Pork Wrap October 7

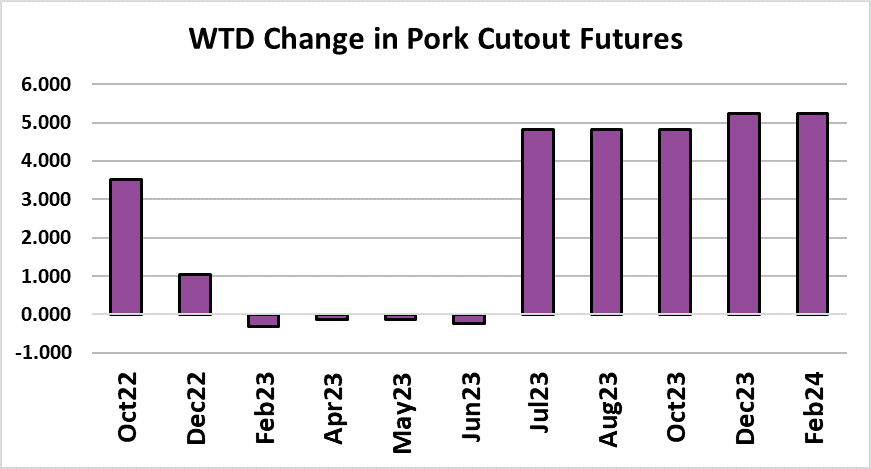

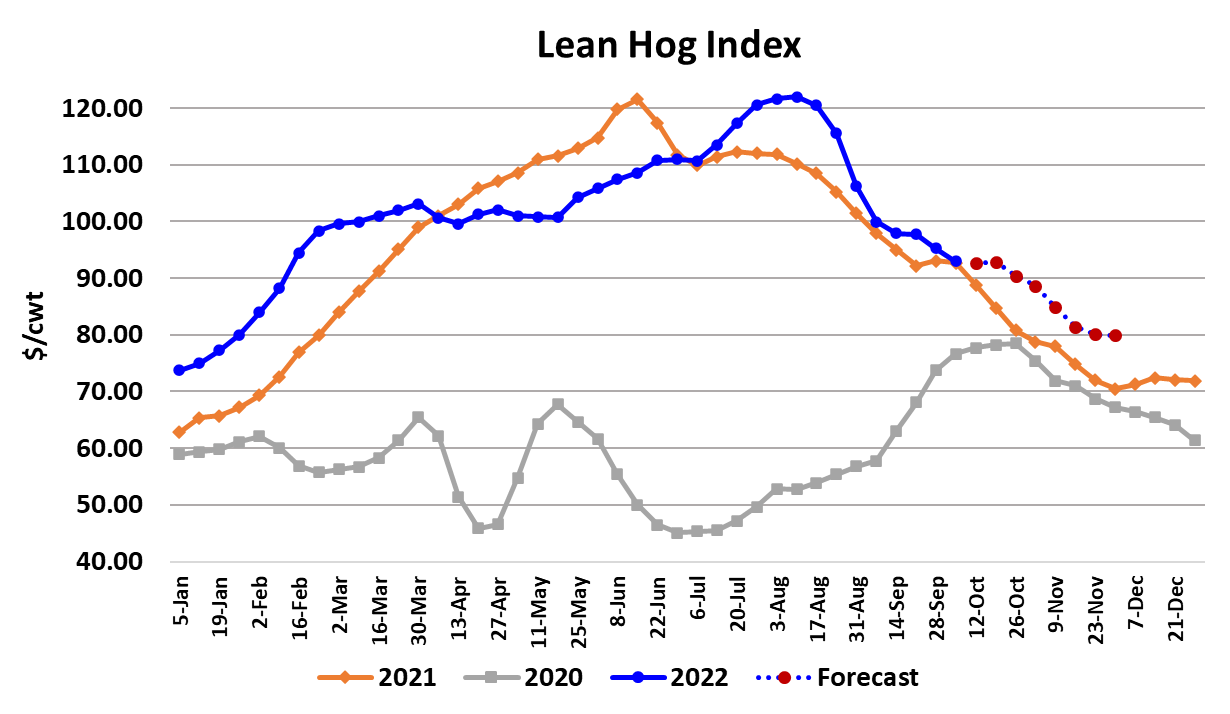

After trending lower for the past couple of months, the pork cutout

managed a small gain this week, adding $0.57 to average just

over the $100 mark. Cash hog markets were a little weaker, with

the WCB negotiated market dropping $1.74/cwt. on a weekly

average basis. With pork moving up slightly and cash hog prices

