Pork Wrap October 28

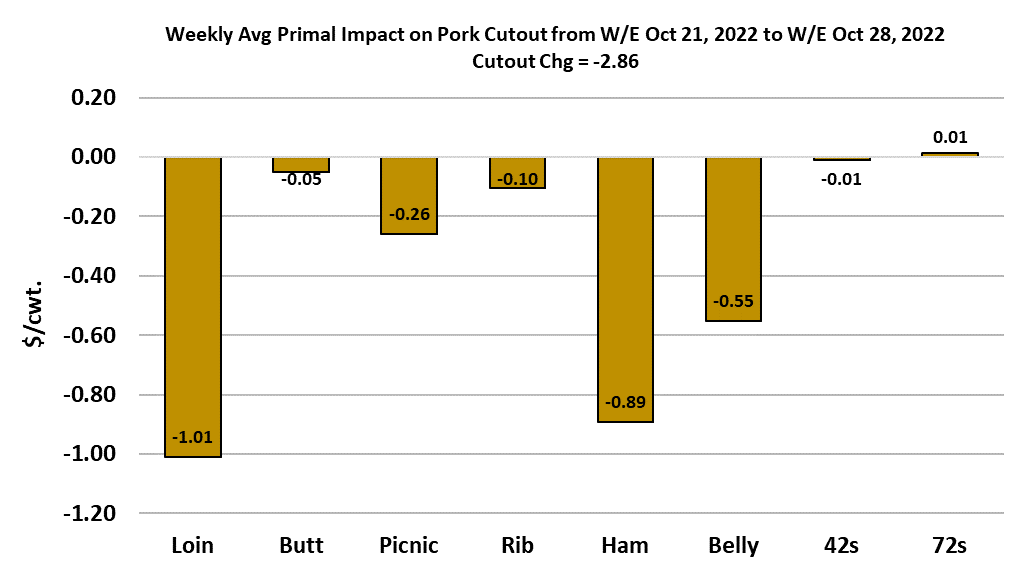

The main feature in this week’s market was the cutout dipping

below the $100 mark for several days and averaging $2.86/cwt.

less than last week. There were some interesting dynamics

within the carcass and within the week however, starting with the

surprising bump higher in the belly market on Friday. Prior to

Friday, the bellies had been trading softer, but someone

managed to sell a good quantity of 13/17 lb. bellies at $205 on

Friday morning and that caused the belly primal to jump.

However, the bellies that traded Friday afternoon were much

closer to the $160/cwt. level that had been common earlier in the

week. So, while that might have been an anomaly, it did allow

the cutout to finish the week back in triple digits. On a weekly

average basis, the belly primal was down about $3.50 this week.

Another important feature in this week’s market was the

continued slide in the loin primal, making it the biggest drag on

the cutout. That is probably a sign of some pork fatigue starting

to set in at the retail level. Hams also lost ground this week and

that is probably due to less demand from domestic processors

who are now up against a tight timeline in order to get hams

processed in time for the holidays. Trims were the bright spot,

with both the fat and lean trim up around $3 on a weekly average

basis, but trims make up a much smaller part of the cutout

calculation than do the other primals. When it was all said and

done, the cutout posted an average of $99.59 for the week. Last

year at this time, the cutout was about $5 lower than where it is

now. On the surface, that would seem to indicate that pork

demand is still robust, but when we take inflation into account,

the picture isn’t so rosy.

