Pork Wrap October 27

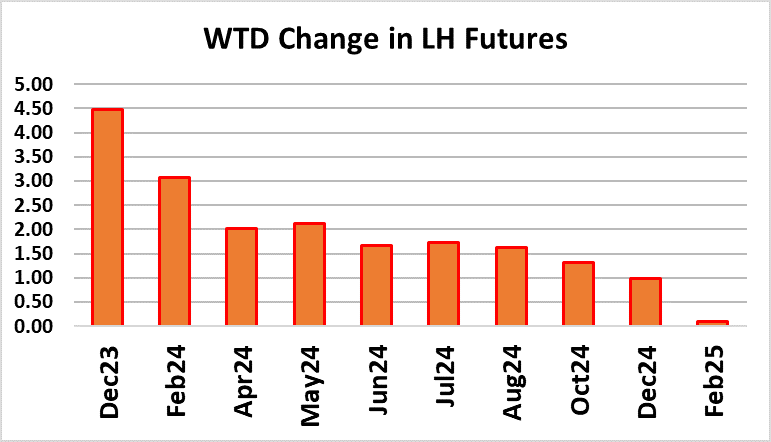

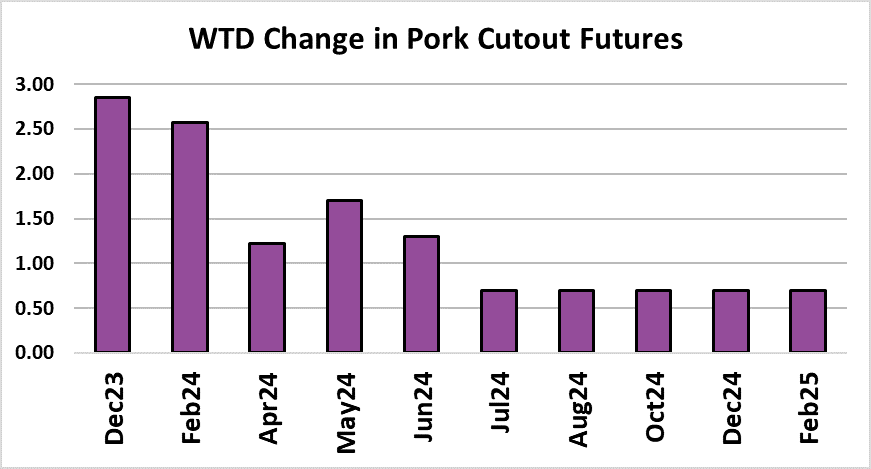

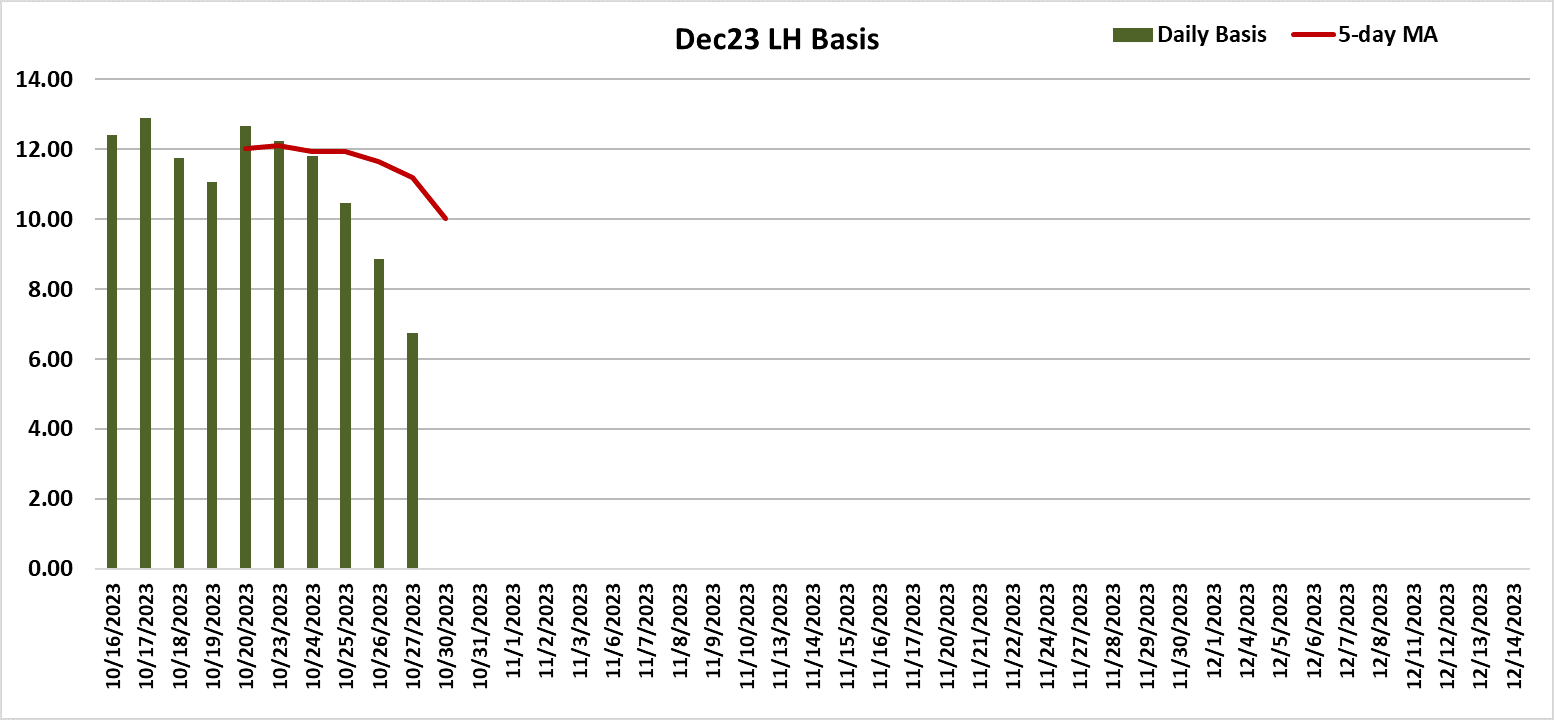

Compared to the cattle complex, the hog and pork complex was relatively sedate this week. The cutout drifted $1.79/cwt. lower on a weekly average basis and the WCB negotiated cash hog market averaged $1.12/cwt. lower. As a result, packer margins held pretty close to last week at $13/head. With production approaching its annual highs, both hog and pork prices are expected to remain under pressure, but the rate of decline should slow now that kills are very near their high point. In fact, there is a reasonable chance that by mid-to-late November prices will stabilize and may turn a bit higher heading into December. That thought must have crossed futures traders’ minds this week as they finally decided that the nearby Dec contract was carrying too much of a discount to the current cash market, given the slow pace of weekly price declines. The Dec contract settled above $70/cwt. on Friday—the highest close in nearly three weeks—and is now just a little over $6

