Pork Wrap October 29

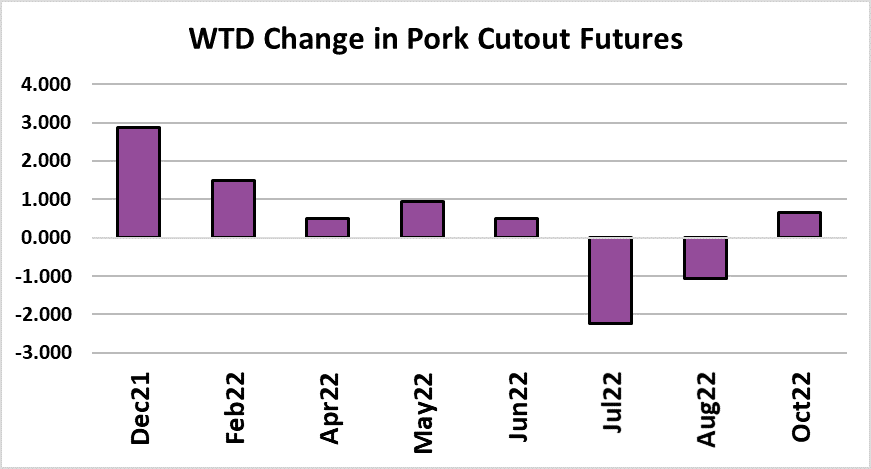

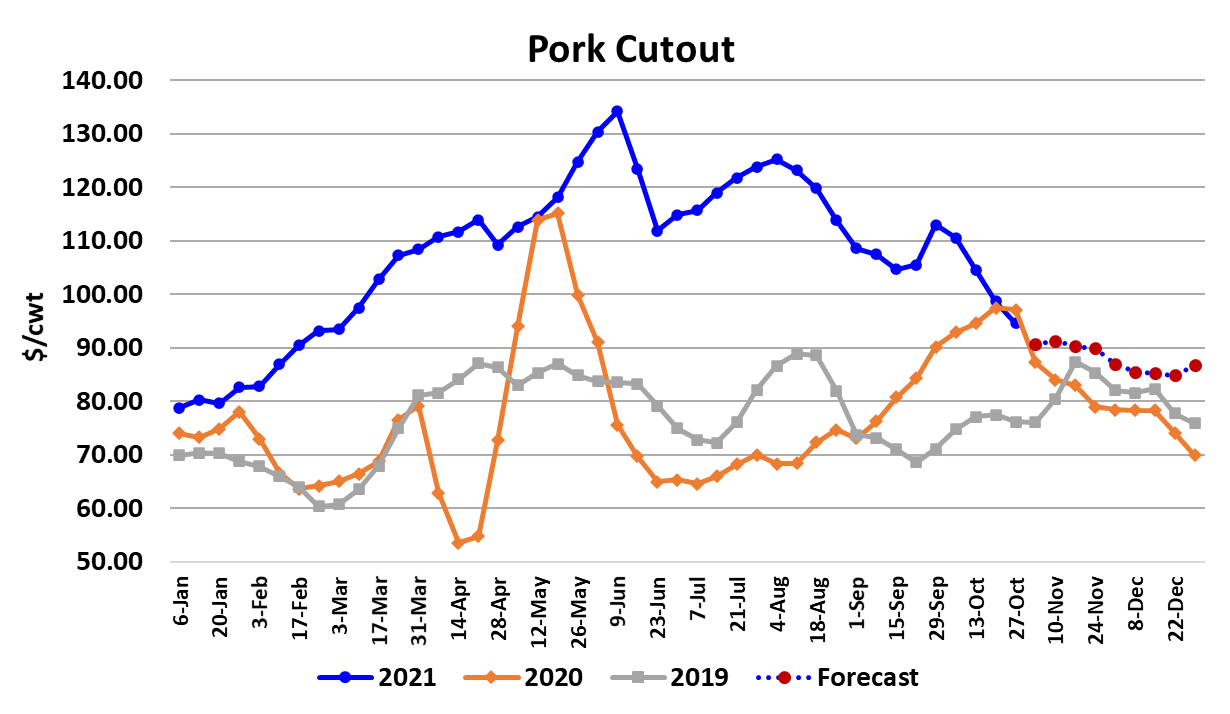

Everything continued lower in the hog and pork complex this

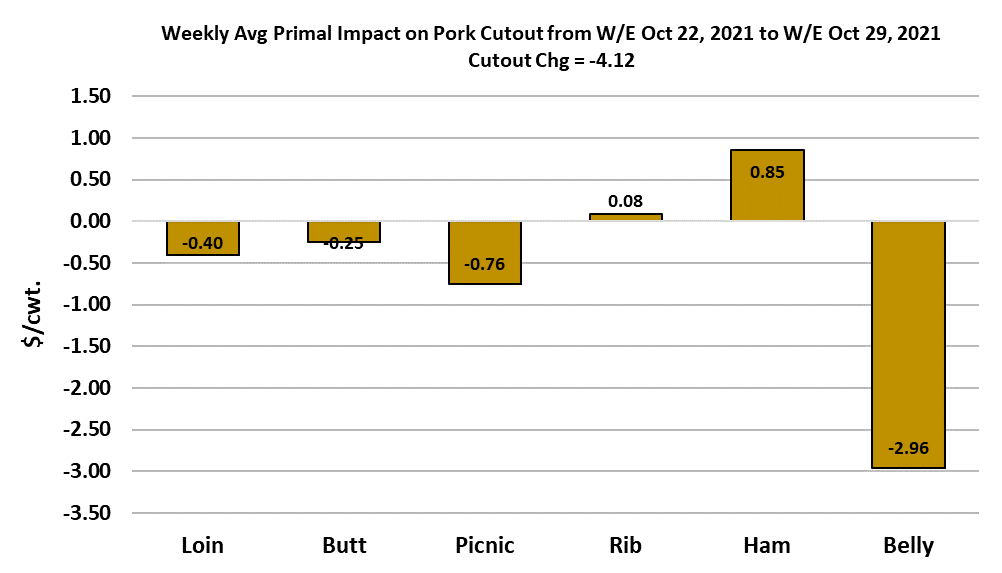

week. The cutout lost $4.12 on a weekly average basis and the

NDD negotiated hog market was about $3.50 lower. At this point,

everything is being driven by the cutout and the cutout is being

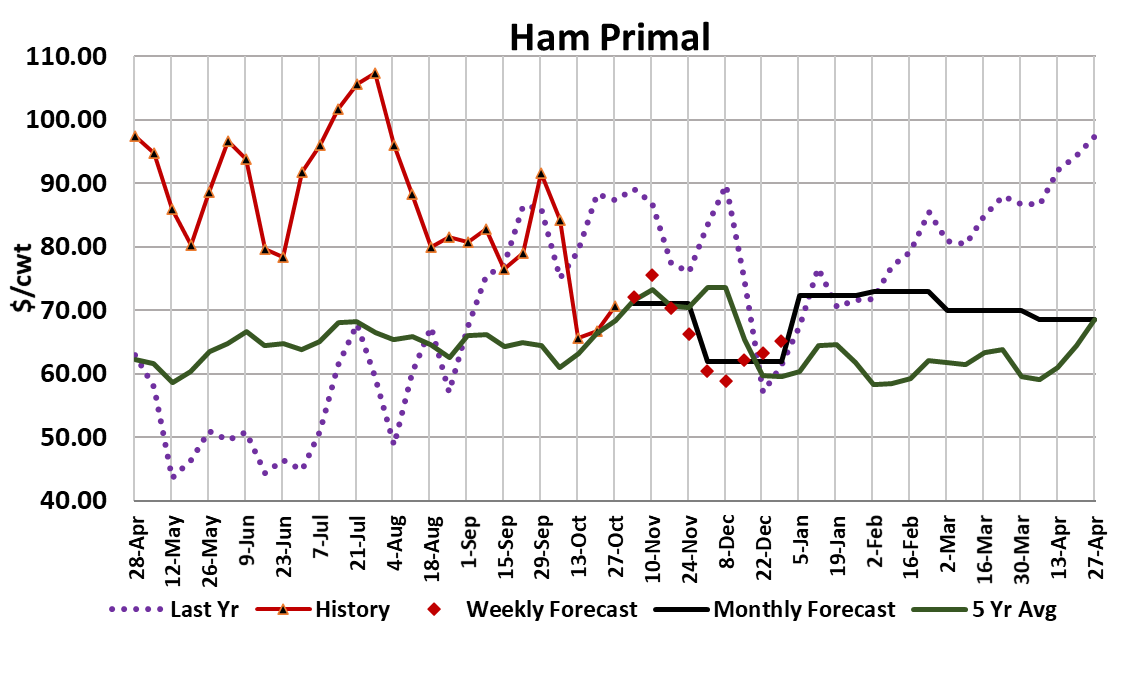

driven by the bellies and hams. The belly primal continued to

work lower, finishing the week $21 lower than where it ended last

week. On a weekly average basis, the ham primal was up $3.90.

So far, the declines in the bellies have outweighed the modest

support provided by the hams. We are also seeing some

slippage in prices of the retail primals. The loin primal dropped

about $1.75 on a weekly average basis.

Given that this week’s softer pricing occurred against the backdrop

of a little smaller production last week than the week before, it is

reasonable to conclude that overall pork demand is still softening.

USDA revised last week’s kill down to 2.59 million head and this

week packers did a much smaller Saturday resulting in a 2.55

million head kill. That should reduce availability somewhat next

week, but if the demand softening continues that might not be

enough to raise price levels. Hams look dirt cheap right now and

I’m pretty surprised that hasn’t attracted more buying interest.

The forecast has them moving modestly higher next week.

Bellies probably have at least one or two more weeks of softer

pricing before their cycle turns higher. My biggest concern right

now in the pork complex is the retail cuts and trims seeing softer

demand. Even if the hams move higher next week, I think

declines in the retail items and trims will be enough to keep the

cutout on a downward trajectory. Those declines are likely to be in

small chunks and the forecast has the cutout holding in the upper

$80s for much of November.

