Pork Wrap October 8

Last week’s relatively small kill didn’t do much to support the pork

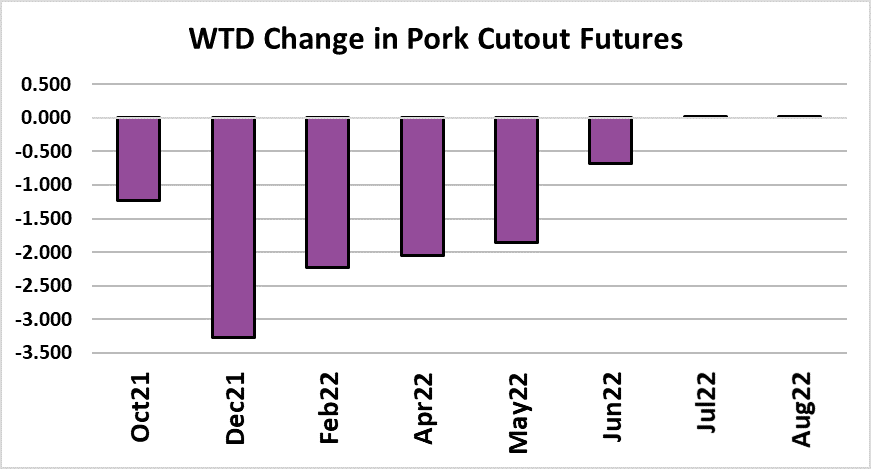

market this week as the cutout lost $2.44 on a weekly average

basis. The negotiated markets were also lower, down $3-4.