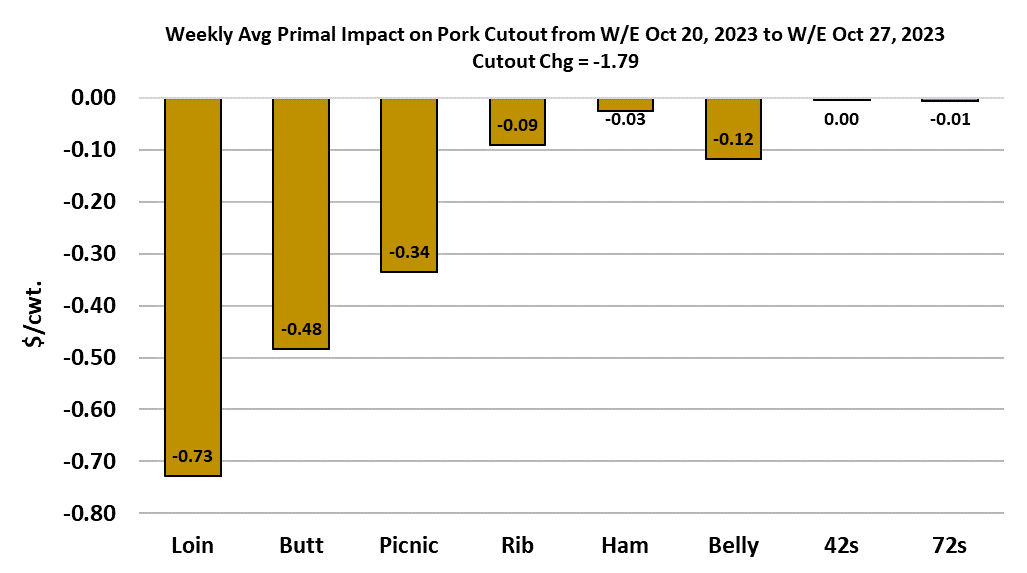

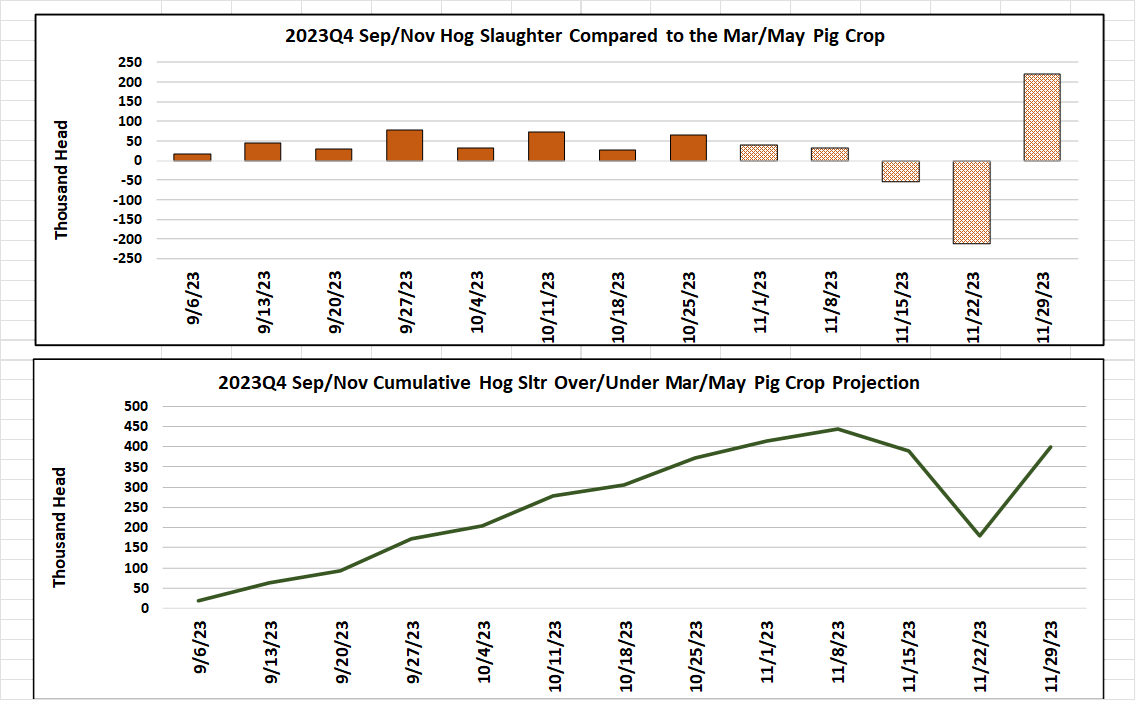

discount to the LHI. At the beginning of this week, Dec was $12 below the index, so that was a pretty significant narrowing of the basis. Finally, we had a week where the bellies and hams were not the primary items dragging the cutout lower. This week it was the retail items that helped the cutout lower, particularly the loin primal. It is starting to look like perhaps the hams and bellies might be carving out a bottom, but I’m not ready to call either substantially higher in the near term. Time is running out for holiday processing demand for the hams, so any additional demand improvement is likely going to have to come from the export market. There is a reasonable chance of that happening given that US ham prices are at their lowest level in months. If we do get some improvement in ham or belly prices, I’d expect the gains to be modest at best. USDA provided another look at cold storage inventories this week and the news was mostly positive. Total pork in cold storage was reported down slightly in September from August and is now almost 14% lower than last year. Belly and ham inventories both declined, indicating that users are still drawing down stocks and have not yet begun to build inventories. Some inventory build might be evident in the next cold storage report given the lower pricing structure that has been in place during October. In general however, it is good news that cold storage levels are running below last year because that was a huge hinderance to advancing prices during the winter and spring quarters a year ago. Overall pork demand still seems to be running soft and it doesn’t help that retail pork prices moved sharply higher in September. That said, the macroeconomy is doing better than expected and this week we learned that GDP in the third quarter advanced by almost 5% YOY. Consumers seem to still be spending with enthusiasm, even