Pork Wrap September 01

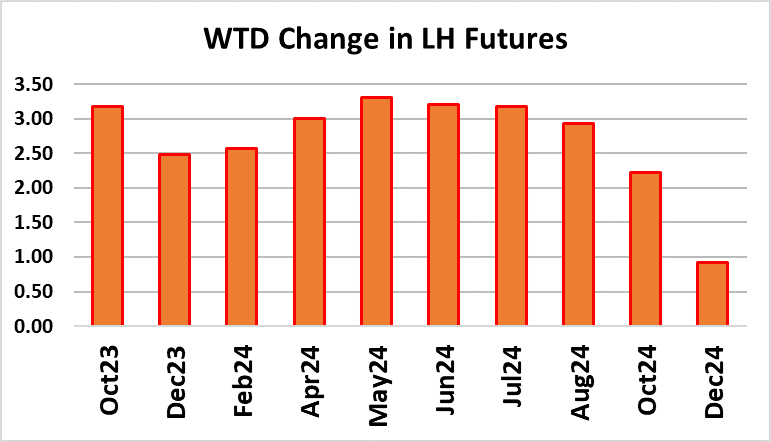

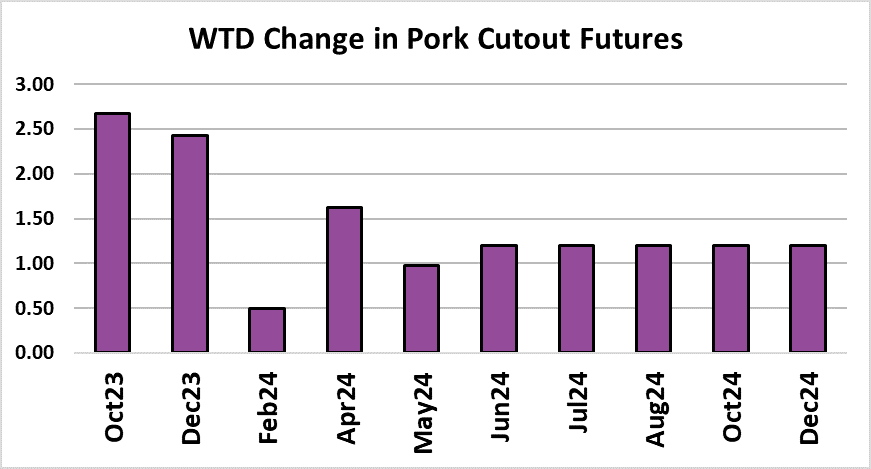

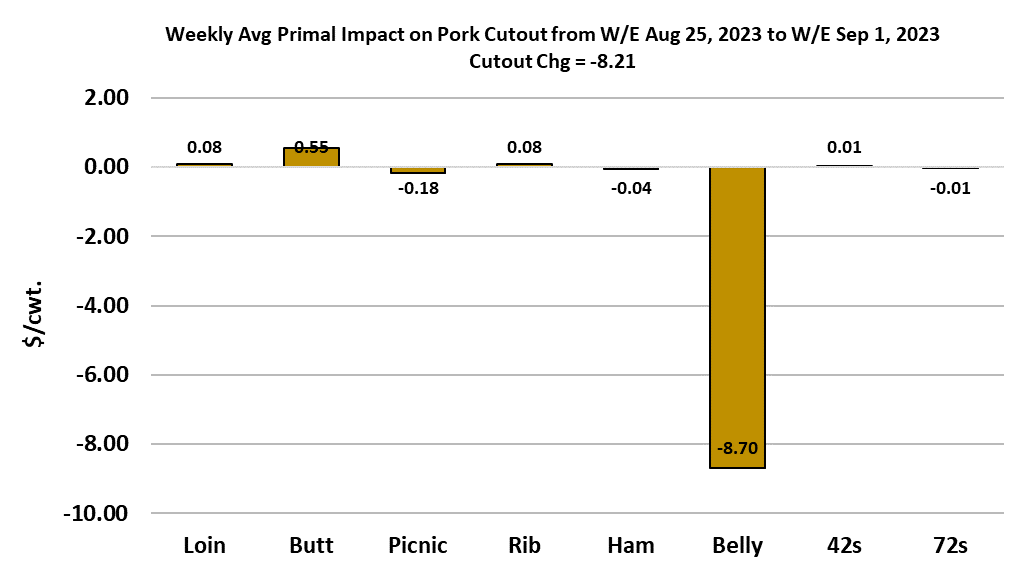

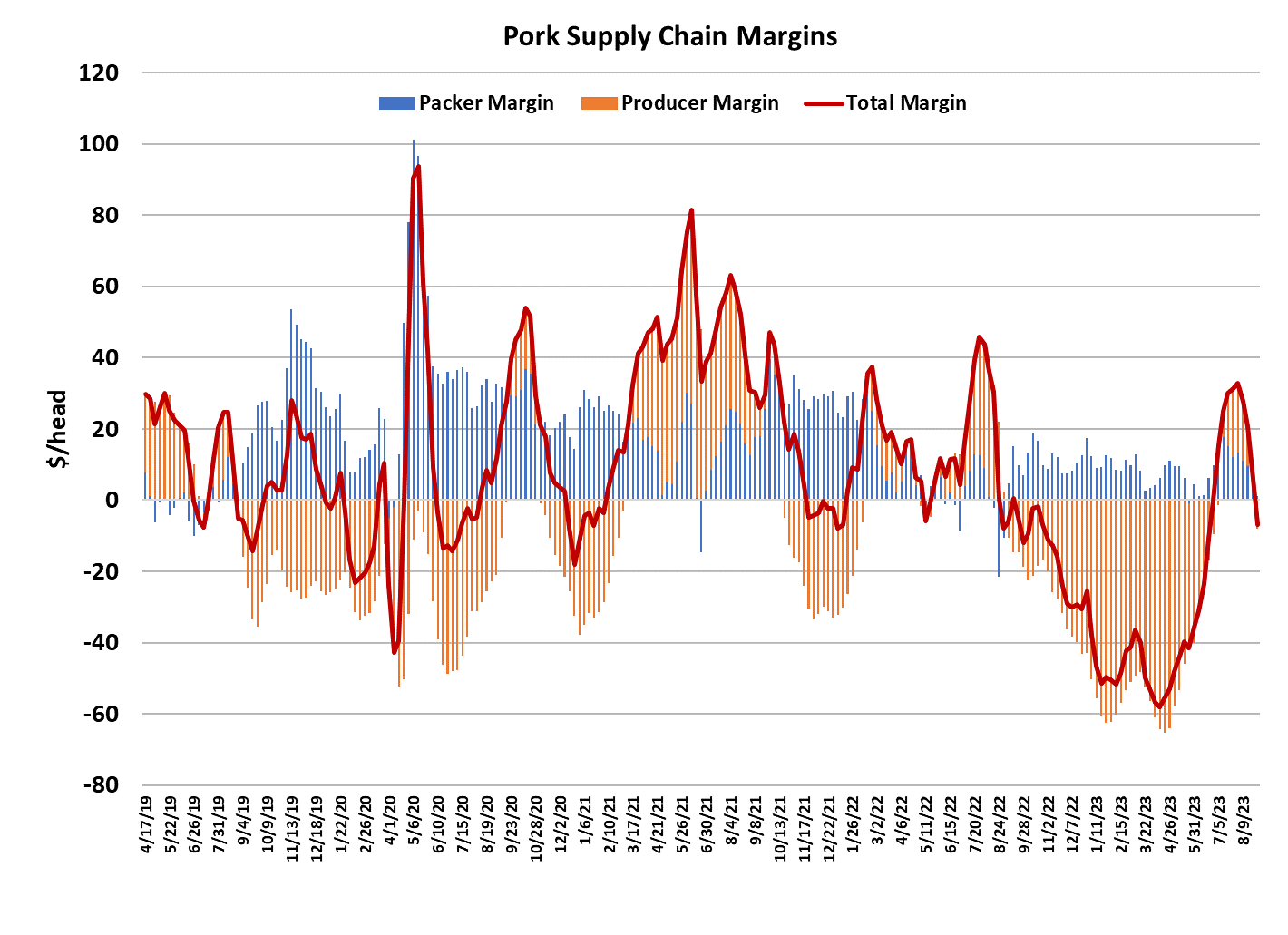

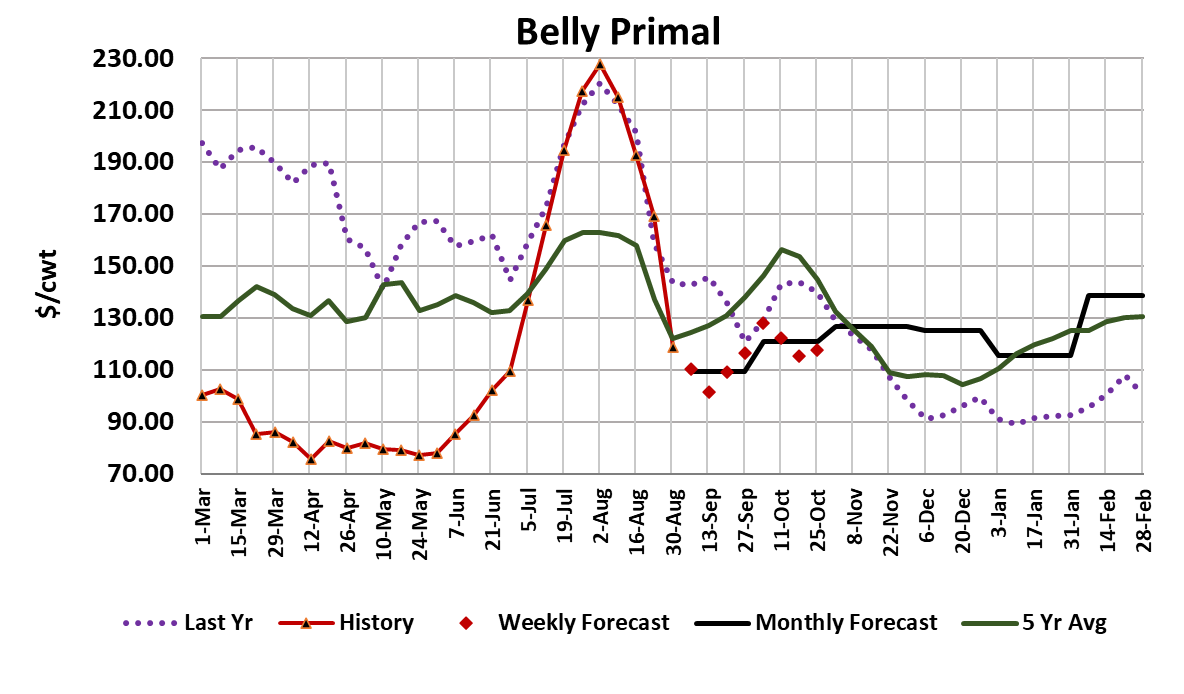

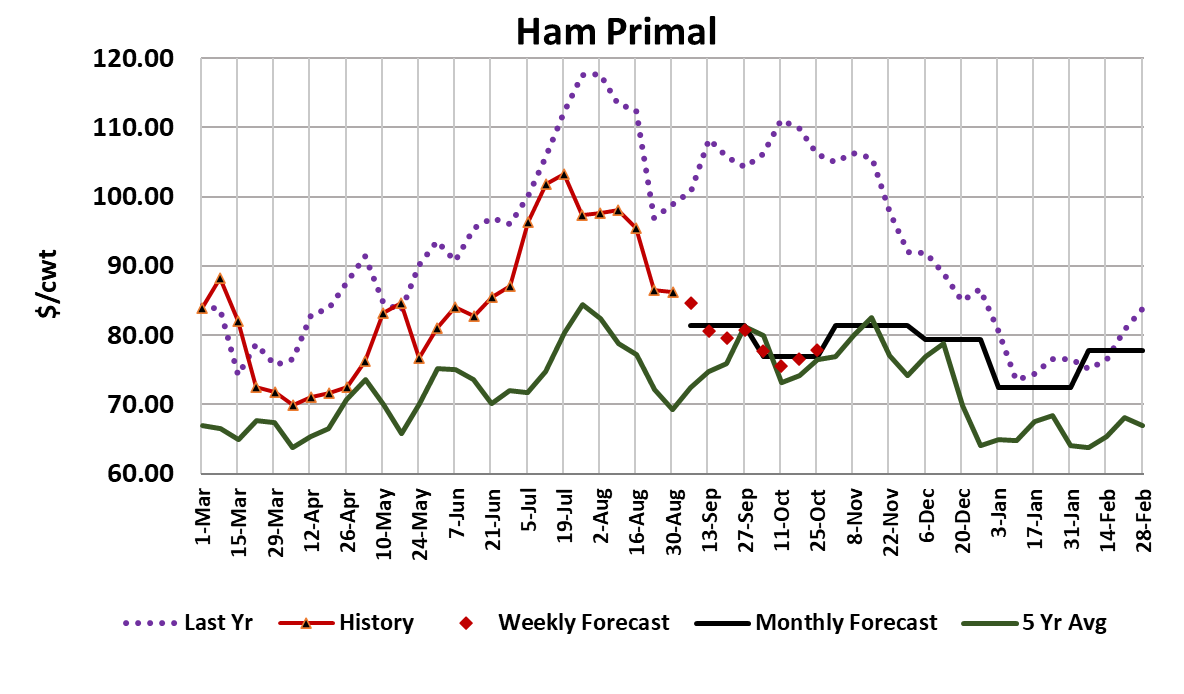

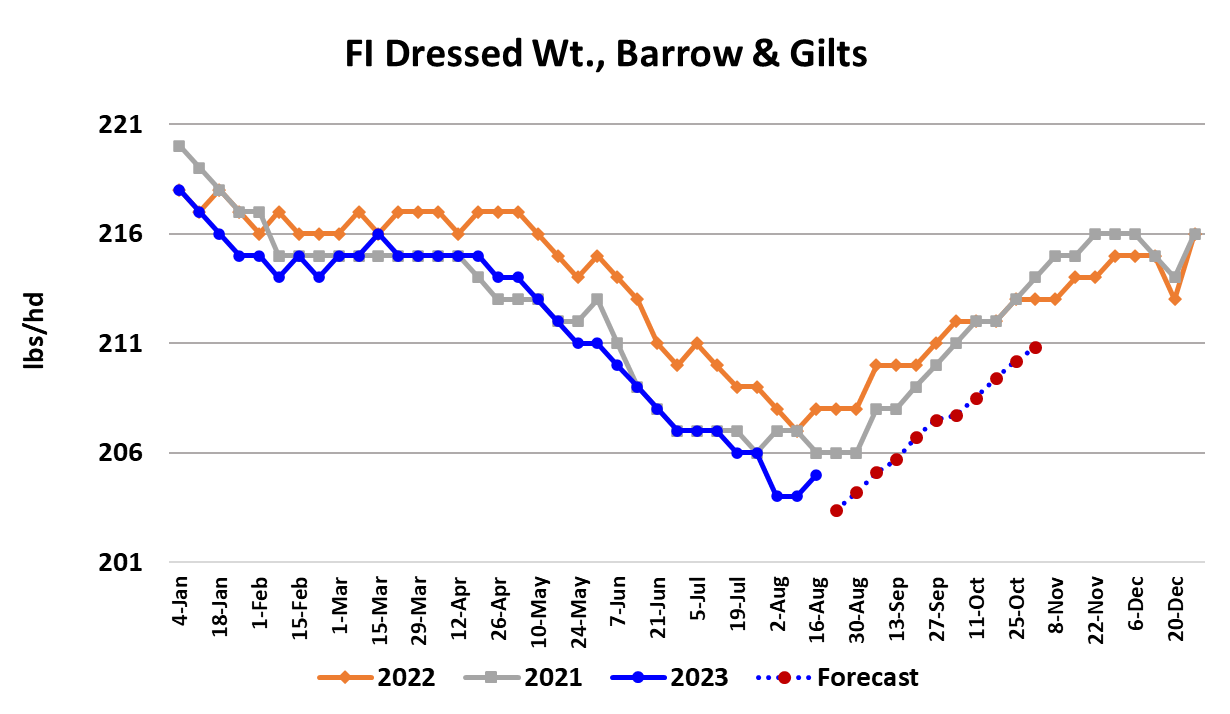

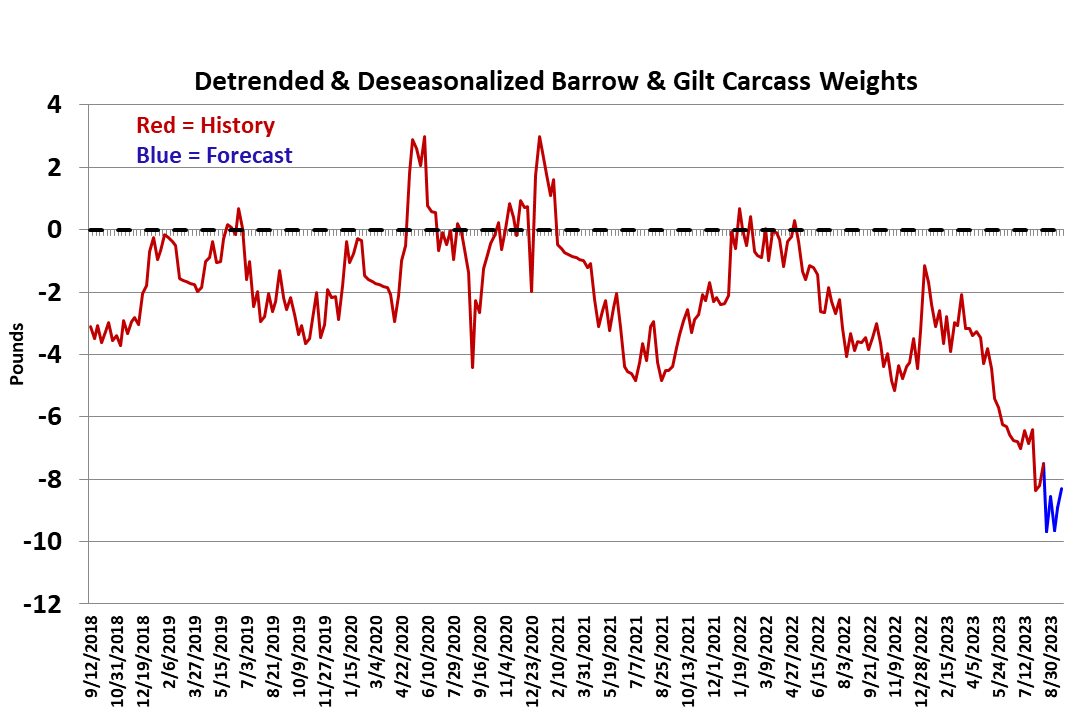

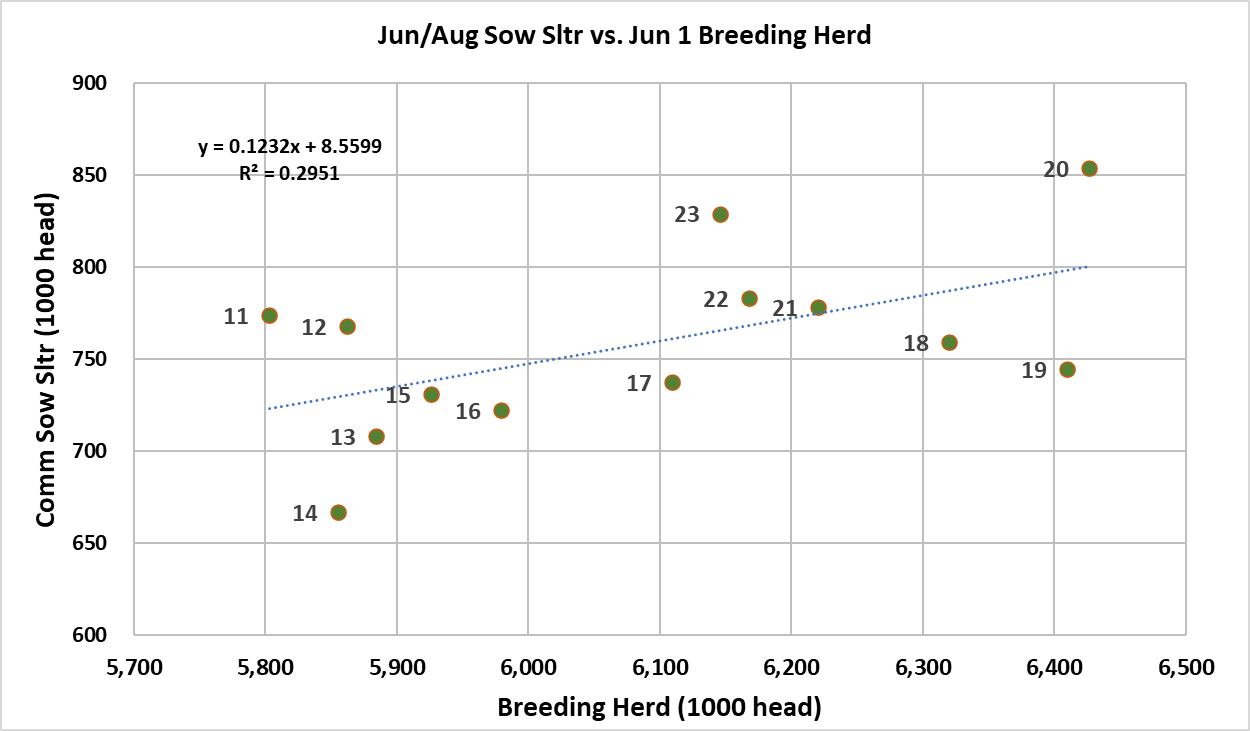

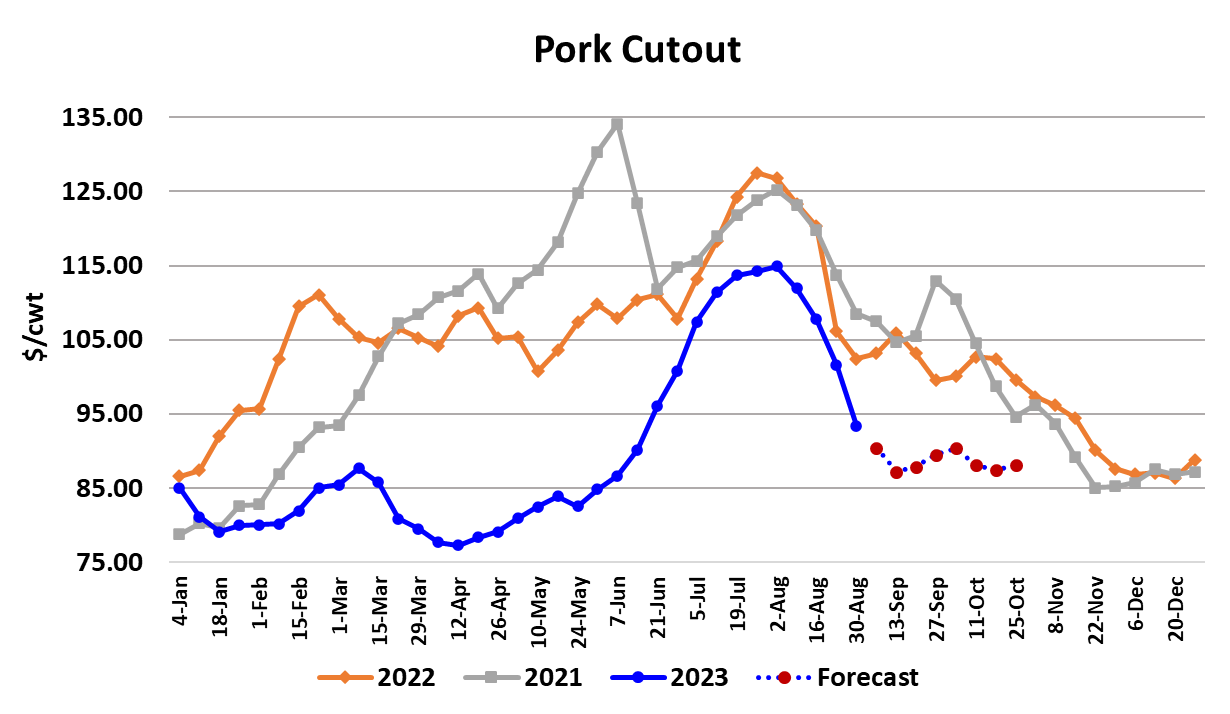

Bellies continued their correction this week, pressuring the cutout down $8.21/cwt. to average $93.39. In response, packers pressured cash hog prices lower, with the WCB negotiated price dropping $6.84/cwt. to average $81.91. The declines in the cutout and cash hogs are still working their way into the LHI, so this week’s packer margin of only $1/head will likely improve next week once the LHI has caught up. Still, packers can’t be too happy about their margin situation right now since margins should be expanding, not contracting, as we move past Labor Day. That likely means that they will be conservative with the kill until their margin picture improves. They will