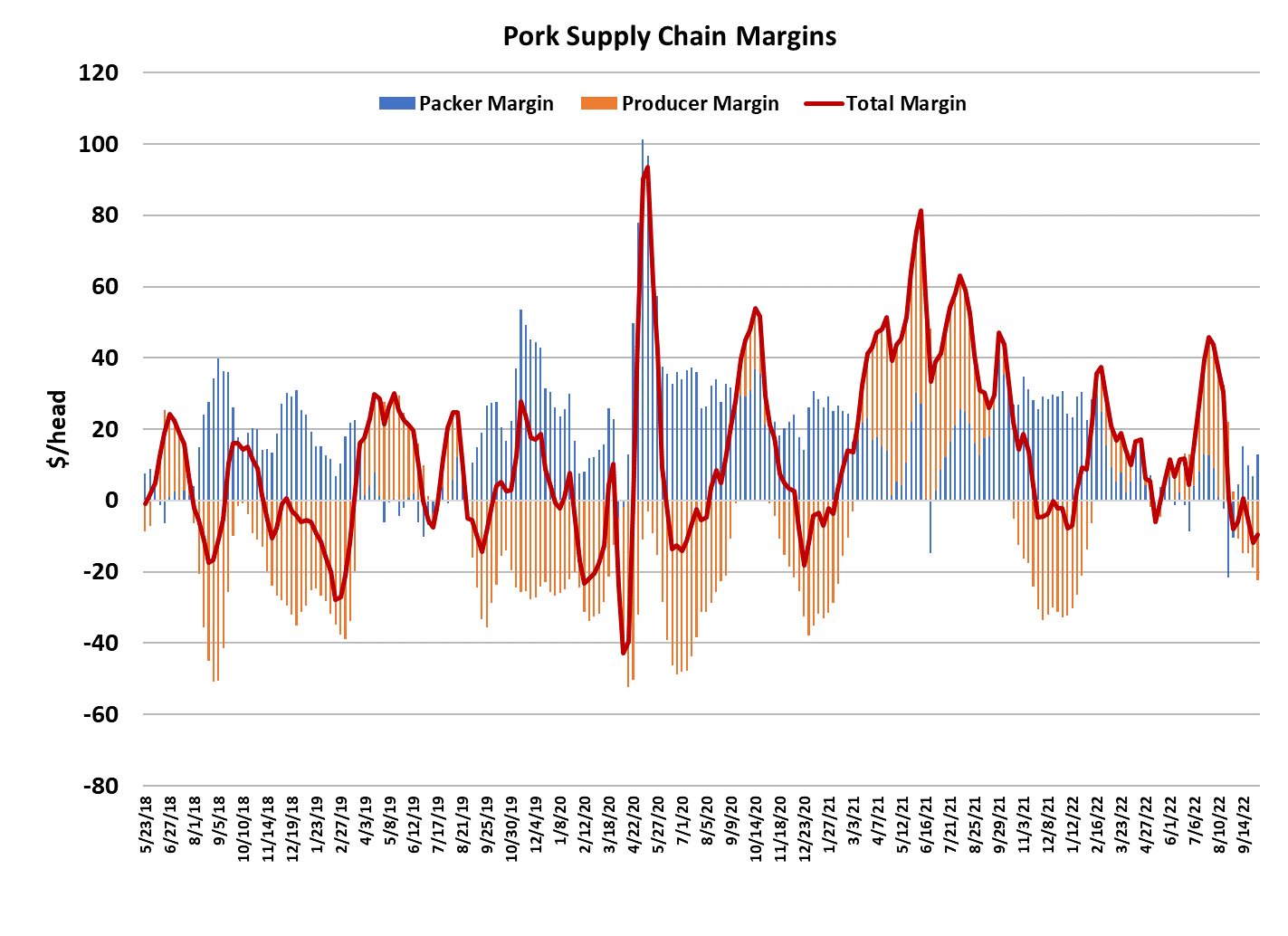

moving lower, packer margins expanded out to about $13/head.

That represents about a $7 spread between the cutout at $100

and the LHI which is now close to $93. Perhaps the most

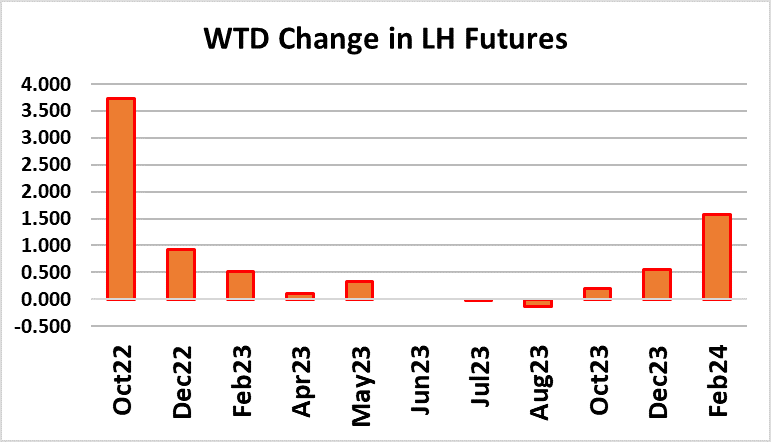

surprising feature of this week’s market happened in the futures,

where traders beat down the nearby Oct contract to below $87 on

Tuesday only to realize that was a significant mistake and thus

the contract rallied $6 over the next three days to finish the week

just a hair below $93. I’m not really sure why traders felt the need

to sell Oct so hard when it was so close to expiration (next

Friday), because the rate of decline in the LHI suggested that

there was very little chance that the index would drop to $87 in

just eight trading days.