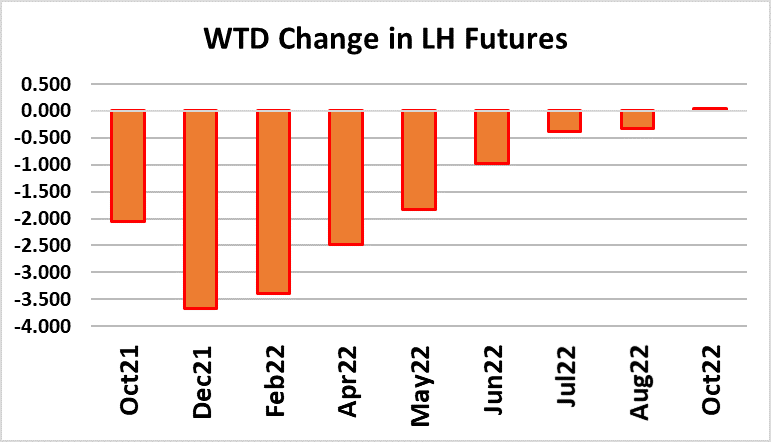

Interestingly, the LHI was almost unchanged on the week. Nearby

futures were down a little over $2. Last week, I talked about the

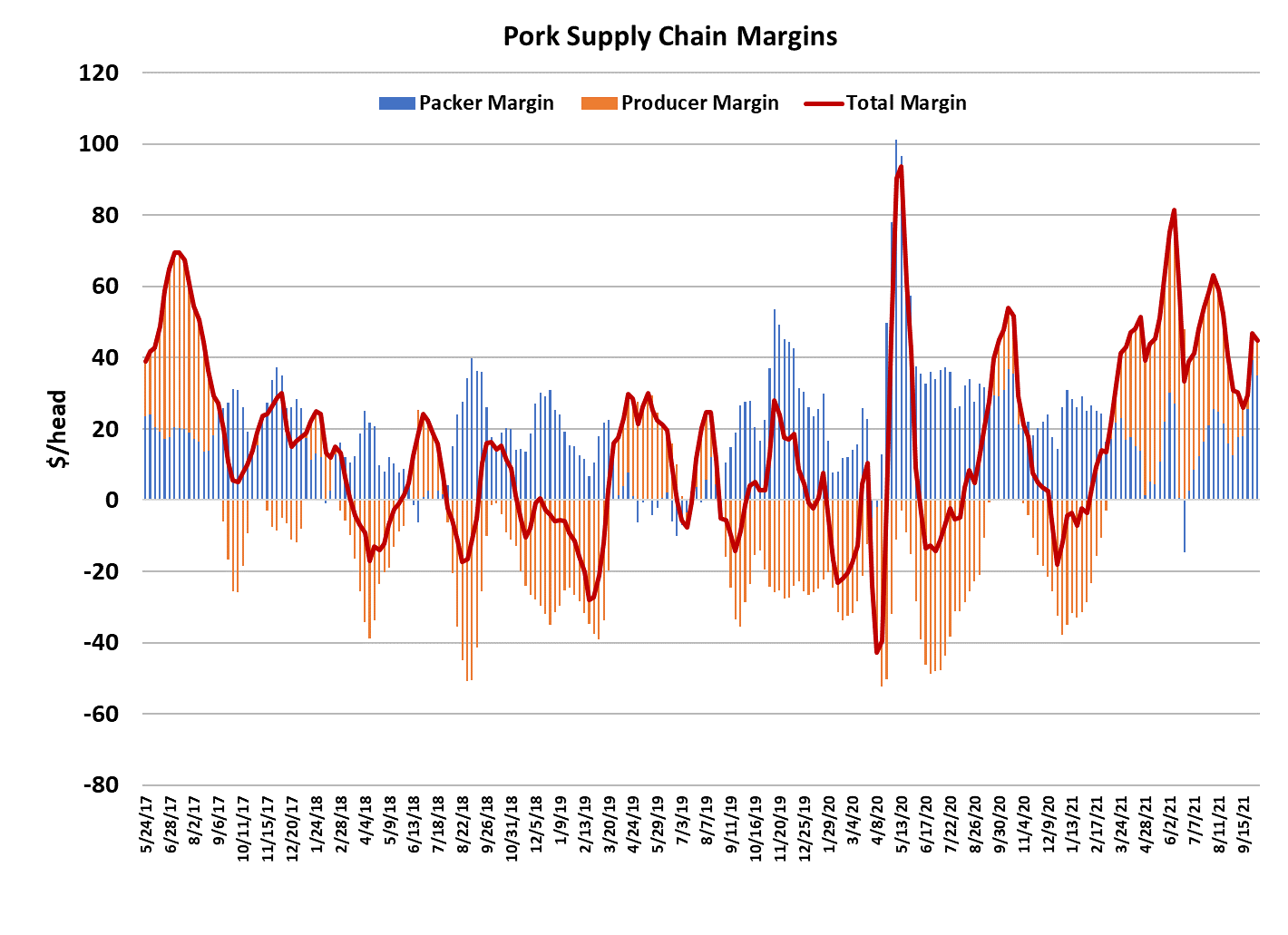

turn in the demand cycle that I’ve been seeing in the combined

margin chart. This week that upcycle took a little pause when the

combined margined ticked a little lower. We’ve seen those kinds

of breathers in the past, and this could be one of those. This

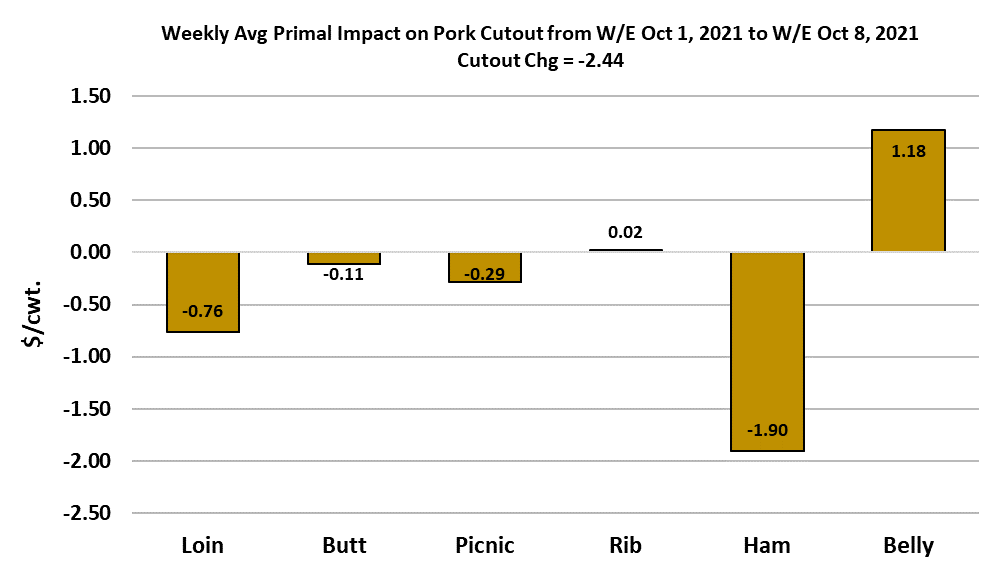

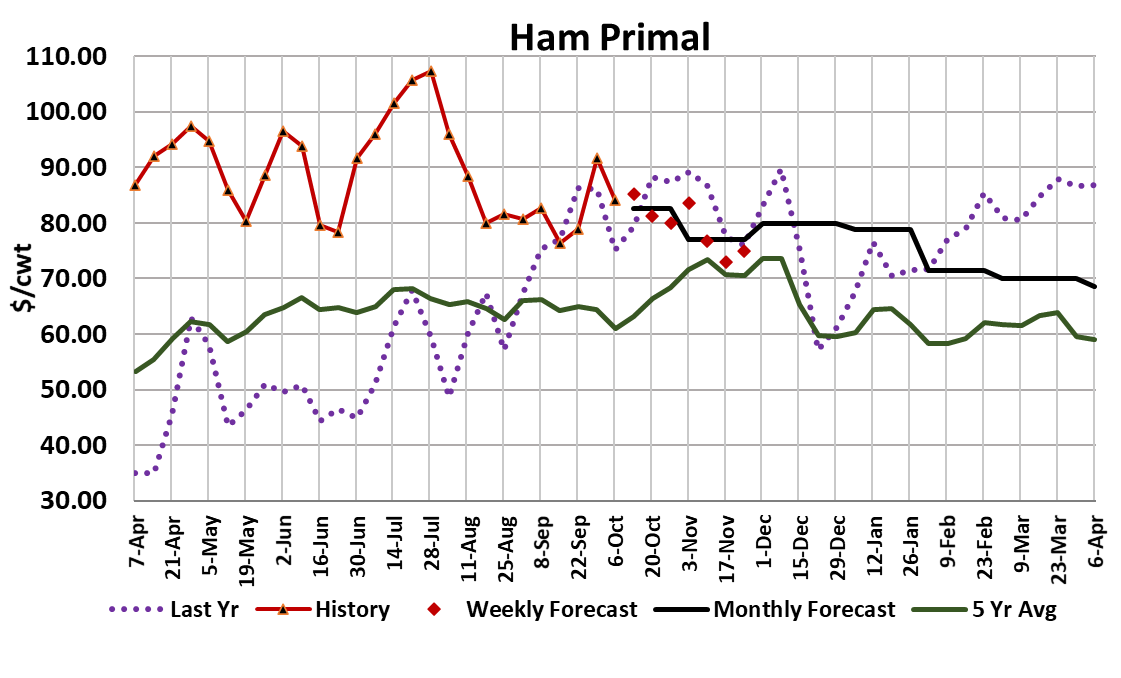

week’s decline in the cutout can be directly traced to unexpected

weakness in the ham market and, to a lesser degree, the loin

market.

Bellies were on the positive side of the ledger. There was a big

drop in the price of 23/27 bone-in hams on Thursday that really

took the primal lower. The value of the ham primal still bounces

around a lot based on the percentage of boneless hams in the mix,

but a $10 drop in a stalwart like the 23/27 is a sure sign that the

complex is softening. The belly primal averaged $203 this week

and while that is still a good ways below the $234 top that was

posted this summer, the bellies appear to be pretty vulnerable at

these levels. I’ve got it holding steady to a little higher for a couple

more weeks, but then breaking lower on bigger kills late in the

month. It may break sooner.

