Pork Wrap October 6

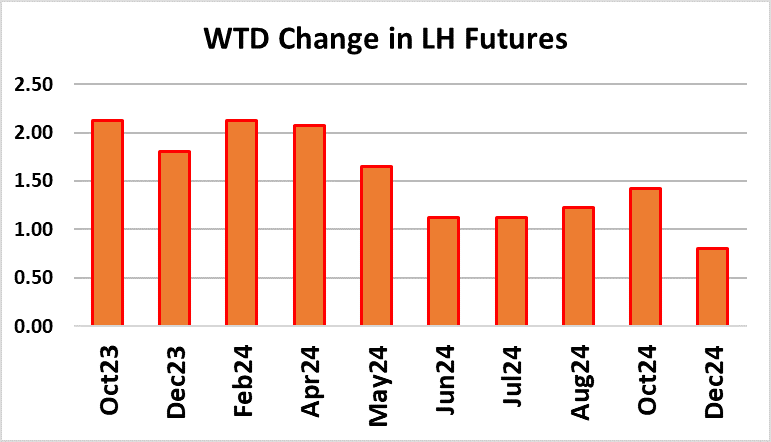

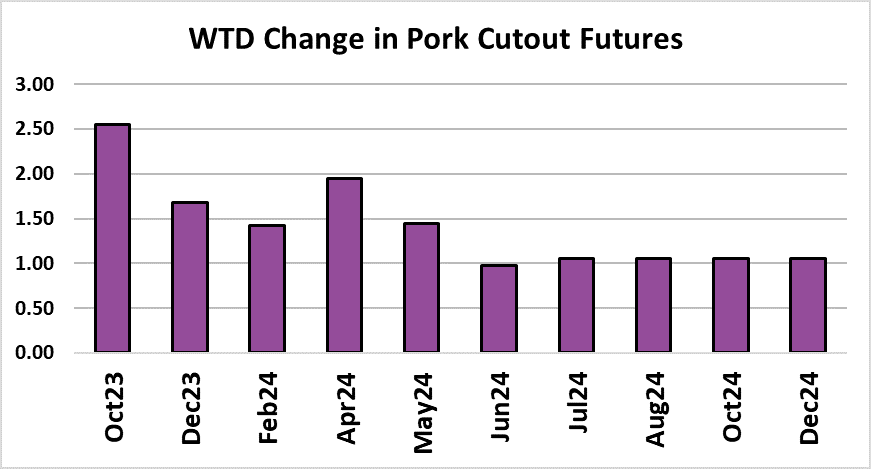

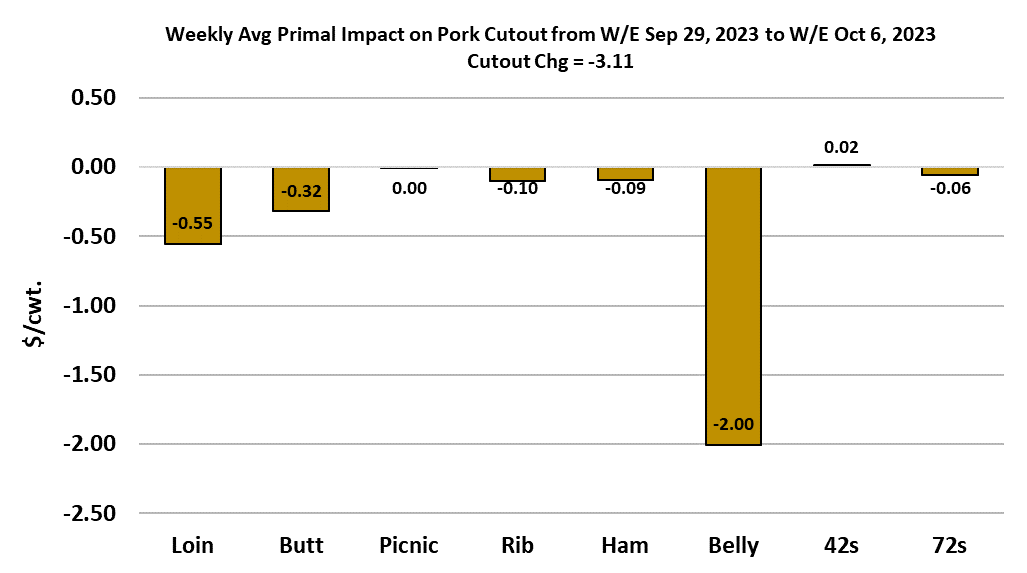

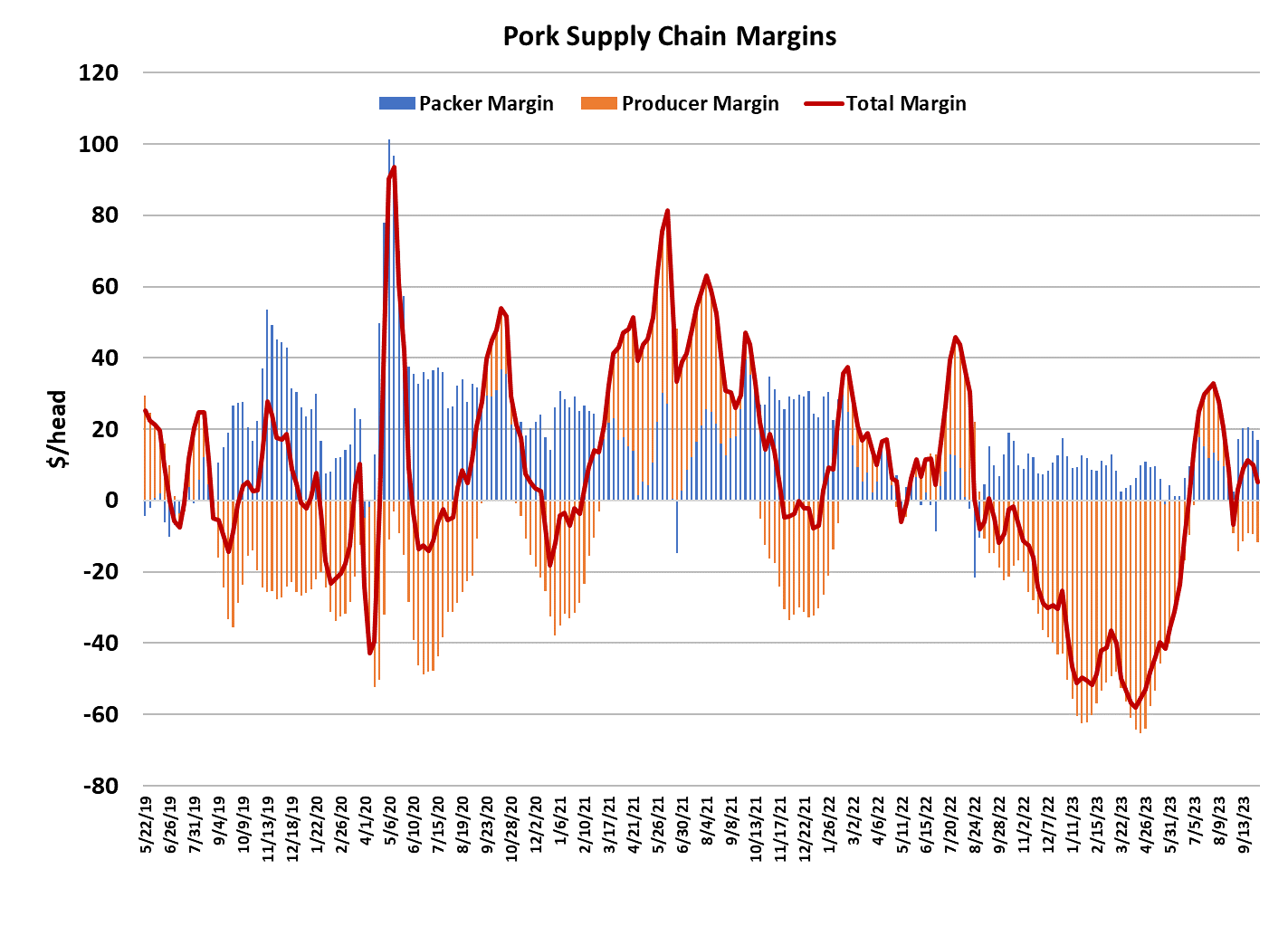

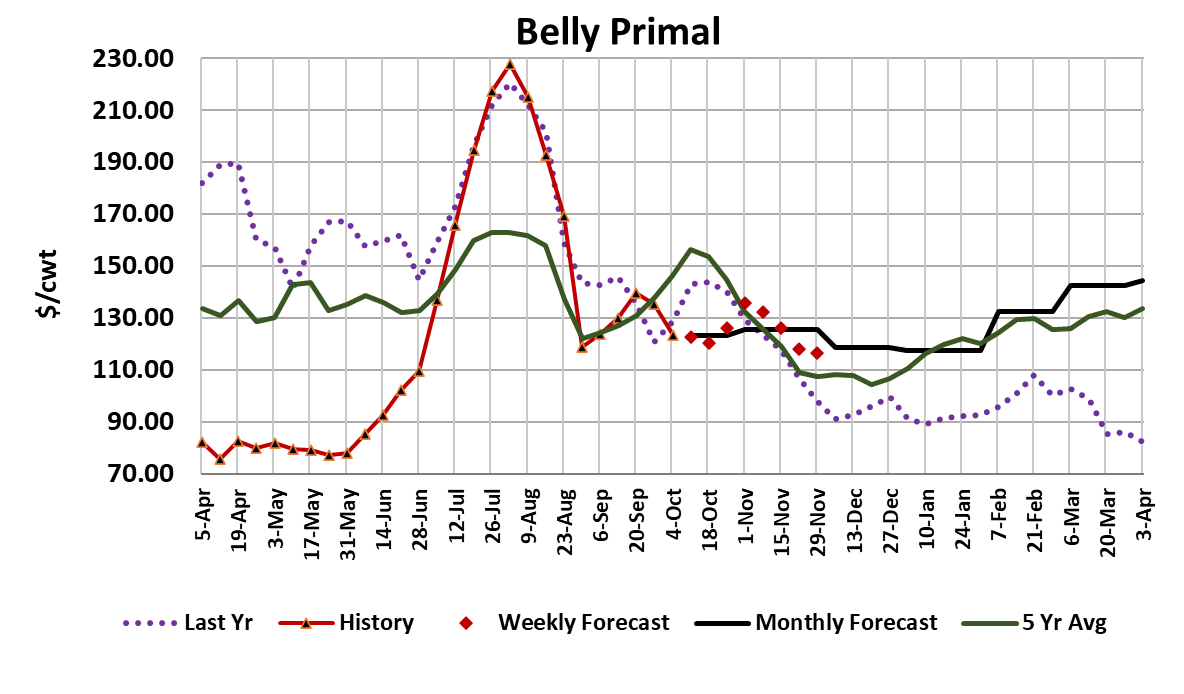

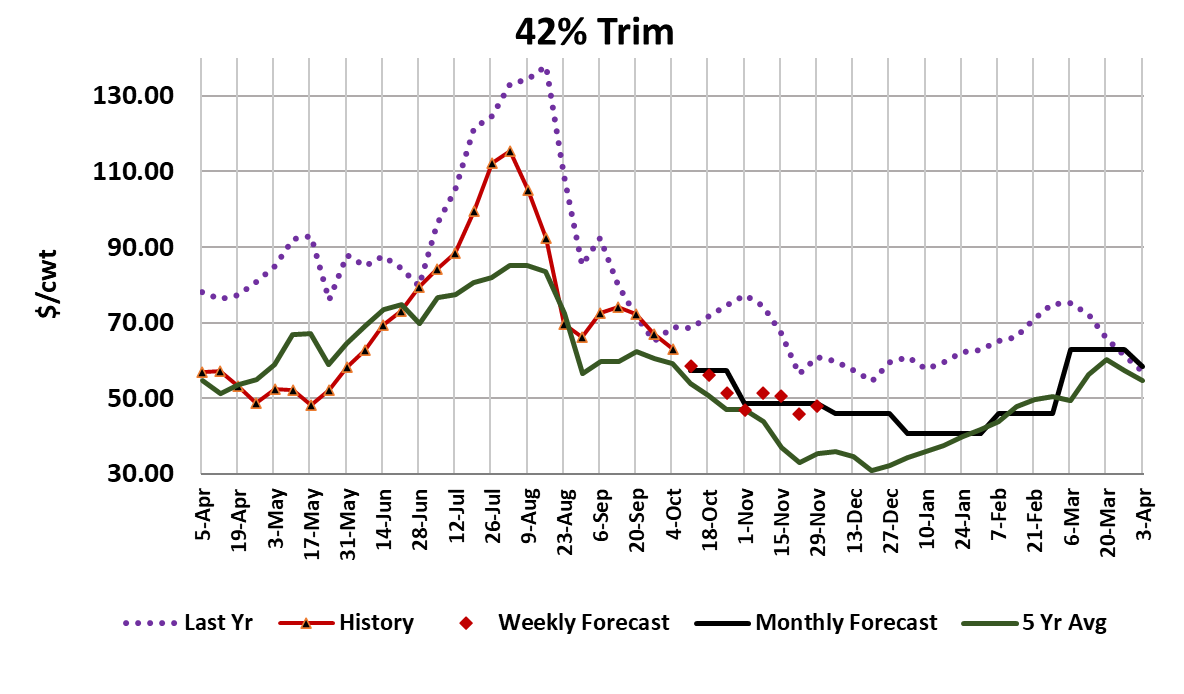

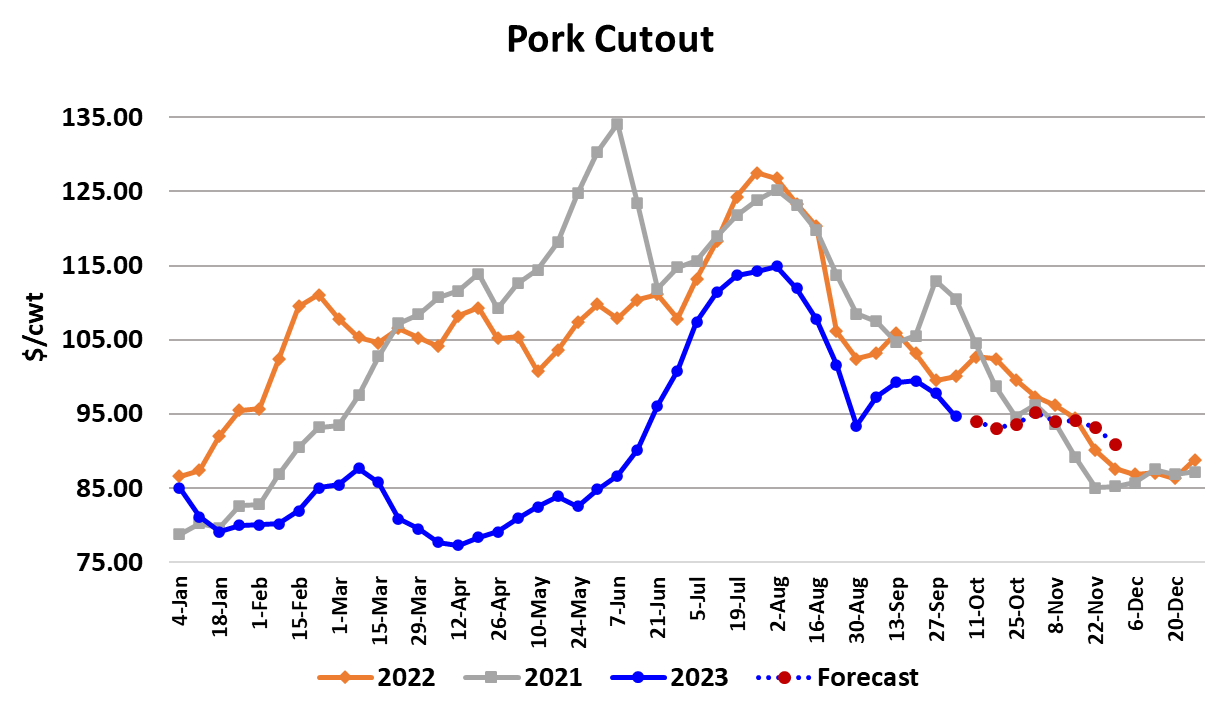

It was a $3 week in the hog and pork complex. The WCB negotiated market lost $3.21/cwt. on a weekly average basis, the NDD market averaged $3.57 lower, sow prices dropped $3.58 and the cutout fell $3.11/cwt. Three dollars is more than we have seen in recent weeks, so the speed of price declines is starting to increase. Nothing is really falling apart—it is more like a controlled slide lower. Packer margins were estimated at $17/head, down about $2 from the week before. The cutout finished on Friday at $93.22, which was $4 lower than the previous Friday. The attached chart indicates that the bellies were responsible for most of the decline in the cutout this week. We shouldn’t be too surprised that