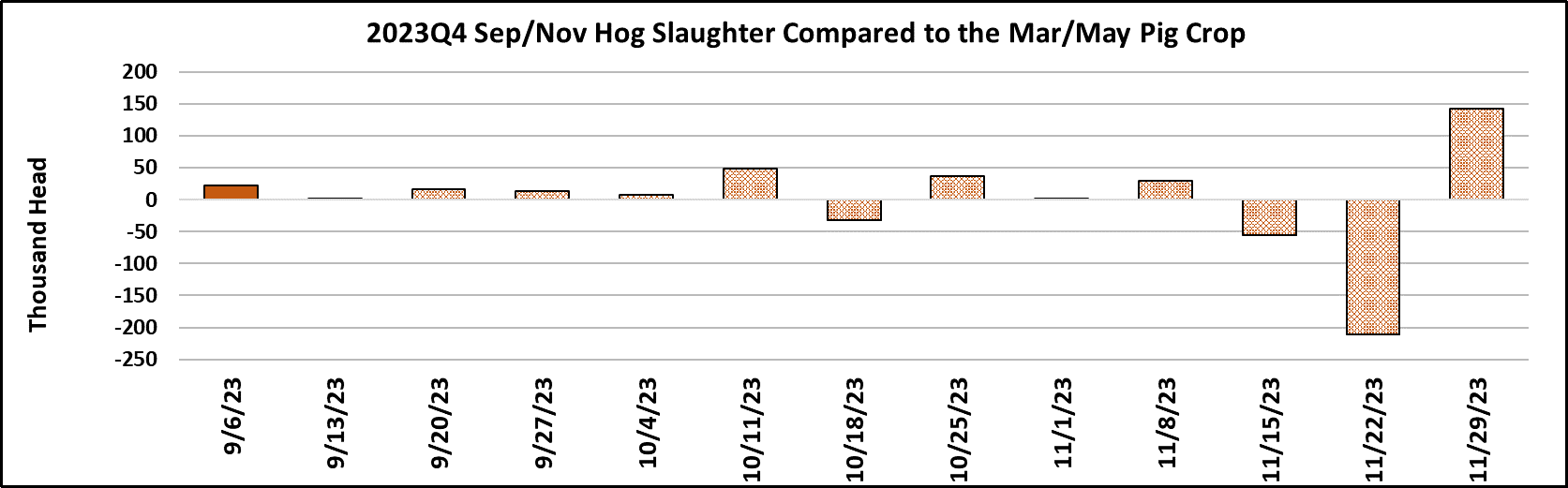

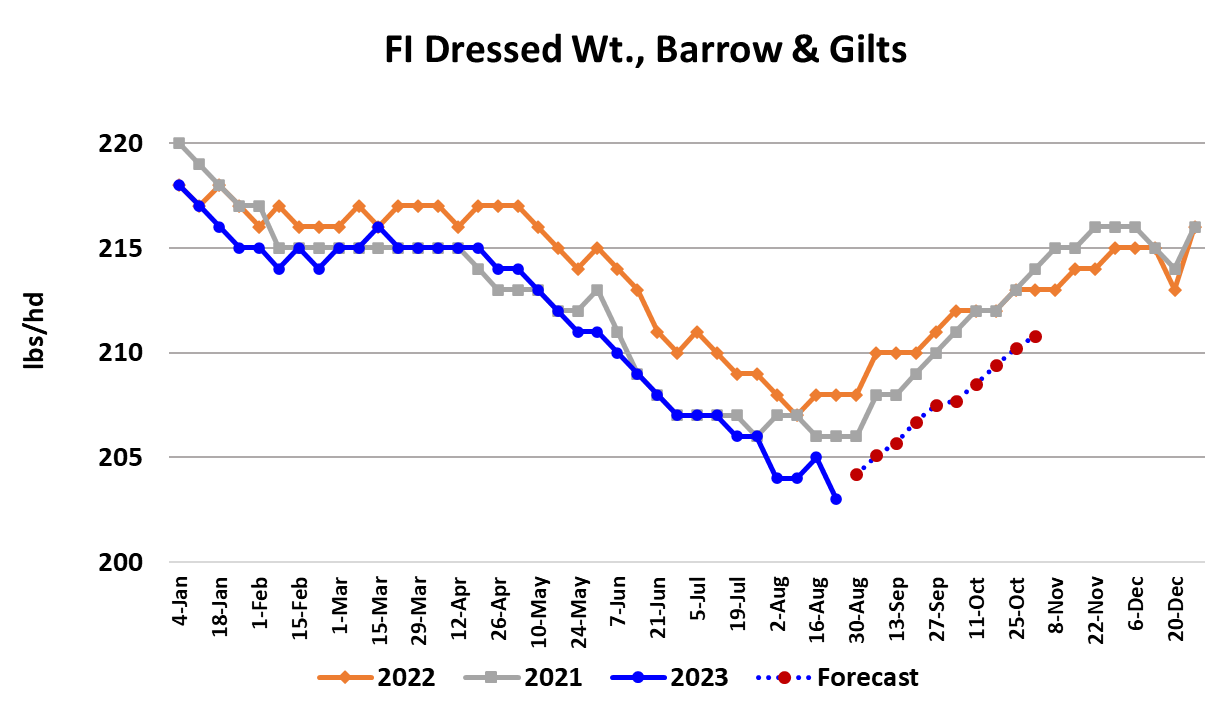

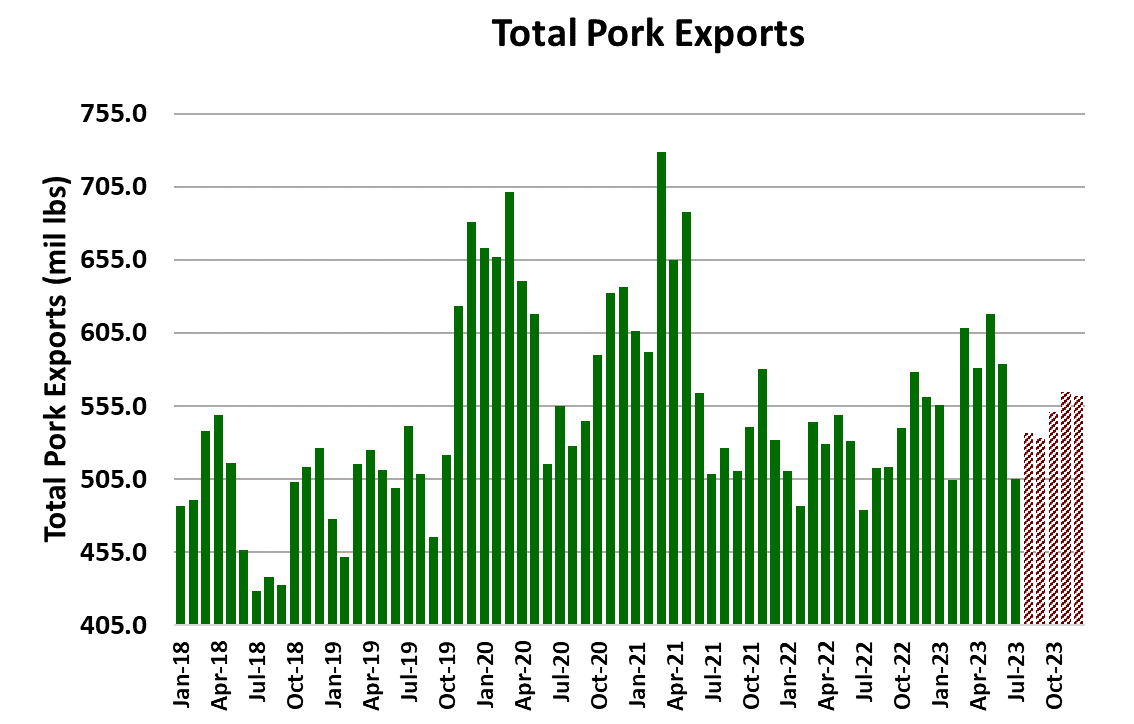

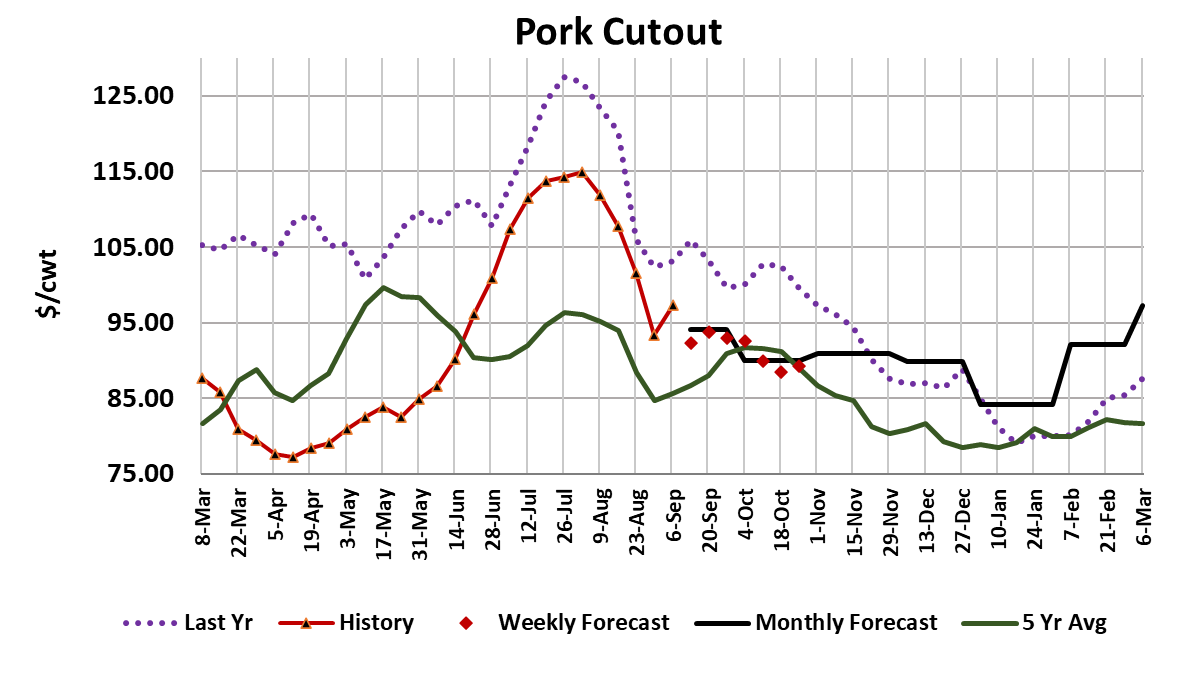

The pork market got a little goofy this week as small volume trades at much higher prices in the bellies helped push the cutout back into the $98-99/cwt. area. It is unlikely that the cutout will hold up here now that production is back to normal following the holiday, but for a few days it has given the bulls something to cheer about. I’m not ready to call a bottom in the belly market just yet because this week’s prices were not very representative due to light volume. I honestly think that the hams are going to be a bigger driver for the cutout next week. The price action this week in the ham market looks like it has bottomed and will trade higher in the near-term. The retail items were also higher this week, partly due to small production, but I also think that there was a bit on demand improvement coming into those markets. This week’s cutout averaged $97.30, which was up $3.91 from last week’s average. The negotiated hog markets were lower as one might expect in a holiday week. The WCB negotiated cash market dropped $2.60/cwt. on a weekly average basis to $79.32. With the cutout moving higher and cash hogs lower, packer margins soared to $17/head, up $2 from last week. Of course some of that is artificial due to the belly move and I’d look for a significant retrace in margins next week. This week’s kill was about 2.23 million head as nearly all plants were dark on Monday. Packers tried to