That, of course, raises the question as to whether or not the

demand upcycle can remain in place if the hams and bellies are

going the other way. Time will tell, but it is reasonable to expect

the price impact of this cycle to be considerably muted by

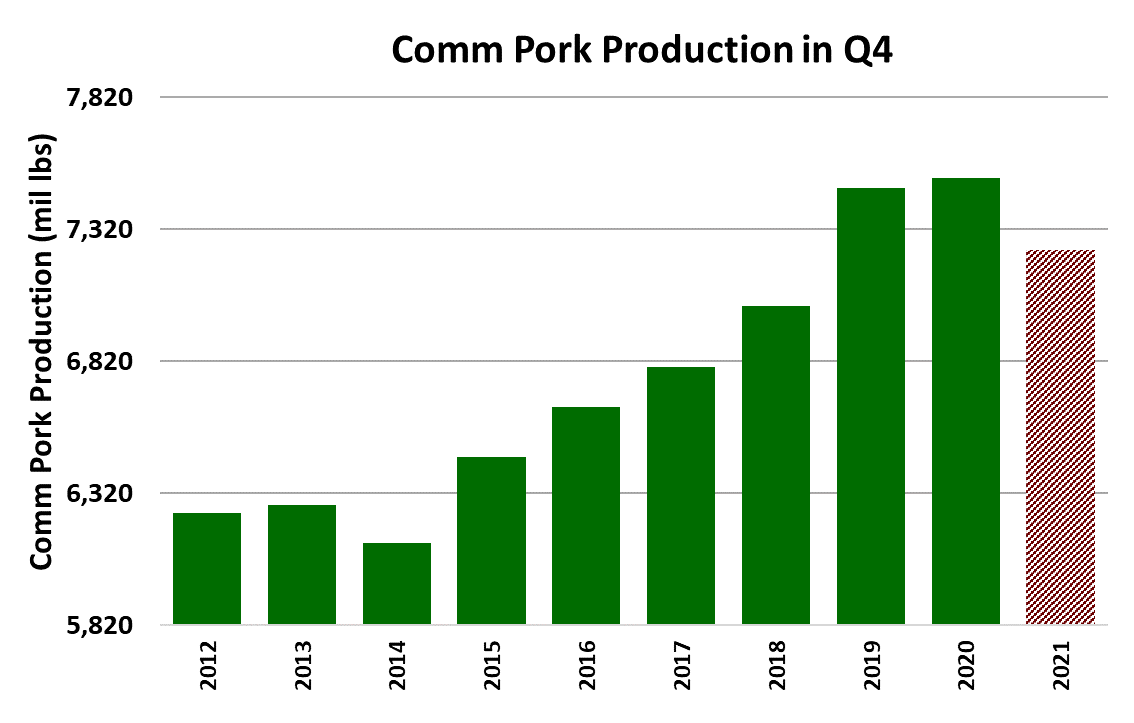

seasonally increasing pork supplies. This week’s kill came in at

2.597 million head—just a hair under 2.6 million. Packers will kill

224,000 head tomorrow. That will expand pork availability next

week, which won’t do the cutout any favors. The good news is

that kills probably don’t have much more room to increase since

the prior pig crop suggests a max kill just below 2.7 million head

this fall. This week’s kill was closer to what the pig crop implied,

but still fell a little short. So far, the industry is running a 400,000

head deficit relative to the pig crop since the first week of

September.

However, the recent Hogs & Pigs report weight range data

indicated that the pig crop was front-end loaded and that

supplies should tighten up in the second half of the quarter

(mid-Oct through Nov). That might help erase some of the

deficit and it might also make it harder to reach a peak kill of 2.7

million head. Barrow and gilt weights increased one pound this

week in normal seasonal fashion. I’m forecasting about 6

more pounds of carcass weight increase before weights plateau

in early December. The DTDS weights don’t suggest that hogs

are backing up at this point, but producers who negotiated their

hogs daily with packers continue to accept lower prices.