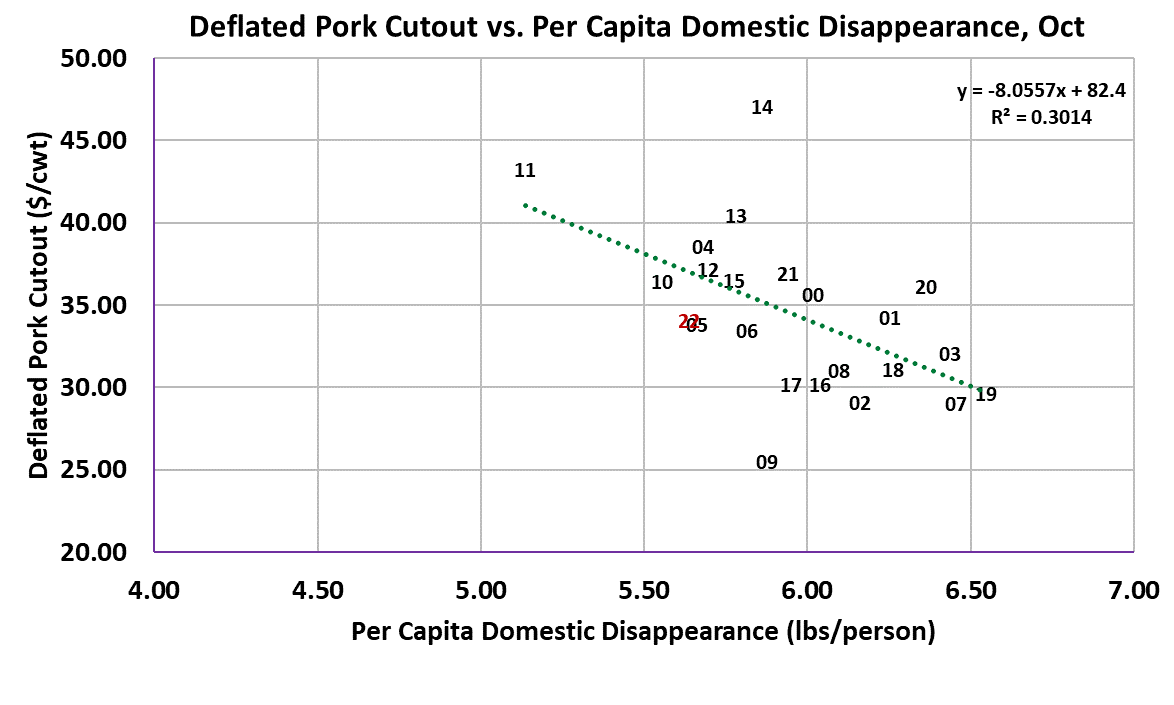

The attached scatter diagram gives the demand curve for

October calculated using CPI-deflated price levels and we see

clearly that demand was stronger in October 2021 than it was

this year. In fact, demand looks really soft compared to recent

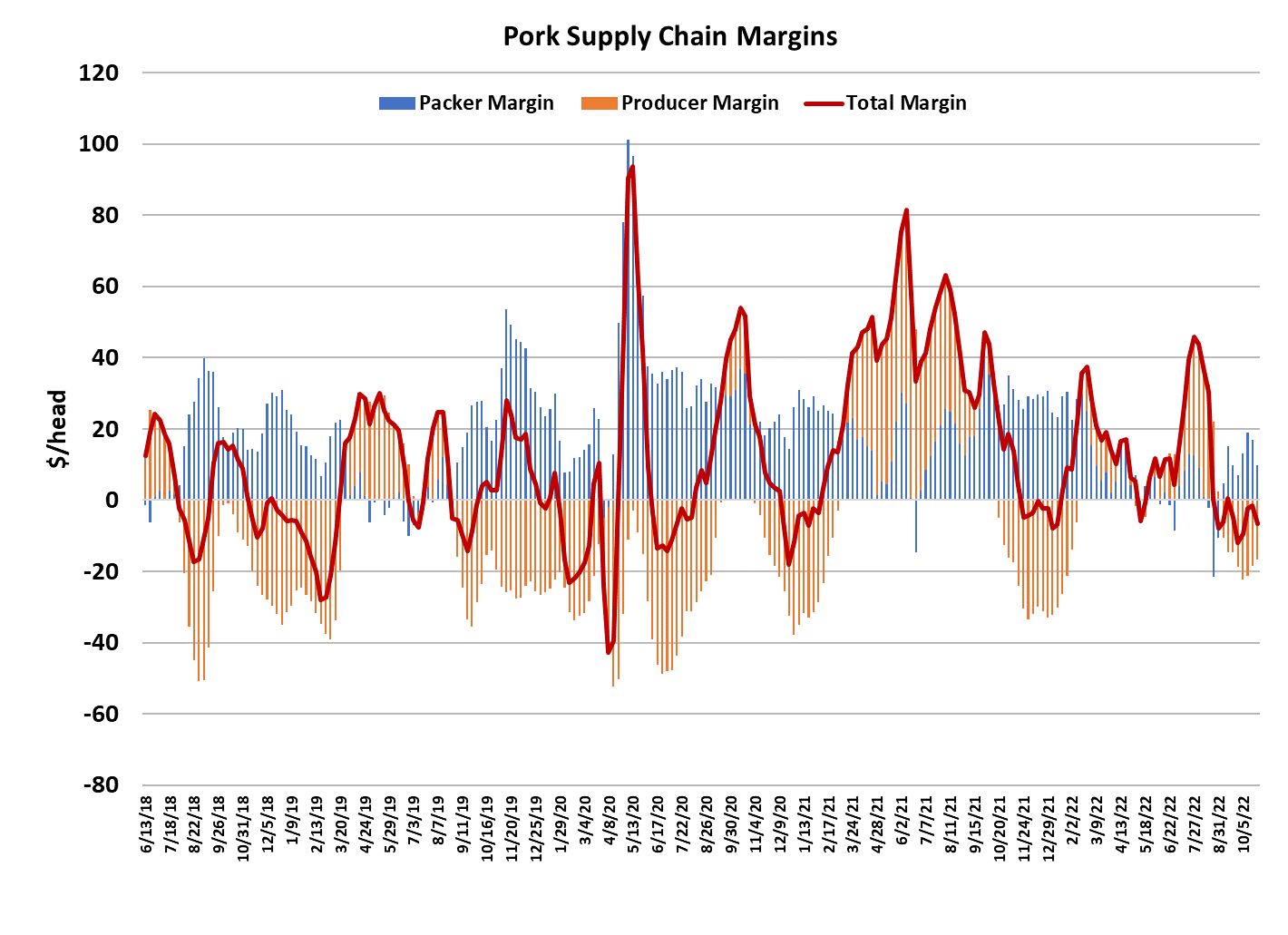

years. That fits with the combined margin, which is also on the