get some help in that regard from the Labor Day holiday. Saturday’s kill was very small at only 21,000 head, bringing the weekly total down to 2.39 million head. Next week, it looks like packers are scheduling about a 300k Saturday slaughter in an effort to partially make up for a zero kill on Monday. I have dialed in 2.19 million head for next week’s total. After that, it will be back to a steady diet of 2.5 million+ kills per week, heading toward a peak of 2.6 million head sometime in November. How will the market handle that? Well, futures traders seem to think it will be no problem since they have been holding the Oct contract in the $83-84 range, just a $2-3 under the $86 that appears to already be baked into the LHI. If it holds there, that would be an abnormally tight basis with still six weeks to go before expiration. Traders are probably thinking that the downward correction in belly prices has now run its course and absent that, the cutout shouldn’t see declines like this week moving forward. Personally, I don’t think that the drop in belly prices is done yet, but the magnitude of the decline in the next couple of weeks is likely to be much smaller than what we saw over the past three weeks. The attached chart on the belly primal shows how closely prices tracked last year over the summer. However, they have now fallen substantially lower than they did at the end of August last year, when they flattened out for a couple of weeks before taking another leg down. My guess is that belly prices will run below last year through October but then trade above the very weak prices that started to be reported near the end of last year. If I’m right about the bellies, then it is going to be hard to get much lift out of the cutout in the next couple of weeks. The current forecast has the cutout easing into the $86-87 range by the middle of September and then trading sideways to a little higher until the middle of October. As the down move in bellies slows, attention will turn to the hams because they will once again become this biggest driver of cutout changes. The ham primal was only down slightly on an average basis this week and I suspect that traders who are long the futures are expecting the hams