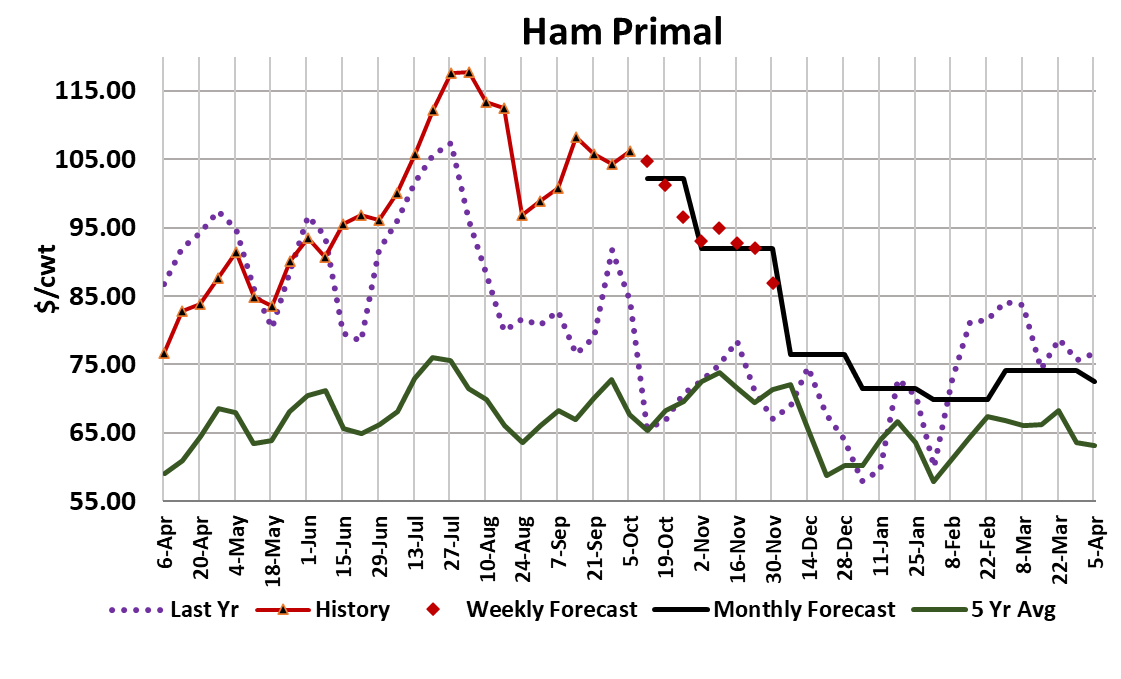

Part of what prompted the turnaround in the futures was some

strengthening in the cutout, which moved from below $99 early in

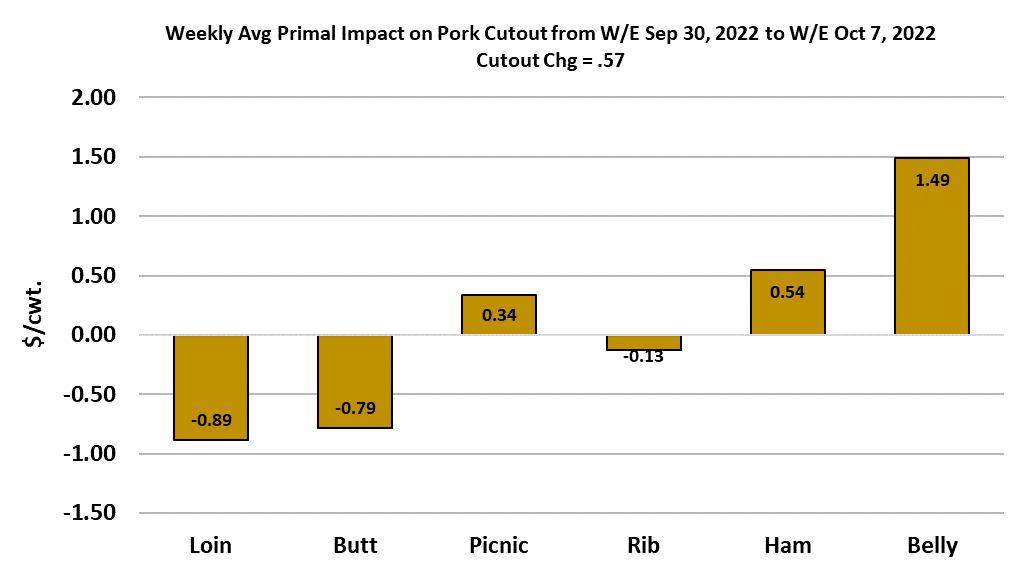

the week to over $101 for the last two days of the week. Those

gains were largely driven by stronger belly and ham pricing. Just

when I thought that the strength in the hams had finally topped,

the primal was able to add more than $2 this week. I’m a little

uncertain as to where the hams go next. Growing production and

the narrowing window to get hams processed in time for the

holidays suggests that ham prices should work lower, but those

conditions have been in place for a few weeks now and we have

yet to see any meaningful weakness in ham prices stick. They

may get pushed lower for a few days, but they always seem to

resurrect. I’m going to keep the forecast on a slight downward

trajectory for now, but recognize that hams are probably going to

stay well above last year for most of Q4.