defensive and signaling weak demand. If we have a $99 cutout

on weak demand, imagine where it will go when demand enters

its next upcycle, which I would expect to begin in the second half

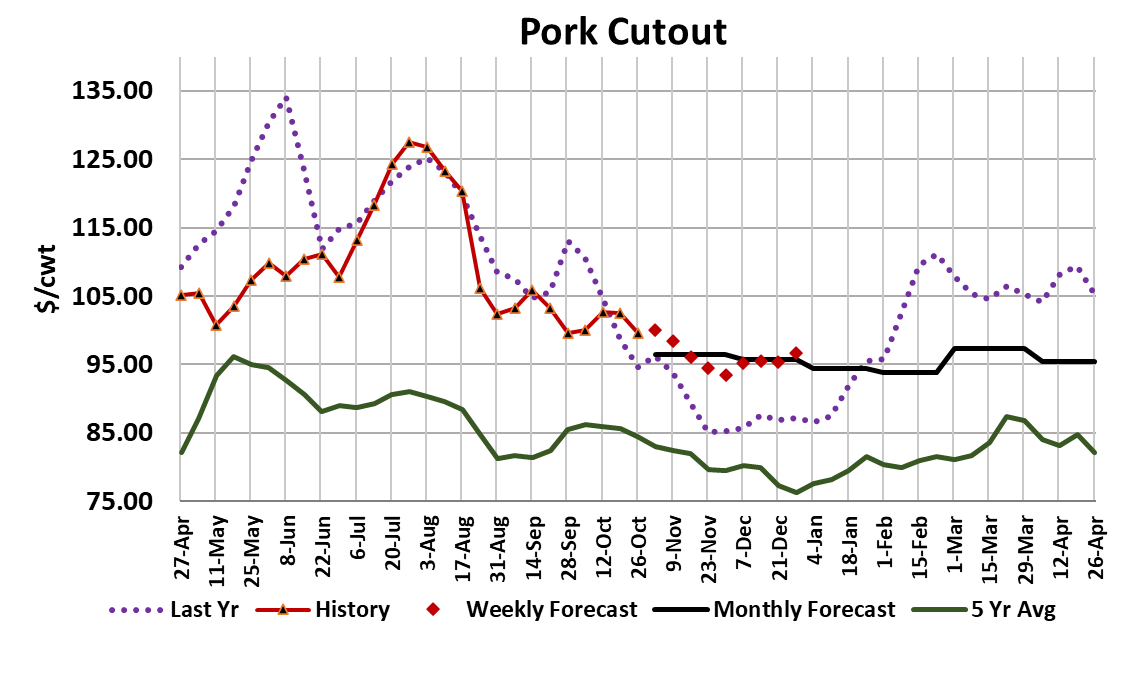

of November. The forecast has the cutout easing lower through

most of November and then strengthening modestly into