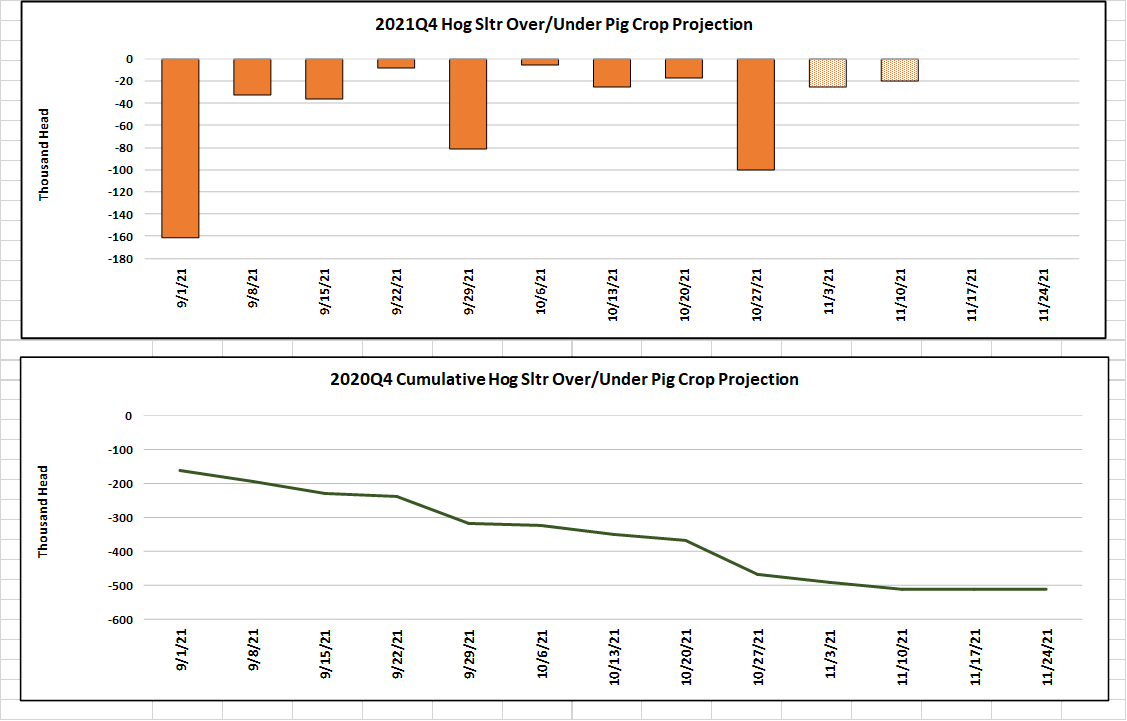

Figuring out what is going to happen in the cash hog market is a

little more complicated. USDA’s March/May pig crop made it

clear that we should expect less hogs coming to slaughter this fall

than last. So far, that is what we are seeing. In fact, we’ve

actually seen slaughter come in about half a million head below

what the pig crop implied in the Sep/Nov quarter. However, we

also know that plants are struggling with a labor shortage that

seems worse this fall than it was last fall. If there are more hogs

than the plants can process, that is very bearish for the cash hog

market, but if plant labor is sufficient to handle this fall’s smaller