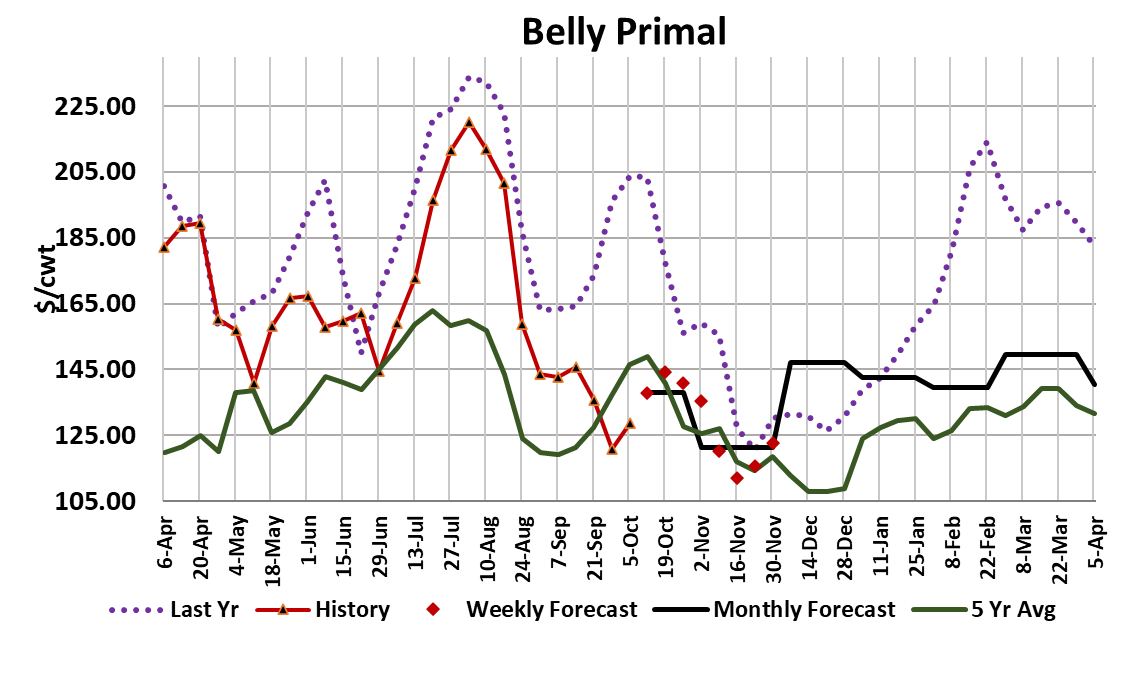

With respect to the bellies, I’ve been suggesting for the past few

weeks that they were due for an upward move and this week the

belly primal managed to add almost $8/cwt. Belly prices are still

quite low relative to recent history, so perhaps this week’s gains

will cause some buyers to get off of the fence and break out the

checkbook. I don’t think a huge price rally is in the cards for

bellies, but they may be able to build on this week’s rally for a

couple of more weeks before growing production moves them

lower again. One thing that gives me some hope for further gains

in the bellies is that trim prices have been holding up rather well

recently and there is normally a pretty strong correlation between

trim prices and belly prices. On the losing end of the spectrum

this week was the retail items, particularly loins and butts. The

butt primal lost about $6 on a weekly average basis and the loin primal was down about $2.50/cwt.

These are the items that pork month

promotional incentives were designed to support, but even a well

planned industry promotion can’t always overcome the negative effects

of seasonally increasing pork production. I’m looking for the cutout to

average just over $100 again next week on further belly strength and

then start to slip slowly lower until it is near $90 in mid-to-late November.

Last year, the cutout lost $23 from early October until mid-December and

that may be influencing the way that futures traders are pricing the Dec

contract, but that big drop was a bit of an outlier. Usually a decline of

$4-6/cwt is more common. I’m going to stretch that a bit and call it down

$10-12 this year, but I can’t find a plausible scenario where it loses $23.

It does seem like traders have been overly negative on the Dec contract

and it finished today more than $15 below the Oct contract and close to

$77. My read on the fundamentals suggest that $83 would be a better

choice for Dec.