to rally like they did last year in the fall. However, my thought is that the incredible strength in ham pricing last fall was largely a function of super-high turkey prices last year, as buyers shifted away from turkeys and towards ham. That dynamic isn’t present this year since turkey production has rebounded sharply following last year’s avian influenza outbreak and price levels for turkey are way lower. As a result, my forecast has hams continuing to ease lower once production picks back up after the holiday. The item that has provided the most support to the cutout in the last couple of weeks has been butts, which have posted a counter-seasonal increase after a big collapse this summer. I don’t think that is going to last either, and we should see those prices ease a little once production returns to normal. Loins, the other major retail primal, normally work lower post Labor Day and that should be the case again this year. None of these are major moves, but together they add up to a modest negative move for the cutout during September. There has been a lot of interest in hog carcass weights lately as the daily data provided by USDA is showing barrow and gilt weights down three pounds from last year. The weather in the Midwest has also been hotter than normal in the past week and that is forecast to continue into next week, so the thought is that hog weights could remain rather light for a while. We have certainly seen the evidence in the DTDS weights, which are hovering near record lows at -8 pounds and are projected to decline even further in the next few weeks. Normally, this would be a very bullish signal since it implies that packers are pulling harder than they should on the hog supply. However, these super-low DTDS weights have been part of the picture all summer long and it hasn’t really resulted in any abnormally strong pricing in the cash hog markets, so I don’t expect it to suddenly become a big influencer this fall. Maybe the reason that weights have fallen so much is that producers are in liquidation mode and eager to market hogs rapidly, so rather than being a strong “pull” from packers, this event might be more of a strong “push” from producers. Packer margins this summer were