compensate by killing 348k on Saturday. Needless to say, packers’ coolers will be full of fresh pork next week and that may necessitate some price concessions in order to keep inventories manageable. The forecast for next week’s kill is 2.48 million head and after that it should be over 2.5 million head per week until the end of the year, outside of holiday weeks. Carcass weights are light and were reported down another pound this week. That should be the low for the year and weights should work higher for the next few of months. USDA’s estimate of the March/May pig crop suggests that slaughter levels during the Sep/Nov quarter that we just entered, should be up about 0.8%. It looks to me like the light carcass weights will more than offset the increase in slaughter and thus overall pork production should be down slightly YOY in the remaining four months of 2023. Exports could be a little larger than last year also, so that points to slightly reduced domestic availability for pork this year in Q4 compared to last year. The bigger unknown is what pork demand will look like in the upcoming quarter. On the positive side of the demand ledger, pork demand could get some boost from very high retail beef prices and it is possible that exports will outpace what I have dialed in. On the negative side, there is the potential Prop 12 effect reducing demand for pork in California, student loan repayments restarting in October and the risk of further softening in the US economy. My current price forecasts for Q4 have impounded demand that is about 5% weaker than last year, so I may be a little too pessimistic on demand this fall, but I’m definitely leaning towards not-so-great demand to finish out the year. We will get another issue of USDA’s Hogs and Pigs report on Sep 28 and I will be really surprised if that doesn’t show some meaningful reduction in the breeding herd. Sow kills ran strong all summer long and that liquidation is likely to continue this fall. The first signs of tightening in the hog supply due to this summer’s breeding herd reductions won’t show up until December or January, but it will be welcomed by producers and hopefully will help them escape the dreadful margin predicament they were in last winter and spring. It doesn’t look to me like futures traders are adequately respecting the potential for supply reduction in 2024 and the positive impact that would have on prices. Maybe the upcoming H&P report will change their thinking. USDA gave us the trade numbers for July this week and those were encouraging, showing total pork exports up 4.3% YOY in a month where pork prices were seasonally high. So far in 2023, pork exports have been up YOY in every month. For 2023 as a whole, look for exports to be up from last year in the neighborhood of 6%. Near-term, things should get back to normal next week now that the holiday has passed. Traders will be concerned with how well the market handles the seasonal increases in production. Packer margins should improve and producer margins should shrink. Look for the cutout to move lower next week and cash hogs right along with them.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}