It might even outperform that because the combined margin is acting like

it wants to bottom again and if that holds, we could see a much flatter

trajectory in the cutout and LHI than the futures currently imply. I’m not

ready to call this week’s little uptick in the combined margin a bottom, but

it sure seems like it is in the right zone for it. Next week’s data should

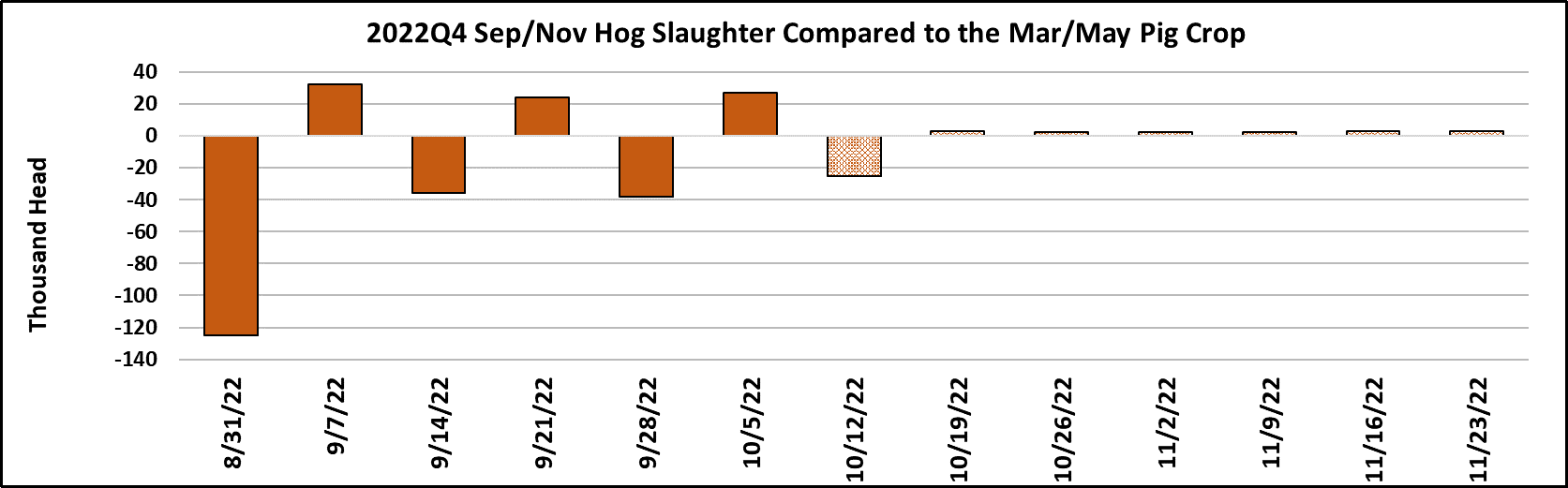

help clarify. This week’s kill registered 2.56 million head and that was a

little larger than what the March/May pig crop implied. As we approach

the halfway point in Q4, it looks like the industry has underkilled the pig

crop by about only 100,000 head. It’s not a big miss, but it makes me

think that perhaps there are just a few less pigs out there than what

USDA projected for the Sep/Nov quarter. The industry will start killing

the summer pig crop come December and that was estimated to be 1.1%

below last year. So, YOY production declines are dialed in for the next

few months unless the survey missed a lot of pigs. Barrow and gilt

weights were steady at 210 pounds this week, marking their third week in

a row at that level.

The uptrend in weights should continue next week and probably won’t

top until mid-November or later. There isn’t anything in the weight data to

suggest that the production pipeline is experiencing any problems.

Export data for August became available this week and it showed a 2.6%

YOY decline. Movement to China was actually up about 9% YOY, but

that is only because we are now lapping the point where exports to China

dropped off a cliff last year. Mexico is looking like the most promising

destination at moment that probably says a lot about why the ham market

has performed so well this year. The US dollar hasn’t appreciated

against the peso to near the degree that it has against other currencies,

so Mexican buyers have an advantage there. Imports remained elevated

in August, up 2% from last year and about 9% stronger than in July.

Next week, watch for further strength in the bellies—it will be needed if the

cutout is to hold above the $100 mark.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}