the bellies are starting to struggle given the big production levels lately and all of the concern about the macroeconomy. Bellies have a lot of exposure to foodservice and if consumers are having to cutback now that most of their pandemic savings have been depleted, eating out will be one of the first things to go. I don’t look for a serious collapse in belly prices this fall however, because there should be processors wanting to rebuild freezer stocks in November and December in anticipation of much stronger pricing next spring and summer. The bellies bear close watching though because they were a big contributor to the cutout’s woes last spring and summer. In that sense, the bellies can be the “canary in the coal mine” as it relates to the state of pork demand. The ham primal averaged a little lower this week, but we started to see prices for the bone-in hams firm up toward the end of the week, so perhaps they may be close to a near-term bottom. Hog and pork prices are elevated in Mexico and that should generate significant interest in US hams from that trading partner. We often see a modest boost in demand for hams as the deadline to get hams processed and delivered in time for Thanksgiving features draws near. So, I’m hopeful that the hams can muster enough strength next week to offset some of the softness in the belly market. Trim prices have tanked hard recently. Three weeks ago, the 72s were near $100 and this week they averaged close to $80/cwt. 42s averaged $63/cwt. on the week but Friday’s daily price was near $53, which suggests there may be further downside risk next week. Kills are big and hog weights are increasing, so that is putting a lot of supply-side pressure on trim prices that probably won’t let up until early in Q1. This week’s slaughter is estimated at 2.57 million head, down 35k from last week’s super-sized kill. The market did a fairly good job of working through that big kill this week without undue price concession, so I’d say the pork market still seems to be heading for a gentle glide