hog supply, then I would expect cash hog prices to be relatively

firm

The cash hog market hasn’t firmed up, but instead keeps

trending lower. This week’s kill was only 2.55 million head, with

a much smaller-than-normal Saturday kill. Is that because the

hogs aren’t available or is it because of labor shortages? I’m

leaning toward the latter explanation, but also recognize that it

could just be some plants doing maintenance over the

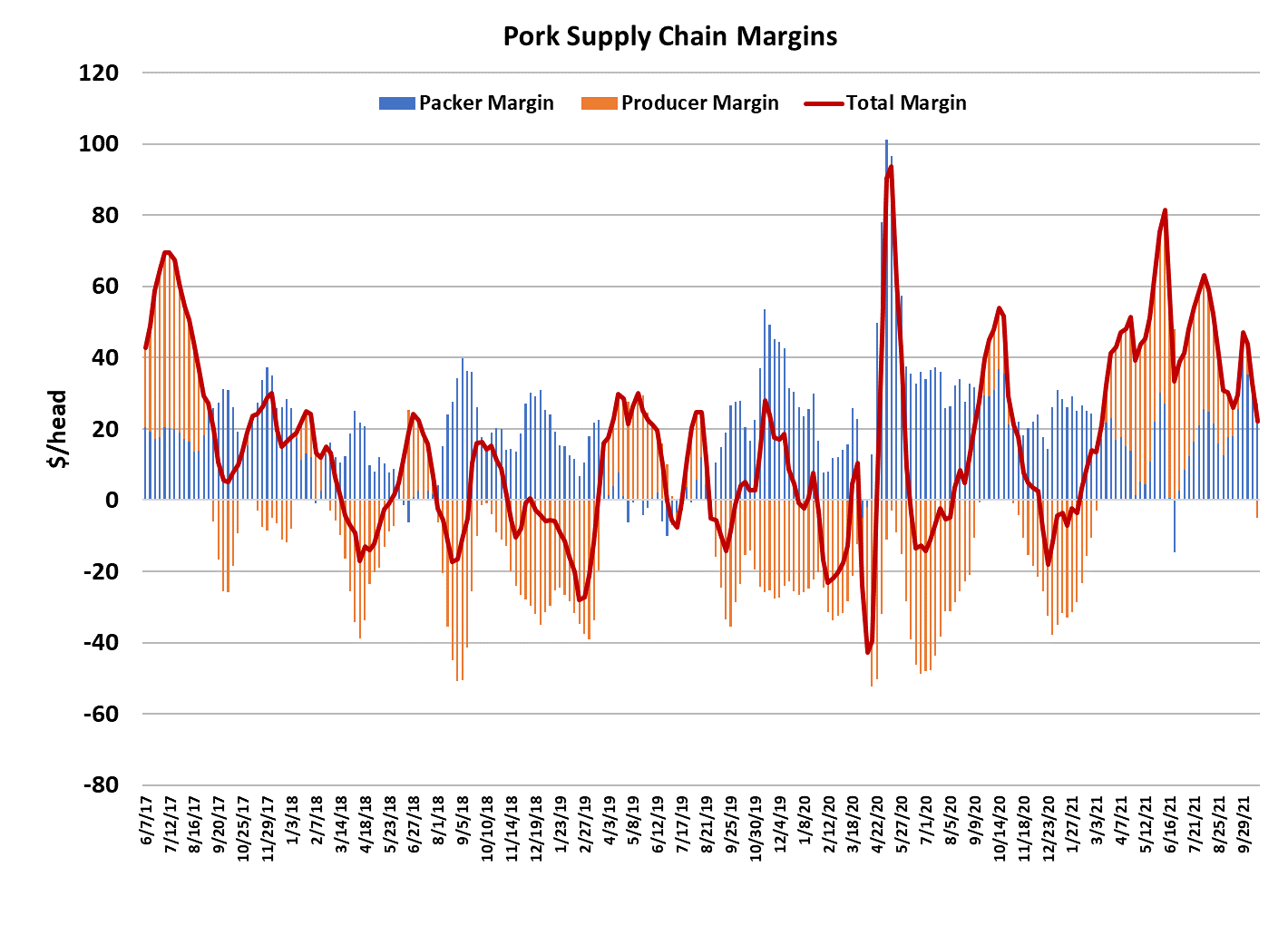

weekend. Maybe maintenance was scheduled with marginenhancement in mind. This week’s packer margins registered

$26/head, down about $1 from last week. That is a pretty

typical margin for this time of year, but I’m sure that packers

would like to see it larger.