December. One place where there is definitely not weak

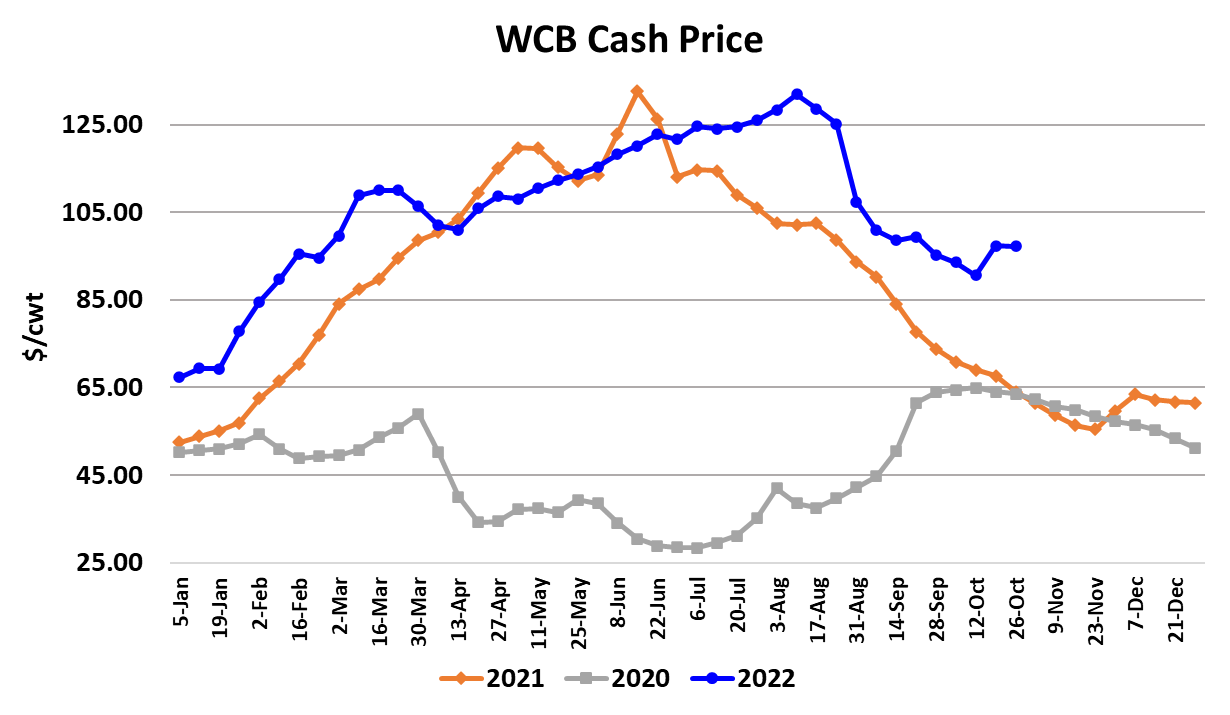

demand is the negotiated hog market. The WCB market

averaged $97.22 this week and was nearly steady with the week

before. I think the strength in the negotiated hog market is

simply a sign of the hog supply being too small for the available

processing capacity.