better than expected and thus didn’t suggest that packers were having any trouble finding hogs. If that was the case this summer, then it should be even easier for packers to find hogs this fall as availability increases seasonally and the pig crop being killed this fall was estimated to be about 1% bigger than last year. Even so, it is clear that very low hog weights are the biggest, and perhaps only, near-term bull argument in the market right now, so we need to keep a close eye on it. It is pretty clear that producers were busy liquidating sows this summer. The attached scatter shows how high Q3 (summer) sow slaughter has been relative to the breeding herd that USDA reported on Jun 1st. Liquidation appears to be approaching 2020 levels and that was a big liquidation year. That is very bullish in a longer-run context, as it will start to limit hog slaughter in the upcoming Dec/Feb quarter. That suggests to me that this could be one of those rare years where pricing in December is higher than in October, or at least much closer to October than normal. Yet, the futures are going in the other direction, keeping the Dec futures at a roughly an $8 discount to the Oct contract. Maybe that has to do with fears over Prop 12 enforcement later this year resulting in lower pork pricing outside of California, but it is really strange that we aren’t hearing much talk about Prop 12 anymore. Traders thought Prop 12 was a huge deal this summer, but after there was no discernable effect initially, it dropped off of their radar screens. That might be a mistake. Still, I think the supply curtailment due to sow liquidation will be a bigger influence on pricing and so have the cutout averaging slightly higher in Dec than in Oct this year. Next week, I wouldn’t rule out a small increase in the cutout due to the short kill but would expect it to be rather short-lived. Years ago, one of my hog market mentors commented that “everything changes after Labor Day” in the hog market, meaning that suddenly traders start to wonder where all of the hogs are coming from, and then adjust their pricing expectations downward. It will be interesting to see if that holds this year.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}