if more of those purchases are being financed with savings and credit. Export demand for US pork seems to be holding up fairly well from what we’ve seen in the weekly data and that is super important at this time of year when production is near its high point. If export demand were to stumble at this time of year, the negative price reaction would likely be swift. This week’s kill clocked in at 2.61 million head again this week and it is looking like next week’s kill may be a little stronger. The industry now appears to have overkilled the March/May pig crop by close to 350k head, which is a little less than one day’s slaughter. Fortunately, overall production isn’t much bigger than last year due to carcass weights running below last year. Barrow and gilt weights were reported up one pound this week to 209 pounds, but that was still about 1.4% below last year. By December, weights should be running close to last year. The DTDS weights are still very low and that suggests that producers are remaining current on their marketings and thus we probably don’t need to be concerned about hogs backing up this fall. In fact, it seems like packers are running the kill fairly hard relative to available supplies and that is why their margins are below average for this time of year. Below-normal margins are likely to be a persistent theme for the foreseeable future because producers are actively reducing breeding inventory and that means that hogs supplies will likely be smaller next year. With packing capacity expected to remain steady, packers will likely have to chase hogs a little harder next year than they did this year, resulting in some margin loss. For now however, the hog supply is sufficient and we should see some modest improvement in packer margins during November. Next week, expect more of the same—slowly declining hog and pork prices, big kills, and ample availability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}