Packer margins are the key variable to watch to discern if

plants don’t have enough labor to process all of the hogs. If

that becomes the case, then packer margins would likely

balloon out to $50/head or more. So far we haven’t seen that

either so it’s reasonable to conclude that processing capacity is

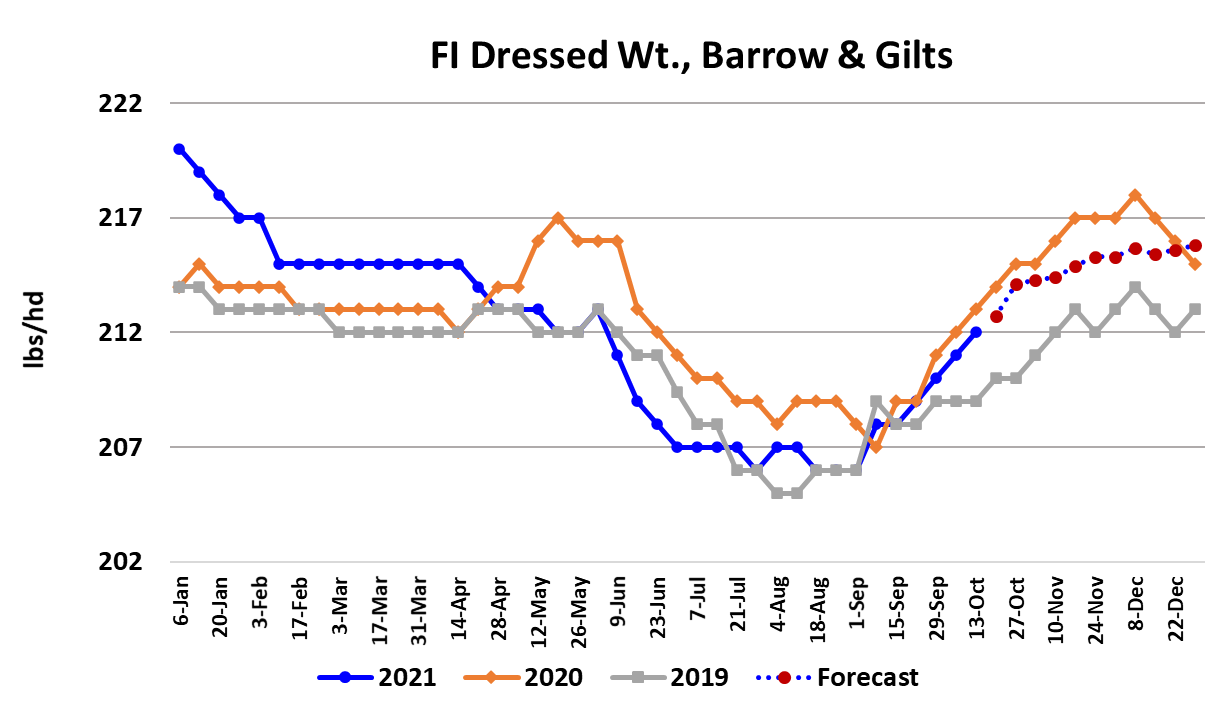

sufficient for now. Barrow and gilt carcass weights moved

another pound higher this week to 212 pounds, only one pound

below last year. This is a normal seasonal increase in weights

and doesn’t necessarily indicate that hogs are backing up. The

DTDS weights have risen a bit, but are still relatively low from a

historical perspective, so that piece of information doesn’t

support the idea that hogs are backing up either. The demand

side of the market looks like it is slowly weakening to me.

Hams may creep higher from here, but I don’t think the bellies

are done moving lower.

International demand is down also. China continues to back

away from the US market, but Mexico has been a stronger

buyer lately. I had hoped that perhaps we would see China

increase purchases this fall to support their New Year’s

celebration, but so far that hasn’t shown up in the data. Pork

prices at retail are record high—just like beef. That should be

detrimental to movement through the retail channel over the

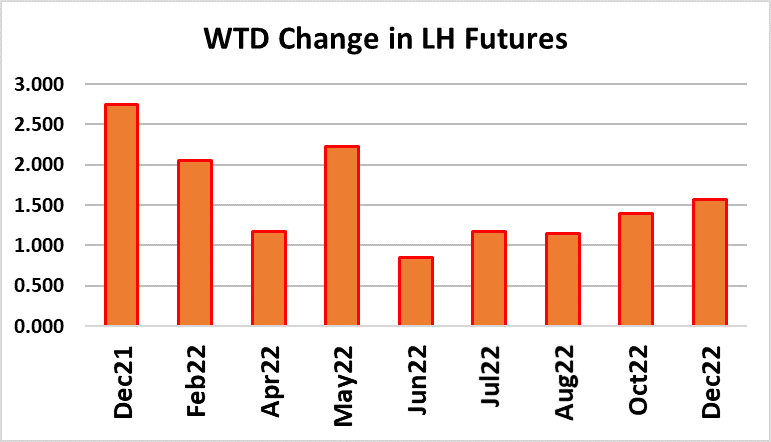

next couple of months. Lean hog futures were higher across

the board this week, with Dec the biggest gainer. Next week,

watch the hams and bellies. They will have the most influence

on the cutout and the cutout will influence the futures.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}