As a result, packer margins this fall are much narrower than in recent

years. This week’s margin is estimated at $9.86/head, well below the

$27/head that packers were realizing last year at this time when labor

constraints were reducing processing capacity. The Lean Hog Index

averaged over $94 this week and the cutout is just shy of $100, so it is

easy to see that margins are tight for this time of year. I think that is

going to continue and may get worse as we go into 2023 because

USDA’s surveys have been telling us that the hog herd is going to stay

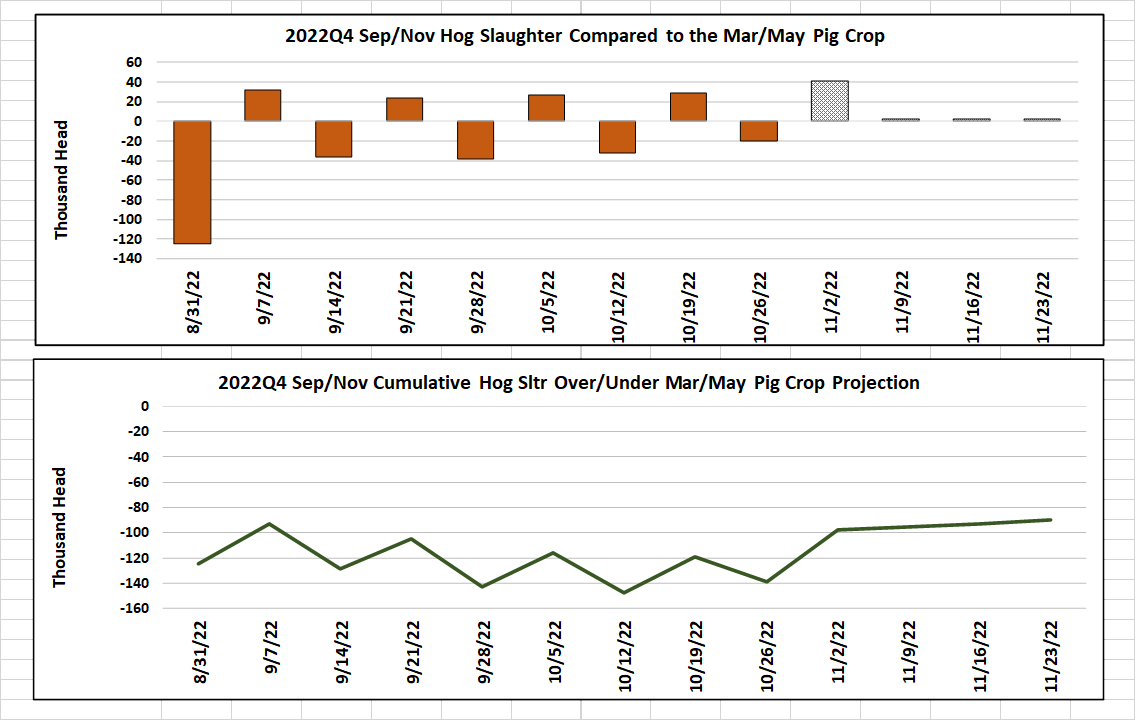

on a downward trajectory at least for another six months. This week’s kill

was reported at 2.56 million head and this was a “small Saturday” week

in the context of the oscillating weekend kills that are clearly visible on

pig crop implied chart.

Next week will be a big Saturday and we could even get the weekly kill

up to 2.61 million head, which should be the practical top this fall.

Except for Thanksgiving week, we should look for kills to hover in the

2.55 to 2.62 million head range until early December. By January, the

weekly kill should ease back into the 2.4-2.5 million head range. Hog

weights were steady this week, but they still could add 3-4 more pounds

before they hit their annual top. The DTDS weights continue to tell a

story of relatively current market hog supplies and that fits with the

strong pricing in the negotiated hog market. Producer margins are

about $17/head in the red right now and may reach -$35 or -$40 later in

December. Stubbornly high corn prices are gobbling up any benefit that

producers might have seen from high hog values. However, producers

are accustomed to losses of that magnitude near the end of the year

when hog supplies are near their peak.

They know that they will likely make it back in the summer when hog

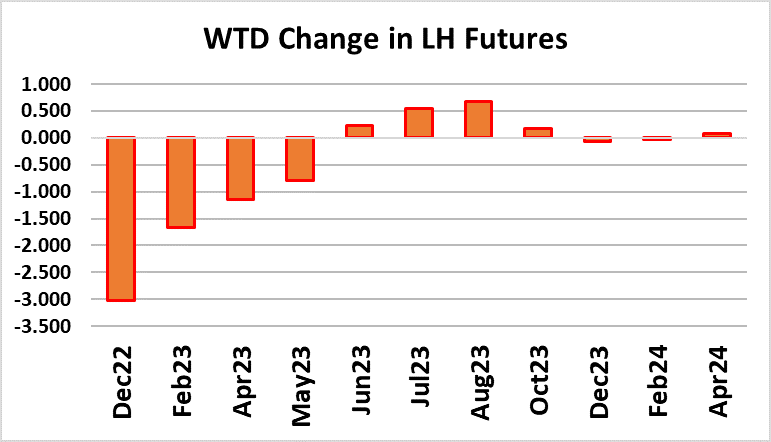

supplies tighten and hog prices soar. This week the nearby futures

made an abrupt turn lower on Thursday in response to the cutout

softening. On the week, Dec lost close to $3 but keep in mind that Dec

probably got a little overdone when it gained $7 the week before. As of

Friday’s close the Dec LH futures are sitting very close to what the

fundamental forecast says is fair value. They are in a comfortable spot

with little need to move much higher or much lower unless something

dramatic happens to the cutout next week. Of course, if packers

decided to slow the kill in order to improve margins, that could have a

material impact on both the cutout and hog prices, but my sense is that

they currently don’t have an appetite for that. If anything, they would like

to kill more, not less. Next week, watch the belly market to ascertain if

Friday’s bump has any staying power and keep an eye on the retail

primals since they seem to be the weakest link in the complex right now.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}