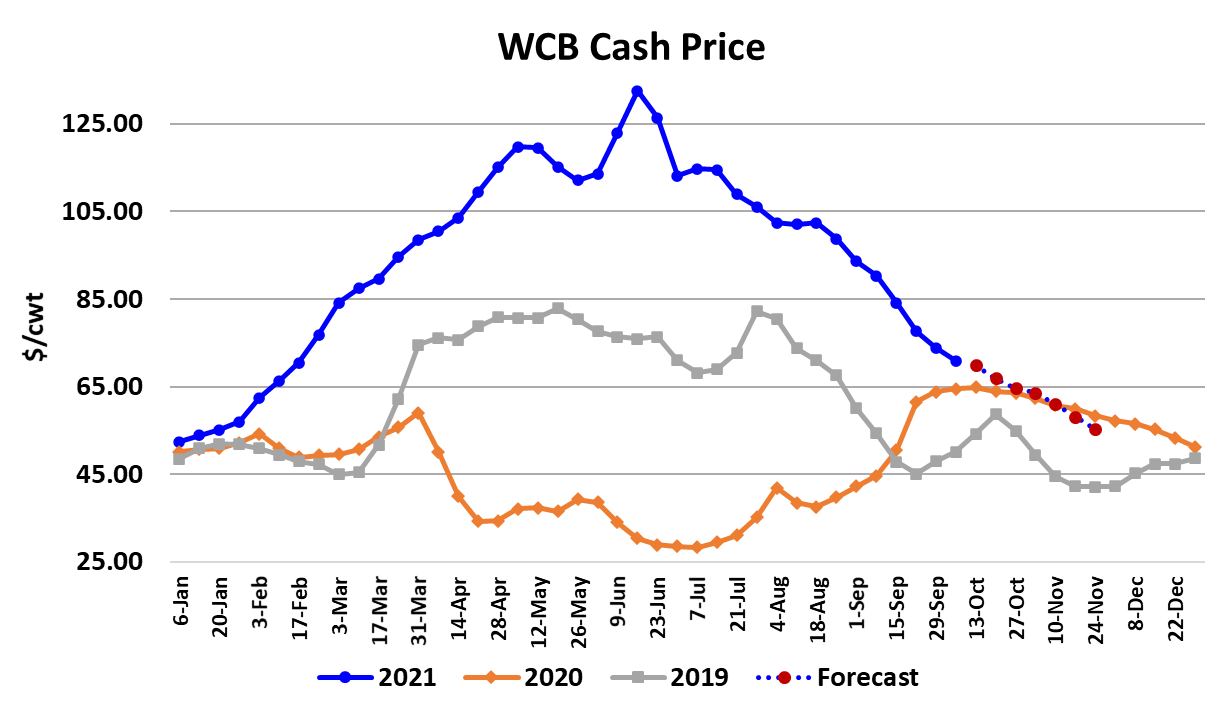

Negotiated hog prices have been in a downtrend since peaking

back in mid-June. Soon, those prices will be at risk of falling

below last year’s level. That is something that hasn’t happened

yet in 2021. USDA reported the official export numbers for

August this week and they were almost dead on with last

August. Strong movement to Mexico helped offset very weak

movement to China. So far, there hasn’t been any indication

that China is going to come back into the US market in a big

way. Pork prices in China are below what US product can be

landed for and producers in China are enduring negative

margins.

That may cause some smaller producers to exit the industry

and there is a good chance that the Chinese hog herd shrinks a

little bit in 2022. USDA is forecasting a 6.5% YOY decrease in

sow numbers. That would likely lift internal pork prices and

could rekindle interest in US pork next year. Oct LH futures will

expire on Thursday and the LHI currently sits just under $92,

while the futures have wanted to hang closer to $90. The

softness in the cutout late in the week is likely to drive the index

lower early next week. Next week, watch the ham and belly

primals. They hold the key to the cutout and the cutout holds

the key to the LH

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}