lower and a soft landing that sees prices bottom in late November or early December. Lean hog futures were rather subdued the first three days of this week, but posted strong gains on Thursday and Friday that reflected a shift away from the very bearish tone that started late last week with the Hogs and Pigs report. There was also a bump higher in the negotiated trade on Friday that probably helped stoke the rally. However, traders may have overdone it to the upside as the cutout lost about $3 from noon until the close today and that is likely to bring back the bears early next week. It is interesting that the Dec futures have now regained everything that was lost after the H&P report. I guess traders have a short memory. I’d put fair value for the Oct contract around $81. It has five more trading sessions to go and the LHI is at $83 and falling. The retail cuts are also easing lower under the weight of seasonally large production and that is unlikely to change in the near term. Perhaps the best hope for cutout support comes from the hams over the next couple of weeks, so watch those closely. There has been stronger than normal correlation between hog futures and cattle futures in the past couple of weeks. Cattle seem to be reacting to the equity market and hogs seem to be reacting to cattle. In that type of environment, the potential for whipsaws and surprises is high. No wonder open interest is declining. We got export data from USDA this week that covered the month of August and showed total pork exports up 2.8% YOY. That was a little softer than what I had dialed in, but we still haven’t had a negative YOY month for exports in 2023. That may change in Q4 since the comparables will get much tougher. Still, once 2023 is done, I think we will have total pork exports up about 4-5%. Next week, expect more of the same—a gently declining cash pork market and probably lower hog prices as well. Outside markets are likely to continue having an outsized influence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}